This week Robert Swift takes a look at an investment thematic – Japan and robotics. What does this mean going forward? Where do the opportunities lie?

Investment Thematic: Robots, Demography, and ‘virtual world’ for seniors Robert Swift

This piece is on Japan. It covers Japanese demography, a much misunderstood influence on GDP, robotics (a labour saving device or a threat to everyone’s livelihood?) and technology which is typically adopted by the young but has a much bigger wealthier market if the elderly were to “get on board”. We will stay focussed and address only a couple of trends in Japan and technology you can use to make money!

Please click and watch the video clip below from the Nikkei news company. – it takes 3 minutes or so. Nikkei is a Japanese media business which owns the Financial Times of London, the Nikkei, the world’s largest circulation business newspaper, and various stakes in Japanese TV broadcasting companies. It also calculates the Nikkei 225 and Nikkei 300 indices which you may use to follow Japanese share prices.

Fascinating? We think so and it strikes us that robotics is a useful tool and not to be feared or rejected.

Japanese demography is aging and the workforce shrinking. Such a pattern is not conducive to GDP growth but it doesn’t matter from an investor’s perspective. On a per head of population basis Japan has outperformed Germany a little and most definitely the USA, the UK and Australia over the last 20 years. In other words its citizens are more productive and getting wealthier even though the total pie is not growing that fast. Think about it. Australian working age population has grown about 2% p.a. for many years and general price increases (ignoring property) have averaged about the same. These two together make 4% p.a. and account for nearly all of the annual nominal GDP growth p.a. in Australia, leaving very little real improvement in living standards per head of population. This explains both the frustration of the average family here and the RBA which correctly worries about a lack of productivity growth.

Japan is a better performing economy than Australia. This is not the point we want to make here. What we do want to emphasise is that aging demography is feared but shouldn’t be. It may result in lower nominal GDP numbers but the spending power per person may remain strong and the spending patterns change and it is that change that provides the new investment opportunity. Medical care, aging and robotics in Japan looks one such trend.

“Japan ranks as the third biggest medical device market after the United States and the European Union, on track to expand even more with the percentage of seniors (65+ years) going from 24% in 2012 to 40% in 2050” – Maine International Trade Center

It also struck us that a ‘virtual’ interaction like we see on the video is not so different with the ‘virtual’ interactions we all witness with our children’s “social” lives. Our children will have “friends” on Facebook or gaming sites, they have never, and may never, meet! How different is that from having a robot help folks exercise, provide comfort and company by responding to touch or voice, or even cleaning bed pans? Not much if at all. Consequently we see no moral or ethical barriers to widespread adoption in Japan and ultimately, elsewhere.

This also reminds us that Japan was a technology innovator and although Japanese technology may not grab the headlines like USA technology which tends to be more software and advertising focussed, if we do see a return to more acceptable levels of public and private sector capital investment, then Japanese companies are well placed. We are reminded of this technological prowess by the current coverage of the sad demise of Toshiba which is facing a breakup after poor acquisitions and some business cultural failings (a common Japanese problem) but which at one time was the global leader in memory chip technology.

It also shows us that Japan is wealthy and is able to provide dignity to its elderly. Analysts focus on Japan’s gross debt but this is misleading since it is also a very significant creditor nation having had years of current account surpluses to build a very strong Net Foreign Assets (NFA) position. Anyone care to think what the UK or Australian NFA position looks like?

Japan may not be leading the way in the use of robotics but it is up there and many of its companies will be successful internationally. We are currently evaluating SMC, Fanuc, Omron, Keyence, HitachI High-Tech, JTEKT and Terumo. There is a rich seam to be mined if the price is right.

In conclusion we emphasise that Japan is a market rich in stock opportunities but surrounded by misperceptions of its economic performance.

The TAMIM Australian Equity All Cap Value IMA is significantly overweight tech stocks compared to the ASX as a whole. This week Guy Carson, manager of the strategy, takes a look at finding value and quality in the software space without having to go to Silicon Valley.

