This week we continue looking at needs not wants; companies that provide critical services that people need rather than want. We are using this theme to highlight companies that are best positioned for inflation with some even set to benefit from higher interest rates. We will be diving into the insurance industry and highlighting one company in particular.

There is a reason why Warren Buffett’s Berkshire Hathaway has such a large stake in the insurance industry; insurance companies provide a service people need and is an almost recession-proof business model. Property and Casualty (P&C) insurance protects against property damage and provides liability coverage for claims against insurers for injuries or damage to others’ property. Two of the most common forms of P&C insurance are auto and homeowners. Insurance companies will not only benefit from rising interest rates as they earn more money from the premiums they invest but the policies they write will grow as a result of inflation which leads to higher prices for the things that people need to insure.

Chubb Limited (CB.NYSE)

Chubb is the world’s largest publicly traded P&C insurer, based on a market cap of $90.6bn. Chubb is a global company, with local operations in 54 countries and territories. Chubb provides commercial and personal property and casualty insurance, personal accident and supplemental health insurance, reinsurance and life insurance to a diverse group of clients. As an underwriting company, they assess, assume and manage risk with insight and discipline.

Chubb has a clear advantage in its underwriting capabilities stemming from experience and scale. Their combined ratio is well ahead of their peers, the ratio measures the profitability of an insurance company by adding the expense ratio and its underwriting loss ratio. Any ratio above 100% indicates that the company is paying out more money in claims than it is receiving from premiums.

Source: Company filings

Interest Rates

During 2020, the pandemic resulted in widespread panic and plenty of questions about whether economies could survive lockdowns. Economists from every corner of the globe all had a different take on the issue but consensus was that global markets would require stimulus from central banks to mitigate the impacts of slower economic growth. People were worried about deflation rather than inflation in those ancient times. The Federal Reserve took interest rates from 1.75% to just 25bps and rapidly expanded their balance sheet through quantitative easing programs to provide much-needed liquidity to falling markets.

Source: Robert J. Shiller, National Bureau of Economic Research

Fast forward to today and the headlines are dominated by inflation with the word being the most used out of any economic terms in finance related articles. The tables have turned and we aren’t worried about lockdowns, rather we are worried about our eroding purchasing power thanks to higher energy prices and ongoing supply chain issues. While rising rates and inflation is a curveball for most industries, especially those with poor pricing power, there are some companies that stand to benefit.

Unlike most industries, insurance companies have a positive correlation to interest rates. As part of an insurance company’s business model, they invest the premiums they receive from customers into bond-like instruments. There are stringent regulations on what insurance companies can and cannot invest their money in and they are typically restricted to investing in treasury bonds and asset-backed securities. During the GFC AIG (AIG.NYSE) famously found themselves investing in credit default swaps, which were underpinned by securitised mortgages the devil of 2008. Due to the restrictions on what insurance companies could invest in, AIG was attracted to the higher yields they could obtain from exposure to securitised mortgages that were still rated AAA. As long as the insured bonds were performing, AIG would receive their regular interest payments. If the assets underpinning the bonds were to collapse however… As we know, they did when the housing market collapsed and AIG found themselves in a far from enviable situation. AIG ended up owing Goldman Sachs traders $20bn. Most of which was paid out when the US government was forced to bail AIG out.

The recent 50bps rate hike by the Fed will have an impact over time on insurance companies’ bottom line. The more rate hikes there are, the more insurance companies will continue to benefit from the increased yields. The chart below highlights the recent increase in Municipal bond yields, 9% of Chubb’s investment portfolio is invested in Municipals.

Source: Factset

Chubb’s investment portfolio is worth a staggering $118bn and every rate rise will have an impact on Chubb’s investment income over time. Here we’re particularly refering to the segments with floating rates in the below allocations.

Source: Company filings

Outlook

The insurance industry has endured an extended period of tough operating conditions due to tighter regulations post-GFC as well as a lengthy period of low rates. However, with rates rising insurance companies are one of the few clear winners in the current environment and pose an interesting proposition for investors in terms of sector allocation.

Source: Factset, TAMIM

Chubb is trading below the average Price/Book Value ratio of its peers and has just about the best combined ratio. They are also in a strong position to take advantage of the cheap equity prices in the sector through M&A given their balance sheet, a trend we believe will continue in the sector.

This week we look at a new government in Canberra and what, if any, are the implications for markets? Before proceeding into what is intrinsically a divisive topic, we’ll start with the conclusion, the answer is the implications are negligible.

Some context

As market participants it sometimes pays to be cognizant of a rather Schumpeterian view on government policy as well as the shorter term policy framework (where monetary policy is included). Schumpeter is the arguable father of the Austrian school of economic thought which pushed for a more Laissez-Faires approach to markets. A man who is perhaps best remembered for the term “creative destruction” to explain market cycles and dislocations. Without getting into the details, the argument is simply this: there exists a natural long-run rate of growth in the economy (he wrote during the depths of the Depression), approximately 2-3%, that doubles living standards roughly every 40–50 years. Policies (whether fiscal or monetary) are only effective insofar as people and polities care about shorter term dislocations. So, what matters?

Broadly the categories are technological change and innovation, human capital (and growth in productivity), demographics (i.e. working age population) and finally labour force participation. As such, in the absence of changes to the existing institutional framework (i.e. changing the nature of the production), government policy will only impact longer-term growth and inevitably company earnings that we care about if, and only if, any of the aforementioned categories are impacted.

