Over the past few weeks we have been covering stocks we believe are poised to benefit from the ongoing reopening of Australia and New Zealand. This week we will be writing about a small cap payments company that should be a huge beneficiary of this reopening thematic.

Author: Sid Ruttala

The stock in question today is Smartpay. While most stocks that have “pay” in their name have been pumped at some point in the last few years by investors desperate to find the next BNPL unicorn, SMP is not one of them. Smartpay is a profitable business operating in both New Zealand and Australia, trading at a significant discount to the value of its businesses and we will show you why.

Smartpay (SMP.ASX)

Smartpay Holdings Limited is a provider of technology products, services and software to merchants and retailers. The business designs, develops and implements payment solutions for customers in New Zealand and Australia. Smartpay is a merchant-facing, in-store EFTPOS payments provider; they have a significant position in the New Zealand payments market and a fast growing Australian business. SMP currently provides payment terminals for over 30,000 merchants.

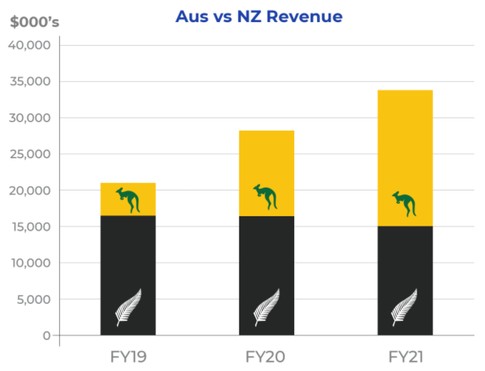

Smartpay has a huge presence in the New Zealand market but right now they are focusing on expanding into the Australian market which will provide a huge platform for growing the company. They currently have almost 7,000 operating terminals in Australia and are looking to add around 4,000 terminals per annum. Smartpay also has a huge SME market to attack in Australia. They currently have a tiny piece of the market but Smartpay’s reliability and competitive cost structure, through their zero cost eftpos solution, are seeing them winning market share in Australia, having grown Transactional (Acquiring) revenue almost 7x, from $2.5m in FY19 to $17.1m in FY21.

Source: SMP company filings

Revenue Model

Smartpay generates their sales through the transaction volume of terminals and processing those payments at a fee of about 1.6%. They earn a fixed fee per terminal and also receive income from software development, sales of terminals, short term rentals and other ancillary services. Their business model is mainly recurring and, once they acquire a customer, quite sticky; the churn rate is very low given the complexity involved in changing providers.

Each terminal in Australia adds around $3,900 of recurring revenue per year. If Smartpay are able to achieve their goal of adding 4,000 terminals in Australia p.a., considering the operating leverage SMP have from scaling their merchant base this would add over $6m of EBITDA p.a.. The majority of Smartpay’s cost base is fixed and sits across compliance, IT, marketing and employee costs. If Smartpay executes on their growth in the Australian market they will see a huge lift in their bottom line earnings figures given the mostly fixed nature of their costs.

Source: SMP company filings

Reopening Tailwind

The past few years have seen significant changes occur in the payments industry, the pandemic further accelerated the use of electronic payments opposed to cash payments for hygienic reasons; however, lockdowns have had a stupendous impact on volumes. Heading out of lockdown and into the holiday season, retail and hospitality should receive a huge boost in activity and, given the length of the most recent lockdown, there is a lot of pent up demand. Revenues from transaction processing made up over 50% of Smartpay’s sales in FY21. In their recent trading update management said “The impact of COVID lockdowns, primarily in NSW and VIC, throughout Q2 FY22, resulted in approximately 1,400 terminals in their Australian fleet unable to transact in the month of September.” Direct competitor Tyro has seen their November transaction value (to the 12th) up over 40% compared to the same period last year. Smartpay will no doubt be experiencing a similar rise which will have a significant impact on their FY22 result.

Valuation + Outlook

Note: all AUD

When looking at the valuation of Smartpay we need to separate their Australian and New Zealand segments. Their New Zealand segment has 20% market share and is far more mature. The NZ business is a solid, mostly recurring stream of income and gets most of its income from a service fee for the terminals. The NZ business is not where SMP’s growth will come from. The real driver of the business going forward will be growth in the Australian market as opposed to the NZ.

Source: SMP company filings

In 2019 Smartpay received an offer for their New Zealand business; the offer was a cash consideration of $70m NZD. At the current exchange rate (~96c as opposed to ~94c at the time), that values the NZ business at 29 cents per share.

Looking to the Australian business, we are going to make comparisons with their peer Tyro Payments (TYR.ASX). Tyro has struggled to gain traction as a public company and earlier this year they had severe operating issues with their terminals. Short research firm Viceroy also launched an attack which, in all fairness, was a bit overstated.

Tyro:

Note: FY21 figures

Smartpay currently has 6,737 terminals operating in Australia. Using their average revenue per terminal of $3,900 this would give the group around $26m of revenue p.a. but if you account for their growth plans (adding 4,000 terminals a year) as well as the increased transaction volume heading out of lockdowns, this figure could be well north of that. To be conservative, we will say that their Australian segment will do $26m of revenue for FY22. If you apply the same EV/Sales ratio that the market affords Tyro, this would value their Australian business at $173m or around 75 cents per share.

