Sid Ruttala continues his exploration of the top end of the market, this time moving just past the surface of the ASX and going outside the Top Ten. This week we look at Macquarie Group (MQG), Telstra Corporation (TLS) and Rio Tinto (RIO).

Author: Sid Ruttala

This week we continuing publishing my notes on individual companies. At the beginning of this particular series, we were going to limit ourselves to the Top Ten but due to significant interest from readers, we’ve decided to continue down the list by market capitalization. Next on the list for this week are: Macquarie Group (MQG), Telstra Corporation (TLS) and Rio Tinto (RIO).

MQG is one security that held up relatively well through the Covid selloff, the twelve-month number coming in at -8.3%, a stellar achievement given the performance of financials on the ASX broadly. Numbers-wise, overall operating income was down -3% for FY2020, to $12.3bn AUD, with profit coming in at $2.7bn AUD, an 8% decline on the previous year. The more important metric in my opinion was the EPS. At $7.91 AUD per share, it represents a 10% decline from the previous year.

Breaking it down by division, MAM (Asset Management) and CGM (Commodities & Global Markets) were the performers in terms of income. The Asset Management division printed higher than expected (my expectations at least) management and performance fees, while commodities and global markets have held up relatively well with particularly higher business in the commodities lending business (thank you, iron ore). As expected MacCap has seen lower DCM (Debt Capital Markets) revenue partially offset by M&A activities and, for the foreseeable future, this will be the silver-lining if management continues to get themselves onto deals which we can certainly expect (given their track record).

Looking to the future, recent HY21 guidance suggests that NPAT will be down 35% YoY. Management has taken a conservative and prudent approach by increasing provisioning for Covid-19. Also problematic is the higher Australian Dollar, given that 69% of MQG’s income is now global. Numbers-wise, a 5% swing in the spot rate will result in a 3.5% swing in the NPAT (either way). For the number-crunchers among you, happy to share the TWI (Trade Weighted Index) calculations.

Red Flags & Risks: The biggest risk comes from Covid. One saviour for Macquarie Capital has been M&A activity and unless we see a marked improvement in the overall economy we will continue to see stress (including increased provisioning) across BFS (Banking and Financial Services). There is downward pressure on EPS and management will need to be diligent in increasing AUM for MAM in order to circumvent these headwinds. On the upside, however, the continued decline in AUM for AMP has meant that it has been receiving flows (including to its Macquarie Wrap platform). The key will be reaching enough scale in terms of inflows to offset the margins on the annuities like business (i.e. infrastructure and green assets).

My Expectations: A fair substitute for the Big Four. Messy short-term outlook with headwinds across the investment divisions and likely increases to provisioning going forward. We will see increased M&A activity but it will probably not be big enough to offset the declines across DCM. The Asset Management division is likely to be the knight in shining armour given the illiquidity and stickiness of the underlying assets, including renewables and infrastructure. That said, the business has a proven track-record of close to 51 years of profitability, one can probably trust that track record. A long-term hold.

Dividend Yield: The current dividend yield stands at an exceptional 3.6%, assuming a price of $118.69 AUD.

Though on a nominal basis we don’t expect this to stay put through the next FY due to increased provisioning and short-term declines in NPAT. Over the long run, we expect the company to maintain a consistent payout ratio (above 50%).

Telstra Corporation (TLS.ASX)

Telstra is one Australian company that never ceases to disappoint. Every time it starts to look cheap, it surprises investors by getting even cheaper (eventually it becomes a habit). With that in mind, I can’t say I was overly surprised by a rather disappointing FY20 result. NPAT was down 12.6% to $1.8bn AUD with the biggest declines by segment across Fixed (-11%) and, more concerningly, Mobile (-4.4%). Greater than expected decline, in my opinion, in ARPU (Average Revenue per User) even factoring in less roaming charges (i.e. no international travel). What was more disheartening was the DATA and IP segment declining close to 13% due to increased competition. This is while we live in a Covid world where consumers don’t do much other than use the internet; everything was online for at least a few months there.

On the positive side, the one bright spot is the value (longer-term) of its infrastructure with close $1bn p.a. in recurring payments from NBN. InfraCo has a lot of untapped potential and should create a buffer for the company.

Much will be contingent on management. One trend we have seen is that TLS has taken the lead in raising prices higher, especially 5G, and others will likely follow suit. Until now the play has been to increase usership at all costs, but a rationalisation might be in order. Especially targeting premium customers and increasing margins per customer. Its main competitors, Optus and TPG, are also likely to follow suit with TPG also indicating that its discounts are not going to become a permanent fixture. The accelerated digitisation as a result of Covid could become a tailwind for the largest telco in the country (though they do have a track record of not taking advantage of such things…).

Red Flags & Risks: Simply put, competition is the biggest risk for the company. Until now, telecommunications has been a race to the bottom (granted, beneficial for the consumer). What we are likely to see is a consolidation and rationalisation, with market shares becoming stable. TLS will have to focus less on the acquisition of customers and more on the monetisation of its existing infrastructure and user base.

