Attempting to time the market perfectly is typically a fools game. That said, it can certainly help to know what to look for when trying to identify the bottom. So, what signs are we looking for?

From March 2020 to mid-2021, Australian investors were treated to an impressive rally of almost 60% following the market’s COVID-lows.

So far, 2022 has proved far less generous with the S&P/ASX All Ords falling by as much as 15% since peaking in August last year.

However, last week felt like 2020 all over again – not just because the virus is ramping back up with talks of returning to mask mandates and the like, but because of all the green in the market. The ASX recorded its strongest week in four months, led by the banks, miners and tech stocks.

The question now is whether we’ve seen the bottom of the market, or is this just a bear market rally with further pain ahead?

No one knows for certain what lies ahead, but there are a number of factors that might just provide us with a clue of what’s to come. So, here are some things to look for that might signal that fear has peaked and the market has bottomed.

Peaking interest rates

Historically, markets don’t tend to bottom until interest rates stop rising and central banks adopt more dovish monetary policy.

At its July meeting, the RBA lifted the cash rate for the third consecutive month. It now sits at 1.35% after rising from an all-time low of 0.1%. The RBA meets again on Tuesday and another rise is widely expected.

The RBA has said that further steps to normalise monetary conditions in Australia would be taken over the months ahead. They believe that the current rate remains too low, particularly considering that inflation remains unacceptably high and the unemployment rate is at fifty year lows.

If inflation does moderate and interest rates are increased only modestly, the market may soon recover. But if inflation remains high, the RBA may have to keep raising rates (making a recession possibly unavoidable) and the sharemarket will remain volatile.

Based on current RBA predictions, the cash rate is expected to reach a peak of around 2.5%, with inflation expected to reach around 7% by the end of year and not fall until early in 2023.

The market is forward looking and has priced this information in already. The risk lies in whether inflation continues to increase unabated or if the RBA makes a policy error by hiking rates too high despite inflation pressures having abated. This leads us to our next point.

Market capitulation & extreme fear

One sign that the bottom is near would be market capitulation – the point at which extreme fear enters the market and investors give up on trying to recapture lost gains from falling stock prices. At this point markets tend bottom out and subsequently recover once there is no longer fear.

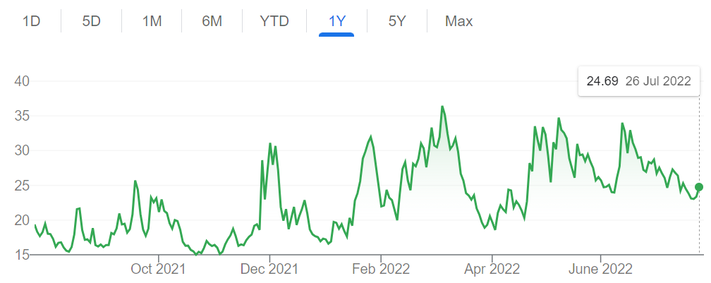

This can be seen by a spike in the VIX or “fear index”, which measures the expected volatility of the US stock market over the coming thirty days. When the market capitulates there will be a corresponding spike in the VIX.

Source: Google Finance

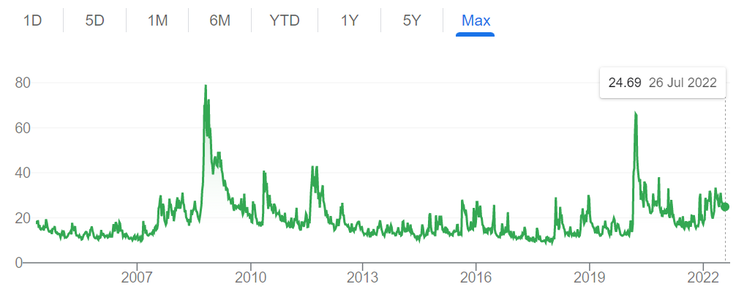

Currently, the VIX is elevated but there has been no significant spike. Below you can see what significant spikes look like, those two peaks being 24 October 2008 and 27 March 2020.

