Finding unique opportunities in Japan is a thematic we have been enthusiastic about consistently over the years. Japanese balance sheets have historically been less than optimal, with many companies holding excessive cash reserves instead of returning capital to shareholders. However, we anticipate a shift in this trend, making the market increasingly attractive. Japan’s reputation for high-quality hardware production is evolving as companies invest more in digital transformation and artificial intelligence (AI). Despite its lag in software development, Japan is now embracing the digital economy, spurred by government incentives and a strategic pivot towards balanced growth in hardware and software. This change, coupled with favourable valuations and a stable economic environment, underscores the significant investment potential within the Japanese market.

Japan and the Digital Economy

Japan has long been renowned for its exceptional production of high-quality hardware, establishing itself as a global leader in sectors such as consumer electronics, automotive manufacturing, and precision machinery. Household names like Sony Group Corporation (TYO: 6758), renowned for its cutting-edge electronics and entertainment systems; Toyota Motor Corporation (TYO: 7203), a pioneer in automotive innovation and hybrid technology; and Canon Inc (TYO: 7751), a leader in imaging and optical products, epitomise Japan’s engineering prowess. This expertise in hardware has been underpinned by a meticulous approach to engineering and a culture of relentless pursuit of perfection. However, despite these strengths, Japan’s digital economy has struggled with the integration and development of quality software. This lag is partly due to historical focus and investments predominantly channelled towards hardware innovation, coupled with a conservative corporate culture that has been slower to embrace agile software development methodologies and disruptive technologies. There are signs that this dynamic is beginning to shift, presenting new investment opportunities. With increasing recognition of the importance of software in driving future growth, Japanese companies are now investing more heavily in digital transformation initiatives and software development. The government is also actively promoting the digitisation of industries through policies and incentives designed to spur innovation. This pivot towards a more balanced emphasis on both hardware and software is expected to yield significant advancements in the digital economy.

