The managers of the TAMIM Australian Equity Small Cap Individually Managed Account (IMA), take a look at the importance of understanding the psychology of other players in the market and reveal where they look to gauge what others are thinking and how this informs their investment decisions.

Gauging Market Expectations

Summary:

Understanding what the market is expecting from a company is a key input in our investment process. We are looking for under-appreciated stocks where the valuation reflects the market’s low expectations for the business. As a result, we look to gauge market expectations before investing and look to forums, broker reports, investor discussions and subscription research services to better understand what the market is really expecting from a company. In our experience, understanding behavioral finance allows for a more accurate interpretation of market commentary.

Start with the stock’s valuation:

The market’s opinion on any given stock is clear for all to see in the form of the current stock price which in theory represents the current value of expected future cash flows. As a result, we view a stock’s current valuation as a great starting point in gauging what the market is expecting from a company looking forward.

As passionate value investors we are always looking for stocks which are trading significantly below their intrinsic value, which encapsulates that company’s future cash flows discounted back to a present value. Stocks which trade well below their intrinsic value generally do so because their shareholders have low expectations of future cash flows, and thus value the business accordingly.

As a result, gauging market expectations is a key part of our value investment process.

The smaller companies market is inefficient:

One of the great attractions of investing in smaller companies is the inefficient nature of the smaller companies’ market. There are far fewer analysts and investors looking at each stock at this end of the market, which creates a significant opportunity for smaller companies’ investors who are prepared work hard to fill in the information gaps themselves. These market inefficiencies mean we need to work harder than just looking at the stock price to gauge what the market is really thinking. We need to listen to the market…

Listen to the loudest opinions and take them with a grain of salt:

We are believers in the power of using behavioral finance to your advantage when investing. In our experience listening to market voices can add significant value when gauging market expectations. However, not for the reasons you may think.

Any psychology graduate will recognise that when people are expressing particularly loud and strong opinions about something there is generally a deeply held personal reason for it. In our experience, when someone is talking particularly positively about a stock, it generally means they are invested in the stock and are thus comfortable to “talk the stock up”. And conversely, when someone is negative about a stock, it generally means they aren’t invested in that stock and thus feel comfortable to “talk the stock down”, possibly so they can buy the stock at a lower price in the future.

Knowing why people are broadcasting their opinions can be a useful tool when gauging market expectations, particularly in the small world of smaller companies investing. If, for example, five of Australia’s leading smaller companies fund managers are all invested in the same stock (which is incidentally a more common occurrence than you may think!), and have all published positive research updates recently, the chances are high that expectations are high. Those five fund managers are likely to have already built their positions in this stock, and by broadcasting their opinions loudly across the market, the chances are high that some retail investors have followed the “smart” money into this stock as well. In this scenario, we would be cautious regarding the stock’s short and long term potential knowing that the incremental buying is likely to slow down looking forward, and also that once that happens some of the more short-term focused retail buyers are likely to sell down once the stock starts under-performing, leading to further under-performance.

By knowing that expectations were high in this example, an investor would have been in possession of a significant advantage versus the broader market.

Where are the loud voices to be interpreted?

We pay attention to the opinions from across the market and see 4 main communication channels as worth factoring into expectation analysis:

Read stock message boards like Hotcopper – Hotcopper provides a fascinating insight into what people want you to think they are thinking, and provides a forum for the loudest opinions to be broadcast across the market. In our experience, stocks which have many Hotcopper postings each day tend to be followed closely by short term focused investors/traders. The more people are discussing a stock, the more they are generally hoping from that stock in the short and long term, and vice versa. We tend to be invested in stocks where there is minimal commentary on Hotcopper since few people follow or understand them.

Talk with other investors – Similarly to Hotcopper, it is interesting to talk with other investors and take what they are saying with a grain of salt. Of particular interest to us is when many investors are talking about the same stock/s, which tends to indicate expectations are rising.

Follow broker analysis – At the smaller companies end of the market it is generally uncommon for brokers to write regular research updates so following broker research can be of marginal use. However, in the rare cases it does happen, we are aware that expectations may be rising as a stock continues on its journey from undiscovered to discovered.