Source: Google Finance

We are yet to see panic selling in the US or in the Australian market, where a ‘buy the dip’ mentality seemingly persists instead. So, while market volatility may remain for some time still, it’s not pointing to another massive market crash.

Decline in company earnings

The current reporting season will be important to watch to get an idea of how companies are coping in this inflationary and rising rate environment.

Earnings expectations remain high but do seem to be pulling back, possibly to do with a recent pullback in commodity prices. That said, cost pressures, labour shortages, rising interest rates and supply chain constraints also remain threats.

It’s also the start of the US reporting period, yet most companies won’t report until next week. Despite cost pressures and supply chain issues there are early signs that companies are performing better than expected, although earning growth is below longer term averages.

Keeping a close eye on company results will tell whether they are managing in this more challenging environment or if it is carrying over to hit the bottom line, which would suggest further share price declines are in store.

But rather than trying to pick the bottom, it may be better to recognise that the market could still see some volatility in the months ahead. While share prices are starting to look attractive, a strategy of not picking the bottom but rather of using weakness to average into an investment over a number of months may be the way to go.

As we have previously said: Keep it simple. Keep it disciplined. Keep it rational.

A quick Google search for investing news provides 20+ sensationalist headlines. Interest rate changes, inflation, market cycles and quarterly updates provide media and marketers with an abundance of topics to craft clickbait with the intent of attracting eyeballs to their product. So, how do we approach this?

So much of the focus in investing media and discussion centres on what can be done in the short term: finding the next big winner, the newest trend, the latest current event impacting today’s stock prices. Little of the minutiae presented will actually help you invest better – the overload of fast information with a short shelf-life can so easily leave our minds scattered.

In the effort to become a better investor, it is natural and intuitive to search for more information, what more to do or what more can be added. It may be surprising to many, but the best predictors of financial success over a lifetime are often consistent simple behaviours (i.e. your long-term habits), rather than stratospheric stock picks. The problem is that many people know the fundamentals of what to do, and yet still don’t succeed.

In fact, financial success is one of the few, if not only, fields where a nonchalant everyday person can outperform a high-flying professional simply by out-behaving them. You’ve heard the story before: an 80-something year old janitor leaves behind a multi-million dollar fortune nobody knew about while a Wall St “pro” has to sell his yacht and declare bankruptcy.

The fortune was created by a consistent, simple investing approach underpinned by a few straightforward character traits that allowed compounding to work its magic over a long period of time. The outcome of harnessing the power of compounding for a long time is profound, even with average returns.

As most readers would find a “what to do” list redundant, let’s try a different approach based on one of my favourite Charlie Munger-isms:

“Invert, always invert: Turn a situation or problem upside down. Look at it backward.”

Instead of looking for how to succeed, make a list of how to fail instead. Charlie Munger is widely recognised as an incredibly intelligent polymath and he freely admits his studies of historical figures is to help reduce what he calls standard stupidities. Munger finds success through avoiding errors and subtracting distractions that could interfere with his mental clarity.

Thousands of years before Munger, the Taoist philosopher Lao-Tsu wrote that the path to wisdom involves “subtracting” all unnecessary activities:

“To attain knowledge, add things every day. To attain wisdom, subtract things every day”.

Here is a quick list of seven financial behaviours to avoid. Doing so should greatly improve your prospects for success over the long run:

Spending more than you earn, overextending and taking on too much debt

Not investing at all

Constantly checking the market and your portfolio

Following headlines, advice from media and tips from friends

Constantly turning over your investments

Concentration into too few investments or di-worse-sification into too many

Letting your emotions rule

At the heart of every difficult challenge lies three tough choices:

What to pursue versus what to ignore;

What to leave in versus what to leave out; and

What to do versus what not to do.

Most people make the mistake of adding too much complexity to their investing, preoccupying themselves with the superficial and irrelevant. Focussing on the second half of each choice — what to ignore, what to leave out, what not to do — helps confront the things that could go wrong with your investments so you can lessen the chances of them happening to you.

