Investing in small-cap stocks can be a rollercoaster ride.

Aside from their ability to generate outsized returns, Micro and small caps tend to be more volatile, experience larger downturns, and have lower liquidity than their larger counterparts. And it is times like now when the markets are unpredictable, that can reveal an investor’s true risk tolerance.

Overall, sentiment was quite negative towards equities during 2022 and has been this way again in the past month. In fact, a recent survey by JP Morgan suggested that people were shying away from equities altogether, with just 29% of clients planning to increase their equities exposure in 2023, the lowest in several years.

Moreover, it’s been a particularly tough time at the smaller end of town. For reference, the S&P/ASX Emerging Companies Index is down 24.3% over the past 12 months, and 26% from all-time highs in January of last year.

However, it is at this exact time that fortunes can be made. There’s a plethora of analogies that famous investors tout to help everyday shareholders withstand the natural vicissitudes of the stock market:

The big money is not in the buying and the selling, but in the waiting

In the short run, the market is a voting machine but in the long run, it is a weighing machine

The short term is unknowable, but the long term is inevitable.

And so on…

Those with enough experience and equanimity know that history is on your side if you’re a patient, long-term investor. So if you haven’t adjusted your allocation to small caps, now might be the ideal opportunity.

Fear not, the general outlook is encouraging

The stock market has good years and bad, but don’t let short-term dips shake your faith in the long-term trend: upwards. Despite this being a well-known fact, it never ceases to amaze us how many investors panic during so-called “bad” years.

Taking a closer look at historical share returns in the U.S. and Australia may provide some much-needed encouragement. Over nearly two centuries of research, it has been found that in the U.S., the chances of a positive return in any given year are at a solid 71%. Meanwhile, in Australia the statistics are even better.

During the 147 years of trading data available on Australian exchanges, the market has risen for 117 years and declined for only 30 years. That means 79.6% of the time, the market rises. While there may be a decline on average once every 5 years on average, it’s important to keep in mind that over the past 147 years, the market has averaged a return of 10.8% per annum, including dividends and share price growth.

And since the introduction of the Accumulation Index in 1979, the data points to an even stronger outcome. Over the past 43 years, the market has risen by an average of 13% per annum, despite some seriously scary episodes, including the 1987 stock market crash, the 1997 Asian Financial Crisis, the GFC, and the record-breaking fall caused by COVID-19.

Additionally, it’s worth noting that negative years – such as the one we just experienced in 2022 – are typically followed by a positive one. So, while the current state of affairs may seem grim, investing wisely now could pay off in the long run.

So, take a deep breath, and remember that despite the bumps along the way, the long-term trend of the stock market is upwards. Don’t let short-term fluctuations cause you to miss out on the rewards of long-term investing.

Sentiment is short-term, business performance is what matters

Negative market sentiment towards small-cap stocks isn’t purely related to the performance of the underlying businesses. So where does the selling pressure come from? For a start, larger funds and institutions are facing growing challenges to investing in small listed companies. As the giant super funds grow their funds under management by tens of billions of dollars, their ability to generate meaningful outperformance by investing in Australian small-cap stocks becomes increasingly tough.

The need to continually generate new investment ideas and implement those ideas encourages the biggest asset owners to focus on much larger companies. Additionally, as funds become bigger, they cannot invest in, nor continue to add to, positions in small caps in a meaningful size relative to their total portfolio. It is common for larger funds to invest hundreds of millions of dollars in one company. Most small caps don’t have the market cap to support these large investments – in order to buy a position large enough to make a difference in their fund’s performance, a fund manager would have to buy a significant share of a small cap company.

There have been multiple cases of institutions and funds unwinding exposure to small caps in the past two years (e.g. Rest Super). To adapt, some small-cap investment firms are rolling out mid-cap offerings as a means of staying relevant to their biggest clients.

This poses an opportunity for nimble investors who are able to identify and take advantage of these smaller investment opportunities.

Finding mispricing opportunities is easier among small caps

Investing in small caps is appealing for several reasons, one of which is it’s a less efficient market. Compared to larger companies, small caps receive less scrutiny from analysts and investors, resulting in far less attention and potential undervaluation. This inefficiency in pricing means that there may be information about small caps that are not reflected in current stock prices, making them attractive to investors who are willing to do the research.

While micro-cap investing has been described as a “killing field,” we believe that there are compelling opportunities for investors who are willing to take a long-term view.