Accounting for SMP’s net debt (3.8 cps), now the maths becomes simple:

Giving us a valuation of about $1, approximately 33% higher than it is currently trading (~$0.75). At current prices, we think SMP is significantly undervalued, there is a sizeable margin of safety here too as there are multiple ways to win on the upside.

As mentioned, the reopening should see a big boost in transaction volumes across all payment terminals. This should see Smartpay’s revenue per terminal rise above what it has been the past couple of years thanks to on and off lockdowns around the country. Smartpay is a cheap way to get exposure to the digital payments thematic and, given their growth plans in Australia, Smartpay can expand their service offerings and offer new solutions such as business loans, bank accounts, data analytics, insurance while using their existing customer base to cross sell products.

We believe SMP will do over $40m in sales in FY22 revenue and over $8m in EBITDA. SMP is growing much faster than Tyro yet it is trading at a discount, we see Smartpay having a significant multiple expansion re-rate. If SMP is able to execute their goal of adding 4,000 terminals p.a., they will be doing around $18m of EBITDA by FY23. This would put them at a forward EV/EBITDA of around 10x.

Given the cheap valuation that SMP is trading at, they could also be an interesting potential takeover target having already fielded an offer for their New Zealand business.

We value SMP at $1+ and it is a core holding for the TAMIM Fund: Australia All Cap portfolio heading out of lockdowns and into the holiday season. SMP’s recent trading update saw a 58% YoY increase in total transaction volume; SMP’s half year result is due this month.

This week we begin a new series centred around the global pharmaceutical sector with a particular eye to ascertaining where the opportunities and risks may be. Going back to our broader macro views, in particular around inflation, this sectoral allocation is one that we feel may have legs.

Author: Sid Ruttala

Before proceeding further, a disclaimer. We are experts in neither the field of medicine, pharmacology nor epidemiology. As such, what follows is simply an investors quest to understand and find opportunities. Moreover, throughout this piece a great degree of data is ascertained from the International Federation of Pharmaceutical Manufacturers & Associations (IFPMA), given the lack of nuance (in this author’s view) provided vis-a-vis theoretically independent agencies such as the World Health Organization (WHO) and our very own Therapeutic Goods Administration (TGA). Nevertheless, we shall try and keep the argument as impartial as possible.

Background & Context

For the history buffs among you like myself, this is one sector whose evolution has never ceased to fascinate and tells the story of human ingenuity and enterprise. What began with local apothecaries, expanding their traditional role distributing botanical drugs, turned first into wholesale manufacture, not least aided by discoveries in morphine and quinine, to now becoming a sophisticated global industry central to modern economies (as was illustrated in our most recent global pandemic). My own fascination came about from reading into the prolific use of Laudanum for the most mundane of problems in the Regency Period to the opioid wars that led to the handover of Hong Kong to the British Empire. That particular tangent aside, let’s look at the nature and structure of the modern pharmaceutical industry.

It may come as no surprise that it can be quite difficult to disentangle the structure of the industry and the regulatory framework from its evolution in the USA. From its rudimentary form of oversight starting as a result of early outbreaks of tetanus and distribution of contaminated smallpox vaccines (though even here we have seen instances of regulatory capture arguably as recently as the Nixon administration’s War on Drugs) and passage of acts such as the Biologics Act of 1902; the modern regulatory framework has evolved to create a diverse range of actors both private and public with national bodies, such as the FDA in the US and TGA domestically, becoming the final and peak arbiters. With that, lets look broadly at the process of firstly bringing new drugs/treatments to market.

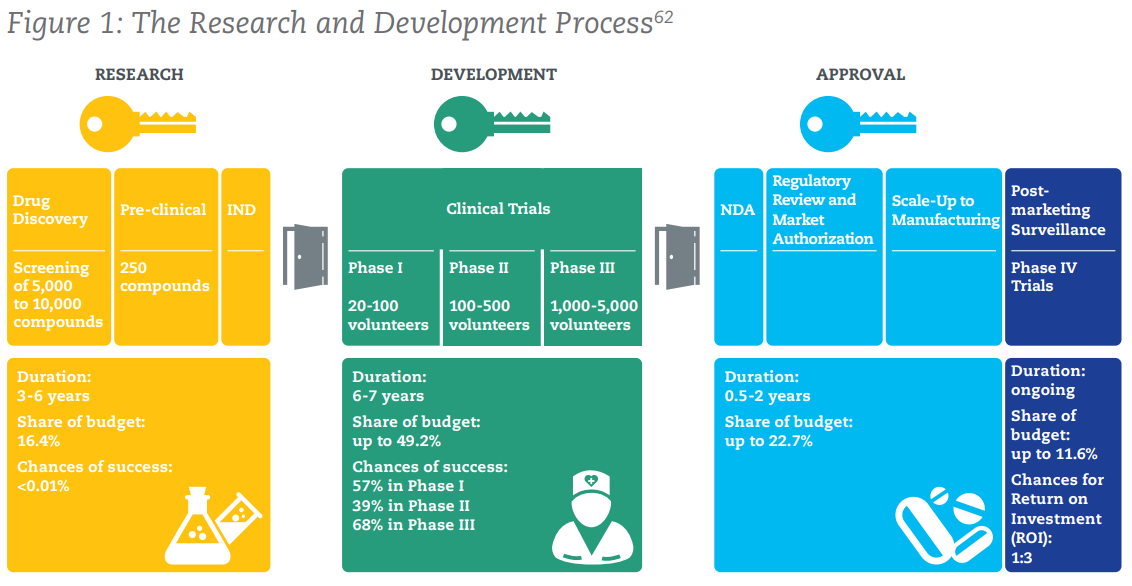

Source: IFPMA

The above figure shows the process by which a new drug/medication is brought to market. To sum up some numbers that may be truly eye-opening, here are some key points:

2.5% – 5%: The success rate of compounds passing through the screening process to proceed to pre-clinical trials.