Many of the greatest investors recognise the need to craft an environment that enables deep concentration and amplifies high performance habits. From Warren Buffett to Chuck Akre to Nick Sleep, each one has championed subtraction in order to deeply focus on what matters most to their investing practice. Buffett purposely lives and works in sleepy Omaha, away from the chaos of Wall Street. His office door remains closed and blinds shut so he can peacefully sort through annual reports without distraction. Akre, who’s firm Akre Capital Management beat the market for three decades, is based in a town with one traffic light and views of mountains. Sleep prefers a deep armchair to a desk and stores his Bloomberg Terminal (the pinnacle of fast information, stock prices and alerts) on a low table in a corner of a room separate to his office, making it uncomfortable to be there for long.

As the best investors show, it is not addition but subtraction that is key to sustained excellence.

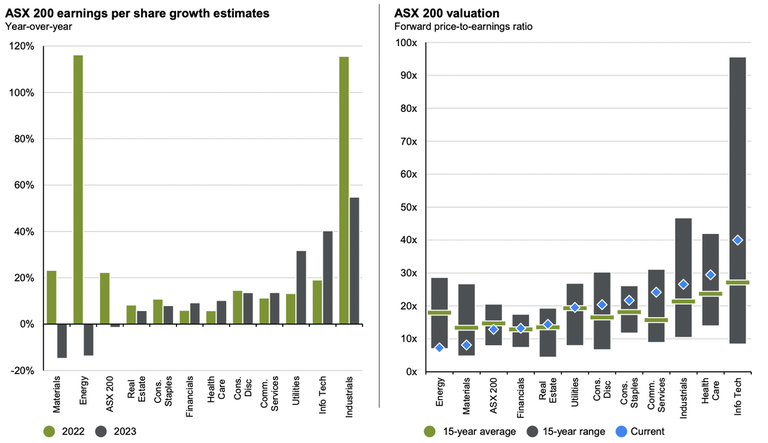

The August reporting season is just around the corner; a time when the majority of ASX-listed businesses will provide FY22 results. With that in mind, we provide an overview of what to expect, how certain sectors will perform and where the market might be getting it wrong.

The most exciting month on the investing calendar is upon us. Earnings season will begin in August, with the majority of ASX-listed businesses providing the market with FY22 results and critical information about earnings going forward. With that in mind, we provide an overview of what to expect, how certain sectors will perform and where the market might be getting it wrong.

What goes up, must come down

The pandemic created an almost perfect storm for the consumer discretionary sector, particularly retailers. No dining out. Those who could worked from home. Travel was off the table. And that’s before including government stimulus payments and record low-interest rates. Subsequently, the savings rate topped a historic high of 20%.

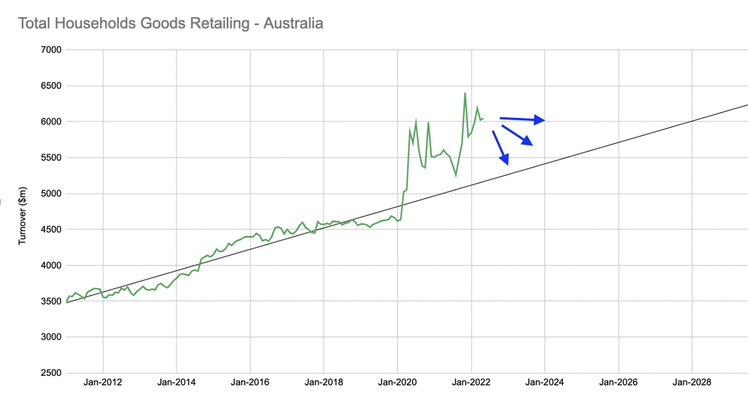

The one thing consumers could spend on was household goods such as couches, electronics and homewares. As a result, total goods spending reached levels not expected until 2028 resulting in a boom for Australian retailers.

Source: ABS, Author’s calculations

Retailers generally have a lot of fixed expenses. Therefore when sales increase, profits increase by a relatively higher amount. To illustrate, just a 13% increase in sales at JB Hi-Fi (JBH.ASX) led to a 67% jump in FY21 profits.