What does the change in government represent?

Thanks to the nature of Australian politics, namely mandatory voting, it tends towards moderatism (rather than political extremes). We are by no means political experts but the Independent performance this election looks to be a swing back to the middle against a perceived drift further down the political spectrum. The Labor and Liberal parties do not have what may be termed drastically different policy outlooks, at least in terms of the aforementioned categories. Both parties put forth budgets that espouse a greater emphasis on growth as opposed to austerity, both came through with policies aimed at priority areas of the digital economy (where the creative destruction will come from), childcare (impacting the longer-term participation rate) as well as manufacturing.

The major difference, in our view, is in the area of climate and associated action. Although there are certainly loud elements within the party that advocate higher tax rates on corporates, we somehow doubt this will have any discernible avenue to be translated into actual policy (especially in the current global economic environment). On certain questions such as aged care, where a great deal of noise has been made, we take a wait and see view in terms of actual policy.

Perhaps the most interesting outcome in the election has been the spectacular rise in Independents. This was combined with a substantial fall in the primary vote; at the time of writing the Labor Party having won 32.8% of the popular vote (-0.5%), the Liberal Party 23.9% (-4.2%), the Liberal National Party 7.8% (-0.9%) and The Nationals 4.0% (-0.3%). This should, one hopes, give the establishment some food for thought. One of the great things about Australian politics (and one that is an exceptional outcome for the investor) is its tendency towards the center. Both parties, as part of a broader global trend, have put too much effort in bringing fringe issues to the mainstream at the cost of rational policy debate. This has meant turning fundamentally economic or scientific questions into those of political ideology. One area where this is most obvious is climate change and action. On this the electorate has spoken and done so resoundingly, many of the Independents campaigning with climate change as a key issue while the Greens also picked up 11.8% of the vote (+1.4%).

So, with that let’s move on to the elephant in the room. This is probably where we see the most drastic shift from the old management team to the new: climate policy.

Climate: The Major Policy Difference

Let us be clear, there are obviously a myriad of policy differences between the two major parties. Here we are referring to the idea that climate policy is probably the only one that will have real impact on the long-term performance of the economy. A clear outcome in this election is that voters have come out in favour of more action on climate change. Labor unveiled a plan last year that aims at emissions reduction to the tune of 43% by 2030 and net zero by 2050. We are aware that this is often a contentious issue for many so we shall leave aside the science and just work through the implications for markets.

For the investor, the question is not the targets but how these targets are achieved. If the mechanism relies on punitive measures such as restricting supply and taxation, the outcomes are vastly different from say Commonwealth subsidies for renewables or increases to R&D incentives. If the emphasis is on the latter, then opportunities abound for those that can correctly identify windfalls for certain sectors of the ASX, including but not restricted to materials and infrastructure. An emphasis on the former could be a form of contractionary government policy that may place increased pressure on inflation data that is already steaming ahead (utilities and energy prices being a large proportion of the CPI basket). This also has implications for monetary policy which remains of much greater importance than the fiscal side. Again, we have to remain patient as to what form that policy takes.

We hope that cabinet chooses to co-opt the private sector as opposed to otherwise. We found it rather interesting that the previous government took a more interventionist approach, in the form of direct action, as opposed to the more market friendly ETS (Emissions Trading Scheme). This particular policy has even been implemented in China to reasonable effect.

From an investing perspective, it is quite irrelevant whether one chooses to believe in climate science. Especially when sitting in a country that has an abundance of resource endowments that are crucial to the global shift toward green (commodities such as cobalt and copper right through to iron ore). If anything, we take the view that the Commonwealth should push aggressively despite shorter term implications for electricity prices and overall dislocations. We’re talking potential short-term pain for long-term gain. There is no reason for the commodities boom to be over in this country, they’re just different commodities this time around. Australia, in our view, has the opportunity to become part of what has been termed by The Economist as ‘electrostates’ (i.e. analogous to the petrostates of the 20th century), the payoff could be quite astounding.

Moreover there is an argument to be made for what the negative externalities in traditional markets are (i.e. costs not currently priced in). Unfortunately, an impact of short election cycles is that it promotes shorter-term thinking when it comes to policy; that short-term pain can cost you an election after all. While undoubtably cheaper as it currently stands, the price of coal power generation, for example, does not include the medium- to long-term costs of pollution and associated healthcare costs. It’s not the outcomes that we are against but rather the ineptitude of policy. We firmly believe that market based solutions are the most efficient and effective delivery mechanism for equitable outcomes.

To conclude, we shall say this, investors have to be rational. The human part of us, with our intrinsically political outlooks (we are social animals after all), may lead us otherwise. In this instance, what we see in terms of fundamental policy differences gives us every reason to believe that the change in government isn’t going to have all that much of a long-term impact in terms of the long-term performance of the economy and thus the all important investor returns.

As we concluded last week: Keep it simple. Keep it disciplined. Keep it rational.

This week we return to the recycling theme touched on a couple of weeks back. Last time we spoke about an Australian recycling company benefiting from industry tailwinds and participating in the circular economy. This time we dive into the fundamental problems we face in recycling plastic and highlight a company that is looking to revolutionise this through the use of digital watermarks.

