Reporting Season is well and truly underway in Australia. With this in mind we asked our Australian managers to provide a preview for the coming weeks. Here Guy Carson , manager of the TAMIM Australian Equity All Cap Value, reveals what he expects to see.

TAEACV Reporting Season Preview Guy Carson

Every six months reporting season comes around for the Australian Equity Market. It’s an important time for investors as we get detailed look into how a company has been performing and in some instances, an indication of how management see their outlook. The market typically will react to how the result and the outlook compare to the current market expectations. Hence, heading into reporting season it is important to understand what the market is expecting in order to understand the share price reactions that occur.

The expectations at this stage are for a strong year in terms of earnings growth. Consensus earnings growth for the market is in double digit territory for the first time since FY11. In fact if expectations are achieved, it will be the first positive year for earnings growth since FY14.

These positive expectations come despite what can only be described as a weak AGM season late last year and the number of downgrades seen through the recent “confession season”. The key driver offsetting the plethora of recent downgrades is the materials sector, where a rebound in commodity prices is set to drive earnings up over 80% following a 42% fall the previous year.

Source: Thomson Reuters

Given the high expectations and the fact that commodity prices (in particular Iron Ore) remain above last year’s level, earnings for the commodity companies are largely locked in by this stage (for the first seven months at least). Hence, when they report this time around there is very little likelihood of surprise. Most of the focus will be on how much of the windfall in profit gets returned to shareholders. Further gains in the share prices this year will likely be dependent on commodity price moves.

One aspect of the big miners’ reports that will be intriguing to us is how their capital expenditure expectations have changed over the last six months. With the rally in commodity prices, we have seen mining service companies follow suit. In recent years, these services companies have seen their order books shrink as mining work has been cut back. The expectation now is that with the higher commodity prices, capital expenditure budgets will increase and work will start to flow back to the contractors. This work won’t come from expansion of production but more likely through maintenance work that has been delayed in recent times in the name of boosting cashflow. The degree to which the likes BHP and RIO increase their capital expenditure budget for the coming years will help tell us to what degree the recent rally in mining services stocks is justified.

Overall, the direction of the market over the early part of this year will most likely come down to the largest sector, Financials. Within financials, the key driver will be the banks. We have Commonwealth Bank set to report its half year result as well as quarterly updates from the other 3 of the big 4 and the consensus expectations for the sector this year are reasonably low at 2% growth. However given the recent rally in the share prices of the banks (the big 4 are up between 11 and 18% since the US election); we’d suggest that the market is running ahead of the sellside analysts in upgrading future earnings. We are sceptical that these upgrades will occur and we wrote in depth about the challenges facing the banks from the Western Australian and Queensland economies last week (see 2017 Outlook). Typically problems in the housing market take a while to play out however the increase in arrears from WA over the last 12 months suggests we may start to see an impact on the profit numbers soon. With only CBA set to give a detailed half year report in February, we may have to wait until the other three release their results in May to get a full view of how this is playing out.

The other areas within the top 20 companies which are seeing earnings pressures are Consumer Non-Cyclicals and Telcos. The consumer side is dominated by the two large supermarket chains, Woolworths and Coles (owned by Wesfarmers). The supermarkets are facing increased competition from Aldi and Costco combined with the potential entry of Lidl. There seems to be no respite from these pressures in the near term, however Wesfarmers should see a boost to their result from Coal prices over the last six months. The Telco sectors is dominated Telstra, where earnings would be going backwards if not for the reimbursement from the government for the NBN. Telstra, by their own admission, have a $2-3bn earnings hole to fill over the coming year. So whilst investors may still be attracted by the significant yield on their shares, the uncertainty of their longer term earnings plus the increased competition in the sector makes us cautious on the outlook.

When we look at the earnings expectations above, it’s no surprise that the materials sector was far and away the best performer last calendar year with a very strong rally off a low base.

Source: Thomson Reuters

At the other end of the spectrum, Telecommunication stocks were the worst performing sector with concerns around the NBN pricing structure. The next worst performing sector was Healthcare after a significant sell off from August onwards. This selloff has us interested, particularly as the sector has been the most consistent in terms of earnings growth over recent years and this is expected to continue will expectations of over 10% this year. When share prices stagnate or fall whilst earnings rise, valuations become more attractive and hence we get interested. It’s a sector that we have increased our exposure to over the course of December (adding CSL to the portfolio as the price fell from above $120 to the mid $90s), and one we will watch closely over reporting season.

Along with Healthcare, Technology is a sector which has lagged in recent months whilst earnings expectations have been robust. The sector within the Australian market is small and is an eclectic one. A number of companies trade on high multiples with high expectations of future growth. These companies are susceptible to disappointing such as Aconex just last week. Elsewhere, you can find niche companies with strong products and a high degree of recurring earnings. Given their niche offerings, they are typically ignored by larger institutions and hence can offer attractive opportunities.