For example, Viva Leisure Group (ASX: VVA), recently reported record results and yet its share price sits more than 30% below recent highs. The Company operates health clubs (gyms) with 166 locations across Australia and owns the largest non-franchised health club brand in the country.

With H2 FY2022 providing the company’s first six months of uninterrupted trade for several years, H1 FY2023 has continued that momentum and generated promising performance. The following highlights show the business is performing very well:

Operating earnings (EBITDA) exceeded all previous results, including all previously recorded full-year results

EBITDA margin at 20.7% for the HY showed significant improvement, exceeding H2 FY2022 by 4.3%

Revenue nearly doubled from H1 FY2022, with the start of CY2023 showing continued growth

Highest net profit (NPAT) result ever recorded

Strong Free-Cash-Flow generation, allowing the company to self-fund future growth

Network membership now over 343,000 (growing organically each month), representing 2% of the Australian population aged between 15 and 69

No sign of growth slowing due to current inflationary pressures.

The low valuation of Viva’s shares is likely driven by the stock being in ‘small-cap purgatory’ due to liquidity issues, but this is no restriction for the retail investor and we believe the company’s track record of execution makes it a compelling investment opportunity.

Another example of an unrecognised, profitable and steadily improving business is Clearview Wealth (ASX: CVW). Clearview has reported a strong financial result for the first half of 2023, with an underlying net profit of $16.3 million, which is 31% higher than the previous period. The growth was mainly driven by the life insurance segment, with a significant increase in premium income and new business. Clearview also plans to sell its managed investment business, which will result in a 40% stake in Human Financial Pty Ltd, valued at $16 million, and release $15 million of cash to strengthen its balance sheet.

Due to the strong performance, Clearview’s full-year underlying net profit after tax (NPAT) is expected to be in the range of $30 million to $32 million, excluding the Wealth Management NPAT loss of $2 million. This represents a 21-28% growth on the previous year. Clearview’s balance sheet is robust, with net assets of $476.7 million and an embedded value of $0.902 per share, including franking credits.

The company’s dividend policy remains unchanged, with a pay-out of 40-60% of underlying NPAT. The stock is currently trading at a 29% discount to its net asset per share, making it an attractive investment opportunity. With an expected earnings growth of over 20%, a price-to-earnings ratio of 11x, and a fully franked dividend yield of 4-5%, Clearview is also an attractive takeover target. The company’s strong performance and simplified business model make a takeover even more likely than in the past year when we first began covering the Company.

The TAMIM Takeaway

Investors should avoid falling into the trap of negative sentiment and instead take a closer look at the underlying businesses of their investments. Historical share returns in the US and Australia show that positive years follow negative years – the pattern is notable.

Investors should take encouragement from the wealth-building tendencies of quality businesses and remember that, ultimately, as businesses become more valuable, their share prices should follow.

Although the current mood of Mr. Market is unfavourable for micro and small-cap companies, it is crucial to keep in mind that market sentiment always turns and, when it does, small caps are likely to hit it out of the park.

Disclaimer: ASX: VVA and ASX: CVW are currently held in the TAMIM Portfolios.

One of the biggest advantages of investing part of your portfolio in the global equity markets is the ability to gain exposure to industries and specialty companies that are not as prominent in Australia. This includes the likes of luxury brands in Europe (e.g., LVMH, Ferrari), software in Canada (e.g., Constellation Software, Shopify), consumer goods in the United Kingdom (e.g., Unilever, Diageo), and in the United States, technology and insurance.

FAANG – an Opportunity in Plain Sight?

Large technology names have dominated the investment headlines in recent years, and with good reason. Facebook, Apple, Amazon, Netflix and Google are widely regarded as some of the best businesses in the post-industrial era, with enormous network effects and economies of scale, impressive revenue growth, and fortress balance sheets. While it’s tempting to look for complex, out-of-the-way situations to generate outsized investment returns, sometimes keeping it simple is the right approach and the best investment ideas are in fact right in front of you – as the saying goes, in investing you don’t get paid for complexity.