The poster children of current world issues are (arguably) the ongoing pandemic, Ukraine and climate change/pollution. Compared to even the very recent past, most people are far more conscious of their carbon footprint and make an active effort to minimise waste and recycle (there are obviously degrees to this). But what if I told you that right now the plastics you put in the recycling bin are as effective as eating carrots to improve your eyesight…

Today we are recycling over 50% of the world’s paper but, according to a study conducted by National Geographic, only 9% of the world’s plastic is being recycled.

Why is that though?

Of all the materials that end up in our recycling bins, plastic is the most difficult to recycle. This is because plastics are composed of several different polymer types. It’s currently almost impossible to recycle different plastics together as they melt at different temperatures. We also need to be able to sort food contaminated products from those that aren’t contaminated. Not all plastics are created equal, if we aren’t able to sort plastics the quality of the end product is very poor. Currently, when waste reaches a processing plant, it can be a challenge to identify what packaging is made of and what it was used for; which can be a barrier to more plastic being recycled into higher quality items. On top of this, plastic loses its quality as it’s being recycled. Without demand from companies to buy recycled plastic, this is all for nothing. We need to produce a recycled product that is worth using. If we were to be able to sort the different plastics on a mass scale then the whole recycling process would be far more efficient and valuable, creating a more sellable end product. Everyone is aware of our plastic pollution problem. Everyone is aware that it needs addressing. So we have a problem, what’s the solution?

Digimarc (DMRC.NADSAQ)

Digimarc is one company attempting to solve the above sorting issue. DMRC delivers transformative product digitisation solutions featuring digital watermarks and other unique identifiers combined with product intelligence in the cloud. Digimarc activates products, objects and digital media for greater accuracy, efficiency, security and recyclability. Companies benefit from deeper business insights, better brand integrity and supply chain traceability for total transparency.

Digital Watermarks

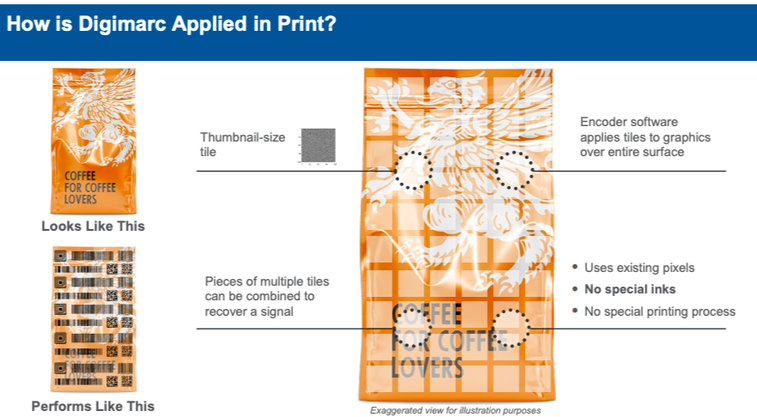

Digital watermarks are invisible codes, the size of a postage stamp, covering the surface of consumer goods packaging and carrying a wide range of attributes. Digital watermarks, functionally a barcode, allow for companies to maintain their packaging and branding without having to add visible barcodes.

Source: DMRC company filings

The aim is that once the packaging has entered a waste sorting facility, the digital watermark can be detected and decoded by a high-resolution camera on the sorting line, which is then, based on the transferred attributes (e.g. food use vs. non-food, one plastic type vs. another), able to sort the packaging in corresponding streams. This would result in better and more accurate sorting streams. Consequently, this allows for production of higher quality recyclates, benefiting the complete packaging value chain. Due to the items being covered in these barcodes the machines can identify them at whatever position they are in, even if they are in pieces, and will know what they are made of and the right kinds of plastics can be reused.

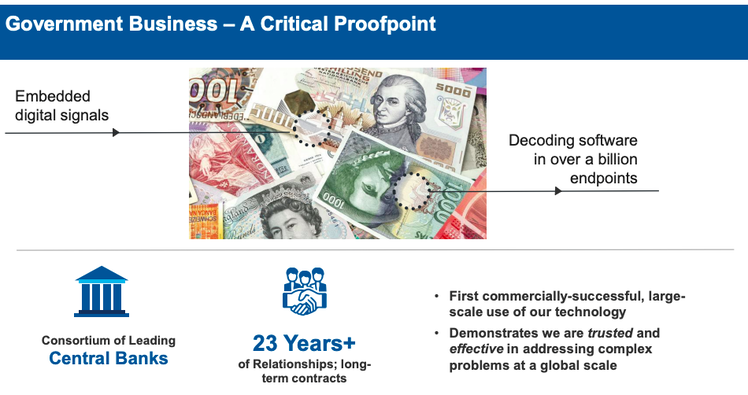

Additionally, Digimarc’s current customers include central banks. They use the watermark technology for banknotes. They are currently receiving around US $26.5m in revenue from this segment of the business. The revenue DMRC receives from central banks is sticky, recurring and provides the business with a solid base of cash flow with potential upside stemming from the counterfeit and recycling segments.