What has been frustrating to watch has been the lack of willingness to look at alternative revenues and diversifying the business. It took the company until last year to even think about rationalising its product line. Looking at their global counterparts in the States, AT&T acquired Time Warner, Verizon made multiple acquisitions across cloud security and more recently drone tech company Skyward, and Singtel (Optus) is buying up broadcast rights to sports left, right and center. It will be key for TLS to move into the 21st century and shake off its public sector roots. Vision 2022, which includes a move to digital and IoT, at this stage remains all flash and no fire. They’ve talked the talk, time to walk the walk.

My Expectations: While at current valuations it does look cheap, especially when one considers the true value of its infrastructure assets, there is too much up in the air and it relies on flawless execution by management. Even with regards to InfraCo, there has been no clear outline of how it will be monetised.

The company needs to modernise, ARPU will get higher but this is probably contingent on international travel being opened up again. One thing I did like was the Capex brought forward despite Covid,

Personally, I am a fan of Andy Penn but he is fighting an uphill battle. If you hadn’t picked up on it by now, to put it bluntly, still not a buy for me.

Dividend Yield: The current dividend yield stands at an exceptional 5.7% assuming a price of $2.82 AUD.

On a nominal basis we expect this to stay put, though the yield might keep going higher if past performance is anything to go by.

Rio Tinto (RIO.ASX)

Before getting onto the recent events that culminated in the ousting of CEO Jean-Sebastian Jacque and several other top executives, let’s go through the numbers. The company has certainly put out some stellar results buoyed by iron ore prices, NPAT was at $4.8bn USD while EPS was at $2.94 USD per share which represents a slight decline of -3%, a positive given the environment. What is immediately evident was that the impact on the firm from Covid was minimal, only showing up in terms of slightly lower cash conversion.

Division and commodities wise, iron ore was, as expected, the outperformer. What was rather surprising to me was the aluminium and bauxite numbers, driven primarily by prudent cost management and margins despite the prices tumbling. Corporate cost cuts were also evident across Escondida. Projects-wise and in terms of growth catalysts, fieldwork across the assets in Guinea is to commence this year, despite my expectations of it being pushed into next year (another positive). The Oyu Tolgoi copper/gold project has been facing some hurdles in terms of a slower than expected ramp-up (this one is a negative).

It was exciting to see the maiden resource for the Winu project coming in at 500m tonnes at a grade of 0.45% CuEq (copper equivalent), Australia’s newest tier-1 project. Though still in its infancy this could be the next catalyst for Rio, especially given the likely upward trajectory in Copper spot prices.

Red Flags & Risks: The biggest risks currently are related to the uncertainty around management going forward. Whatever the market may say about the previous CEO, he has been interesting for shareholders from a pure numbers perspective, putting steady dividends into our pockets. That being said, the rather blasé attitude to corporate and social responsibility has done some irreparable damage to the company’s brand. Blowing up a 46,000-year-old site of immense cultural importance and then trying to assume plausible deniability in a parliamentary inquiry will do that. You would hope they have learned their lesson.

Scalps have been taken. These include the CEO, the Head of Iron Ore division and the group executive for corporate relations, all by mutual consent of course. Though the consent did cost a tidy $80m AUD. The new CEO, whoever that might be, faces a decent challenge. This includes but is not limited to dealing with the Mongolian government in putting the Oyu Tolgoi copper mine in order and ramping up production, hitting the ground running with the Guinea assets (i.e. Simandou Iron Ore project) and placating a wide group of rather aggrieved stakeholders due to the aforementioned PR disaster.

Risks also include project execution and keeping Capex in line, to meet the expectations of now rather spoilt shareholders (this will include the Oyu Tolgoi, Amrun and Koodaideri projects).

Currency wise, Rio’s revenues are inversely correlated to the AUD and a higher AUD will create a rather messy P&L.

My Expectations: I tend to be contrarian when it comes to the price of iron ore, though many have said it is toppy, and my expectation is that, while volatile, there are catalysts that will apply upward pressure in the medium to long-term, including higher infrastructure spending around the planet. Copper will remain an interesting buffer for the company and Winu creates the potential for stellar upside.

That said, there is a lot of uncertainty concerning the leadership of the company and what this means for the existing strategy, including the cost-cutting measures. Simply put, environmental and ethical concerns aside, a great business. I would hold if I already owned but wouldn’t be adding to the position with great conviction.

Dividend Yield: The current dividend yield stands at an exceptional 5.9% (approx.) assuming a price of $103.740 AUD.

On a nominal basis we expect this to stay put with potential upside on the underlying security if management gets its act together and doesn’t decide to ignite a museum or look for ore under the Pyramids.

Firstly, credit where it’s due, the CEO (Elizabeth Gaines) has done a stellar job in turning around the business, cutting debt and costs. From a numbers perspective, a record EBITDA of $8.38bn USD ($10.99bn AUD) and NPAT of $4.25bn USD ($5.85bn AUD). More importantly, the free cash flow continued to grow in double digits. From a yield perspective, the company’s 100c p/s was certainly above the market expectations and represents a 77% payout ratio.

In terms of capex and additional projects, the two majors in the pipeline are Eliwana and Ironbridge. This is in addition to Pilbara Energy Connect which aims to decrease the firm’s carbon footprint by investing in hybrid solar-gas transmission infrastructure. Currently, capex stands at approximately $1.96bn USD for 2020 with guidance of $3.4bn USD in 2021. Although this does represent a substantial increase, it puts the company in a strong position for the future with my expectations being a substantial decrease (i.e. 50-60%) post-2021.