Through our portfolio we hold a number of software companies, and whilst they are relatively small on a market cap basis they are leaders both domestically and globally in what they do. The underlying business model is one that we are attracted to for a number of reasons. When software is embedded in a company’s operations it is typically very difficult to remove, as a result clients tend to be sticky (as long as the underlying software is of a high standard). Additionally, when new clients are added there is typically limited cost to adding them, meaning these companies can grow with very little cost. The nature of the business model means that these companies can potentially see:

A high level of recurring earnings;

A high level of Free Cash Flow;

Increasing margins as new clients are added; and

Increasing returns on capital.

Consequently companies with high quality software products can be relatively safe equity investments (not that any equity investment can ever been considered 100% safe). This is particularly true if they dominate or have a significant market position in a particular niche. Thankfully, several companies of this nature exist on the Australian Share Market and whilst they may appear small in market capitalisation terms in our opinion it would be a mistake to classify them as risky.

To illustrate the above points we will have a look through some of the major software companies listed on the ASX to see how we identify those high quality companies with the characteristics we have described above. The companies we have chosen are:

Aconex: A company providing Software as a Service (SaaS) to clients in the construction sector. A recent IPO from US Private Equity investor Francisco Partners.

Altium: Altium designs software for the design and manufacture of Printed Circuit Boards. They are the fourth largest player in the PCB software market globally, having grown from a 10% to 16% market share over the last year.

Class: Class is the leading provider of software for the administration of Self Managed Super Funds.

Freelancer: Freelancer is a platform that enables businesses to connect with independent (or freelance) professionals primarily in the IT space to complete one-off tasks.

Gentrack: Gentrack is a software company specialising in billing for Utilities and Airport management software.

Hansen Technologies: Hansen, like Gentrack, also specialises in billing for Utility companies.

IRESS: IRESS provides software for financial market participants including the flagship market access product as well as wealth management platforms.

Integrated Research: Integrated Research is a leading global provider of performance management software for critical IT infrastructure, payments and communications systems. The company has 120 out of the Fortune 500 companies amongst their clients.

MYOB: MYOB provides accounting software to Small and Medium Enterprises.

Technology One: Technology One provides enterprise software primarily to the local government sector.

Wisetech Global: Wisetech is a software solution for supply chain management.

Xero: Xero is a competitor to MYOB and provides accounting software for small and medium enterprises.

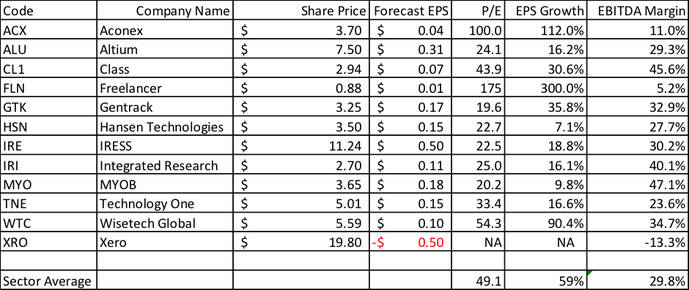

The first thing we have done is look across this selection of companies at the current consensus forecasts for Earnings per Share (EPS) as well as Earnings growth and Margins. Ultimately we want to see solid margins, good growth and a reasonable multiple.

From this table we can divide in the universe into a number of groups. The first group to highlight are those companies trading at large multiples (Aconex, Freelancer, Xero, and Wisetech Global). These companies have large addressable universes and are spending in the hope of being the global leader; they have lower margins than the other companies and are all about growth. As a result we can expect their share prices to be volatile. They are what some commentators call “Long Duration” stocks (i.e. their valuation depends on earnings a long way into the future) and hence small changes to their expected growth rate can cause significant changes to their valuation. We have seen this in recent times with all of these companies below their highs from mid last year, most notably Aconex down 58% and Freelancer down 51%.

Another group though is of more interest to us. These are companies that trade at reasonable multiples although still have impressive growth rates (Altium, Gentrack, Hansen Technologies and Integrated Research). They tend to operate in smaller niche markets and are leading players in them globally. Due to their market leading position, the profitability of these companies far exceeds the first group seen by the higher margins above. They don’t need to spend or price aggressively in order to attract new customers.