Source: DMRC company filings

In terms of other uses for the technology, digital watermarks can also be used for basic packaging on top of the anti-counterfeit purposes above. Since the packaging is covered in what are effectively barcodes, it could significantly decrease checkout times at grocery stores; instead of having to find barcodes to scan, the whole product is simply covered in them. Another potential use on the packaging front is for the watermarks to also be embedded with information on how to correctly dispose of them, allowing people to sort their own recycling at home as they can scan the watermarks and see how to properly recycle them.

The use of the technology in counterfeiting extends beyond currency too. The counterfeit market is a $464bn market and is only expected to grow alongside e-commerce. It’s hard to prevent the trade of counterfeit items on a mass scale, especially if they are coming from countries that do very little about it. The application here, for example, is that designer brands like Gucci or Louis Vuitton use digital watermarks on their products to make them easily verifiable, preventing a lot of people from getting scammed through counterfeit products traded in online marketplaces.

Holy Grail 2.0

The objective of the Holy Grail 2.0 program is to prove the viability of Digimarc’s digital watermarking technology for accurate sorting and business use at large scale. The program is led by Procter and Gamble (PG.NYSE) and has 160 (and growing) participants across the circular economy. These include global CPG brands, retailers, trade organisations, recyclers, printers, plastic converters, plastic resin manufacturers and NGOs.

Among other companies, PepsiCo (PEP.NASDAQ) will trial these invisible watermarks on the surface of some of their product packaging, encoding them with information about the manufacturer, product, material type and whether the packaging is food safe. When scanned by a high resolution camera on a waste sorting line, this information helps to sort the packaging into the right stream. Thus more high quality material can be recycled, more efficiently. Digital watermarking has also been included in the European Commission’s Essential Requirements for Packaging and European Parliament’s Circular Economy Action Plan. The program is currently in the third and final phase of trials and the results have been promising, showing consistently strong results across all tested categories of plastic packaging material; 99% detection, 95% ejection and 95% purity rates. The Holy Grail 2.0 program can prove a commercially viable case for Digimarc’s technology to be implemented for some of the worlds largest brands.

Source: DMRC company filings

Outlook

Barcodes were first patented in 1951 but took over twenty years to be implemented on a commercial scale. So, what will drive the adoption of Digimarc’s technology at scale today?

If we told you ten years ago that by 2030 you won’t be able to buy a new ICE vehicle and that you can hail a ride with no human driver in Phoenix, you’d probably have thought we were short a few marbles. The world’s shift on emissions over the last few years has been powerful, is accelerating and is rapidly transforming the way we live our lives. The EU are implementing aggressive regulations on emissions, legislating what kinds of cars can and can’t be sold going forward for example. Regardless of your stance on the issue, the Green Transition is being accelerated by some powerful regulatory tailwinds. In many cases, adoption of technology like electric vehicles or DMRC’s watermarks simply isn’t going to be a choice, it will be a requirement.

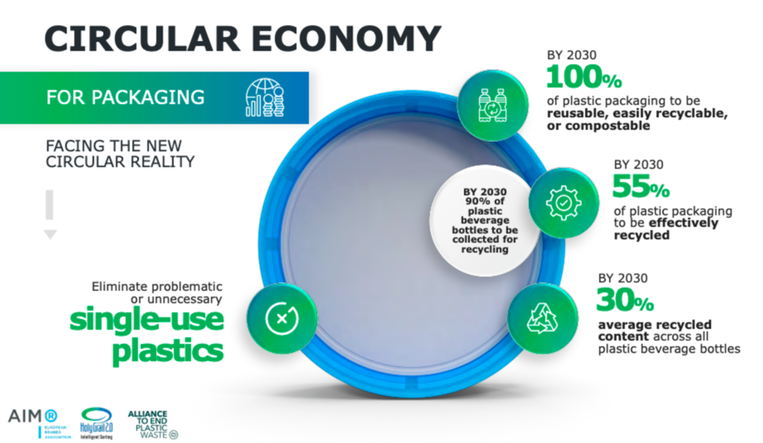

On that note, similar to EVs, the EU has put forward requirements to ensure that all packaging in the market is reusable or recyclable in an economically viable manner by 2030 and introduced a regulatory framework for biodegradable and bio based plastics. Most of the world’s largest plastic producers, like Pepsi and Coca-Cola (KO.NYSE), are being targeted by activists to do more about their waste. According to Greenpeace, PepsiCo uses 2.3m metric tonnes of plastic every year, while Coca-Cola is responsible for over 100bn bottles of single-use plastic. Additionally, countries like China are no longer accepting waste export from other countries; the problem can no longer be outsourced and ignored and we need a solution to deal with it. Regulation and a generational transformation are driving companies to change their ways and fast, Digimarc has the technology to benefit. Humanity’s current plastic recycling regime is ineffective and simply not sustainable, DMRC can help address this.

Source: DMRC company filings

The opportunity for Digimarc is enormous; they believe the market for plastic recycling is worth $16bn in the EU market alone. While the technology seems viable so far, there are still a lot of questions to be asked of Digimarc. The problem is there and in need of a solution but the use of this technology and whether it gets implemented on a large scale is no guarantee. Digimarc also has only US $33m of cash on the balance sheet. Given that they burned US $18m last quarter, further capital raisings are all but certain. This will dilute shareholders and put downward pressure on the stock price. There is some downside protection in Digimarc given that their work with central banks is churning out over US $10m of free cash flow a year. This is very sticky revenue. Digimarc’s current market cap is about US $350m. If they were to succeed in integrating their watermark technology into companies like Pepsi and Nestle (NESN.SWX), they could be a multi-billion dollar company.