Chances of Success: <0.01% in pre-clinical, 57% in Phase 1, 39% in Phase II, 68% in Phase III

9.5 – 15 years: The average time it takes for a new treatment to go from initial screening to market.

US $2.6bn: The average cost of bringing a successful medicine to market. Some more context: this was US $179m in the 1970s…

More concerning than the above numbers, is the graph below. It showcases the exponential declines in IRR (Internal Rate of Return) from pharmaceutical innovation over time for a cohort of the twelve largest biopharmaceutical companies by 2009 R&D spending. It shows that returns have declined from about 10% in 2010 to just 1.8% as of 2019. Little wonder then for the rather extraordinary underperformance of the sector for shareholders in recent years.

Source: IFPMA

So, that brings us to the question why has this been the case? Especially given the per capita expenditure on healthcare across most of the developed world. To answer that question, let’s look at a similar graph which rather prominently shows the disconnect from overall expenditure on healthcare amongst OECD nations. It shows that while overall expenditure increased significantly, the expenditure on biopharmaceuticals has remained broadly constant.

Source: IPFMA

It is perhaps not that particularly difficult to fathom why. Given the likelihood of success in R&D combined with declining IRR, firms are by extension incentivised to increase profitability of existing products (before patent expiration) as opposed to take on the risk of bringing new products. So, on to the next question, why are IRRs declining?

In a world saturated with conspiracy theories, pharma PR debacles and general pushback against the industry, it may not be a popular opinion but the increased regulatory requirements which, although well intentioned, also had the effect of stifling new innovation and increased consolidation of the space. This is the flipside of regulation, creating high barriers to entry most prominently seen within the financial services sector. Across the planet we have increasingly stringent testing requirements and the cumbersome process of receiving regulatory approvals, national health authorities also require companies to track and report patients’ experiences while reporting requirements also substantially raise investment cost (for the duration of time that the medicine is marketed). To put it simply, we remain of the view that the investment and regulatory landscape has swung too far. But, what’s at stake here?

Quickly, for those that think that Covid-19 was a outlier event in terms of the overall impact upon the global economy. $500bn is the estimated yearly cost of pandemic influenza to global GDP. $3tn is the estimated loss worldwide due to antimicrobial resistance, in the form of superbugs, to the global economy per annum in worst case scenario modelling. By 2030 it is estimated that the cost of tuberculosis every year will be $1tn USD.

Current Landscape

With that context, let us actually get to the current reality of the global biopharmaceutical industry. While overall R&D has seemingly declined (and in our view still remains woefully underwhelming given the centrality of global efforts to the overall economy), the sector still remains an outlier in terms of the amounts spent on R&D, 7.3x greater than aerospace and defence and 1.5x that of software and computer services. Great numbers, aside from the massive cost increases involved in the process over the last four decades.

Conversely however, there have been ways in which the pharma industry has evolved in order to tackle the often prohibitive costs associated. New and novel collaborations through joint ventures, including with non-corporate entities such as academia, and cross sector collaborations are just some of the more recent trends. The most recent and obvious example of this has been the global effort to bring Covid-19 vaccines to market in record time; AstraZeneca’s collaboration with Oxford or the creation of the global COVAX initiative alongside public sector organisations such as the WHO, the Coalition for Epidemic Preparedness Innovations (CEPI), and UNICEF (i.e. for delivery) is a prime illustration of the changes that have taken place.

This unique and complex landscape has also led to certain dislocations. For the truly global investor, we are certain at least some may have taken advantage of the growth in generics in emerging markets such as India. That particular country now accounts for close to 50% of global vaccine manufacturing capacity, 40% of generic medicine demand in the US and 25% of the same in the UK. Combine that with a domestic market that has grown in the high double digits for the last two decades, likely to go 3x over the next two, and equities investors in the overall sector would have seen on average return of close to 15x over the last two decades. The growth in the generics market has been the second trend and the centrality of India is the third that remains crucial to understanding the global market.

No longer is the market characterised by blockbusters being bought to market and the exceptional cashflows generated re-used to generate further blockbusters. We have a truly global supply chain, one which many may have become painfully aware of when India’s own bipolar policy response to Covid put the entire global vaccination program at risk. Increased capex is required while patent expiration for existing medicines combined with competition from generics provides massive headwinds to the market. Combine that with an aging population and future growth coming from emerging markets such as India (which require different pricing), for the non-discerning investor, it is a nightmare to sift through.