Alphabet (NASDAQ: GOOG), named as a pun about investment returns above a benchmark (‘alpha-bet’) was founded in 2015, and is best known as the holding company that houses the Google search engine. As you likely know, Google dominates the online search market. As at March 2023, it captured approximately 85% market share, compared to 9% and 3% for Bing and Yahoo! respectively (according to Statista). Online search is also a hugely profitable business. It is getting more mature though, and Google’s extremely high market share does mean that the company’s growth rate is likely to slow in coming years. This is where Alphabet’s other businesses come in. YouTube is riding the wave of people consuming an ever-greater amount of video content, both professional- and creator-produced. Google Cloud offers infrastructure, platform and other services to businesses, along with cloud-based collaboration tools such as Gmail and Google Docs. It’s the third-largest cloud services provider behind Microsoft Azure and Amazon Web Services, but it’s growing at a rapid pace. Let’s not forget the Company’s device business, which includes the likes of the Pixel, Fitbit (acquired in 2021) and the associated Play application store. Finally, there is ‘Other Bets’ – Alphabet’s venture capital and private equity operations, home to emerging companies at various stages of development including Waymo, X and GV. While currently unprofitable, Other Bets is targeting big innovative areas of the economy including health, autonomous driving, and technology.

On 2 February, Alphabet reported its financial results for both the full-year and fourth quarter of 2022. Revenue for the full year came in at US$282 billion, a 10% increase over the prior year 2021 [or 14% excluding the effects of foreign currency, as the increase in the U.S. Dollar (USD) decreased the value of international revenue translated back to its USD financials]. The currency effect was even greater in Q4, where revenue increased only 1% to US$76 billion but 7% on a constant currency basis. Inside this 1% number, Google Advertising (the biggest division that includes both Search and YouTube) declined 3.6%, an unusual but unsurprising result after a couple of blockbuster years during the pandemic. Google Cloud revenue increased 32% to $7.3 billion for the quarter, a growth rate that shows great momentum in the business and outpaced both its major competitors. Other Bets revenue also grew from US$181 million to US$226 million, although this still remains a drop in the ocean compared to US$76 billion in quarterly sales.

Expenses have been a hot topic over the past 12 months, and Alphabet’s total operating expenses expanded 8.2% to US$57.8 billion, due to higher cost of revenues and higher research and development (R&D) expenses in the quarter. R&D increased due to the Company’s artificial intelligence (AI) efforts, which are a ‘strategic priority’ for Alphabet and have been consistently called out by Alphabet CEO Sundar Pichai over the last several years (and even more recently with the launch of Bard to combat the highly-publicised ChatGPT developed by OpenAI). This meant that operating profit decreased to US$18.1 billion, from US$21.8 billion and net income fell to US$13.6 billion compared to US$20.6 billion in the prior year’s Q4. With a weakening macroeconomy and revenue growth slowing after a strong period during the pandemic, Alphabet (like many other large tech companies) is looking to reduce expenses and announced 12,000 layoffs. This has been welcomed by most investors given the increase in expenses in recent years and should provide an opportunity to significantly increase profitability going forward, as the company continues to deliver new advertising solutions, YouTube and Cloud achieve standalone profitability, and Other Bets either achieve scale or are sold/closed down.

Quiet Industry Champion Churning Higher Returns

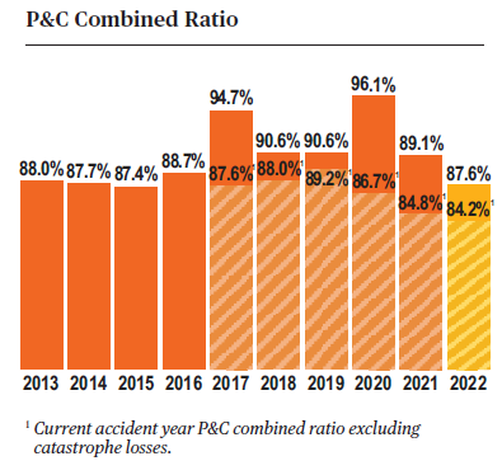

While insurance isn’t known for being stimulating or sexy, there are a number of quality insurers in the U.S. that have delivered heart-throbbing returns over the years. One such company is insurance stalwart Chubb (NYSE: CB). Operating in 54 countries and territories and employing 34,000 people worldwide, Chubb is the world’s largest publicly-traded property and casualty (P&C) insurer. It provides a range of insurance products, including commercial and personal property and casualty insurance, personal accident and supplemental health insurance, reinsurance, and life insurance. Approximately 62% of the Company’s business comes from the U.S., with 14% from Europe, Middle East and Africa (EMEA), 12% in Asia (including Australia), 6% Latin America, and the remaining 6% from Bermuda and Canada. For customers, It is known as a reliable and well-funded company with exceptional credit ratings from each of the credit rating agencies (AA from S&P, Aa3 Moody’s and A++ from insurance rating agency AM Best), and for providing prompt and fair payment of claims. For investors, Chubb is known as being a consistently profitable business with disciplined insurance underwriting, generating an average combined ratio of 90.8% over the past 5 years, and less than 100% in each of the past 10 years (The combined ratio is a commonly reported insurance metric which represents the profit on insurance underwriting relative to 100%. A combined ratio under 100% represents a profit, and over 100% indicates a loss).