Red Flags & Risks: The biggest red flag is the current share price at $18.25 AUD per share, this represents a substantial premium to NAV and even small fluctuations in the price of ore could lead to amplified downside risk from a valuation perspective. That said, from a cost-discipline and management perspective, I could not find fault (not for lack of trying). The biggest metrics to watch going forward will be steel production in China (and thus the trade relationship that underpins it) and the infrastructure pipeline both domestically and abroad. We would guess that there will be a fair amount of infrastructure spending in the coming years given the need for stimulus globally.

My Expectations: Personally, I remain bullish about iron-ore spot prices, even with the possibility of Brazil coming back online, due to the amount of fiscal stimulus that is being touted across the planet as mentioned above. This is pure-play on exposure to that growth trend. Though the security remains overvalued from a historic perspective, Fortescue is one great Australian business that fits well into a portfolio despite the downside risk (mainly due to the substantial run in the share price).

Dividend Yield: The current dividend yield stands at an exceptional 9.6% assuming a price of $18.37 AUD.

On a nominal basis we don’t expect this to stay put through the next FY due to the upcoming elevated capex. Over the long run, we expect the company to maintain a consistent payout ratio (above 70%).

Woolworths (WOW.ASX)

Not surprisingly, Woolworths was one security that effectively behaved as a hedge during the Covid-19 market sell-off. That being said, it remained consistently volatile calendar year to date, the share price returning 2.29% since January. Amidst the lockdowns and stay at home trends, there has been a spike in home consumption increasing the volumes but reducing the frequency (i.e. large bulk orders and less frequency in orders).

This is one security that has been on my radar ever since Amazon’s entry into the market in 2017. Despite the doom-and-gloom type hype associated with the move, WOW has been adapting and growing it’s business consistently. Online sales growth came in at 69%, a stellar result that equated to 100% of the sales growth which stood at 8.1%. Normalised EBIT came in at 8.8% (assuming the exclusion of the hotels since this was an exogenous event, we would exclude this particular metric in assessing management). Australian Food continues to grow in the high single digits with the NZ business growing at a double-digit rate.

What has been pleasantly surprising was the inventory turnover which was pushed down to 37 days and indicates that management has been forecasting in a reasonable manner. The lower than expected capex was surprising and, though taken well by shareholders, is not a positive (in this author’s opinion at least).

Red Flags & Risks: Management seems to be disciplined when it comes to cost management and balance sheet discipline but there is uncertainty around the divestment of Endeavour and the profitability of same-store sales. If the Endeavour divestment is done at a reasonable valuation, it could put some cash in the pockets of shareholders though. Big W somewhat surprisingly beat my expectations, though I believe it would be better off sold rather than remaining a part of the broader group.

The competition from pure-play online retailers could put downward pressure on profit margins (including price deflation). The competition could also come in the form of convenience stores. The key will again be in the delivery, turning existing stores into effective distribution centers (DCs). What caught my eye in this instance was the partnerships with Sherpa, Uber and Drive Yellow for last-mile delivery, a problem that remains the single biggest headache for retailers both in Australia and globally.

Woolworths Fairfield Heights, a TAMIM property

My Expectations: Not a growth play but rather a play on the balance sheet (bottom line as opposed to top-line). Much will be dependent on continuing to increase inventory turnover, reinvestment in IT and last-mile delivery. The business’s competitive advantage could also come from regional areas where existing store-presence gives them a head-start on online retailers (i.e. stores as DCs). The divestment of Big W along with Endeavour would make the business much more manageable and focused in my view.

Dividend Yield: The current yield stands at 2.5% assuming a share price of $37 AUD.

This is likely to stay consistent at around $1 AUD per share (give or take 0.2c) for the foreseeable future as the business continues to reinvest in order to keep up with competition and margin pressure.

Transurban (TCL.ASX)

Transurban is one company that sits on the frontline for the Covid economy and not in a good way. Government lockdowns and policy responses have meant that all major markets have been impacted including Montreal, Melbourne, Sydney and to a greater extent Washington. Numbers-wise, EBITDA stood at $1.89bn AUD, representing a decrease of 6%, while revenues were down approximately 3%, coming in at $2.492bn AUD. Of this, the North American operations represented a less than stellar figure of $154m AUD. Traffic restrictions across key regions, including Melbourne, are likely to take a further toll on the company. July traffic declined more than 25% in fact with the biggest negative coming from Citylink being down close to -48%.

That said, while the current situation does seem rather gloomy, TCL remains relatively well-capitalised though debt and gearing has continued to increase to 35%. What is more interesting is the pipeline of additional projects, the more attractive of these being the M6 extension, M12 Motorway, in Washington (with the announcement of the Capital Beltway Accord) and Montreal set for a toll increase of 14% (A25).

Red Flags & Risks: Much of the businesses immediate future will be contingent upon the whims and vagaries of government policy as well as economic conditions, mostly Covid-19 related. What was been surprising is the resilience of commercial and large trucking haulage. It will be incumbent upon management to win additional business in North America where the groups best prospects for sustained growth are likely to come. From a macroeconomic perspective, the business depends upon the urbanisation of populations which, from a long-term secular growth perspective, could start to decline or at the very least slow somewhat as a result of the pandemic. We have seen signs, especially in North America and to a lesser extent Australia, of a move out of the city for opportunities in regional or suburban areas or, in a pandemic-accelerated trend, even the same opportunities but with the option to work from home. For those interested please feel free to look at the dislocations in the San Francisco property market, with increasing movements of populations away from the main city.