But what goes up, must come down. The market has already begun to price in falls, with the S&P/ASX 200 Consumer Discretionary index down -20% this year. Households simply aren’t going to buy a second lounge couch or another monitor screen. The latest Westpac-MI Consumer survey confirmed consumers are 26% less likely to purchase big-ticket items than one year ago. Goods spending growth will normalise, possibly even decline.

The operating leverage retailers benefitted from will also unwind. Third quarter sales at Kogan.com (KGN.ASX) fell -8%, however gross profit sunk -20% and net profit -164% (it went from positive to negative).

It’s not however all bad news. The resulting impact on individual retailers will vary. On Tuesday, JB Hi-Fi reported a 7.7% profit increase for FY22. Cumulatively, that’s an 80% earnings jump since 2020. Given how far consumer discretionary share prices have fallen, it could prove an opportune time to pick high-quality retailers. Investors should remain cautious as elevated pandemic numbers and economic conditions normalise though.

Inflation to hit earnings estimates

In the most recent McDonald’s (MCD.NYSE) earnings call, inflation was mentioned on 25 occasions. On the same call a year ago, it was mentioned just once. With hindsight, an inflationary spike was inevitable. Factories and offices were literally shut down. Supply chains were choked. Poor weather conditions contributed to a global food shortage. And that’s all before Russia invaded Ukraine and threw Europe into chaos. Subsequently, commodity and input prices soared.

The RBA predicts inflation will reach 7% by year-end while in the United States it’s already hit 9.1%. Put simply, inflation eats away at purchasing power. Consumers trade-down to less expensive items, while prioritising needs over wants. Corporates are forced to either raise prices and risk losing market share or absorb the cost increase and take a hit to margins.

Exemplifying the pressure on margins, quarterly input costs increased 4.8 per cent compared to just a 2.3 per cent increase in final product prices.

Even wages, after years of languishing, are starting to see growth. It remains negative in real terms, but the need for skilled labour is a key concern for Australian companies. Around 62% of large businesses are having difficulty finding suitable staff, while 40% of firms reported wage growth exceeding 3%.

Source: J.P. Morgan

It’s not unrealistic to suggest the average Australian company is facing an annual increase of 5-10% in operating costs going into FY23. Unless businesses have pricing power, margins will be squeezed. With the ASX 200 expecting earnings estimates to remain flat on FY21, this implies more downside than upside to analyst expectations. Judging by the implied sector growth rates, those most at risk are Industrials, Utilities, Communications and the aforementioned Consumer Discretionary.

One sector well positioned in a rising inflation environment is healthcare. Typically medical companies pass through increased costs given the essential nature of their products. CSL (CSL.ASX) has already banked 80% of its earnings in the first half of FY22, leaving potential upside in its August result. Elective providers Cochlear (COH.ASX) and ResMed (RMD.ASX) will benefit from economies reopening and patients returning to clinicians.

Despite having the lowest estimates, Materials and Energy are not immune to cost headwinds. Rio Tinto (RIO.ASX) recently flagged US$400 million in inflation impacts. Whitehaven Coal’s cost of production increased 13.5 per cent compared to FY21. The reason this isn’t making more headlines is that commodity prices have risen exponentially over FY22, which should lead to another solid year for the sector.

In recent weeks signs of weakness have appeared as prices begin to roll over. As we have written previously (See: Commodities: An Abundance of Policy Missteps) the supply crunch is likely to persist for the time being. But with costs on the up and prices falling, FY23 will be a more difficult period for producers.

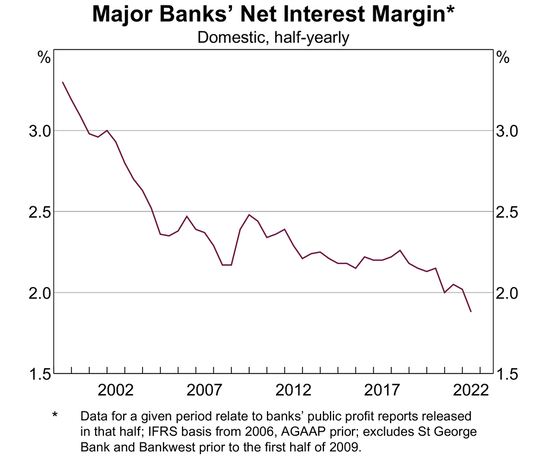

Interest rates a double-edged sword for banks

For decades Australian banks have complained about deteriorating net interest margins (NIM) due to the impact of falling interest rates.