One of the greatest privileges of being in this business is the ability to talk to other investors on a daily basis and understand the pulse of the market. Right now the pulse seems to be confusion, not necessarily fear. Confusion breeds uncertainty which can paralyze an investor, sometimes leading to even worse results. So, what do we need to keep in mind when thinking about investing?

Before proceeding further, the inspiration for this article is what the Oracle from Omaha has been up to. That is, the continued and aggressive deployment of the massive cash pile on Berkshire’s balance sheet as the markets continue to sell off.

Berkshire has been deploying cash at an aggressive pace this year. Cash on hand has gone down by over $40bn from the beginning off the year, to around $106.3bn in March, and it seems the business has continued on its trajectory. So, what has Warren been buying? Nothing new, adding to existing outsized positions in Occidental Petroleum (OXY.NYSE), Chevron (CVX.NYSE), HP (HPQ.NYSE), Citigroup (C.NYSE), Apple (APPL.NASDAQ) and Ally Financial (ALLY.NYSE). So does this mean it’s time to forget that confusion and jump in? Certainly not if your premise is investing because arguably the greatest investor alive is doing so. Berkshire has also exited its position in Wells Fargo (WFC.NYSE) which also tells us that even the greatest of investors is not infallible. Moreover, one must also remember that Berkshire is in the insurance business and their time horizon and rate of return requirements are quite different from you or I as a result. So, what should we look to and where should we look?

The first thing to remember is this: buy for the right reason. That reason is simple, once the valuation of an underlying security fits your requirements as an investor. A selloff is simply an opportunity to buy at a more lucrative price. Whatever the market conditions may be, if your investment thesis is simply wrong then there is no better time to sell than now (hence the sale of Wells Fargo). Our greatest frustration with a bear market is not that returns are negative, only that we don’t have the opportunity to buy more at a given price. It is unfortunate perhaps that investors have the curse of liquidity, which tends to exacerbate the Keynesian animal spirits in either direction. After all, we don’t buy a residential property and promptly go on to the street in order to ask every passer-by what they might pay for that particular asset and make decisions in the space of a moment.

Using more localised examples, take the case of businesses like Zip (ZIP.ASX) or Pointsbet (PBH.ASX, which we owned way back in the ancient times of 2020). What about these businesses changed over a time frame of two years that saw them reach dizzying double digit price heights and promptly fall from their peaks by 90% and 81% respectively? This aspect is perhaps what Keynes referred to when he saw equity markets as a game of musical chairs (for no intrinsic value add to the overall economic welfare) and, while we do disagree with the notion, market gyrations without a more balanced understanding sometimes make it seem otherwise.

We are by no means suggesting that we are or aren’t in a bubble or that recent price action has been irrational. Let’s try to understand what has happened to date, from there we can then formulate a view of where this may lead.

Context

At this point we are all tired of reading about central bank policy and its impact on the market. With that in mind, we’ll aim to keep things rather simple and go back to basics. First, what the stock or price of any given security represents? It can be categorised as two things: 1) the actual value of the business or asset today; and 2) what the market expects for the future of the business. Also worth remembering is that the market price is only as good as what the last marginal investor bought their share of the business for (keeping ourselves to equities), it is not the total value of the transactions or even the amount of money that changed hands. This is why stimulus checks, which bought retail punters with a preference for a more adventurous return, created some ridiculous price action. With that return to the basics, how does a central bank actually impact this? Quite simply, liquidity and valuation.

Remembering the second factor that affects the price of a security, that the future value of the business (ultimately in the form of earnings) has to be accounted for today, we need to use a discount rate. The most obvious mechanism for this is the rate of return of cash on hand today. The lower this is, the higher the price you pay today. Aside from this mechanism, the second form is liquidity. Oversimplifying again, QE injects money into the system which allows that marginal investor to pay an ever higher price. Reverse this and the result follows, you are essentially taking away liquidity or at very least lowering the price the marginal investor is willing to pay. So yes, a reversal of central bank policy can be a fundamental shift, taking away the marginal dollar and investor. To what extent though?

That depends on the change in policy. The S&P multiple under Volcker, who had the gumption to hike the economy into recession, was around 8x earnings. Today it stands at 17.6x forward earnings. In Australia it stands at a similar 17.5x. At face value, the possibility that there is more pain to come looks likely. If you take this view then, yes, the markets are not attractive. Hold on a moment though, we posit a different argument.

Despite similarities (the 70s and 80s did have similar supply shocks), things are very different now to four or five decades ago. We are facing wage pressures but this comes after more then two decades of stagnation and, while it does become a potential headwind for corporate profitability, it does create a stronger consumer which should feed into top line growth. Second, despite Powell seemingly espousing a desire to emulate Volcker Stateside, he may have forgotten that the latter effectively ruled out the possibility of similar policy shifts given an aging demographic, which also creates immense buying pressure and liquidity for investible securities (i.e. all things equal, an effective higher multiple for longer) and a natural moderation in inflation. On the latter point, think about the age bracket for the highest expenditure (i.e. mid to late 30s/young families).