In the shorter term, the bigger concern for me was the slight but still telling increase in costs, of 2.3%, despite the fall in earnings. I would have liked to see this remain flat.

My Expectations: The business will focus on expanding its North American footprint going forward, especially with the likelihood of fiscal stimulus being directed toward the upgrading of existing infrastructure as well as build out of new projects. Similar trends are likely in Australia as governments are forced to stimulate growth. TCL, while currently seeing some short-term pain, will benefit substantially from these catalysts as long as they win net-new contracts. Management does have a proven and consistent track record when it comes to this.

Earnings growth will remain less than stellar in the short-run unless we see traffic levels revert to something near pre-covid levels, which in my opinion may take longer (at least eighteen months) than many seem to expect. Over the medium-to-long run, given the likely additional infrastructure pipelines across all the geographies that the group operates, there are catalysts in the form of net-new wins or contracts. So, for the more patient long-term investors it might pay to stay invested as long as the expectation is not for a quick turnaround.

Dividend Yield: 3.6% assuming a share price of $13.97 AUD.

I expect the payout ratio to be consistent and the nominal dividend to remain around 50c p/s for the foreseeable future. Over the long-run (I’m talking 3+ years) I would expect to see this grow in the mid-to-high single digits. This is based on my assumption that traffic volumes won’t return to a normal or pre-covid level for at least the next eighteen months and the fact that any additional contracts would require capex and put upward pressure on the cost base.

As promised, this week we continue to look through some of the key highlights, and my notes on the top end of the market (by market capitalisation). The securities this week are CSL, BHP, and Wesfarmers.

CSL Ltd (CSL.ASX)

This is one company with which we’re sure the vast majority of our readership has had a pleasant experience with through their investment careers. Despite the volatility, it continues to be one of the few consistent performers in the ASX50. The company and management has once again managed to surprise in releasing yet another round of stellar results. Numbers wise, revenue continued to grow by 11% and Covid, while impacting the supply chain in regards to the collection of Plasma, has not materially impacted revenues.

The company remains well-capitalised with over $750m USD cash on the balance and available liquidity of close to $3.1bn USD. What was perhaps missing in the reporting, was an indication of how the Vitaeris Inc. acquisition was coming along. Although this seemed to be a small acquisition given the broader portfolio, it was interesting in that Vitaeris was conducting phase III clinical trials for a treatment for organ rejection within kidney transplant patients. Another niche but highly promising and potentially lucrative market. Perhaps not in the same way as haemophilia but arguably on par, with existing treatments in that particular instance ranging from anywhere between $300,000-$500,000 USD per patient (more than compensating for the small market size).

Red Flags & Risks: Covid-19 has undoubtedly cost the supply chain in terms of plasma collection, something that remains central to CSL’s business model. While the company controls around 30% of collection centers globally, the current lockdowns and health concerns have inevitably led to supply constraints. The flip-side of this is that the economic damage caused as a result might force more people, especially from lower socio-economic stratas (in the US that is, you don’t receive compensation here), to give more blood.

In terms of the competitive environment, the vast majority of the portfolio including the immunoglobulins and Seqirus related products are plasma based and, although CSL has a marked advantage in this area given the highly consolidated nature (oligopolistic structure with the closest competitor being Grifols), there is also potential for competition from recombinants (see below). The next phase of growth will very much rely on the Asian markets where cost will play a greater and more significant role. In other words they have to compete with recombinants in the developed world (i.e. recombinants being more expensive) and cost in the east. The product pipeline, including the acquisition of Vitaeris, is potentially a way to diversify the portfolio but this remains in its infancy.

“…recombinant product versions of plasma derived products are also available. These are manufactured by the expression of equivalent proteins from genetically engineered cell lines.“

Forgive the Wikipedia definition, but: “Recombinant DNA (rDNA) molecules are DNA molecules formed by laboratory methods of genetic recombination (such as molecular cloning) to bring together genetic material from multiple sources, creating sequences that would not otherwise be found in the genome.”

That is all to say, plasma synthesised in a lab as opposed to collected from donations.

My Expectations: Management continues to deliver, with consistent expenditure on R&D. The haemophilia B market remains lucrative for the company with further expansion into the European markets providing long-term revenue growth. Covid, while having an impact on the supply-chain for plasma, will also potentially be beneficial as the company would be part of the equation for the distribution and commercialisation of Covid-related vaccines at least in Australia. The R&D pipeline looks solid with my bets on the transplant and hematology related aspects to deliver.

Dividend Yield: Current yield of 1% (assuming share price at $281 AUD).

We would expect the payout ratio to remain the same but on an absolute basis for dividends to grow at double digits over a long term horizon.