On the question of pricing, let’s use a simple and quite recent example: the introduction of the first oral treatment for Covid-19 by Merck (MRK.NYSE) which has ascertained regulatory approval (before you get excited, it is not a cure but simply reduces the chance of hospitalisation by 50% if administered within three days of onset). The actual pricing and distribution of the product is likely to be tiered with developed markets such as the US, which has already agreed to buy US $1bn worth of product, being used to subsidize distribution in poorer or emerging markets. This is done through licensing deals with generics manufacturers, though in the instance of Merck they have decided to distribute it for free. Call me a cynic but we are quite certain that, as they bring to market newer versions and are no longer in the limelight, we will see nice little margins ascertained over the next decade or so (not to mention the PR bump in the short term). The development of the drug itself, to illustrate the other point of collaborations, was done in conjunction with Ridgeback Biotheraputics.

Not to be left behind, Pfizer (PFE.NYSE) has also seemingly come up with its own antiviral pill that is 85% effective (compared to Merck’s 50%) if administered within five days of onset (compared to Merck’s three days). Both work in slightly different ways, with Pfizer being a protease inhibitor (blocks the enzyme and multiplication) while Merck’s is a nucleoside analogue (introduces errors into the genetic code of the virus). Pfizer’s own mRNA vaccine and Covid-19 pill is, by the way, a collaboration with German company BioNTech (BNTX.NASDAQ).

The above example of the Covid-19 anti-viral pill illustrates another example of the modern context. Merck effectively giving away its own IP stands in contrast to Moderna and Pfizer’s ongoing refusal to transfer technology to mRNA vaccine producers in Africa, LATAM and Asia. As mentioned, we have a feeling that Merck’s strategy could be a PR coup which we believe puts them in a better place in those particular growth markets for monetization later. For now however, Pfizer has been the frontrunner in terms of its vaccine efficacy as well as in Covid-related research to date.

With that let us finally get to the first security we like and one which we own in the TAMIM Fund: Global High Conviction portfolio, Pfizer.

Pfizer (PFE.NYSE): Investment Case

We originally bought Pfizer years ago, trading out in early 2016 due to the potential merger between the company and Allergan Plc, which was at the time a potentially lucrative windfall due to tax inversion (i.e. shifting headquarters to Ireland).

“So, if the regulators and governments allow the merger to proceed, it is our view that Pfizer may have just bitten off more than they can chew…doing something for tax reasons alone is seldom a good reason.”

Unfortunately for the company, the US Treasury (at the time under the Obama administration) issued new rules to effectively prevent the deal (though it was not pointed out). There was a US $150m breakup fee and somewhat lacklustre performance since.

We bought back into the stock in 2019. Why?

For one we feel the company is often misunderstood. Even before their Covid-19 vaccine, they had a strong pipeline of drugs which fit in perfectly amidst an aging and increasingly obese population. Although mature, Lipitor (cholesterol), Viagra and Celebrex (anti-inflammatory) are three core products. This is combined with prudent acquisitions throughout the 2000s (i.e. effectively ensure stable cash flows for the foreseeable future). With the advent of Covid-19 however, we feel that the company has hit a new period of potential growth. Granted, given the global environment and an increasingly confrontational approach to the sector in the presence of vaccine shortages (yes, this is an issue for a vast majority of the global population despite it not being the case in the West), we will see incremental monetisation going forward. As Covid-19 continues to evolve in the presence of vaccines (superbugs are all but guaranteed) and we see continued rounds of yearly vaccinations globally, this will potentially remain a sticky revenue stream. Believe it or not, the real money is likely not made now when there is a great degree of immediate necessity and potential PR nightmares, we expect increased margins over time as the world learns to live with it.

Arriving at the numbers, revenues for the company grew at a stellar 130%. Even stripping out Comirnaty (their Covid-19 vaccine), the company continued to meet expectations with 7% growth. That second aspect is important given that the flipside of Covid has been a decline in OTC medications and healthcare expenditures. We believe that this is due to Pfizer’s unique product line, aside from lockdowns providing a tailwind for Viagra sales, there has been consistent growth across product lines such as Vyndamax (heart failure – transthyretin-mediated amyloidosis), Ibrance (Breast Cancer) and Eliquis (blood clots), all three of which have grown at high double digit rates. On the negative, cost of sales increased close to 41% (granted, a result of vaccine distribution requirements). What is more concerning however is the 5% increase in Selling, Informational & Administrative Expenses (SI&A), this goes back to our point about the increased expense burden across the sector.

What is more interesting, in our humble opinion, is the all important R&D metric, that is the success rate of the drug pipeline. Across all three phases, Pfizer stands out in having a rate approximately 20-30% higher than industry averages; Phase 3, for example, at 85%. Using simpler metrics, PE at 16.2x (compared with the S&P500 at 29.51x) and a dividend yield of 3.3% (don’t use Australian standards, this is reasonably attractive for US equities) with a payout ratio of 52.45%, we expect this to go sequentially higher over the coming two year period.

Over the coming weeks we will continue to explore the pharmacuetical sector. Given the events of last couple of years, it is easy to have Covid-blinkers on when looking at the space but we will look to explore some of the other dislocations and interesting vaccines/treatments currently in develpoment and the opportunities that these present.

Robert Swift takes a look at what happened in October in markets. This is an excerpt from Robert’s Global High Conviction report for October 2021.

Author: Robert Swift

Global equity returns were unusually strong in October rising over 4.5% in USD terms and essentially flat in AUD as the Australian dollar strengthened.