While the US may have some more flexibility given that their debt profile skews toward public in nature, we remain highly cynical that there is the political wherewithal to hike the economy into a recession (the independence of central banks will start to unravel rather quickly). Looking to Australia, there is much less wiggle room. Household debt to GDP has now ballooned to a staggering 120% of GDP, much of which has been a more than buoyant property sector. Assuming sanity prevails, we similarly doubt that policy makers fixated on inflation inadvertently cause a depression.

What does this mean?

Don’t place too great a focus on earnings multiples based on history. The policy shift is not, given current constraints, likely to be as drastic as people expect (although the days of easy money and an effective central bank put are long gone). Despite a significant and (importantly) indiscriminate buyer leaving the market, of the reasons listed above the most important is demographics, there is a longer-term bid. If one does expect the left-field 70s repeat, remember that cash wasn’t a particularly great store of wealth. There was effectively nowhere to hide aside from select agricultural and real assets. Moreover, while the market multiple may shrink, keep the first category, i.e. earnings, in mind. Company earnings are the best hedges against inflation, assuming that they have pricing power.

This brings us to the original issue, is there reason to be fearful? Potentially, yes. But has the market ever been otherwise? No. It is our view that it is precisely these environments that create the most opportunities. It is a more reasonable bet to buy investments with a thesis that holds (assuming one is cognizant of their rate of return and valuation) than to effectively time the market. The marginal investor willing to sell at a bargain is a discerning investors gain. The bargain not being fixed but only compared with an individual investor’s valuation.

Is it better to wait?

It might be. It might not be. Despite humanity’s best efforts to make it otherwise, the world has always been messy. Left field events exist and if they were easy to predict then they wouldn’t be left field events. To name a couple, we currently have a war in Europe wreaking havoc on energy markets and an pandemic still causing supply chain issues years in.

Returning to the Buffett story, the stocks being bought were existing holdings. They obviously have an investment thesis that still holds and we would assume that there was a price the Berkshire team had in mind when making the original decision; they obviously have a higher price at which they are comfortable buying and they continue to buy at a lower price. An investor can only work on a balance of probabilities based on reason. Too often we find that there is an endeavour to create a neat certainty and ascertain all potential outcomes; a tendency that ultimately begets pain via FOMO or actually missing out.

It pays to keep things simple. Two questions are fundamental: what is your expected rate of return? What is the risk you are willing to take on? We are talking about volatility here not market risk, which is the potential for something to go to zero. If there is a potential for the latter, perhaps best a road better not travelled. All volatility, or a sell off, represents then is an opportunity. Ironically, it is quite a lot more productive to be fearful in a bull market than a bear market, in the former there is a lot more to lose than the latter.

Where to next?

With all that said, we can only say that we understand the reason and nature of the recent price action. We also can reasonably say that there are secular forces at play that should prevent another GFC or a depression like scenario. On the flip side it is also just as true to say that the unprecedented level of central bank largesse (driving immensely easy returns) is now at an end, nothing is forever after all. We remain of the conviction that equities are still the best possible asset class to be exposed to, one just has to be a little more discerning than in the past. Three important metrics to consider are:

Pricing Power – Allows the business to keep ahead of, or even with, inflation;

Revenue Stickiness & Visibility – Typically this is associated with technology companies but it can be applied across the board. There are even consumer discretionary players that have almost cult like following, like Nike. It can also come in the form of healthcare or biotech players that are protected by regulatory practices (i.e. patents).

Debt on Balance Sheet – It doesn’t have to be low levels, fixed rate debt with long duration is effectively a transfer of wealth from the debt holder to the equity holder. Think about global businesses such as say Siemens (SIE.ETR, issued negative yielding) or Berkshire.

Look to those metrics when buying, the current environment has made a lot of companies even more attractive. It is a rather futile endeavour to consider whether they might get cheaper, they’re attractive now and unless you genuinely have divine attributes that enable you to see into the future then you won’t pick the bottom!

One also wonders at the hubris of our kind, who somehow believe themselves to be the exclusive consumers of information or understanding changing contexts. As though management teams or employees of our holdings are not also trying to navigate the exact same circumstances? Be it inflation or the potential for a central bank policy error or any number of variables. We are willing to concede that a CEO of Woodside (WPL.ASX) or ExxonMobil (XOM.NYSE) might have a better understanding of the future of energy markets than us and make decisions accordingly or that the management of CBA might have a reasonable understanding of RBA policy or inflation. Assuming we pick stocks with reasonable management teams, we know where we would rather park our capital.

We shall conclude with one of the more memorable quotes in investing. Baron Rothschild once boldly stated, “Buy when there’s blood in the streets”. It is curious that the second half of the quote is so often overlooked: “even if the blood is your own.”

Keep it simple. Keep it disciplined. Keep it rational.

Over the past few years investors that owned the much-coveted “FAANG” stocks would have been amongst the most popular people in the room. Fast forward to today and the NASDAQ is down -26% YTD; Facebook, now known as Meta Platforms (FB.NASDAQ), alone is down over -40% YTD. Growth stocks went on a tremendous rise to the top post-Covid however in the current environment, where fear is winning the arm wrestle against greed, those same growth stocks are being sold off heavily. So, where to allocate?