BHP Group Ltd (BHP.ASX)

Stellar results from BHP with FY20 NPAT of $9.1bn USD, EBITDA margin of 53% and, most importantly for the yield hunters, a 55c US p/s dividend, lower than expected but in my opinion prudent and a number which still represents a 72% payout ratio. As expected, the laggards were the petroleum and coal divisions. What was exciting (in my view) was the potential divestment of half of BHP’s coal production, especially thermal and PCI assets (didn’t necessarily expect the Bass Strait Gas assets to be included). But any demerger via a trade sale, especially a demerger when trying to get rid of thermal assets, would have to be sweetened.

The company continues to look for oil acquisitions, in which they would of course be joining their global counterparts (Exxon et al.). My expectation is bolt-on acquisitions of juniors (maybe the Gulf of Mexico or, even more interesting, Horizon’s P&G interests which lie on the pipeline route of ExxonMobil and Oil Search).

What was rather disappointing, however, was the copper division especially in a time of stellar copper prices. Underlying EBITDA of $4.35bn USD was less than impressive due to higher costs in Antamina and Olympic dam. This, I feel, is one division to which management could allocate some much needed resources, the existing pipeline of Tier-1 assets look less than stellar especially when compared with Rio’s Winu (this includes the LATAM assets where costs have been kept reasonably within range).

Red Flags & Risks: While BHP has a diversified base in terms of commodities, the name of the game is pro-cyclicality. Weakening demand for steel production in China could hamper future growth and much will be contingent on maintaining cost discipline and hedging. Further delays in restarting Samarco and any weaknesses on project execution can be painful for shareholders. The divestment of coal assets could see some much needed focus, in my opinion, better allocated by getting a hold of copper assets which should have a longer runway and lessen the cyclicality of earnings (copper being central to electric vehicles as well as having a long-term secular growth story to it).

My Expectations: Management has delivered some stellar results and navigated the Covid mess in a better then expected manner. The business has to be streamlined somewhat however with the riddance of legacy assets as soon as possible, here I am thinking of thermal coal. The shifting of focus towards copper, rare-earths and oil will put the company in a better place over the long-run. Not a growth story but a yield story.

Dividend Yield: Assuming a share price of $37.5 AUD, then BHP has a great 4.5% dividend yield.

BHP remains a credible substitute for the banks from an income perspective.

Wesfarmers (WES.ASX)

Wesfarmers results showcased fantastic performance across the retail segments. Bunnings was the standout with same store sales growing by 14% through FY20 and delivering an overall EBIT of $1.8bn AUD (17.6% growth). Target remains the outlier (on the downside) continuing to be loss making while Kmart remains profitable. Revenues were cushioned primarily via strong online sales growth( coming in at close to 34%), with the major impact of Covid coming from supply-chain constraints (stock-outs).

Officeworks, with an EBIT of $190m AUD, represented double digit growth (13.8%). What was surprising to me was the chemical, energy and fertilizer divisions which beat on expectations. Volumes continued to grow for both chemicals and fertilizers, though LPG was weaker within expectations. Overall this segment still delivered an EBIT of $450m AUD (not Bunnings type growth but nothing to cause concern).

Red Flags & Risks: Though the company has maintained market share within an increasingly competitive environment (especially in online retail), the flip-side of this will be the margins. Unlike pure-play online retail, the existing store-footprint means that the cost base is substantially higher and uncertainty around Covid-19 as well as the impact on supply chains remains uncertain. It will be incumbent on management to deliver an omnichannel experience to customers whereby the stores are effectively turned into distribution centres. That said, credit where it’s due, the spin-off of Coles was a solid play and gives the company ammunition to go hunting for deals. For the moment, consumer sentiment and overall outlook will be the biggest factors impacting the business going forward.

My Expectations: Management has delivered for shareholders and remains a business that has consistency in terms of managing expectations as well as payout ratios for its shareholders. A lot of the reporting was however quite tactical and backward looking to do with the retail division and how the business was coping with Covid. No clear outline was given about where it was heading from here. In my view, a focus on their chemicals business will be interesting and the play for Lynas last year was an indication to me of where they were looking in terms of the future (though one wouldn’t have known it from the commentary).

Dividend Yield: Assuming a share price of $47 AUD, then WES has a stellar 3.6% dividend yield.

With a proven consistency in terms of payout, a good yield for the income hunters.

Disclaimer

BHP is currently owned by the author of this article, Sid Ruttala. TAMIM has no current exposure to the three stocks mentioned in this article.

Kevin Smith takes a look at one long-term holding and two more recent acquisitions, all of which performed very well in July 2020, each stock rising by more than 40% for the month.

High volatility has been a feature of the equity markets in the region during the past two years, with the key events being trade tension between the United States and China and the subsequent Covid-19 pandemic with the associated disruption to economic activity across the world. Three-year annualized volatility for the Asia region to the end of July was close to 20%, well above the long-term average and a big jump from the 13.5% volatility figure recorded in the region twelve months earlier. While volatility has been at high levels, market returns have remained well below their long-term average. During the year to end July 2020 our benchmark index of small to mid-sized companies in the Asian region in Australian dollar terms fell by 3.1%, while our Asian portfolio net of all fees increased by 0.5%. It is very pleasing for us as fund managers to achieve a positive return when the underlying markets are in decline. If you had not looked at markets in the past twelve months and had avoided all news stories you would have concluded that markets had been quiet during that time with the small negative outcome for the index. The purpose of this article is to take a closer look at our responses to three examples of highly volatile companies in our portfolio, China Lesso, United Microelectronics and BayCurrent Consulting, all of which increased by more than 40% in July, a month when the overall index recorded a decline of 2.6% in Australian dollar terms.