Chubb reported its fourth quarter and full year 2022 financial results on February 1. Net premiums written increased 10.3% to $41.8 billion for 2022, or 13.0% excluding the impact of the strong U.S. Dollar, which reached a 20-year high in September (net premiums written are the total insurance policies written during the period, after deducting those that are ‘ceded’ to a reinsurer, meaning the risk is transferred). Q4 results were even stronger, with net written premiums up 11.9% to $10.2 billion, or 16.0% excluding currency effects. This was boosted by the acquisition of the Cigna Asian business during Q3, which led to a 92.0% increase (100.8% in constant dollars) in life insurance premiums in Q4.

Profitability was again a highlight for Chubb, with the combined ratio coming in at 87.6% for 2022 versus 89.1% in 2021, and 88.0% for Q4. Chubb, like most insurers, also provides certain adjusted (or ‘but for’) numbers that exclude the effects of various ‘one-off’ events such as natural catastrophes, but which are arguably part of the cost of doing business as an insurance company. One of the few beneficiaries of higher interest rates, net investment income was a record in both Q4 (rising 23.6% to $1.12 billion) and the 2022 full year (up 8.2% to $4.02 billion). One of the few minor blemishes was a $107 million underwriting loss in the North American Agriculture division. This is unlikely to be the cause of the share price fall on the day, though, which is more likely the result of commentary on the earnings call regarding a moderating in insurance pricing. Insurance has been in a hard market for several years (meaning that prices have been rising), and this a key focus for investors. Given higher inflation and increased catastrophe losses though, most insurers seem intent on higher prices at least in the short term, which should bode well for insurance companies such as Chubb.

No Time Like the Present?

While it might be a psychological struggle to think about investing overseas when the Australian Dollar has been a bit weaker of late, the ASX only constitutes about 2% of the global equity opportunity and has a large concentration in banking, resources, and supermarkets. Looking globally can give you unique exposure to high-quality businesses and industries that are simply not available on the local bourse. Additionally, volatile share markets are often the perfect opportunity to acquire shares in high-quality companies, and with Alphabet and Chubb down around 32% and 18% from their highs, now might be just the time.

The age-old investing wisdom was always to maintain a portfolio consisting of 60% equities and 40% bonds (commonly referred to as the “60/40 portfolio”). Bonds have been out of favour since the Global Financial Crisis though, as TINA (“there is no alternative”) took over and investors piled into more risky assets.

The main reason for this was the incredibly high prices, or inversely, the incredibly low yields that bonds offered investors for most of the past 15 years. (The price and yield of a bond are inversely related. For example, when the yield of a bond increases from 1% to 2%, the price of that bond falls). In fact, bond prices (yields) had steadily increased (declined) for about 30 years up until 2020.

Notorious Bonds and the Tale of Silicon Valley Bank

This has been a hot topic of late given the collapse of several U.S. banks, including the high profile failure of Silicon Valley Bank (SIVB). SIVB had a large portion of its balance sheet invested in long-term bonds, predominantly mortgage-backed securities with a 10-year duration. Without getting too much into the weeds, the main issue here was that these bonds were purchased during the pandemic at extremely high prices (with yields of 1.70% to 1.80%, for example). During this time, central banks such as the U.S. Federal Reserve and the Reserve Bank of Australia had cut benchmark interest rates and implemented other measures such as quantitative easing to lower interest rates, stimulate the economy, and reduce the risk of deflation. This was quite effective, and the yields on fixed income securities fell sharply. With a huge influx of deposits from a boom in technology, venture capital and special purpose acquisition companies (SPACs), along with very little loan demand, SIVB’s management felt that they had very little option but to invest in these otherwise “safe” (but expensive) securities.

Fast forward to 2022 and the economic environment is vastly different: restrictions on movement have eased, the economy has roared back to life and central banks now have to combat the challenges of low unemployment and higher levels of inflation. As a result, they rapidly increased interest rates – at the fastest rate on record. Higher market interest rates cause these bonds offering low yields to significantly decline in value. Simultaneously, SIVB’s deposits begin to decline as the bank’s clients fall on harder economic times and have a greater need to use their funds. Eventually, SIVB needed to sell a portion of its bond portfolio, which at today’s interest rates, were worth substantially less than when the bank purchased them.