Follow subscription research services like Motley Fool – Some of these subscription research services advise many thousands of investors, and they are often looking at the smaller companies end of the market. It can be worth being aware of their recommendations in stocks you are following because they can significantly impact upon expectations and the type of shareholder on the register.

Management engagement and communication.

We have noticed that management communication is also very important when gauging market expectations. There is a spectrum of management communication styles across the market, and in our experience management teams which focused on under-promising and over-delivering tend to do just that. And they also tend to attract stable long term shareholders who are taking a truly long term view on the investment, rather than aiming to trade in and out around results. In our experience this is the ideal type of shareholder register to support long term value creation.

We encountered an interesting example of management communication behavior we aim to avoid recently when we noticed the CEO of a company we were analysing (who will remain nameless) was communicating directly with investors through Hotcopper on an almost daily basis. The following quotes are indicative of his communication style:

“It’s time to put your seat belts on and enjoy the ride and for those that got in at these price levels…… well done!”

“Further news flow should see this break out.”

Needless to say the stock has attracted a highly speculative and short term news-flow focused shareholder register. We believe this may create challenges for the stock’s short and long term outlook as expectations are already high, with many shareholders in a hurry for results.

Use the noise to ultimately ignore the noise: Think long term:

Buffet’s famous quote couldn’t be more accurate in our experience. Markets will always be driven by greed and fear, and it is only by mastering our emotions as investors that allow ourselves to be exposed to significant wealth creation opportunities in the equity markets.

We believe being aware of market expectations and the behavioral finance implications are powerful tools investors can use to ensure they are exposed to the right type of stocks which they are able to think long term about, and ultimately ignore all the short term noise.

Conclusion:

Gauging expectations is core to value investors’ psyches since we are looking for stocks which are largely ignored and under-appreciated, and thus under-valued. Low expectations is near the top of our shopping list of the attributes of high quality, under-valued smaller companies we are looking for. We will continue to focus on stocks where expectations are low.

Karl Hunt & Roger McIntosh, of the TAMIM Global Equity High Conviction Individually Managed Account (IMA), take a look at portfolio holding Randstad Holding HV.

Stock Report – Randstad Holding NV (RAND.AMS) Karl Hunt & Roger McIntosh

Randstad Holding NV (Randstad) is a recruitment and human resources consulting business based and listed in the Netherlands. This is a company we purchased early last year in February believing that it was a good vehicle to benefit from a European economic recovery. The company has operations throughout the world in three key areas, professional recruitment, temporary recruitment and human resources consulting services.

Recruitment agencies are a good bell weather to check the temperature of economies and a timely indication of where markets are in the economic cycle.

Within its industry group of Commercial & Professional Services we evaluate it globally as being the best rated company and within the broader Industrial economic sector grouping it is 13th out of 320 companies.

We first took a position in Randstad in February 2016 and following further review of both the company and broader European signals, increased our exposure to an overweight position in August 2016. It ranks very highly on our price momentum model and very highly on quality measures such as low debt to total assets, very high interest coverage and expected return on equity, relative to its industry group and the broader market.

Over the last 6 month to its most recent reporting date, Randstad has outperformed the broader European market by around 30% in local currency terms.

Source: Thomson Reuters

Randstad reported Q4 2016 results last week, beating analysts’ expectations and confirming continued economic recovery in Europe which makes up 67% of group revenue. Europe overall was up +8% in Q3 2016, led by accelerating growth in France, Germany, Italy and Iberia. Interestingly there was marked growth in the hire of blue collar workers which is an early cycle sign showing increasing demand for workers involved in production.

Interestingly their results showed flat growth in USA for Q4 (same as Q4), Canada +4%, Australia/New Zealand still strong at +12%, and Japan still making progress but more modestly at +5%.

The shares have reacted positively up 4% and these results should lead to further analysts’ upgrades for 2017 profits.

Reporting Season is drawing to a close with just one week remaining. With this in mind, we thought it would be appropriate to provide an analysis of two of the bigger names to report so far. Guy Carson, manager of the TAMIM Australian Equity All Cap Value IMA, provides his thoughts on Telstra (TLS.ASX) and Brambles (BXB.ASX).