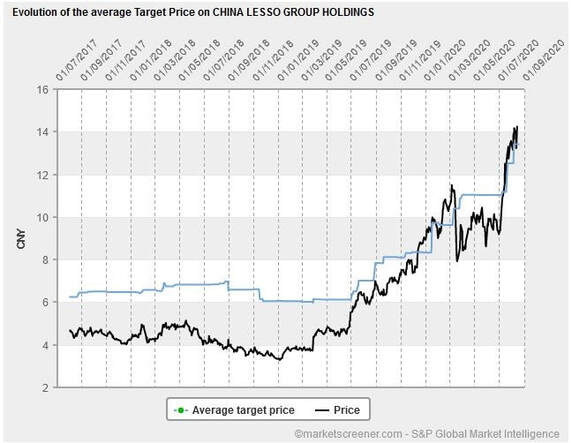

We first acquired a position in China Lesso (Lesso) (HKG.2128) in the fourth quarter of 2018 at an average price of HKD 4.08, at the time of writing the shares trade at HKD 15.50 to be the strongest performer in our Asian portfolio. During the month of July shares in Lesso increased by 48.4% from HKD 10.08 to HKD 14.96. We have taken profits along the journey, in particular for risk control purposes, it is important not to let an individual stock position grow too large in a diversified portfolio. Lesso was a major contributor to our performance in the past year. Lesso typically has coverage provided by seven or eight analysts and the progression of the company share price versus their target prices is shown in Figure One. The analysts have struggled to keep pace with the underlying share price.

In October 2018 we concluded that “Lesso meets our standards for accounting, strategy and governance. Lesso has a strategy directed towards the development of China, the company has a strong home market in Southern China and is well placed to benefit from urbanization of the interior of China and major infrastructure projects funded by local government bodies and the national government.” Lesso has 90% of sales from plastic pipe systems, revenues grew by 11.0% and earnings per share increased by 22.5% in 2019. Figure Two illustrates the level of valuation of Lesso when we first acquired the shares in 2018 on a p/e ratio of 4.3x, the valuation has since expanded to the current (and still reasonable) level of 12.9x. With continued growth in profits expected out to the year 2022, Lesso trades on a prospective p/e ratio of less than 10x.

Figure One: China Lesso Share Price Versus Average Target Price

That expansion in multiple explains the majority of the return achieved in the past two years. We are happy to retain a position in the company since our original reasons for investing remain intact, the company continues to score well on our measure of VMQ (valuation, momentum and quality) and high standards of governance are being maintained. Lesso remains a key beneficiary of the urbanization of the interior of China with 25 production bases located across 16 provinces in China and a nationwide sales network of more than 2,000 exclusive distributors.

Figure Two: China Lesso Valuation History and Forward Estimates

Source: marketscreener.com

United Microelectronics Corporation (UMC) (TPE.2303) manufactures and markets integrated circuits. The company provides wafer manufacturing, assembly, testing, mask production and design services. UMC operates 12 fabs that are located throughout Asia with a maximum capacity of more than 750,000 8-inch equivalent wafers per month. The company employs approximately 19,000 people worldwide, with offices in Taiwan, China, United States, Europe, Japan, Korea and Singapore. In Q3 2019, UMC ranked fourth in the pure semiconductor foundry industry with 6.7% market share (source: Trend Force). UMC manufactures semiconductors using advanced production processes for customers based on its own proprietary integrated circuit designs. UMC’s wafer fabrication process includes services such as design, mask making, testing and assembly services. We believe UMC will transform into a specialty foundry, changing its business model, and focus on 28nm, 40nm and 8″ foundry products, which will result in significantly improved profitability by reducing capex and R&D.

We built our initial position in UMC during May 2020 at an average price of TWD 15.15. There are 20 analysts producing forecasts for UMC, in July 2020 there was considerable positive earnings surprise when second quarter earnings were reported some 56% above the market consensus that is derived from those 20 analysts. The share price of UMC responded by rising 40.6% during the month of July to close at TWD 22.35. We did not buy our position because of any particular insight regarding the next set of quarterly results, our time-frame is to take a view over several years. We do not make forecasts for an individual quarterly earnings period however we look to form a judgement regarding the likely success of the strategy being employed by the company we are assessing. For UMC, the company scored very well on our broad categories of value, momentum and quality and as noted above we liked their strategy of becoming a specialty semiconductor foundry with the scope to increase profitability. The earnings increase that surprised the investment analysts in the second quarter results was a vindication of the company strategy albeit somewhat earlier than we had anticipated. Figure Three shows that the market is now expecting continued growth of earnings in the next two years with a prospective price earnings ratio of 11.5x. Since we take the view that the company strategy as far from complete, we are retaining our position in UMC.