The USA rose 7% driven by decent corporate results, and a continued postponement of the tapering of central bank intervention. Inflation is rising quite clearly, even using today’s somewhat massaged construct, and with wage rates also rising, the chances are high that inflation expectations become embedded. In the short term this is a tailwind for equities given that they are a claim on nominal growth and a better inflation hedge than bonds. In the long term it is a problem for asset market stability, but a problem, as yet, unacknowledged by policymakers.

The USA continues to provide contradictory messages in the domestic and international arenas. President Biden recently indicated that the United States would defend Taiwan if that became necessary which is somewhat at odds with the official line that respects the “One China” policy. Taiwan’s President Tsai Ing-wen confirmed that there are a small number of US forces located in Taiwan to help with training of Taiwanese soldiers, an admission that annoyed Beijing with a call for the United States to immediately cease military and other official interactions with Taiwan. This will raise tensions and provides a source of volatility to a complacent equity market. The deal to export US LNG to China was announced while at COP26 as the need to reduce fossil fuels further was announced by the US delegation. The infrastructure bill remains mired in Congress with some Democrats now removing their support for the ‘social’ spending aspect. Popularity ratings continue to fall. (The infrastructure bill has passed through Congress since writing, the social spending and climate package are up next).

Essentially, investors are becoming confused about US monetary, economic, and foreign policy.

Japan was the weakest market in our portfolio with the index declining by 3.7% ahead of the general election called by recently appointed Prime Minister Kishida. There were fears that the ruling LDP would lose their majority in parliament, however, this fear proved unfounded as results announced on 1st November indicated a clear single party majority for the LDP. Prime Minister Kishida now has a mandate to push ahead with the additional budget spending that was promised during the campaign. This will include increased military spending to counter a more assertive China. The market responded positively to the election result. The election could be seen as the beginning of a change of generations within the LDP, having seen several senior lawmakers losing their long held seats while younger lawmakers including Taro Kono and Shinjiro Koizumi achieved emphatic victories. The equity market should enjoy better returns now that this major period of uncertainty is out of the way.

We sold ABB (ABBN.SWX) in Switzerland after moderate results but a clear indication that next year was going to be tough as the European economies continue to struggle. We purchased Cheniere (LNG.NYSE American), a US LNG provider, and ONEOK (OKE.NYSE), a pipeline company supplying to the US export terminals in Texas. The US is now an exporter of LNG, a clean energy source. Such businesses are stable and thus attractive investments if a sell-off in the exuberantly priced equities is forthcoming.

Results were strong for Norfolk Southern (NSC.NYSE), Seagate Technologies (STX.NASDAQ), KLA (KLAC.NASDAQ) and Simon Property Group (SPG.NYSR) and all rose 10% or more.

We see irrational exuberance in many pockets of the market; and rapid and punishing share price falls on adverse news. Tesla rose 10%, or many billions of dollars in value, on a ‘deal’ announced by Hertz that they were buying Tesla cars for their rental fleet. It transpired that there was no signed deal. In any event, the sale of cars to the rental companies was long considered to be poor quality business for the auto manufacturers because they were at low margins and the quick resale of these cars hurt the second-hand prices of all models. More confusing to us is that if demand is so strong for high margin retail sales, why would Tesla countenance this move? The company is now capitalised at about $2m per vehicle produced and is worth more than the next nine auto companies combined even though it may produce c. 700,000 vehicles next year in a global market of over 75 million. It is on a P/E of over 300 x

We obviously ‘don’t get it’ but were told the same in 2001 and in 2008.

The words of Scott McNealy, CEO of Sun Microsystems, in April 2002, come to mind. “At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?”

There are currently 28 companies in the S&P on over 10x revenues.

Snap Inc. (SNAP.NYSE) fell 20% plus when it blamed a shift in Apple policies for a dramatic and ‘unexpected’ reduction in ad revenues, and Zillow (ZG.NASDAQ) fell almost 40% in three trading sessions as its punt on flipping houses proved both difficult and costly.

This week we visit our second category within the mobility thematic, that is autonomy. A topic that is arguably more important than the general electrification of transport, we arrive at three key considerations for those wishing to take advantage of the thematic.

Think for a moment about the impact of this autonomy theme, not only within the automobile segment but the broader economy. The questions that spring to my mind include the impact on automotive sales, especially in densely populated geographies such as China? The economic impact in nations such as India where driving as a profession makes up the primary income source for over 150m people? On the flip side, the ultimate nirvana of fully autonomous vehicles (connected) should also reduce road accidents and fatalities. This is one topic that has clear benefits and will potentially lead to large dislocations in the overall economy.

Autonomy and shared mobility, which we refer to as ACES (Automated, Connected and Shared Vehicles), has already had a tremendous impact upon the border economy. Just think of the more well-known Uber and Lyft IPO’s and, in emerging markets, companies such as Ola. The way I try to contextualise this trend is to think about the evolution from the simple mobile phone to the smartphone, trends that are mutually reinforcing. Where the hardware (in this case the Electric Vehicle) is evolved into the fully autonomous vehicle (in this case software that enables connectivity in the same way as the iOS or Android systems make up the vast majority of the underlying interface that enables the features of the smartphone). As of today, the market for automotive software has been silently growing at about 7% annual CAGR with the market expected to grow to over $469bn USD by 2030 (Source: McKinsey). This is the first thing that the discerning investor should be aware off, the overall automotive market (characterised by end-user sales) is, in contrast, expected to grow at 3% p.a. over the next decade (assuming current trends are not changed). Simply put, the best opportunities do not necessarily lie in access to final producers or downstream so to speak, but rather in the components that make it up. As if that were not enough, it is more than likely that we will see the same creative destruction trends that we saw in other markets. Think about it in the same way that Apple revolutionised the smartphone market and now the market share of Nokia today.