In simple terms, banks earn revenue from the difference between the interest rate charged to borrowers (mortgages, business loans) and the cost of funding loans (deposits, hybrids, bonds). The spread between the two rates is referred to as the NIM. As rates have fallen, competition has become more fierce and NIMs subsequently contracted.

Source: Reserve Bank of Australia

For the first time since 2009, interest rates are on the way up. Typically banks will pass through the full cash rate increase to borrowers, but retain some of the rate rises for depositors. Subsequently, the NIM expands and earnings are boosted.

While this might sound rosy, it fails to account for the impact on the economy. The RBA is raising the cash rate rapidly to slow demand and bring inflation back to more acceptable levels.

The flow on impact is that the serviceability of existing loans becomes more difficult as the interest component increases. Per the RBA, a 3% increase in interest rates would result in at least a 30% increase in borrowing costs for two in five households. It’s likely that the cash rate is at 1.85% by the start of August, potentially leading over-leveraged borrowers to fall into arrears.

Additionally, households and businesses become less optimistic about the economy. Home prices are falling (See: House Prices: How Far Will They Fall?). And the higher cost of debt reduces the incentive to invest. Credit activity subsequently slows and banks compete more fiercely for a shrinking pie.

Ultimately it will depend on how high the RBA needs to push to quell inflation. The economy is in a strong position with unemployment at 3.5%. Moreover, corporates have never been more profitable. It’s going to take some serious demand destruction to reign in inflation.

Due to the uncertain economic environment, banks will likely adopt a more conservative outlook. Credit provisions could increase, which will weigh on earnings and subsequently dividends.

Wrapping up

Given inflation and interest concerns have only really come to the fore in March, it is likely most corporates report another strong set of results in August. However, the key will be earnings outlooks. Will management teams provide guidance? What does the cost base look like? Are balance sheets stretched with too much debt as rates rise? Can price rises be pushed through? The answers will decide if earnings estimates are too high or low, and likely where the direction of where the ASX heads next.

Disclaimer: RIO is currently held in TAMIM portfolios.

Special situations in investing are potentially lucrative, aming to seize short term opportunities for outsized gains, but not always easy to identify. This week we take a look at three types of these situations.

When you hear value investing you probably think Warren Buffet and Berkshire Hathaway; growth investing might conjure the more recent example of Cathie Wood and her ARK Innovation (ARKK.NYSE) fund and on the more exotic end, quant investing may bring to mind Jim Simons and the Renaissance Technologies’ Medallion fund.

There is, however, another breed of lesser discussed investor; the special situations investor. These investors look to profit, in the short term, from opportunities that present themselves. There are myriad opportunities but we will examine three common ones.

Merger Arbitrage

This is a classic special situation; one company makes an offer for another and the target’s share price rises but trades below the offer price. The opportunity is in buying the target, riding the price up till the deal closes and harvesting the difference. Typically, as conditions to close (successful due diligence by the acquirer; approval from shareholders of the acquiree; regulatory approval if required etc) are ticked off the market price will converge to the deal price.

The acquisition of TAMIM holding Uniti Group Limited (UWL.ASX) was a text book merger arbitrage opportunity. A telecommunications and digital infrastructure entity holding infrastructure assets that have been in demand with several similar entities acquired in 2021.

The below chart shows the share price (SP) movement from $4.12, when UWL first mentioned discussions with parties in relation to a takeover, to $4.99 after a binding scheme implementation deed was signed, a 21% gain in just under three months.

Not all mergers are created equal. On the other end of the scale is Elon Musk’s bid for Twitter (TWTR.NYSE). When he emerged as the largest shareholder the price was $49 and a merger agreement was subsequently signed for $54.20. Musk has since sought to terminate the deal and the SP is currently in the mid $30s. A world of pain (so far) for those who tried to arbitrage to $54.20 but is it NOW a great merger arbitrage opportunity? Plenty to play out still and a lot for any investor to ponder in that trade.