With rate hikes being implemented across the globe and even more expected over the remainder of the year, growth stocks are worth materially less than they were under lower interest rates. Their cash flows, which are further out in the future, are being discounted at a higher rate. On the other side, the stocks that already have strong cash flows and are paying steady dividends are holding up far better. We’re focusing on companies with steady cash flows, strong dividends and attractive moats in their respective industries here. These companies may seem boring but they are consistent performers with nearly unbreakable business models. We are looking for companies that provide products or services that people NEED rather than want. Central banks are raising rates in an effort to curb consumer spending. We want to position our portfolio to have a mix of companies that are critical to day-to-day lives and are irreplaceable.

The FAANG stocks have had their day in the sun. The stocks we are going to highlight here go by the mnemonic QUAKE. QUAKE is predominantly made up of infrastructure stocks which provide investors with exposure to cash flow generating assets, high earnings visibility and strong dividends. Critical infrastructure – the likes of railroads, utilities, ports and airports – typically have natural built in protection from inflation and fare well in a rising interest rate environment. They are often also seen as safe haven assets or bond proxies, this attribute could see a lot of investor capital enter the sector given the pessimistic outlook on markets today.

Quanta was founded in 1997. The company is a leading specialised contracting services company, delivering comprehensive infrastructure solutions for the electric power, energy and communications industries. This includes design, installation, repair and maintenance.

With operations throughout the United States, Canada, Latin America, Australia and select other international markets, Quanta has the manpower, resources and expertise to safely complete projects that are local, regional, national or international in scope.

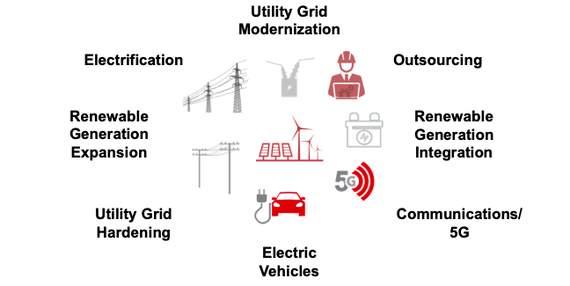

Quanta is well positioned to benefit from the energy transition toward a carbon neutral economy. They offer investors exposure to favourable long-term trends such as utility grid modernisation, system hardening, renewable generation expansion and integration, electric vehicles (EV), electrification and communications/5G.

On the back of energy transition tailwinds, we continue to see strong earnings and revenue growth for Quanta. Quanta will be a significant player in America’s move towards renewable energy and the utility industry’s heavy spending programs on grid hardening. This exposure to renewable energy goes beyond just solar and wind, also including renewable diesel, hydrogen, and carbon sequestration. In addition, Quanta also participates in the rollout of 5G and in the building of necessary infrastructure for EV charging stations.

Quanta has a diverse but high quality portfolio of clients including American Electric Power, AT&T, Verizon and BP. We are seeing these companies grow their investment in capex and infrastructure. Quanta has one of the best reputations in the industry and has long term relationships with their clients, contributing to repeat work.

Source: PWR company filings

Union Pacific (UNP.NYSE)

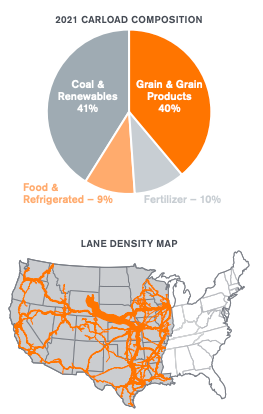

Union Pacific Corporation, through subsidiary Union Pacific Railroad Company, operates in the railroad business in the United States. Union Pacific is the second-largest railroad in the United States after BNSF Railway. The company offers transportation services for grain and grain products, fertilizers, food and refrigerated products, as well as coal and petroleum products (amongst others).

UNP are responsible for transporting critical cargo needed to keep the lights on as well as ensure people aren’t hungry. A need, not a want. UNP holds an effective duopoly over railway shipping in the Western United States, this gives them pricing power in an inflationary environment. These railroad businesses may be mature but it doesn’t mean they aren’t also putting out spectacular numbers. In FY21, UNP’s ROE was sitting at 41.9%! For context, Amazon’s (AMZN.NASDAQ) ROE in FY21 was 28.8%. The company still has room to grow through providing more channels for distribution to other geographies. There is also potential upside in UNP utilising their existing capacity more efficiently to maximise their operating leverage. The business ticks all the boxes for us: high barriers to entry, strong cash flows, and provides a critical service.

Amada is a large Japanese manufacturer of metal processing equipment & machinery based in Kanagawa. They serve an array of markets, including construction, mining, aerospace and defence, automotive, agriculture, oil and gas, electronics/electrical components, industrial equipment, and the general consumer. The tailwind driving growth of the company is automation, which will increase efficiency and lower labour costs in turn, while development of the latest and innovative products will drive growth in the days ahead. Growth in end-use sectors such as manufacturing, aerospace and automotive is anticipated to drive the metal fabrication market over the next few years.

Amada are currently trading at an EV/EBITDA of 5.4x, they are also forecast to grow their EBITDA by +63% in FY22. Japanese companies have been notoriously overlooked by investors and are sitting on rock-solid balance sheets. Amada is sitting on a net cash position of ¥85m. As governance improves across the board in Japan we expect companies like these to get more attention. A longer-term tailwind for Amada is the urbanisation of India. India currently sits on a GDP per capita of less than $2000, their low GDP per capita means that most consumer spending goes towards food and other basic living necessities. Once GDP per capita crosses through $4000, spending on higher cost items that require metal – cars, fridges etc – will rise accordingly.