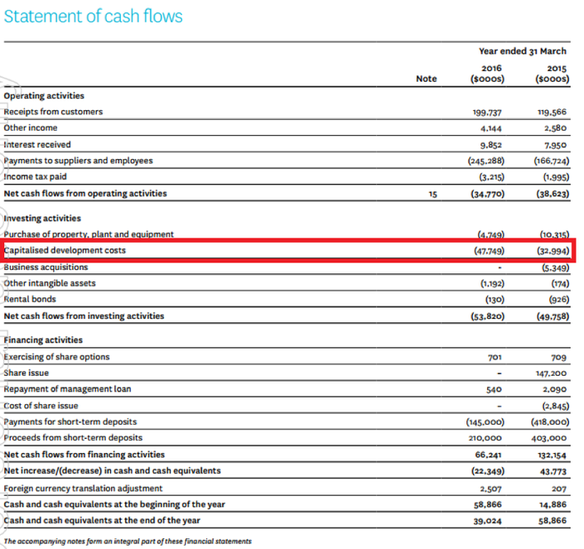

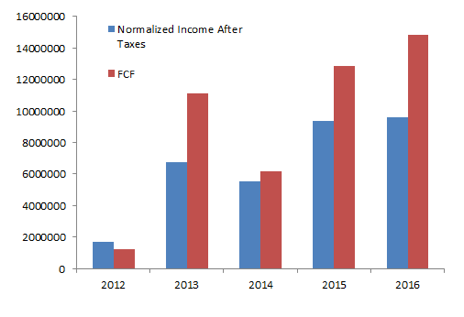

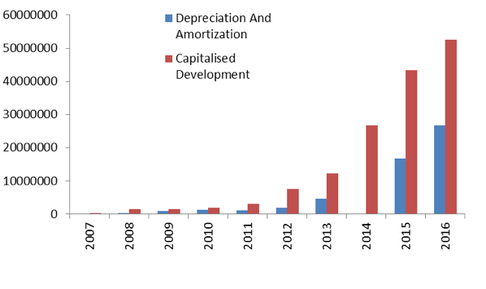

The next thing we need to highlight is that with software companies not all growth is created equal. Accounting standards give companies the flexibility to capitalise development costs of software. Essentially this allows companies to take the development cost of the software onto their balance sheet and amortise it over the expected useful life of that particular product. The effect this can have is to boost short term earnings growth and potentially reduce free cashflow relative to profit. Thankfully it is usually fairly easy to spot. The below extract is from Xero’s financial statement, where we can see the impact of capitalised software through the cashflow statement.

Source: Xero company filings

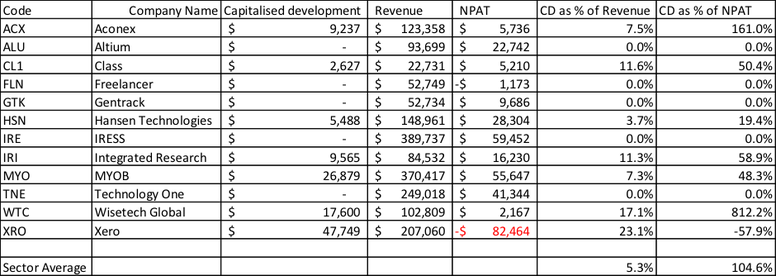

The table below collates information from each company’s most recent annual report and looks at their capitalised development as a percentage of their revenue and Net Profit after Tax (NPAT):

Pleasingly, a number of these companies take the conservative approach to their accounts and expense all Research and Development. As a result these companies are more likely to have Free Cash Flow that matches their Net Profit. Two of the companies that caught our eye from the first table fall into this category: Altium and Gentrack. When we look at their recent history we are pleased to see this is the case (Altium is on the left and Gentrack is on the right). In most years, Free Cash Flow actually exceeds NPAT.

Source: Altium company filings

Source: Gentrack company filings

A number of companies though stand at the other end of the spectrum and are capitalising a significant amount of their software relative to their revenue and profit. As mentioned above, by capitalising software development a company can spread the impact of that spend over multiple years, hence boosting short term profit. A number of these companies that are doing this fall into the other group mentioned above, the ones with high valuations that need high earnings growth in order to justify their current share prices. The standouts in this regard are Xero, Wisetech Global and Aconex. In fact Wisetech Global and Aconex are current capitalising at rates more than their profits.