The Japanese Market

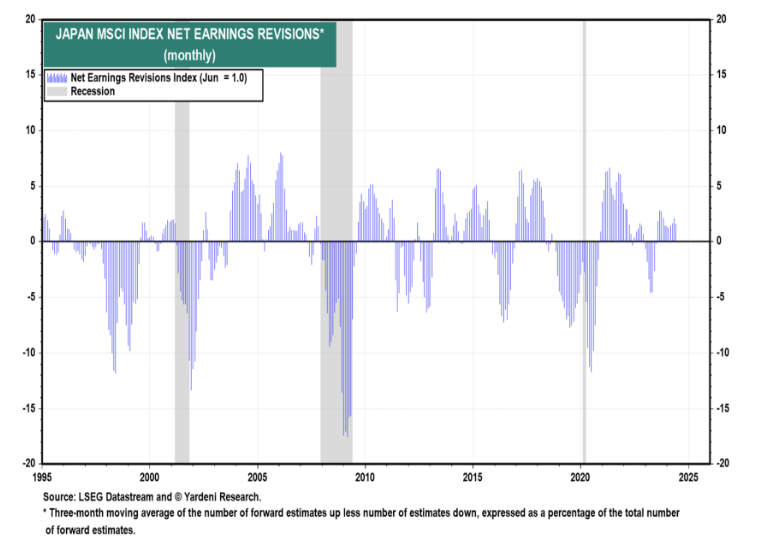

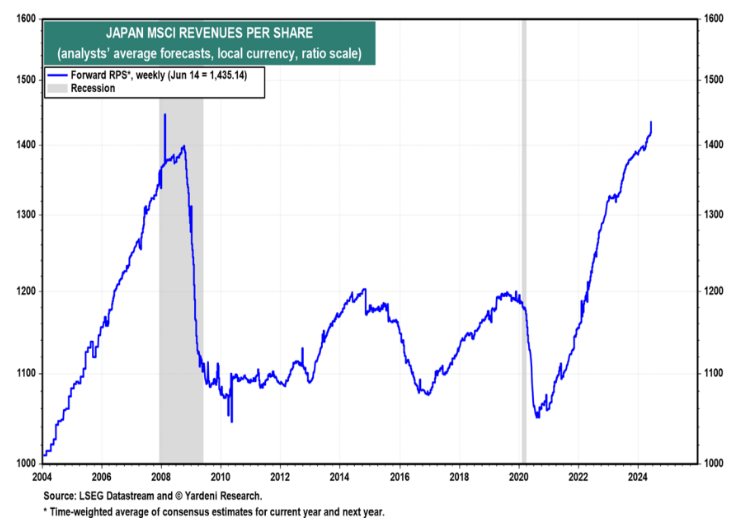

In our view the Japanese share market generally remains attractive. Valuations in Japan appear cheaper when compared to the United States, with lower price-to-earnings ratios signalling a potential for value investment. Business conditions are favourable, buoyed by strong industrial output and a stable economic environment. Furthermore, corporate earnings revisions in Japan have generally been on an upward trajectory, reflecting improving profitability and operational efficiencies among Japanese company’s. Notably, revenue per share of Japanese companies is growing nicely and has recovered compared to previous years. As an investor, you are buying into a market with substantial change, which remains quite cheap and attractive. The Japanese market had a great year last year and a strong first quarter before a recent pullback, suggesting there could be a significant opportunity here.

The Opportunity

As a result of the recent pull back, the TAMIM Global High Conviction team has revisited a number of Japanese businesses. One of these investments is Advantest Corporation (TSE:6857). Advantest stands out as an attractive investment opportunity within Japan, particularly for those seeking exposure to the “picks and shovels” play in the burgeoning fields of AI and semiconductors. Advantest has established itself as a global leader in semiconductor and component test systems, manufacturing automatic test and measurement equipment used in the design and production of semiconductors for applications including 5G communications, the Internet of Things (IoT), autonomous vehicles, high-performance computing (HPC), including AI and machine learning, and more. The company’s comprehensive product portfolio includes SoC test systems, memory test systems, and system-level test solutions, which are critical for the development and production of advanced semiconductor devices. Advantest’s strategic positioning in the semiconductor industry is further bolstered by its commitment to innovation and technological advancement. The recent launch of the DC Scale XHC32 power supply, designed to meet the rising power requirements for AI and HPC devices, exemplifies its forward-thinking approach. Additionally, the company’s global footprint, with operations across the Americas, Asia, and Europe, ensures a broad market reach and diversified revenue streams Over the long term Advantest has performed very well with a strong return for shareholders. The recent share price pullback is one we see as an opportunity to capitalise upon.

The TAMIM Takeaway

We continue to believe that the Japanese market offers a unique and compelling investment. As the country continues to bridge the gap in its digital economy, the integration of superior software capabilities with its world-class hardware production could unlock significant growth potential, making it a market to watch closely for both traditional and software-focused investments. We continue to believe that now is an opportune time to consider investing in Japan, leveraging the anticipated corporate reforms and technological advancements that promise to drive long-term profitability and growth. ____________________________________________________________________________________________________________________________ Disclaimer:Canon Inc (TYO: 7751) and Advantest Corporation (TSE: 6857) are currently held in TAMIM Portfolios.

This week’s reading and viewing list covers The Clean Industrial Revolution has arrived, Nvidia Is No Cisco, but It Is Getting Expensive, and Meet the Highest Paid CFOs of 2023.

📚 Wall Street’s favorite strategist discusses how to be a better investor(Joseph Adinolfi)

📚 Nvidia Is No Cisco, but It Is Getting Expensive(Dan Gallagher)

While selling at a loss to offset other gains is the obvious benefit, tax loss selling may provide additional opportunities for patient investors.

Tax-loss selling is a strategy where investors sell underperforming stocks at a loss to offset capital gains from profitable investments, thereby reducing their overall tax liability. Investors employ this strategy to minimise the taxes owed on their net capital gains for the year. It becomes popular towards the end of the financial year when investors review their portfolios and look to optimise their tax positions.

However, tax-loss selling can potentially lead to quality companies becoming oversold during difficult periods.

When investors indiscriminately sell losing stocks solely for tax purposes, it can create excessive selling pressure and drive down the share prices of fundamentally sound companies that may be going through temporary challenges. This overselling can present opportunities for investors to buy into quality businesses at discounted prices, but it also highlights the risk of prematurely exiting positions based solely on tax considerations rather than the company’s long-term prospects.

We take a look at some of the ASX companies that we believe may be suffering from tax loss selling.