KLA Corp (KLAC.NASDAQ)

Source: IC Insights

KLA is the leading supplier of process control equipment used in the fabrication of integrated circuits. Integrated circuits are small chips that perform functions in the digital world like memory storage, timers for automated processes, amplifiers etc. Before they get installed they need to be tested. KLA focusses on this testing. The process control systems, in which KLA specialises, are used to analyse product and process quality at critical junctures (mostly the back end when the whole IC Package has been assembled) of the manufacturing process. Small increases in yields, the % of the IC package that works, are very valuable to semiconductor makers since this means huge increases in profits to them.

There is a growing need to ensure the reliability of semiconductors due to their increasing complexity. The expansion of semiconductor demand has also continuously boosted the demand for testers. The challenges of semiconductor miniaturisation, advancing complexity, and power consumption reduction have continually raised the bar for improving test efficiency. This is all good news for one of the leading companies in this field.

Due to higher costs associated with larger wafer fabrication factories (fabs), manufacturers are mostly inclined toward outsourcing semiconductor assembly and testing services to third party providers. Leading fabless companies will continue to outsource everything, including testing, assembly, and packaging. This is a huge driver for testing companies like KLA.

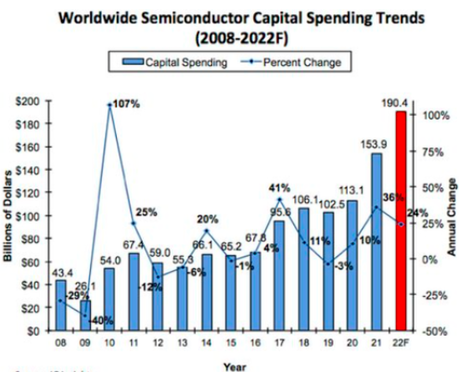

In FY22 KLA is forecast to grow revenue and EBITDA by +36% and +44% respectively. As Capex from semiconductor companies continues to accelerate in an attempt to close the supply deficit, companies like KLA will continue to benefit.

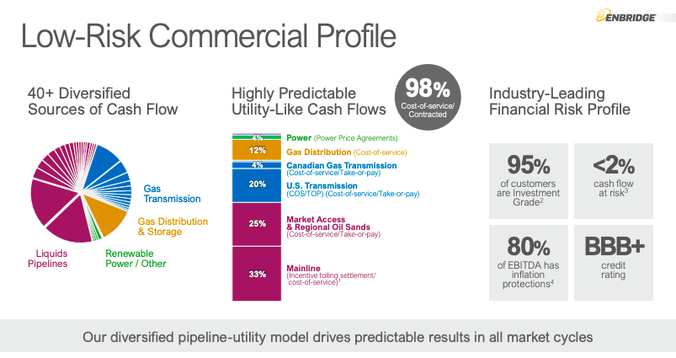

Enbridge (ENB.TSE)

Enbridge owns and operates the largest footprint of crude oil and liquid hydrocarbon systems in North America. They are currently responsible for transporting about 25% of crude oil produced in North America and almost 20% of natural gas consumed in the US. ENB operates the world’s longest crude oil and liquids transportation system, spanning 17,809 miles. Enbridge is the only energy infrastructure company that operates a massive pipeline network while also having its own gas utility company and large renewable energy portfolio.

The continuing conflict in Ukraine has put energy in the spotlight and, as much as society wants to move away from fossil fuels, we are finally starting to accept how critical oil and gas is (at least in the transition period). The pipelines that transport oil and gas are essential pieces of infrastructure, without them homes would struggle to keep the lights on. New England is a great example of how critical these pipelines truly are. In winter the area is largely covered by snow, making their solar panels somewhat redundant. Renewables aren’t yet as reliable as people think and, without oil and gas, New England would struggle to power its cities.

Enbridge is a secure, high-yielding dividend icon with 27 years of consecutive increases, the current dividend yield being 6.2%. Enbridge is also investing in renewable power projects, primarily wind and hydrogen, which is positioning them with a strong portfolio of critical energy infrastructure to service the world’s evolving energy needs.

Source: ENB company filings

Disclaimer: Quanta Services, Union Pacific, Amada, KLA and Enbridge are all currently held in the TAMIM Fund: Global High Conviction portfolio.

Source: Robert J. Shiller, National Bureau of Economic Research

Source: Robert J. Shiller, National Bureau of Economic Research

Author: Robert Swift

Author: Robert Swift

Union Pacific Corporation, through subsidiary Union Pacific Railroad Company, operates in the railroad business in the United States. Union Pacific is the second-largest railroad in the United States after BNSF Railway. The company offers transportation services for grain and grain products, fertilizers, food and refrigerated products, as well as coal and petroleum products (amongst others).

Union Pacific Corporation, through subsidiary Union Pacific Railroad Company, operates in the railroad business in the United States. Union Pacific is the second-largest railroad in the United States after BNSF Railway. The company offers transportation services for grain and grain products, fertilizers, food and refrigerated products, as well as coal and petroleum products (amongst others). Source: IC Insights

Source: IC Insights