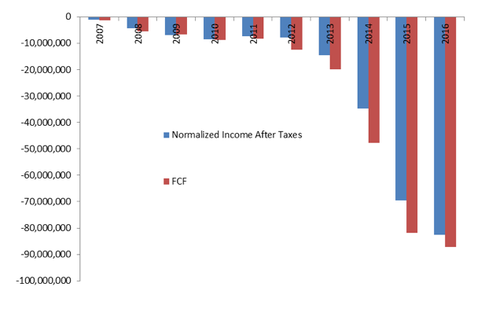

Of particular concern from this group is Xero, where the rate of capitalisation far exceeds the rate of amortisation on the Income Statement.

Source: Xero company filings

Due to this, the cash burn of the company actually exceeded the company’s reported Net Loss.

Source: Xero company filings

Overall, the capitalisation of software development isn’t necessarily a good or bad thing but we highlight it as a key aspect for investors to be aware of. Whilst we prefer the conservative approach of expensing all Research and Development, we won’t exclude companies that have a different approach. By focusing on the underlying Free Cash Flow of the business, you can ignore the noise around various accounting treatments and get a more complete picture of how these companies are performing.

I recently attended a presentation by one of our investment managers to a group of self-directed investors and, as you would expect, the usual question was posed by the audience: “Warren Buffett says you should invest in passive index driven strategies and not with active fee charging managers as they can’t beat the passive index over long periods of time. What are your thoughts on this statement by the world’s best investor?”

Buffett’s Bet Darren Katz

I recently attended a presentation by one of our investment managers to a group of self-directed investors and, as you would expect, the usual question was posed by the audience: “Warren Buffett says you should invest in passive index driven strategies and not with active fee charging managers as they can’t beat the passive index over long periods of time. What are your thoughts on this statement by the world’s best investor?”

I have paraphrased the question above but what ensued was 5 minutes of intense debate with all and sundry trying to get their point of view across. I will try and get my views across and for the record, Mr Buffett, you are wrong. Okay, maybe not wrong but largely misunderstood or misquoted. I present a very simple argument to make my case. Would you rather have invested in Berkshire Hathaway (even on an after company-tax basis) or the S&P 500 over a 10 year period? I would expect that were you to ask Mr Buffett the question, he would give you the same answer every time – Berkshire Hathaway shares.

The debate around the Buffett bet poses a number of interesting intellectual and practical investment questions. It is worth taking some time to review them and attempt to provide you with some answers. Firstly, let’s take a look at the original 2005 assertion by Warren Buffett:

“In Berkshire’s 2005 annual report, I argued that active investment management by professionals – in aggregate – would over a period of years underperform the returns achieved by rank amateurs who simply sat still. I explained that the massive fees levied by a variety of “helpers” would leave their clients – again in aggregate – worse off than if the amateurs simply invested in an unmanaged low-cost index fund.” – Page 21 of the 2016 Berkshire Hathaway annual letter

Ted Seides accepted the Buffett challenge and then put together a stupendously stupid bet that, in my opinion, he could not win. He selected 5 fund of hedge funds to compete against a Buffett selected Vanguard S&P 500 low cost index fund. The Longbets original bet and its terms are as follows:

Excessive Fees:

The stupidity of Seides’ bet is quickly apparent when you understand the cost structures of fund of hedge funds. They invest into hedge funds that typically charge fees of 2 and 20. That is a 2% management fee and a 20% outperformance fee. They will also, due to their more complex investment structures, have large expenses which could amount to an additional 2-3% in yearly costs. Over and above the fees of the underlying hedge funds, the fund of fund structure charges an additional fee of 1 and 10, which is a 1% management fee and a 10% performance fee. To put it bluntly they could potential be charging in excess of 8% to 10% in fees per year. That basically guarantees a Buffett victory.