Are Bonds Lower Risk?

Putting the extreme example above to one side for a moment, bonds are widely regarded as being a less risky asset class than shares. There are two main reasons for this. Firstly, bondholders are legally entitled to receive a regular fixed payment (with the exception of zero-coupon bonds, which are discussed more below). This differs from a dividend for shareholders, which is optional and can be modified or eliminated at the discretion of the Board of Directors (although they generally try to avoid this circumstance). Secondly, in the event of bankruptcy, bondholders are entitled to receive proceeds from the remaining funds before shareholders – who are typically last in the capital structure. (While this is not always the case and we did see a special situation this week with holders of Credit Suisse’s additional tier 1 or “AT1” securities wiped out while equity holders stayed afloat in the takeover by UBS, it is generally true. It certainly pays to read through the details contained in a prospectus, even though they can sometimes be more than 600 pages long!).

How Do I Make Money from a Bond?

The bond market is enormous (much bigger than the equity market) and there is huge variety in the types of fixed income securities available: hybrids, convertibles, some with warrants attached, et cetera. However, sticking with some of the more basic vanilla bonds for now, there are a few main types.

Zero Coupon Bonds: the bond is issued at a discount to par (e.g., 97%) and the investor receives the full amount at the maturity date (e.g., 100%).

Fixed rate securities: similar to a term deposit from a bank, these pay interest in the form of coupons on a regular basis and the principal (initial capital investment) is returned to the investor at the maturity date;

Floating rate securities or floating rate notes (FRNs): pay interest based on a benchmark rate that changes over time. This benchmark is often the Bank Bill Swap Rate (BBSW), which is basically the rate at which banks borrow from each other for different periods of time. The spread (or the margin over the benchmark) is set at the beginning. As with fixed rate securities, the principal is returned to the investor at the maturity date.

Index-linked securities: similar to FRNs, these pay a variable interest rate based on an inflation index such as the Consumer Price Index (CPI). They can be capital-indexed bonds (where the initial capital investment is increased according to the index) or index annuity bonds (which are similar to mortgages, where the investor receives regular payments that include both principal and interest).

In addition to receiving the coupon payments and/or higher capital amount at maturity, investors can also profit if market interest rates decline. Lower interest rates increase the value of certain bonds (such as fixed rate and zero-coupon securities), and instead of holding the bond to maturity, an investor may be able to sell the bond in the secondary market for a profit.

Who Issues Bonds?

Both governments and large corporations issue bonds, while smaller companies (like consumers) typically do most of their borrowing from banks. Governments such as Australia (who maintain their own currency and borrow in that currency) are largely considered ‘risk-free’ because they can always increase taxes to pay off any debts. The U.S. government is the largest issuer globally, and investors can buy securities ranging from 1 month through to 30 years (collectively referred to as the ‘yield curve’). There is also a larger market for corporate bonds in the U.S., while in Australia it is mostly limited to the ASX 50, including companies like the big four banks and the largest mining and infrastructure stocks. The interest rates that these companies pay are based on their perceived risk, which commonly involves a premium or margin over the government bond rate (referred to as a ‘credit spread’).

Alphabet Soup – Is Your Bond Investment Grade?

Fixed income securities are given a grading by credit rating agencies Standard & Poor’s (S&P), Moody’s and the lesser-known Fitch. S&P/Moody’s copped a lot of flak for their performance during the GFC, however, one clear trend from their track records is that companies that are given a grading of “investment grade” (BBB- for S&P/Fitch, Baa3 for Moody’s) are much less likely to default (meaning investors don’t receive all of their interest or principal payments). As a result, companies that do not receive an investment grade rating pay much higher interest rates. The securities issued by these companies are often called ‘high yield’ or ‘junk’ bonds, and have become increasingly popular from both companies and investors, including billionaire Howard Marks. While some sub-investment grade companies are high-quality (often emerging) businesses, caveat emptor.

No Time Like the Present?

The rapid rise in interest rates over the past year has finally provided investors with more attractive yields on fixed income securities. While the world of bonds might seem complex at first (and there is a huge variety of options, some with very detailed provisions), now might be the time to introduce yourself to the more ‘plain vanilla’ types and consider adding a portion to your portfolio. As investors, management and stakeholders in Silicon Valley Bank can attest, it’s important though to consider the price (yield) on offer, and importantly, how that compares to inflation.