Reporting Season Analysis: Telstra & Brambles Guy Carson

With a week of reporting season left to go, it is fair to say that the divergence amongst results has been high. As expected, the mining companies have led profit growth with Rio Tinto reporting 12% growth in underlying earnings for the full year and BHP reporting a 157% increase in their half year earnings. This has translated into increased payouts for shareholders. Of course, given the sharp rally in commodity prices the results were largely in line with analysts’ expectations. It’s at the other end of the spectrum, the disappointments, where we find lessons on what signs we can use to avoid companies. Two of the top twenty companies have issued profits that missed expectations, these were Telstra and Brambles.

Telstra (TLS.ASX)

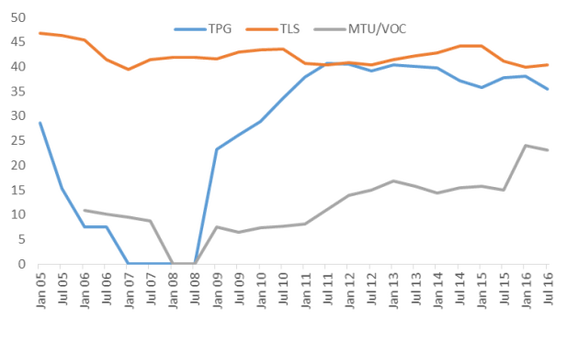

Telstra’s problems are largely not of their own doing. The industry is coming through significant change with the rollout of the National Broadband Network (NBN) and the end of Telstra’s natural monopoly. The NBN is publicly owned and levels the playing field in terms of competition. Hence, Telstra will potentially suffer the most from its introduction. Despite this assessment, last year we saw a significant selloff in the price of their competitors TPG Telecom and Vocus. Of course those companies were trading on significantly higher valuations, but nevertheless Telstra seemed to get off lightly.

The major reason Telstra is set to be the big loser from the NBN is that it effectively loses its place as the lowest cost participant in the market. This will have the impact of reducing margin both through having to pay connectivity fees to the NBN and increased competition. Telstra has historically enjoyed significantly higher margins than the industry and they are clearly set to fall.

Source: Telstra company filings

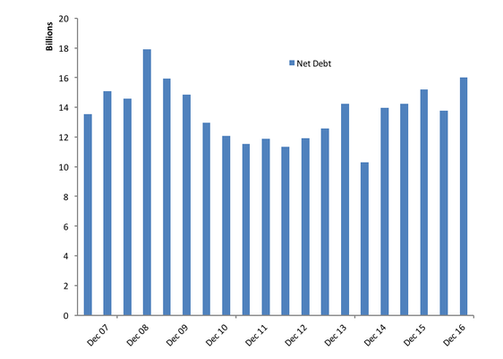

In fact, the company has been kind enough to quantify the impact of the NBN for shareholders. Between now and 2022, the company will lose $2-3bn of recurring EBITDA. Total EBITDA in the last financial year was $10.5bn.

Source: Telstra company filings

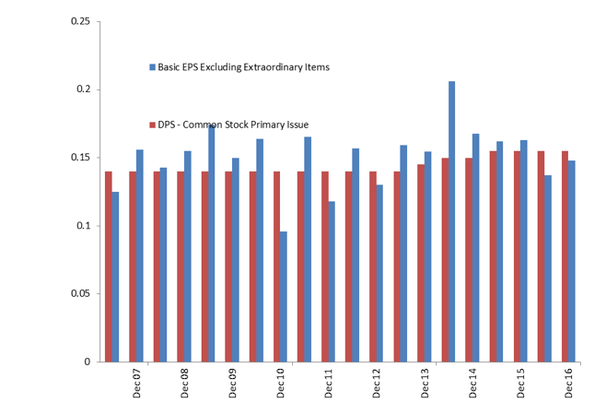

So in all likelihood earnings are going to fall over coming years. In addition to the impact quantified above there is the unknown aspect of competition. The signs in the most recent report are that the company is losing market share ever so slightly. Yet despite all this the company has maintained its dividend in recent periods despite paying out over 100% of earnings.