TAMIM’s solution:

While we don’t believe investment decisions should be based on fees, in instances like this where fees are stupidly excessive you should avoid the investment like the plague.

“And, finally, let me offer an olive branch to Wall Streeters, many of them good friends of mine. Berkshire loves to pay fees – even outrageous fees – to investment bankers who bring us acquisitions. Moreover, we have paid substantial sums for over-performance to our two in-house investment managers – and we hope to make even larger payments to them in the future.”

The last word on fees belongs to Buffett, as quoted above. When an investment manager is delivering you true value then there is no doubt that paying them a large cheque to do so will be worth your while.

Active Manager Skill:

Buffett states the following in his 2016 report:

“There are, of course, some skilled individuals who are highly likely to out-perform the S&P over long stretches. In my lifetime, though, I’ve identified – early on – only ten or so professionals that I expected would accomplish this feat.”

“There are no doubt many hundreds of people – perhaps thousands – whom I have never met and whose abilities would equal those of the people I’ve identified. The job, after all, is not impossible. The problem simply is that the great majority of managers who attempt to over-perform will fail. The probability is also very high that the person soliciting your funds will not be the exception who does well. Bill Ruane – a truly wonderful human being and a man whom I identified 60 years ago as almost certain to deliver superior investment returns over the long haul – said it well: “In investment management, the progression is from the innovators to the imitators to the swarming incompetents.”

So the issue is not that superior mangers don’t exist. They do and Buffett concedes that in his 2016 letter. The issue you face as an investor is how do you find them and avoid the imitators and even more importantly the incompetents! This is where you should rely on trusted advisors to help you.

TAMIM’s solution:

At TAMIM we run significant due diligence on the investment managers we works with. We adhere to the following four step process:

We review the managers historical returns – have they been able to do what they say they can do consistently in the past. People will tell you not to look at historical returns but they are wrong. It is our first step. About the only good thing that came out of the 2008 financial crisis is that is gives us a very good benchmark to see how managers performed when the investment world was crumbling around them. If a manager was able to deliver a positive or even a small negative in that period then they are probably worth examining further. The next 3 steps are worth covering in more depth in later articles and they are: obtaining a deep understanding of the managers investment process, understanding the various drivers (economic and otherwise) that will allow this investment process to be successful and finally understanding if those drivers will be present on a forward looking basis.

Fund Managers that get too big – Yes, we are talking about you:

Size is an issue when managing investments – when managers do well they attract inflows and unfortunately when you manage too much money your returns will suffer. What happens is that managers will have to put more money to work, the small highly lucrative investments they were previously able to make no longer have a meaningful impact on their larger portfolio. As Buffett states in the 2016 letter:

“Finally, there are three connected realities that cause investing success to breed failure. First, a good record quickly attracts a torrent of money. Second, huge sums invariably act as an anchor on investment performance: What is easy with millions, struggles with billions (sob!). Third, most managers will nevertheless seek new money because of their personal equation – namely, the more funds they have under management, the more their fees.”

Using the returns from the table on page 1 of the 2016 report we derive the following information. In the first 10 years of operation a $10,000 investment into Berkshire Hathaway was worth $40,097 on book value and $32,341 on market value compared to an investment in the S&P 500 being worth $11,476. Over the last 10 years to 2016, the same $10,000 investment would have been worth $24,508 on a book value basis and $22,165 on a market value basis. The index was comparable at $23,222. Clearly even Buffett found it considerably easier to generate stronger returns with a small sum of money compared to the significant asset he has had to manage in the latter years.

The investment management industry on the whole has much to answer for. They have forgotten one reality. They exist to generate returns for us, their clients. Instead, these large funds management businesses (most of whom are now owned by the Australian banks), now believe that their business risk is more important than yours.

TAMIM’s solution:

At TAMIM we focus on working with best of breed investment managers who we believe are able to consistently generate you an out sized return. The one key item we insist upon from our managers is that they will never run too much money. All of our strategies are strictly limited in size and in terms of assets they can manage. The following quote from Buffet says it all:

“If I was running $1 million today, or $10 million for that matter, I’d be fully invested. Anyone who says that size does not hurt investment performance is selling. The highest rates of return I’ve ever achieved were in the 1950s. I killed the Dow. You ought to see the numbers. But I was investing peanuts then. It’s a huge structural advantage not to have a lot of money. I think I could make you 50% a year on $1 million. No, I know I could. I guarantee that.”