Within automotive software, as is the case with any new industries, there is significant divergence and segment-level variation. We have yet to see a centralised software or a player take the lead within the space. My view is that, unlike the automotive industry in general, the software itself might just be a winner takes all market (with the caveat being that it will be hard to judge who the leader might be), just as Google took close to the entirety of the search market and Windows (Apple’s iOS nonwithstanding) with the PC market. This is a place where the watch and wait approach might be best with a diversified pool of bets in the portfolio. Some listed companies within the space include, Keysight Technologies Inc (KEYS.NYSE), Thermo Fisher Scientific (TMO.NYSE), Materialise (MTLS.NYSE) and Silicon Laboratories Inc (SLAB.NASDAQ). Existing incumbents such as Microsoft, SAP, Autodesk, Dessault and Oracle are also making headways in building out divisions.

Aside from software, we will continue to see advances made with regards to sensors. One can reasonably expect to reach double digit growth in this market as incumbents scramble to perfect the segment. These include shared mobility players and the more traditional auto manufacturers. Looking more in-depth, the backbone for the technologies can be categorised into two segments, ECUs (Electronic Control Units) and DCUs (Domain Control Units), which underpin VxV (Vehicle to Vehicle communication). The relevant leaders within these segments currently include Nvidia (NVDA.NASDAQ) and QualComm (QCOM.NASDAQ). We expect that high-voltage harnesses within ECU to increase whilst the converse is true for lower voltage (i.e. EV vehicles).

That said, major players have already made certain headways including Volkswagen, which plans to adopt a unified automotive architecture, and BMW, introducing a central communication services and service-oriented architecture (SOA) providing a certain level of scalability. To date, the issues remain the security of the underlying software, the efficiency and efficacy of VxV communication and circuit level complexity. Rather than going into detail that might very well bore, think of it like the problems associated with making an iOS system communicate with Windows. The alternative could be open source and a centralised system with regulators effectively operating as the middle-man. For the more impatient investors, the companies that currently dominate the DCU market are Visteon (VC.NASDAQ), Continental AG (CON.ETR), Bosch (a private company other than their Indian operations) and Aptiv PLC (APTV.NYSE). The upcoming contenders include Chinese player, Huawei (not publicly listed), Desay (part of Huizhou Desay SV Automotive Co Ltd, 002920.SHE), Shenzhen Hangsheng Electronics (HSAE is also not public) and Neusoft (600718.SHA).

What is perhaps interesting about the incumbent players vs. the upcoming players is the geographic segmentation and it adds a secondary consideration for the discerning investor. The first group are domiciled in the EU and US whilst the second are all domiciled in China. This is where we must consider geo-politics, as the Huawei situation has undoubtedly shown with regards to 5G, there will be lines drawn that makes the supply chain and investing a little more complex (and perhaps more profitable for the same discerning investors) since companies are not necessarily competing on a global landscape but within particular spheres of influence.

If regulatory responses were to go toward preferential treatment for certain players, this will almost certainly create scenarios of greater economic profit than would otherwise be the case in a truly competitive environment (in economics this is termed economic rent-seeking). It might very well be the case that it would be better to diversify portfolios across not only market-leading companies but also geographies with the added advantage that risk is mitigated somewhat by ensuring a base-level of profitability (i.e. even if the company is not necessarily best-of-breed globally, they may be profitable purely based on jurisdiction).

To conclude, recognise the following:

1) There is a developing and evolving ecosystem of companies within the broader AV thematic;

2) The industry is still in its infancy and, if the past is anything to go by, then the winners are not so easily discernible, hence it is best to diversify at this stage;

3) Find market-leaders but with the caveat that it might be best to also diversify geographically since the macro political situation warrants and creates a scenario whereby the winners are not necessarily best of breed. For the older generation or the historians amongst you, think back to the creation of keiretsu firms in Japan (which now encapsulate the likes of Toyota and Mitsubishi) or chaebol firms in South Korea (think companies like Samsung, Hyundai and LG) which eventually became best of breed by economic rent-seeking, thus enabling the profits to be reinvested and allowing them to move up the value supply chain. Or, going back even further, American protectionism and policies that created the industrial giants of the late 19th and early 20th centuries. To put it even more simply, take the example of aeroplane manufacturers and ask yourself the following question: If I were to invest in aeroplane manufacturers, would it be more reasonable to choose Boeing or Airbus? Personally, I would spread the investment either equally or proportionally based on market share and it would help me mitigate the risk of regulatory intervention or tit-for-tat scenarios based on the vagaries of politics. Assuming of course that all I care about is a return on my investment and not normative questions.