Source: Telstra company filings

This situation is unsustainable particularly when one factors in the $2-3bn impact of the NBN into the company’s earnings. In the meantime, the company is borrowing to pay shareholders.

Source: Telstra company filings

As a result we expect that Telstra will be forced to cut their dividend sooner rather than later.

Brambles (BXB.ASX)

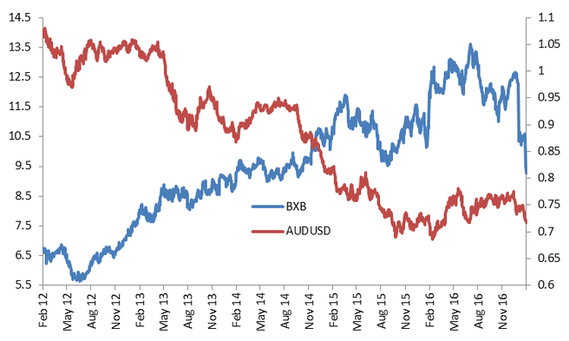

Brambles had been somewhat of a market darling over the last four years with the share price having gone from a low of around $6 in 2013 to a high of over $13.50 last year. One of the big drivers in the share price rise was the fall in Australian dollar from levels of over $1.05 to lows around the $0.70 mark. A popular trade in recent amongst “active” Australian Equities managers was to overweight International earners in order to take advantage of an elevated currency. Stocks such as Amcor and Brambles were noticeable beneficiaries of this trade.

Source: Brambles company filings

Now in the case of Amcor, the rerating was justified as the operation performance of the company improved significantly but in the case of Brambles we don’t think this is the case.

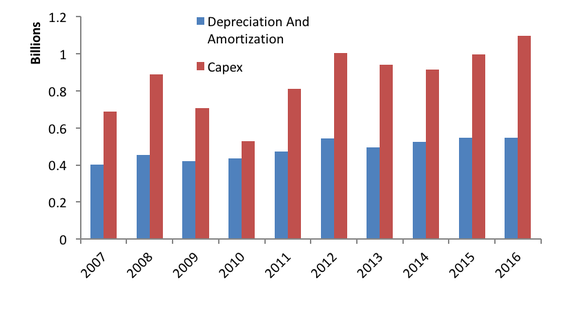

The first warning sign with regards to Brambles was the Free Cash Flow (FCF). Whilst the company has reported reasonable profit outcomes since 2013, the FCF has lagged significantly. This is particularly the case in the last 18 months.

Source: Brambles company filings

The reason for the FCF lagging is quite simple. The company has spent significantly more on Capital Expenditure (Capex) than has gone through the Profit and Loss statement as Depreciation and Amortisation.

Source: Brambles company filings

Now this isn’t necessarily a bad thing. Increased Capex, if used to invest in growth with a positive net present value, can be positive and increased the value of a company. The problem for Brambles is that despite this elevated level of Capex, revenues have barely moved. In fact since the end of the 2012 financial year, Brambles have spent over $2bn of additional Capex and yet revenues been broadly flat. With that in mind, It’s not surprising the company has withdrawn its previous 2019 target for Return on Capital Invested.

Source: Brambles company filings

This brings is to one of two conclusions. The first possibility is that Brambles is underestimating their depreciation charge and as a result is overstating profit. The second possibility is that issues in the business have been papered over by aggressive growth in other areas. Either way the rally in the share price over recent years looks unjustified.

Reporting Season is well and truly underway in Australia. With this in mind we asked our Australian managers to provide a preview for the coming weeks. Here the managers of the TAMIM Australian Equity Small Cap IMA reveal what they expect to see.

Stock Picking – Macy’s (M.NYSE) Robert Swift – Head of Global Equity

Macy’s, the US department store retailer, is a relatively recent purchase for the High Conviction Strategy. Traditional bricks and mortar retailers have found it tough going against big online retailers like Amazon. As a result, Macy’s valuation has been hit hard. In under two years the shares have more than halved from over US$ 70 a share in July 2015 to the low US$ 30 area recently.