Figure Three: United Microelectronics Corporation Valuation History and Forward Estimates

Source: marketscreener.com

BayCurrent Consulting Inc. (BayCurrent) (TYO.6532) is a comprehensive consulting firm based in Japan. BayCurrent is engaged in designing and implementing strategies relating to information technology, global growth, marketing, mergers, joint ventures, alliances, governance implementation and turn-around management. BayCurrent has grown rapidly in recent years with the annual results reported to the end of February showing revenue growth of 36% and earnings growth of 91% over the previous year. We started to have a serious look at the business when the valuation dropped below 20x price to earnings in recent months and decided to build a position in early July at an average price of JPY 8,858. We then watched the share price rise by 49% in the space of three weeks to JPY 13,216 at which point we sold the shares. It is very unusual that we have a holding period of just three weeks, more typically we will hold a position for three years. In this instance the 49% share price increase put the valuation up to 31x expected 2021 price/earnings which was more than our tolerance for value. We will be happy to have another look at the company if the valuation drops back to a reasonable level.

Figure Four: BayCurrent Consulting Inc. Valuation History and Forward Estimates

Source: marketscreener.com

In conclusion, while the Asia regional returns have been subdued in the past two years, we have seen some extreme levels of volatility with individual stocks moving as much as 50% month to month. This article has provided three examples of stocks held in our Asian portfolio that have increased by more than 40% during the month of July. Share price movement of that magnitude will always prompt us to review our position, in two cases, China Lesso and UMC we retained our holdings on the basis that our view of the respective strategies remains intact and the valuation isn’t too high. In the case of BayCurrent the 49% upward price move in three weeks pushed the valuation above an acceptable valuation level and we sold our position.

Kevin Smith, also of Delft Partners, is portfolio manager of the TAMIM Asia Small Companies portfolio. Click here to learn more.

This week we go through some of the notes and key highlights from the top end of the market. A disclaimer before reading further, this is the first part of my notes on the top ten securities by market capitalisation.

Author: Sid Ruttala

Please note, this does not necessarily mean that we currently hold any of the top ten, especially given our domestic equities mandates are broadly ASX ex20. Nevertheless, I do believe it pays to keep a track of what is happening in their universe and their balance sheets to get a feel for the overall economy. In addition, given their sheer weightings in a liquidity driven market (we will leave this topic for another week), it is good for investors to keep a track of them whether they own or not.

Commonwealth Bank of Australia (CBA.ASX)

Given the headwinds associated with Covid-19 and the mortgage deferrals, CBA has been pleasantly surprising in its results. The commentary by management has been rather conservative (as would be expected). Numbers-wise, statutory NPAT stands at $9.6bn AUD (up 12.4%), though this is a result of divestments related to the wealth business, while cash NPAT stands at $7.3bn AUD. The cash NPAT gives a better indication of the operating environment for the bank going forward and represents an -11.3% decline. Painful yet better than expectations. The growth in cash rate linked deposits has also provided a buffer.

What is interesting is the maintenance of a dividend at 98c (with no discount on DRP), taking the full-year dividend to 2.98 AUD p/s. This suggests a payout ratio of close to 50%. Despite the payout and provisioning for bad loans, CET1 remains just above 11.3%, significantly better than its counterparts. This is likely to increase to 12.5% after the sale of non-core assets.

Red Flags & Risks: NIM (Net Interest Margins) continued to fall from 2.09% to 2.07%. This might stabilise, assuming the RBA doesn’t change its policy stance with regards to negative rates. Signs of stress are also appearing with credit card arrears ticking up exponentially from 1.02% to 1.23%. There is also uncertainty around the residential mortgage book since the annual report doesn’t take into consideration any loans deferred as part of the Covid-19 support packages in line with APRA expectations. This might have the caveat of nasty surprises if there are any changes to government and regulatory policy.

My Expectations: NIM’s should stabilise at 1.8-2.0% over the next 24 month period. Cash NPAT will be around $7bn AUD and unlikely to grow for the foreseeable future. Management also failed to clearly outline the status and process of cost-cutting initiatives apart from fluff around digital transformation. Personally, I am not expecting substantial strides to have been made via these initiatives. Provisions have been made to deal with the fallout from the Royal Commision, but recent class action from Shine is likely to complicate matters.

Dividend Yield: Current yield of 4.25% (assuming share price at $70 AUD).

Downward pressure likely to take the absolute payout down further. Payout ratio would conservatively be adjusted, contingent upon overall economic outlook and the property market.

Westpac Banking Corp (WBC.ASX)

Revenues were broadly flat through Q3, as is the case with the other majors, along with softer margins, including NIM’s (down by 8 bp). Perhaps of more concern has been deposit headwinds, which acted as a substantial buffer for CBA. This scenario was somewhat mitigated by non-interest income (i.e. predominantly less than expected insurance claims). We believe the wealth business remains a key headache for the bank going forward. The interim dividend was also cut.

WBC is well capitalised with CET1 standing at 10.8% but was an outlier in that this was a slight reduction compared to the other three competitors. Here we were pleasantly surprised on the upside again, with the BDD (Bad & Doubtful Debts) only coming in at around $825m AUD. $30bn AUD in mortgages remain in deferral, this is similar to the bank’s counterparts in my view and was to be expected.

Red Flags & Risks: NIM’s are under pressure and, when compared to CBA, Westpac is slightly lower at 2.05%. Impairment charges on mortgages have been cushioned somewhat with the help of regulators and, somewhat surprisingly, management expects around half to return to payment. 90+ day delinquencies in unsecured consumer lending are also ticking up steadily, now reaching 2.52%, with the NZ business slightly lower at 2.31%.