This week we revisit the property market, specifically the potential/future for commercial office space. We are in the process of offering our most recent buy in the Adelaide CBD and throughout the process we have consistently received questions around the prudence and rationale behind taking exposure to the space. In particular, within the broader context of increased tendencies toward work-from-home and falling demand. So, we thought we would address that question rather briefly and why we feel that this question, though warranted, may in fact be somewhat overdone.

Author: Sid Ruttala

Before proceeding further, we will put a disclaimer in saying that when it comes to property we have a tendency toward the Buffet school of thought in saying that economics and broader trends are nice to have but, when it comes down to the actual investment, has very little sway in the decision making. A good company is a good company, a good property is a good property. Almost always, the viability and return of a property investment comes down to the price at which you buy and, secondly, the way in which you manage said asset (this second aspect often determining capital growth).

This is perhaps the reason why TAMIM has historically gravitated or been attracted to so called industries in decline. Retail for one. Starting with our community shopping centre in Elermore Vale, our Fairfield Heights asset anchored by Woolworths or the more recent large format retail addition in Rutherford. Just listening to the headlines would’ve turned most investors off looking at these particular assets but it is precisely this tendency which enabled us to buy at what we feel are reasonable (if not) strong yields. If one cared to drill down into the details and past the headlines, it may have been rather evident that perhaps staple stores such as your local Woolies may still have a place. Or that consumers may still rely on physically inspecting big-ticket purchases such as home and contents (i.e. Rutherford) and this may still lead to higher foot traffic. This is all to say that we can’t simply rule out the entirety of a sector (i.e. retail) based on a broad trend, there are good assets out there for those with the patience and expertise to find them. Buy smart and manage well.

Similarly, when it comes to commercial offices, we feel that there are dislocations becoming increasingly evident.

Commercial Office Space

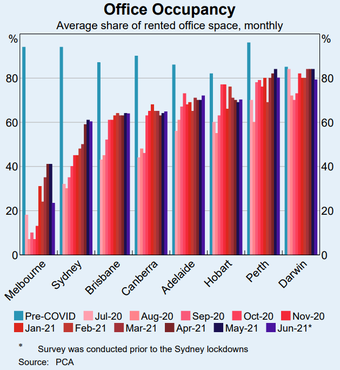

Let us begin by saying this, the headlines are right. Covid-19 has been momentous for the commercial office market in Australia (and globally). We do in fact agree that we will continue to see dislocations in the market and longer term declines in the demand for office space. Most office staff shifted to working from home during the early days of pandemic (and associated lockdowns) with the event acting as a broad catalyst in moving toward work-from-home or flexible working arrangements. There have been some, especially in technology like Atlassian, which have gone even further in effectively letting 100% of the workforce go to a flexible work-from-home arrangement. Currently, occupancy rates across Australia remain at 10-30% below pre-pandemic levels.

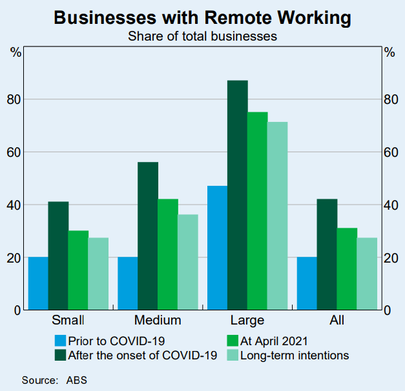

A recent survey by the RBA, for example, found that a majority of firms were looking to reduce floor space by around 25% and make increased use of hybrid solutions. All this might suggest that I’m arguing against exposure to commercial office space but here is where the nuance comes in. Let’s actually look at the previous statements and untangle it a bit. The key word is hybrid, that is businesses were by no means looking to get rid of physical presence but operate through a combination of work from home and office. By extension, the question then becomes whether there is excess supply. Secondly, what are the types of businesses looking to make these arrangements? For some greater detail, have a look at the chart below which shows the proportion of businesses with work from home arrangements broken down by size. The fact of the matter is, large enterprises have by far the highest proportion of remote working arrangements. This occurs for a plethora of reasons but it usually comes down to capacity constraints. Think then about what type of spaces are used by large enterprises (generally owner occupied, think Westpac or CBA) versus medium to small (rented).

Source: RBA

So herein lies point number one, there will be substantial differences in the impact of the changing dynamics, contingent on the profile of the properties in question.