Close the Loop

Close the Loop (ASX: CLG) is a global player in sustainable solutions, operating across Australia, Europe, South Africa, and the United States which we’ve covered in depth here.

The innovative company specialises in creating eco-friendly products and packaging with a strong emphasis on recyclable and recycled materials. Furthermore, Close the Loop plays a pivotal role in resource management by collecting, sorting, reclaiming, and reusing materials that would otherwise end up in landfills. The company’s expertise spans a wide spectrum of sectors, including electronics, print consumables, eyewear, cosmetics, plastics, paper, and cartons.

With 52 week highs of $0.50 the company’s share price has been languishing in the low 30’s.

So why should shareholders be bullish?

Close the Loop is well-positioned to benefit from the growing global shift towards a circular economy and increased recycling of products and materials. Major companies like HP, one of Close the Loop’s key customers, have ambitious targets to significantly increase circularity and use of recycled materials in their products by 2030. This suggests substantial volume growth potential for Close the Loop’s services.

Moreover, the company’s financials are outperforming expectations. In the first half of FY24, Close the Loop reported strong revenue growth of 76%, with even higher increases in gross profit (94%), operating earnings (139%), and underlying net profit before tax (204%). The company is also improving its balance sheet by reducing debt.

With what we feel is an attractive valuation, Close the Loop’s growth runway and financial performance provide reasons for shareholder optimism despite recent share price declines.

Corporate Travel Management

Corporate Travel Management (ASX: CTM) is a leading provider of travel management solutions for corporate customers globally.

CTM’s share price experienced a significant decline in February 2024, despite reporting a 162% increase in underlying net profit and tripling statutory net profit for the first half of FY24. This sharp drop was attributed to the company lowering its full-year guidance, citing a $40 million operating earnings headwind from macroeconomic issues and underperformance of its UK Bridging contract, factors beyond its control.

The initial sell-off slowed but has extended in recent weeks with shares trading around 52-week lows below $13.

However, CTM unveiled a five-year growth strategy aimed at doubling FY24 profits organically by FY29. The key pillars of this strategy include:

1) Revenue growth over 10% annually from winning new clients;

2) 97% annual client retention;

3) Productivity and innovation gains;

4) EBITDA growth outpacing revenue growth, with 50% of new revenue falling to EBITDA;

5) Acquisitions providing additional growth on top of organic goals.

Notably, key metrics like client wins, retention, and revenue per employee are already meeting or exceeding targets.

Despite the short-term challenges, shareholders could be optimistic about a turnaround. The headwinds are considered temporary, while underlying performance remains strong, with January results rebounding strongly across regions. Crucially, CTM is well-positioned to execute its growth strategy, having a proven track record in acquisitions and synergy extraction, positioning it well for likely industry consolidation. Even with the headwinds, underlying operating earnings guidance still represents 31.7% growth over FY23 at the midpoint.

Tabcorp Holdings

Tabcorp Holdings Ltd (ASX: TAH) is Australia’s largest gambling company, operating a portfolio of leading brands in wagering, media, and gaming services.

The company has struggled in recent times, with revenue for the first half of the fiscal year dropping 5% compared to the corresponding period, primarily due to weakening in the wagering segment. Group operating earnings fell 14% to $170 million, while Group earnings before interest and tax (EBIT) declined 32% to $50 million. Tabcorp also took a significant impairment charge of $731.9 million after tax to the Wagering and Media business, attributing the recent weakness to difficult macroeconomic conditions and a return to a more normal market following high growth during the COVID-19 period.

Despite these challenges, we feel Tabcorp may be an attractive takeover candidate for major international players.

With the potential exit of online competitors due to increased taxes and advertising restrictions, Tabcorp’s leading Australian brands, national scale, and reach could position it strategically in the evolving landscape.

However, investing in Tabcorp may be risky, its share price graph resembling a double black diamond ski slope—steep and treacherous and it may be best left only for brave investors.

The TAMIM Takeaway

While tax loss selling can create opportunities to buy quality companies at discounted prices, investors should be wary of indiscriminately selling underperformers solely for tax purposes.