So whilst the next three weeks will be interesting, there will still be a number of unanswered questions around the direction of the share market and the Australian economy. We will be busy foraging through reports, checking in with the companies we own and looking for potential new investments whilst always keeping in mind that when investing it is the long term that counts and not just the last six months.

Robert Swift has penned his thoughts on the outlook for Europe and the US in 2017. The most important conclusion we can draw is that equity markets as a whole may struggle however individual sectors and more specific stocks should do well.

2017 Outlook – Trump so far and is 2017 going to be nasty? Robert Swift

Despite all the predictions of doom and gloom, 2016 was a surprisingly decent year for investors in risk assets. Ignoring the signs of unrest at the status quo as evidenced by the Brexit vote, Donald Trump’s victory and the rise of ‘populism’ in Europe, equity markets appear to be sanguine at the prospect of wholesale political change. Markets are also trying their best to ignore a a radical shift in economic policy toward fiscal expansion and an end to ultra-low interest rates.

Are equity investors too sanguine and is 2017 a year of reckoning, when the increased political uncertainty and the end of easy money, is reflected in lower PE ratios as equity investors reduce exposure in favour of ‘safer’ assets? It’s been a few years since we had a negative year for equities. Is 2017 the year?

Financial markets invariably face hurdles such as economic and political risks, valuations, and management changes. In fact, it often said that ‘markets climb the wall of worry’, so these hurdles are not always a bar to making good returns from equities. 2017 will be no different but Donald Trump seems keen to provide a set of new challenges.

The inauguration speech was rather chilling. He emphasised the US jobs lost and loss in wealth of Americans due to globalisation, and what he believes are unfair practices by the Chinese and a very disadvantageous NAFTA deal with Canada and Mexico. This sounds like protectionism to a world used to free movement of capital and increasingly free movement of labour.

The problem with starting protectionist policies is that it is a race to the bottom where everyone loses as prices rise due to retaliatory tariffs being levied by both sides, and trade volumes and spending shrinks magnifying the downturn. This is what happened in the 1930s after Smoot and Hawley, two Congressional politicians, introduced punitive tariffs on imported goods to protect American farmers.

The US could increase tariffs on certain Chinese imports where there is an element of state interventionist “dumping” like steel, but China can retaliate because US carmakers sell a substantial number of vehicles, imported raw materials, and iPhones there. Both sides typically lose. Of course, the trade imbalance is substantially in China’s favour so China would hurt more, but US consumers would be likely to pay more for their goods. China could substitute European goods or raw materials from elsewhere, so Europe could be an inadvertent beneficiary of a China-US trade war.

But protectionism doesn’t just come in the form of tariffs and import restrictions. The President can also veto takeovers perceived to be detrimental to the national interest and could also introduce legislation to restrict overseas companies buying US listed and privately held companies. Of course if he were to do that, then other countries are likely to follow suit with similar legislation of their own. Once this starts happening all companies with some element of takeover premium in their share prices drop and so markets end up lower.

Additionally, the Chinese are major buyers of US government debt and it is conceivable that they would dump this debt driving prices lower and yields higher. This would have an impact on the USA financial and corporate scene unless the USA can find other buyers for its debt at the same price. Recently the Chinese ceased to be the largest foreign owner of USA debt to be replaced by the Japanese. How much more USA debt will the Japanese buy? Probably a lot if the USA plays ‘big brother’ in Asia but the Chinese were big supporters of US debt issuance and their withdrawal will not be easy to replace?

Interestingly the Federal Reserve has just signalled it wishes to reduce its balance sheet so there will be more than just new USA government debt being sold into the market place. Approximately US$ 1.3 tln of existing debt matures this year which the Federal Reserve will no longer be buying. Indigestion is a real risk. US institutions might have to be ‘persuaded’ to buy USA debt which would be a form of repression. It wasn’t so long ago that banks were obliged to hold a certain portion of their assets in the form of government debt. (This has been happening sotto voce in Europe incidentally).

It’s not all negative. Trump did highlight in his inaugural speech his commitment to infrastructure spending, where he highlighted the run-down state of US roads, bridges, airports etc at the expense of overseas wars. There are no concrete figures on this idea but $1tn has been the figure bandied about. He is also talking about corporate and income tax cuts as part of a tax reform package!

Put together these would lead to a substantial rise in US government debts unless the GDP growth rate increases. The US Debt to GDP ratio is already at 104% there isn’t much room for error and there are implications for interest rates, from which equity valuations are derived. The US 10 year Treasury yield currently sits at 2.5% so we are likely to see further upward pressure on interest rates from such policies. He is also said to be targeting a US GDP growth rate of 4% – substantially above the current run rate and current forecasts – a figure that would be consistent with fiscal reflation and substantially higher borrowings. (Frankly given USA demographic trends this is a virtually unobtainable GDP growth number. Additionally, and counterintuitively, he wishes to worsen demographic trends through a much harsher immigration stance).