My Expectations: NIM’s should stabilse at 1.6-1.75% over the next 24 months. Cash NPAT will remain flat for the foreseeable future. The big concern is in regards to legacy business streams, including the wealth management arm, and substantial exposure to commercial property. I remain of the view that we will likely see more stress within these assets. Additionally, I did not get clear signs of how management was likely to reduce costs. This is what will be the key driver within the Australian banking system in the absence of changes to the interest rate environment or mortgage book growth.

Dividend Yield: Current yield of 4.7% (assuming a share price of $17 AUD) and taking into consideration the dividend cut.

Management are likely to be incentivised to play catch up next year assuming an economic recovery. Taking it higher in the year to come, in terms of yield, to 8%. This also assumes no further stress on the balance sheet. However, this would be a one-off and there would likely be downward pressure again given the cash rate and NIM’s. For the more adventurous amongst you, there is a potential short-term play for dividend stripping here.

National Australia Bank (NAB.ASX)

NAB was a genuine surprise, reporting growth in cash earnings from continuing operations by 25% to around $1.55bn (though Q3 earnings were down -7% when compared to 2019). The caveat here is that most of these would have been balance sheet related. To do with reversal of MtM (Mark-to-Market) losses from the previous quarter (related to Markets & Treasury).

Even NAB surprised with the BDD amounting to $570m AUD, substantially less than my expectation of $850m AUD. Management has indicated a clear pathway to separate the legacy MLC business. This should, one would hope, see some cash coming back to shareholders in the next twelve months. NAB is well capitalised with CET1 standing 11.6%.

Red Flags & Risks: Again NIM’s are under pressure (there appears to be a theme emerging here), we estimate them to be around 1.78% and likely to stay around this level for the foreseeable future. Much depends on management in streamlining the business through the sale of MLC (or spinning off) and placing focus on the SME lending business, a segment in which they have a substantial edge comparatively. There has also been a 2% increase in the costs, to do with remuneration and annual leave accruals, but Covid-19 has meant that the cost-cutting process is now seemingly taking a back seat. Nevertheless, the stock does trade at a significant discount to its peers.

My Expectations: NIM’s to stabilise at 1.4-1.55% over the next 24 months. Cash NPAT to remain flat for the foreseeable future. The big concern is the backseat the cost reduction initiative has seemingly taken. The fact that NAB has the SME portfolio is also a big plus when compared to the others as, in my opinion, the market is mispricing the amount of collateral that is actually put up for SME lending.

Dividend Yield: Current yield of 7.2% (assuming a share price of $18 AUD).

Likely to stay stable overall, assuming that we are right on the SME lending arm and given its relative undervaluation. In absolute terms, likely to stay consistent.

Australia and New Zealand Banking Corp (ANZ.ASX)

ANZ also surprised on the upside with BDD’s standing at $500m AUD. The earnings update was solid with an unaudited profit of $1.3bn AUD. Management has also been exceptionally disciplined in its cost reduction, maintaining a 1% decrease while also increasing capex and seemingly going through with their transformation initiatives. Dividends, thankfully for the investors, were 25c per share for H1 2020.

The caveat, and the one thing that stood out, was the substantially lower net interest margins when compared with the other three, standing at around 1.69%. We expect the bank to maintain this going through the next 24 months while the other three catch up on the downside (catch down is perhaps a more appropriate way of putting it?). The flip side is that, comparatively, ANZ has a greater proportion of fixed-rate loans and disproportionately high liquid assets (13bn). Deposit growth of 2.1% in this environment is to be applauded.

Red Flags & Risks: The NIM’s are by far the biggest concern when it comes to ANZ. The institutional business is stagnant and needs momentum behind it. The commercial business might get rather messy, especially Victoria. Currently, the commercial deferrals stand at approximately 14% of the book. That said, only 6% of this exposure is currently unsecured.

My Expectations: NIM’s will stay flat over the next 24 months, as will cash NPAT for the foreseeable future. However, the upside is that a quicker than expected recovery would see ANZ benefit given its institutional and commercial business, as well as well-diversified portfolio.

Dividend Yield: Current yield of 5.8% (assuming a share price $18.54 AUD).

Likely to stay stable given that absolute payout has already taken a hit. On the upside, increased momentum in the institutional/commercial business and cost reductions could provide some upside. Payout ratio expected to stay at these levels.

Takeaways

Leanest and meanest of the lot: CBA

But look at it like buying investment property… but with leverage given the balance sheets exposure to that particular segment.

Cheapest of the lot: NAB

The market is mispricing the collateral that SME’s put up for the loans.

The laggard of the lot: Westpac

Reading through the reports, I didn’t see any real indication as to how the business was to be taken forward and what the future might hold.

The one I can’t put a finger on: ANZ

NIM’s are the biggest concern but it remains the only one that has a substantial institutional business and seems to be the quiet performer in terms of its cost-cutting measures and vision.

Which one would I buy?

Rationally, either NAB (in need of a substantial re-rating) or CBA (safest bet). That said, I’m a little too scared to own any given I spend too much time reading about what happened to the financials in Europe and Japan in a prolonged low interest rate environment.

Endnote: CSL along with BHP, Wesfarmers and FMG will be next week.