Macy’s recently announced a plan to shed underperforming stores and reduce corporate staff numbers by 6000. The company also owns a significant proportion of its store portfolio which is potentially value that can be unlocked in a sale and lease back agreement.

So the low valuation, the self-help policies put in place by the management and the potential of further value to be unlocked in the company is what attracted us to the business. Since our purchase there was a disappointing trading statement which pushed the share price even lower. We re-evaluated the position and decided to add more at the lower prices.

In the last week the CEO has intimated that the company would be open to offers for the business. Since then Hudson Bay, a Canadian retailer, barely a fifth of Macy’s size has expressed interest in acquiring Macy’s. It may sound bizarre for a much smaller company to gobble up a far bigger rival but it can be done if Hudson Bay can raise the finances to do the deal. The current market value of Macy’s is around $10bn. Pencil in a suitable bid premium and let’s say it gets taken out at $13bn. It is estimated that the property of Macy’s could be worth anything up to $20bn. But let’s be conservative and assume they’re worth only $10bn. So that leaves only $3bn of additional financing – yet Macy’s has substantial cash flow to support additional debt. It’s Earnings before Interest and Tax (EBIT) is around $1.3bn, take off rent now due to the sale and leaseback of $600m, but add in cost savings of $300m from redundancies (the original management plan). This would give you further earnings of around $1bn to finance a $3bn funding loan! Even at a high yield of, say, 6% this would mean annual funding costs of $180m. This would leave a fully funded deal with pre-tax profit of $800m! So the idea of Hudson Bay being able to do this deal and for them to finance it directly from Macy’s own resources is very doable.

It may be that the Hudson Bay approach to Macy’s simply flushes out other potential bidders for Macy’s. We shall have to wait and see. But what it clearly does highlight is the potential appetite for financial engineering with plenty of liquidity to do deals and low interest rates. If companies are struggling to grow organically – which many are right now – they will be under pressure from the market and shareholders to contemplate such deals.

Reporting Season is well and truly underway in Australia. With this in mind we asked our Australian managers to provide a preview for the coming weeks. Here the managers of the TAMIM Australian Equity Small Cap IMA reveal what they expect to see.

TAESC 2017 Half Year Reporting Season Preview

Summary: Expectations for the upcoming reporting season are the highest they have been in three years. In our experience, heightened expectations often lead to disappointments. This is particularly the case for industrials with global operations which in the last 6 months have had to contend with the impact of Brexit and the US elections. Given the market’s propensity to punish poor-performers, we believe this reporting season will be more about avoiding the losers than picking the winners.

H1 Reporting Season: The semi-annual ASX reporting season inevitably presents surprises, disappointments and opportunities. Investors, analysts and shareholders will have their own expectations regarding the results to be reported, and companies will either beat, miss or fall in line with these expectations. Reporting for the half year ended 31st December 2016 started last week and runs through until the end of February, with the potential for more surprises, disappointments and volatility than usual

Heightened expectation: According to Factset consensus earnings estimates, earnings growth for the S&P/ASX200 is forecast to be 12% in FY17, which represents a turnaround in expectations from the last two years which have seen negative earnings growth reported. Much of this year’s expected earnings growth is concentrated in the resources sector, where a rebound in commodity prices is forecast to drive significant profit growth (greater than 50%) for the sector. For the balance of the market (largely industrials) the results and outlook may not be as bright as many expect. In our experience, heightened expectations often lead to disappointments.

Challenging macro conditions: The six months to 31 December 2016 saw two large political events play out – the Brexit vote and the US election. These events have impacted sentiment and business decisions in two of the major developed global economies, and have resulted in exchange rate and general market volatility. Growing global companies are particularly exposed to these dynamics, with two ASX listed mid-cap companies Servcorp (ASX:SRV) and Aconex (ASX:ACX) recently substantially downgrading their profit expectation in part due to this global macro uncertainty. This followed Brambles (ASX:BXB) downgrading expectations on the back of operational weakness in America. The fact that both SRV and ACX downgraded their forecasts after having just provided more positive guidance in late 2016 illustrates the difficulty in forecasting earnings for global businesses with many moving parts, and also perhaps suggests a degree of management over-confidence/naivety in their previous forecasting.