A final warning:

There will be times where it is appropriate and safe to be investing into low cost index funds but there are other times when this could very well be the riskiest investment you could make. Just look at the return table on the front page of the Buffett 2016 letter. There are times when the index has had significant falls in a given year. In 2008 the index was down 37%. It would be silly and naïve to believe this will not occur in the future, in fact these “Black Swan” events seem to occur more and more frequently.

A person who stopped work in 2008 and took all of their hard earned investments and bought S&P 500 fund or ETF suffered a huge loss. If this person was then required to use the existing savings to live off, they would have had a very difficult or even impossible time recovering and could quite likely run out of money to live off.

We believe, as does Buffet that true active managers exist, if you are amongst the lucky few who are able to find them and access them (they are typically the managers who don’t put up big investor events for 1000’s of people to advertise their prowess) you should be utilising them in your investment portfolios. If you would like to find out more about how we find and research Australia’s best investment managers please contact us for a confidential discussion.

With Reporting Season coming to a close a few weeks back the managers behind the TAMIM Australian Equity Small Cap IMA take a look at some of their previously disclosed stocks and how they fared over what was a rocky few weeks at the smaller end of town.

A summary of the half year results from a selection of our previously disclosed positions is detailed below:

Konekt Limited (ASX:KKT)

(February return: -1%)

HY17 result highlights – (*) normalised

Revenue +34%

NPAT + 43%

EPS +43%

Comment:

KKT, a leading provider of workplace injury management and prevention services reported a strong half year result. Operational highlights included a significant panel appointment in the Commonwealth government sector and being re-appointed as a service provider to two major financial institutions.

KKT continued to benefit from the increased scale of the business with underlying EBITDA margins increasing from 10% to 11%, resulting in significant earnings growth. KKT’s increasing EPS trend (by half year) is shown below:

Source: KKT Investor Presentation 15 Feb 2017

KKT noted it is well positioned going into 2H17 with good momentum in the business. KKT has forecast total FY17 revenues of between $51.0m to $53.5m, which is a 14% to 21% increase over FY16. As advised in our January update, KKT is currently re-negotiating a major customer contract, and until the outcome of that is known, its share price is likely to remain weak. We therefore suggest a significant amount of caution with respect to KKT.

Joyce Corp Limited (ASX:JYC)

(February return: -5%)

HY17 result highlights – (*) normalised

Revenue +51%

NPAT +80%

EPS +80%

Div +10%

Comment:

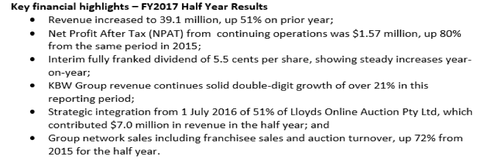

Joyce Corporation, an investment company that owns the Bedshed Franchise, Australia’s largest kitchen renovation company and a leading online auction company, reported a strong operating result relative to the previous corresponding period.

The key highlights from its result are summarized below:

Source: JYC Results announcement 24 Feb 2017

JYC advised that the group is poised for further growth and the underlying business units are continuing with their solid performance into the second half, with the Chairman noting that “The Company is in an enviable financial position with profitable businesses, low debt and substantial growth opportunities which provides a strong level of security for our shareholders.”