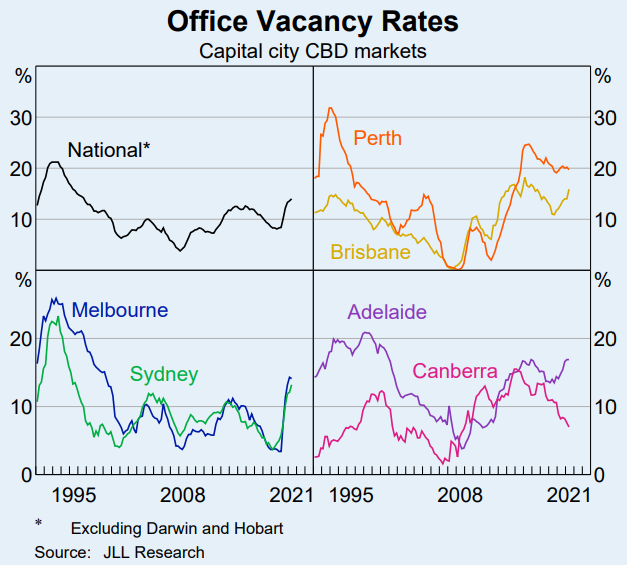

Arriving at our second point and declines in office space demand. There will certainly be particular industries that are more amenable to a remote working dynamic than others. Tech being one example that comes to mind, but what about others? Say, for example, financial services or legal services? Based on our own interactions and primary research, we remain of the view that this may not be quite so simple. Clients, for example, still require physical interaction (I highly doubt any of our investors would be quite comfortable knowing that there is no physical presence or address) or industries which still require training, a point that was recently relayed to us by one in the legal profession. This has broader implications and that is in the nature of employment in relevant cities. Most technology businesses in Australia, for illustration, have their headquarters in Sydney or Melbourne. Moreover, the nature of the labour market in these two cities suggests to us that this is where the greatest amount of dislocation may eventuate. The graph below shows the vacancy and occupancy rates across Australia’s major metropolitan areas. The outlier appears to be Canberra, which has seen consistent declines even despite the pandemic. Why? The proportion of the labour force employed in government (one area not so amenable to remote working).

Source: RBA

Looking at the second chart, showing occupancy rates in comparison to pre-pandemic, what becomes immediately evident is that Melbourne and Sydney remain outliers. This is what arguably matters more for pricing. First, a slower recovery indicates excess supply and bargaining power remaining with the tenant as opposed to the landlord (whereas a better implies the opposite). An excess supply may indicate that there are deals to be had aplenty but, given the nature of the property markets in Melbourne and Sydney, the higher vacancy rates may not be baked into the selling price. The dislocations and real opportunities are likely to come outside of these two cities. Looking at Adelaide, we see some consistent momentum behind it towards pre-pandemic levels of occupancy yet lower in absolute terms which, all things equal, should provide some attractive pricing for buyers.

This may seem like a post-hoc justification but the rationale remains solid.

So, with that, let’s recap. Firstly, yes, commercial office space is a segment facing some long-term headwinds but this is precisely what creates the opportunities for the discerning investor. Especially so in a property market that seems excessive to say the least. Two factors that remain important are location and nature of the tenancy profile. Office spaces that are suitable for flexible working, priced more economically (catering specifically toward SMEs, not for profits, government and quasi-government and services) are likely to sustain themselves over a longer period of time. This doesn’t sit well with the investor who potentially equates larger or higher profile tenants with lower risk, however it is precisely that profile which lowers the bargaining power of the landlord and makes themselves amenable to look toward remote working. Assuming that the market continues on this trajectory and we see declining supply (we will start to see it eventually), we use the same logic in looking at this market as we did with the energy markets.

Digging deeper, we believe that a greater degree of “value add” will need to be provided by property owners to fit into the changing profile of the rental landscape. Physical offices, for example, could adopt creative propositions such as green spaces, exercise rooms and specific attributes, such as natural light, could play a greater role in the value of assets. Similarly, we also see the nature of the landlord-tenant relationship changing; aside from bargaining power, a more nuanced approach to rental contracts (including those that reflect uncertainty around end usage) will increasingly become a factor aside from compression of WALEs (increase in break points). As with anything, these changes cannot be written off by the investor as risks but potential opportunities. A compressed WALE also gives the owner some flexibility in being more active in order to potentially increase rents through more aggressive campaigns than would otherwise be the case. Similarly, a multi-tenant approach, if done properly, could certainly provide for some lift in overall rental yields.

To conclude, we shall say this: be careful what fixation on a theme or headline may cause you to miss! In fact, a bear market arguably presents the best opportunities. In this case market pessimism to a particular sector or category can also be an incredible investment opportunity. After all, going back to our first point, the best investments usually come down to simply the price an asset was bought at.

Once again, buy smart and manage well.

Sidenotes

Some may think that the comparison above when it comes to the major metropolitans may not be fair given the variance and degree of lockdowns and policy implementation. The point here is that, even taking this into consideration, we are not seeing the fall in occupancy which is not necessarily being reflected in the asking price for sales.

And! We have a policy announcement from the RBA. Surprise, surprise! The cash rate stays put at 0.10% with an abandonment of yield curve control (interesting times ahead for the traders). This implies that the central bank will let the long end of the yield curve rise while using the short end to maintain its target till 2023-2024. Somehow we continue to be of the opinion that rates will remain compressed for longer (except only targeting the short end). If you follow that train of thought (and this is in no way advice), every time there are jitters about rates going up (we’re quite sure the pundits will point to the long end) just buy! Balance of probabilities, they’re not. We neither have a Volcker nor the demographics to stomach it.

Smartpay Holdings Limited is a provider of technology products, services and software to merchants and retailers. The business designs, develops and implements payment solutions for customers in New Zealand and Australia. Smartpay is a merchant-facing, in-store EFTPOS payments provider; they have a significant position in the New Zealand payments market and a fast growing Australian business. SMP currently provides payment terminals for over 30,000 merchants.

Smartpay Holdings Limited is a provider of technology products, services and software to merchants and retailers. The business designs, develops and implements payment solutions for customers in New Zealand and Australia. Smartpay is a merchant-facing, in-store EFTPOS payments provider; they have a significant position in the New Zealand payments market and a fast growing Australian business. SMP currently provides payment terminals for over 30,000 merchants.