In addition to the issues in Europe and the United States, China continues to present challenges as the well publicised Bellamy’s (ASX:BAL) downgrade highlighted.

Closer to home, challenging retail conditions have seen downgrades to date from large national retailers, Oroton (ORL) Shavershop (SSG) and Adairs (ADH). The market is unforgiving in relation to any such downgrades, particularly against a backdrop of general rotation away from small caps into large caps, and a de-rating of stocks on high multiples. The real challenge for investors during the upcoming reporting season is to avoid exposure to such downgrades and guidance misses.

Portfolio weighted towards domestic businesses with momentum: Our own smaller companies portfolio is weighted (60%) to Australian businesses with Australian customers. These companies, for the most part, have limited exposure to most of the global issues at play and fewer ‘moving parts’. Generally, these are also businesses that are coming off a strong first half of calendar 2016, and have provided positive updates at their recent annual general meetings (AGMs).

Portfolio examples include:

Debt collector Pioneer Credit Limited (ASX:PNC) advised at its AGM that it was excited about the way in which FY17 had commenced, and that another year of high quality growth was underway. At its AGM, PNC reiterated its guidance for the full year of statutory NPAT of at least $10.5m. Since its AGM PNC has advised of further portfolio purchases and executed an increased debt facility.

Paragon Care Limited (ASX:PGC), a leading provider of consumables and equipment to hospitals and aged care facilities, advised at its AGM that it had enjoyed a strong start to FY17. Strong growth was being delivered across key financial metrics. In the first quarter of FY17, the company’s EBITDA on a like for like basis was up 12% over the prior corresponding quarter. PGC reaffirmed expectations of strong earnings growth for FY17, with FY17 being the first full year of earnings capture from it 2015 acquisitions.

Investment company Joyce Corporation Limited (ASX:JYC) noted at its AGM a strong start to the year, maintaining a relatively high rate of revenue growth for the first quarter. Total written sales across the JYC businesses (including franchisee sales), is expected to be within the range of $180m- $200m in FY17. “At this early stage it appears to be tracking toward the higher end of this range.” This represents an upgrade on the previously advised level of $170m. In FY17, JYC will benefit from the earnings contribution from its recently acquired Lloyds business, and (from January 2017) rental savings when it moves into its new wholly owned property. We expect its FY17 NPAT to exceed $3m (FY16: $1.9m; +58%). The company continues to hold a large cash balance and property assets, and is currently offering a 7%+ fully franked dividend yield.

Property fund manager, and property management company, Blackwall Limited (ASX:BWF) announced the completion of a number of capital raisings and other transactions across the funds it manages during the second half of 2016, which will provide BWF with additional fees, and increase its funds under management into 2017. BWF also continued the roll-out of its shared work space business ‘Wotso’ during the period, noting at its AGM that its annualized turnover had more than doubled to $5.5m since June 2015.

Lower expectations for global businesses: Two businesses in our portfolio with significant global operations are SDI Limited (ASX:SDI) and Gale Pacific (ASX:GAP) – both of which have been adversely impacted by global macro events.

Global dental products manufacturer SDI Limited (ASX:SDI) recently advised that not-withstanding good sales growth, it is on track to report a lower first half profit than the previous year. A reason for the disappointing fall in profit was surprisingly strong sales growth in the UK (+18% on PCP) resulting in relatively lower gross margins due to the weakness of the pound.

Outdoor shade cloth manufacturer GAP noted at its AGM that in America it has seen weaker market conditions due to lower consumer confidence. GAP are guiding for a ‘modest’ increase in revenue and profitability in the first half.

With limited expectations around current earnings, the outlook provided here for both SDI and GAP is likely to be of more interest to the market.

Conclusion: Given the market’s propensity to punish poor-performers, even more so than usual, this reporting season will be more about avoiding the losers than picking the winners. Accordingly, we continue to focus on the downside potential of stocks, and are focused on investing in companies that trade on undemanding multiples and where expectations are low.