Fiducian Group (ASX:FID)

(February return: 10%)

HY17 result highlights – (*) normalised

Revenue +15%

NPAT +27%

EPS +22%

Div +29%

Comment:

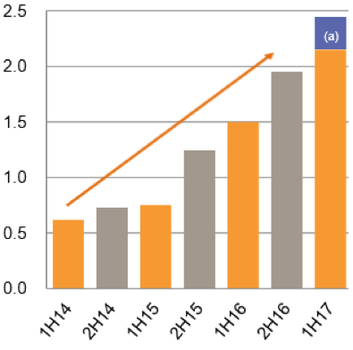

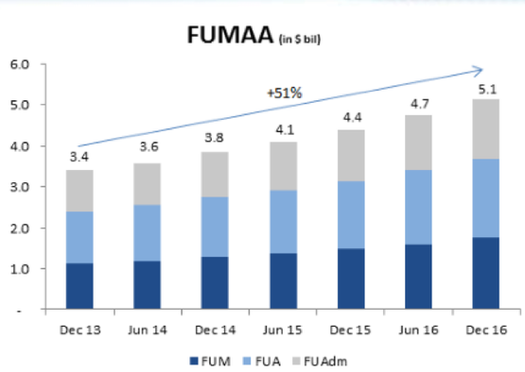

Integrated financial services company FID reported an increase in its underlying after tax profit in HY17 of 23%. Its total funds under management, administration and advice (FUMAA) increased 16% to $5.1b over the 12 months.

FID’s increasing FUMAA trend is illustrated below:

Source: FID results announcement 17 Feb 2017

With 41 offices throughout Australia, FID is now a substantial national financial services business, benefitting from increasing recurring revenue. FID is well placed to continue to build scale organically and through acquisitions, and to leverage its integrated service offerings to “deliver consistent double digit earnings growth in coming years”.

FID noted that they have recorded double digit annual EPS growth in 13 out of the 17 years it has been listed.

SDI Limited (ASX: SDI)

(February return: -25%)

HY17 result highlights – (*) normalised

Revenue -1%

NPAT -33%

EPS -33%

Dividend +25%

Comment:

Global dental product manufacturer, SDI, produced a disappointing profit result at the lower end of its previous guidance range ($2m NPAT).

While sales of its higher quality non-amalgam products are growing, its older amalgam products are declining faster than expected and previously guided for, such that SDI is expecting only marginal total sales growth over the course of this year. Adverse currency movements have further reduced profits relative to the previous period, resulting in significant earnings volatility.

Source: SDI results announcement 23 Feb 2017

SDI have forecast sales growth in Non-Amalgam products to increase by approximately 10% while Amalgam sales (~30% of total sales) will decrease by 13%, equating to a total sales increase of approximately 2% for FY17.

Pioneer Credit Limited (ASX:PNC)

(February return: 3%)

HY17 result highlights – (*) normalised

Revenue +17%

NPAT + 27%

EPS +17%

Dividend +17%

Comment:

Debt purchaser PNC reported a solid result and evidence of further pleasing execution on its development. Vendor partner relationships appear strong with PNC now having secured (under contract) full year PDP investment of at least $53m (up from an initial guidance of $50m) within the half-year, representing solid market share gains. The business is expanding (& diversifying) well, with customer numbers having increased to over 160,000 and its first NZ portfolio secured during the half.

Source: PNC Investor Presentation 24 February 2017

PNC has re-affirmed its forecast FY17 NPAT of at least $10.5m, while its investments made during the year are likely to position it for a particularly strong FY18 result.

Elanor Investors (ASX:ENN)

(February return: -4%)

HY17 result highlights – (*) normalised

Core Earnings +34%

EPS + 11%

Dividend +6%

FUMI +51%

Comment:

Fund manager and asset owner ENN reported a solid operating result. ENN’s key strategic objective is to grow its funds management business and since 31 December 2015, total funds under management and balance sheet investments have increased to $774m reflecting a 50.6% increase on PCP. Earnings highlights included a 90% increase in Funds Management earnings to $7.8m, while earnings from Hotels, Tourism and Leisure assets showed significant year on year growth.

Source: ENN Investor Presentation 22 Feb 2017

ENN noted that they have a number of funds management initiatives in progress, though there are challenges associated with securing quality assets in the current environment.

Of interest is the possible announcement over the next several weeks regarding the sale of ENN’s Merrylands investment property – this will be a significant development for ENN, potentially raising $40m – $50m in cash (currently held on balance sheet at $16.6m).

This week Robert Swift takes a look at momentum and what it is telling us about asset allocation. Where should you deploy your capital and how? Will this achieve optimum results in the current economic climate.