A long-term view on a company’s fundamentals and prospects is crucial. The examples highlighted above show how short-term challenges and tax loss selling pressure can potentially obscure the underlying strengths of a business. Investors with patience and a keen eye for value may find attractive entry points in fundamentally sound companies experiencing excessive selling. However, thorough research is essential to separate temporary setbacks from deeper structural issues.

By looking beyond the tax loss selling noise, disciplined investors can potentially uncover promising opportunities to generate substantial returns over the long run.

Disclaimer: Tabcorp Holdings Ltd (ASX: TAH) and Close the Loop (ASX: CLG) are held in TAMIM Portfolios as at date of article publication. Holdings can change substantially at any given time.

While markets and investors are often captivated by sectors promising rapid growth and technological advancements, there are times when strategic investments in more stable sectors can offer “defence” against economic downturns.

One such sector is Defence, where substantial government spending provides a consistent revenue stream. The United States continues to allocate enormous sums to defence, and recently, the Australian government has also flagged the need for significant investment in its forces and capabilities over the coming decade.

This sector not only includes established giants with sustainable business models but also hidden gems that can surge by supplying innovative solutions.

The Defence Sector: Stability in Uncertain Times

The defence sector is uniquely positioned to provide stability and growth, even during economic downturns. Government spending on defence remains robust, driven by the need to maintain national security and technological superiority. This creates a reliable revenue stream for companies operating within this sector. Additionally, long-term contracts and government budgets often insulate Defense companies from the economic volatility that affects other sectors.

Lesser Known Players in the U.S. Defense Sector

RTX Corporation

RTX Corporation (NYSE: RTX) (formerly known as Raytheon Technologies Corp.) is a leading aerospace and defence company that provides advanced systems and services for commercial, military, and government customers worldwide. The company operates through four principal business segments: Collins Aerospace Systems, Pratt & Whitney, Raytheon Intelligence & Space, and Raytheon Missiles & Defense.

The company delivered an impressive Q1 2024 earnings report, with sales of $19 billion, a 12% increase from Q1 2023, and earnings growth of 32% year-over-year.

RTX’s defence contractor division, Raytheon, reported significant classified bookings, as well as $1.2 billion worth of Patriot anti-air defence systems and $282 million of National Advanced Surface-to-Air Missile Systems delivered to Ukraine. RTX’s civilian divisions, Collins Aerospace and Pratt & Whitney, also outperformed, with Collins Aerospace experiencing a 9% sales increase and Pratt & Whitney reporting a 23% year-over-year sales growth. The company’s 2024 financial guidance anticipates a total sales growth of 14% and potential earnings of over $5.25 per share. The recent strong performance is reflected in the share price with a 13% return over the past three months. As a fundamentally defensive play in the current market environment, RTX offers exposure to growing defence spending in Europe and a strong commercial aerospace business.

The company’s diversified portfolio ensures a stable revenue stream across multiple defence and aerospace domains.

Leidos Holdings, Inc.

Leidos Holdings, Inc. (NYSE: LDOS) is a leading provider of information technology, engineering, and science solutions to the U.S. government, state and local agencies, and commercial markets. The company operates through four segments.

Leidos reported a strong result for the first quarter of fiscal 2024.

Revenues increased 7% year-over-year to US $4.0 billion, driven by strong program execution and strategic acquisitions. Net income grew to $283 million or $2.07 per diluted share, up from $164 million Q1 2023. Adjusted earnings per share climbed 56% to $2.29, while the adjusted operating earnings margin expanded to 12.3% from 9.4% a year ago. The company generated an operating cash flow of $63 million and non-GAAP free cash flow of $46 million. With a solid backlog and book-to-bill ratio, Leidos is well-positioned to capitalise on growing defence and government spending.

The company was recently awarded a US $738 million contract by the U.S. Air Force to provide enterprise IT and telecommunications support, including cybersecurity, to various Air Force and Space Force headquarters and activities in the national capital region.

The contract, which includes a one-year base period and multiple options extending up to five and a half years, will see Leidos deliver critical services such as cybersecurity, IT operations, and program management. Steve Hull, Leidos’ digital modernisation sector president, emphasised their commitment to advancing the Air Force mission with secure, resilient technology solutions, building on over five decades of continuous support.

Leidos’ extensive expertise across various sectors positions it well to leverage government contracts and provide innovative solutions.