Geopolitical Events

Large scale global events can have material effects on markets and particular companies. Let’s take the current war in Ukraine as an example.

On 10 November 2021, the United States reported an unusual movement of Russian troops near the border of Ukraine. By 28 November, Ukraine had reported a build-up of 92,000 Russian troops.

On 7 December, US President Joe Biden warned President of Russia, Vladimir Putin of “strong economic and other measures” if Russia attacked Ukraine. This signalled the willingness of the United States to assist, potentially militarily through supplying weaponry. This was bullish for American defence contractors with Lockheed Martin (LMT.NYSE): and Raytheon Technologies (RTX.NYSE) two of the leading firms in the space.

The chart below shows the SP performance of the two entities with the eventuation of the invasion on 24 February 2022, providing a good exit with returns dependent on how early (brave) you entered the trade. This trade was also counter to prevailing market conditions, providing an even greater relative return.

Product/Service Specific

Sometimes a particular product or service can be impacted by supply and/or demand dynamics which create an opportunity. Earlier in 2022 an infant formula shortage gripped the United States. This provided an opportunity for other nations/companies to assist in filling the void. The two best known infant formula (IF) companies on the ASX are The a2 Milk Company (A2M.ASX) and Bubs Australia (BUB.ASX).

The shortage was due to the compounding of a number of issues:

Historical import restrictions

Supply chain disruptions due to Covid-19 (2021)

Large scale recall and shut down of a factory of one of the three major US producers, Abbott Laboratories (ABT.NYSE), in February 2022

The recall would have had some special situation investors taking notice as that took things from difficult to crisis point.

Out of stock rates for IF are normally 10% but by the end of April had risen to ~30%; mid-May to 43% and 70% by the end of May. On 30 May 2022 BUB announced it had been granted immediate permission to import infant formula into the USA and had an agreement with the Biden administration to provide at least 1.25m tins. The share price rose 40% that day, providing an exit.

Note however, that A2M was in a down trend all year (also dealing with issues like a covid-exposed reliance on the Chinese market and Diagou trade and class action lawsuits) and by the end of June was 30% down from the start of the year. Special situations are certainly not risk free.

In 2021, a similar trade (based on demand of a service) was buying Australian Clinical Labs (ACL.ASX) as COVID intensified in Australia and demand for (government subsidised) PCR testing skyrocketed.

Summary

As we have seen, special situations come in many forms. The intention is to profit in the short term which can deliver outsized returns, sometimes counter to the market trend. That said, there are risks involved both idiosyncratic (i.e. the company you invest in may have issues specific to itself that derail the investment) and systematic (i.e. prevailing market conditions increase the likelihood of failure e.g. A2M).

Finally, it’s important to keep in mind your thesis and realise your gains when the special situation plays out or, if it doesn’t, cut your losses.

Disclaimer: UWL is currently held in TAMIM portfolios.

When it comes to investing, many know the value in identifying stocks with a big moat. Giants like Buffett and Munger maintain that this has been a crucial part of their success, but how can we identify one of these moats in the making?

In the wake of the ruins brought by World War 1, the French government vowed to protect its vulnerable northeast border with Germany from any future attacks. With horrid memories of fighting and living in open-air trenches, the French spent a decade building a 482-kilometre series of fortifications that would be both impenetrable and comfortable to live in.

The monumental concrete glory, known as the “Maginot Line”, included 142 large artillery forts, 352 fortified gun emplacements and 5,000 smaller bunkers (or pillboxes). Behind the imposing line of fixed defensive positions, tank traps and high concrete walls were fully equipped subterranean bases complete with mess halls, hospitals, recreation facilities and railway lines.

The Maginot Line was thought to be impenetrable and would prevent any WW1-style infantry and artillery attack. At the beginning of World War II, however, it wasn’t able to stop the Nazi war machine from quickly overwhelming and occupying France. The Germans quickly abandoned older tactics for a far more mobile and manoeuvrable attack that disrupted and dismantled the French defensive strategy.