Asset Allocation: Momentum: Where should your assets be allocated? Robert Swift

One of the most important decisions is how to allocate your money across different asset classes – property, bonds, equities, or cash. This is because a combination of these assets will be less volatile than simply holding equities, and the returns, although lower, will be safer and reduce the chances of a nasty surprise to your pension pot.

This is probably now consensus thinking and all the major banks, financial planners, and investment management companies produce regular reports giving their views of both HOW you should make the allocation decision and WHERE you should currently be invested.

What is our view on the HOW to do it? Does the HOW impact on the WHERE NOW decision?

We believe that there a systematic process of asset allocation that actually works. Over the last 20 years or so a number of the investment team have worked for some of the biggest multi asset investment funds in the world which have struggled with this question of how to develop a systematic, repeatable process of allocating between asset classes that added value for clients over time. We have been involved in the formulation, development, and testing of many of these models. A lot of quite sophisticated “fundamental” approaches were tested but none seemed to last the test of time.

Perhaps worryingly for some, what did seem to work best (most consistently) was a technical analysis model – simply following a set of rules based on price momentum using 10 day, 50 day and 200 day moving averages of the prices. Only holding above average exposure to those assets that met the criteria and avoiding the others that did not meet the criteria, led to significantly superior results than simply holding a benchmark of all the assets without making any changes.

This seems remarkably simple, possibly even stupid, and runs counter to the view that forensic accounting and meticulous predictions of GDP figures add value in making asset exposure timing decisions! Actually, the phenomenon known as momentum has taxed the financial academic world for quite a while and much work has gone to show that price momentum or trend following, adds value not just across asset classes but also within. In other words, even buying equities whose prices are rising, regardless of their valuation, will make you money relative to equities whose prices are falling.

Psychologically this “momentum factor” actually makes sense. Human beings like to be with crowds, in popular trends and don’t like the ridicule with being unfashionable, or to be too different. Consequently, there is an opportunity to simply jump on a trend and enjoy the ride. This human fallibility is what makes markets inefficient and active management worthwhile.

Think. If momentum exists as a way to make money, which it does, then it can’t be the case that ALL information in the market is instantly discounted so that the relative prices have instantly adjusted to their correct level. If prices instantly adjusted, as efficient market proponents argue, then there would be no momentum. Prices would move instantly and not over a period of time. It is this slow upward and downward movement that allow us to get set and make money.

We use a stock selection model which also incorporates momentum or trend following. In a way acknowledging the impact of price momentum is the ultimate acknowledgement that other people may know more than you. If valuation is acceptable then better to go with what other investors see as attractive?

It is rather ironic in a business where people attempt to develop very sophisticated models that closely fit with financial theory that it is often very simple things that work! This simple price momentum, had it been followed in 2008/9 financial crisis would have avoided much of the damage to portfolios that people incurred by switching out of the falling assets (equities, commodities) and in to the rising assets (bonds). In a business where there is so much information being thrown at you, it is important to be able to separate what’s relevant and what is simply a distraction. We have never found predicting GDP is productive for asset class forecasts. Plenty of firms do but we think they’re wasting their time.

WHERE NOW?

So what is the price momentum model telling us now? Over 2016 the model gradually sold out of all form of bonds – both government and corporate – final sales being in September 2016. These have been gradually replaced by increasing exposure to equities – firstly US equities – then a gradual spreading throughout most of world equities.

This purely price momentum model also fits in with our fundamental view. Following the 2008 financial crisis a large proportion of money was switched out of equities into bonds. Relative to history over the last 5-6 years there has been an over-allocation to bonds over equities. The Bank Credit Analyst a well-respected research group recently released a report where they argued that the world economy was in a synchronised growth stage and this was leading to a general improvement in company earnings. Furthermore we are started to see growth in company capital expenditure which is a sign of more confidence amongst companies after years of below average expenditure on capex. M&A is also starting to picking up – which is something we discussed a few weeks ago.

So with positive technical indicators and encouraging fundamentals we could eventually see more decisive switching out of bonds in to equities.

Equities – overweight with a bias towards Value

Bonds – underweight especially net debtor countries such as Australia, Turkey, Spain