Promising Players in the Australian Defense Sector

DroneShield

DroneShield Ltd (ASX: DRO) is a leading provider of counter-drone (C-UAS) and multi-mission unmanned systems (C-UxS) solutions.The company uses artificial intelligence and machine learning to deliver advanced technologies for military, government, and commercial organisations in over 70 countries. DroneShield’s product portfolio includes fixed-site, mobile, and handheld systems for detecting, tracking, and defeating drones. Their solutions integrate multiple sensors and effectors, offering a comprehensive layered defence against drone threats.In the most recent quarterly report, DroneShield reported incredible financial results for the first quarter of 2024, with revenue growing 10 times year-over-year and a significant increase in order intake.

The company has also expanded its global footprint, securing major contracts with military and government agencies, particularly in the US. Over the past 12 months, DroneShield’s share price has rocketed, reflecting the growing demand for counter-drone solutions and the company’s successful execution of its strategic initiatives.

As the threat of drone-related incidents continues to rise, DroneShield is well-positioned to capitalise on the increasing need for effective counter-drone technologies.

Codan

Codan Limited (ASX: CDA) is an international company founded in 1959 that develops rugged and reliable electronics solutions for government, corporate, non-government organisations (NGO) and consumer markets across the globe.

The company’s communications segment produces equipment used by military, law enforcement, humanitarian, and commercial organisations known for reliability and performance in harsh environments, making them ideal for defence applications. Codan’s focus on innovation and quality ensures it remains a trusted supplier in the defence communications market. The company’s technologies also include metal detection, and it has a global network of dealers, distributors and agents that allow it to deliver solutions worldwide.

The company delivered a strong H1 FY24 result, with group revenue up 26% to $265.9 million and net profit after tax increasing 24% to $38.1 million compared to the prior corresponding period. The Communications segment achieved 12.5% revenue growth, while Metal Detection revenues surged 49%. Despite higher expenses due to acquisitions and investments, Earnings Before Interest & Tax (EBIT) and Net Profit After Tax (NPAT) grew 31% and 24% respectively. Net debt increased to $82.5 million after funding $30.3 million for the Eagle and Wave Central acquisitions. Looking ahead, Codan expects Communications revenue growth to exceed the top end of its 10-15% target range.

Codan’s focus on innovation and quality ensures that it remains a trusted supplier in the defence communications market.

The TAMIM Takeaway

The sector is driven by substantial government spending and innovative solutions catering to evolving defence needs providing market resilience. While some will initially look to increased expenditure as a result of ongoing conflict, a second-level thinking approach looks to the sector’s ability to adapt through technological advancements and market expansion, positioning companies at the forefront of research and development for significant growth.

By recognising these dynamics, investors can uncover quality businesses with strong tailwinds poised to thrive in the coming decade.

This week’s reading and viewing list covers EV Maker Fisker Files for Bankruptcy After Its Glitchy SUV Flops, The Apple-OpenAI “Deal”, Japan and the App Store, Apple’s AI Developer Risk and Google partners with Nevada utility for geothermal to power data centers.

Japan’s reputation for high-quality hardware production is evolving as companies invest more in digital transformation and artificial intelligence (AI). Despite its lag in software development, Japan is now embracing the digital economy, spurred by government incentives and a strategic pivot towards balanced growth in hardware and software. This change, coupled with favourable valuations and a stable economic environment, underscores the significant investment potential within the Japanese market.

Japan’s reputation for high-quality hardware production is evolving as companies invest more in digital transformation and artificial intelligence (AI). Despite its lag in software development, Japan is now embracing the digital economy, spurred by government incentives and a strategic pivot towards balanced growth in hardware and software. This change, coupled with favourable valuations and a stable economic environment, underscores the significant investment potential within the Japanese market. Notably, revenue per share of Japanese companies is growing nicely and has recovered compared to previous years.

Notably, revenue per share of Japanese companies is growing nicely and has recovered compared to previous years.  As an investor, you are buying into a market with substantial change, which remains quite cheap and attractive. The Japanese market had a great year last year and a strong first quarter before a recent pullback, suggesting there could be a significant opportunity here.

As an investor, you are buying into a market with substantial change, which remains quite cheap and attractive. The Japanese market had a great year last year and a strong first quarter before a recent pullback, suggesting there could be a significant opportunity here.