The Oracle of Omaha: Warren Buffett

For decades, Warren Buffett and Charlie Munger have taught all who will listen that a crucial ingredient to their investing success has been finding companies with a big “moat”. An economic moat is the same concept as a moat around a mediaeval castle. It is about protection and long-term survival, preventing other businesses from stealing away a company’s profit margins or market share. Moats can come in different forms: network effects, real assets (e.g. property or infrastructure), intangible assets (such as brands or intellectual property), distribution, switching costs, price advantages and culture.

It’s not hard to see how a huge defensive wall around a business to protect it from competitors might create a very attractive investment. But by focusing only on the size of the moat, investors can miss the opportunity to invest in smaller businesses disrupting the status quo: either globally, like Amazon (AMZN.NASDAQ) or Google (GOOG.NASDAQ), or locally, like REA Group (REA.ASX) or Jumbo Interactive (JIN.ASX). Competition is a potent force in capitalist societies, and mature businesses that once had seemingly “impenetrable” moats have been overrun by the forces of ‘creative destruction’ – think Kodak and Blockbuster.

Instead of focusing only on those mature companies with an existing moat, finding companies that are in the process of building their competitive advantage could be a boon to your portfolio. Beyond the clear-cut growth indicators like compounding revenue and increasing market share, here are some other barometers of an emerging moat:

Management reinvest capital into the business effectively

Jeff Bezos once said:

“Friends congratulate me after a quarterly-earnings announcement and say, ‘Good job, great quarter.’ And I’ll say, ‘Thank you, but that quarter was baked three years ago.’”

Amazon’s growth has been fuelled by continuous reinvestment into innovating and optimising its services. Many of its financial decisions are characterised by a preference for long-term growth instead of short-term profit chasing. Even as the company’s stock price continued to climb through the 2000s, Amazon was and continues to be known for spending big on what some investors considered bad bets, like branching into web hosting. The payoff has been a steep trajectory from a small moonshot company into a trillion dollar megacap.

Reinvestment usually comes in various forms, e.g. research and development; capital expenditure to increase capacity, enhance reliability or boost quality of product or service; and marketing to reinforce branding or gain larger mind share amongst customers. What’s important is to find a company that can continually reinvest funds and earn a high rate of return – the longer this runway, the better.

Destination focussed, avoiding the pursuit of short-term goals

Costco’s (COST.NASDAQ) retail concept is simple: customers pay an annual membership fee which provides entry to the stores for a year, and in exchange Costco operates an every-day-low-pricing strategy by marking up its goods significantly less than competitors (branded goods by only 14% and private label goods by 15%). By sticking to a standard mark-up, savings achieved through purchasing or scale are returned to the customer in the form of lower prices, which in turn encourages more consumers to sign up and buy more products, and extends the scale advantages. This is retail’s version of perpetual motion.

To appreciate the long term focus of building this flywheel, consider this story of Costco founder Jim Sinegal, recounted by well-known investor, Nick Sleep in 2002.

When the opportunity arose to take a higher gross margin than usual on a US$2 million shipment of designer jeans from an exporter (i.e. more than the standard 14%), Sinegal firmly insisted on refusing to break the contract with Costco’s customer, arguing with the exporter that if “I let you do it this time, you will do it again”.

Sticking to the long term destination focus of customer loyalty and footprint expansion has resulted in a 10x return on an investment in Costco from 2002 to today. The focus has firmed the brand, the stickiness of its suppliers and customers – an upward trajectory of its moat.

Alternatively, companies that either damage customer loyalty with operational pivots or reduce investment needs in order to boost short term profits are mortgaging their moats, especially if competition is spending heavily to take over its market share.

The Bottom Line

There are very few companies that last a hundred years. It is vital to evaluate where a company is in the business life-cycle and the direction of its competitive advantage. Disruptive companies can have innovative technologies or operations that are more efficient and make the old way of doing business obsolete. These companies have the potential to change or entirely displace existing businesses and industries. Like David toppling Goliath, finding a wonderful business with a growing moat could provide outstanding returns.