His speech also highlighted the unfair burden placed on the USA by its NATO partners. NATO members are obliged to spend 2% of their GDP on defence expenditure, yet as the table below shows currently only 5 of the 28 members honour this commitment. In fact, this has been happening for years but no US President has been sufficiently forceful to change the situation. If President Trump were to be successful in this area this would be a significant boost for European defence manufacturers like Airbus, Leonardo, Thales, Safran and BAE Systems.

Boosting spending (albeit much needed on USA infrastructure) and cutting taxes while debt is already high leads some to expect higher inflation. Since equities represent a better investment with MODERATE inflation, equities have performed well even as Donald Trump clearly intends to undo a lot of what went before so it is difficult to make the longer-term predictions on which equity investing depends.

It isn’t just the USA that presents a challenge in 2017

2017 sees political events that could again unsettle the uneasy state of the EU. The first key election is the Dutch general election on 15 March. Geert Wilders the far right anti EU PVV leader, is currently leading the polls. However, we don’t think he wins since proportional representation works against his party. Mr Wilders may make good copy for the newspapers, the Dutch election is likely to be a bit of a red herring in terms of substantially affecting the stability of the EU.

However, France is different and as a bigger economy it is critical. The French Presidential election takes place in 2 rounds between the 23 April and 7 May. Anti EU sentiment has risen substantially in recent years. Increased immigration, terrorist attacks, and poor economic growth are the root cause. While the far right National Front led by Marine Le Pen, has risen significantly in the polls, she is very unlikely to become President. Francois Fillon, head of the conservative Republicans party is the more likely winner. Often described as France’s Margaret Thatcher, he advocates significant economic reform – abolishing wealth taxes, and cutting back the role of the state and reforming public health care. His election would likely be good for the French stock market. We think this will be a positive surprise in 2017 and a boost for European equities in general.

The German Federal election takes place on the 24 September where Angela Merkel seeks to retain her position as Chancellor. Mrs Merkel has been heavily criticised for welcoming over one million migrants from Syria and elsewhere and this has boosted support for the far right AfD from 5% in the polls in 2015 to over 15% today. Mrs Merkel will depend on the absence of bad news for re-election. She may just get it if M. Fillon wins in France and promises to reform the economy.

Overall, we see a rise in support for Eurosceptic parties but they don’t win. The EU remains oblivious and intransigent to the message from ordinary voters so it is rather doubtful that we will see too much change in the way the EU is managed or its direction in 2017. We don’t see the Euro break apart.

So what do I do? Equities vs Bonds vs others?

Global Equities are currently valued at 17x 2017 earnings and a dividend yield of 2.5%. Reasonable but not a great bargain. Our view is that we will see a big dispersion between stock returns this year and that the average return may disguise the opportunity to make great money as an active investor, from the shift to the right in economic policy in the USA and Europe.

We could see higher growth coming from the USA as President Trump outlines his reflationary policies in the first 100 days of office. A more probable lift to equities would be an asset allocation shift from Bonds to Equities. Since the 2008 Global Financial Crisis there have been an overallocation to Bonds relative to historic norms, accelerated in particular by the policy of Quantitative Easing as bond yields were driven by central bank policy.

In fact, evidence of more reflationary policies from the USA may indeed trigger the shift out of bonds, as US bond yields rise inflicting losses on bond holders. Nothing causes investors to move more than losses! But of course the extent of protectionist policies needs to be ascertained before investors feel comfortable in making this move.

In recent years, safe and defensive stocks have outperformed and, the market has seen little disparity between the best and worst stock. This will change in 2017. 2017 may be a year when there is merit in focussing upon cyclical rather than safe companies. Cyclical companies have learned to live with a difficult revenue environment by cutting costs and consequently have very strong operating leverage. Any revenue pick up will see their earnings take-off. We purchased Dow Chemical recently for this reason. Financial stocks have been the ‘whipping boys’ for many years and have been hit with fines, lawsuits and a mountain of legislation. This could be over. These stocks are cheap compared to “safe” stable shares which have been bid up because investors saw no boost to GDP or revenue and wanted safety. M&A is also likely to increase which will put a floor on valuations in certain industries. If management doesn’t improve earnings then someone else will do it for them. We are already seeing a lick up in M&A. Things have changed.

So in our portfolio we are overweight financials, overweight cyclicals and overweight Europe. The only way, for some stocks, is up!

Guy Carson presents his outlook for the 2017 year. WA and Queensland are potential economic problem areas which could have an impact on your banking investments, read on to find out the sector and investments that we believe you need to be focusing on in 2017.

Australian Outlook 2017: Beware the two speed economy

Guy Carson

The Australian Bureau of Statistics will release the December Quarter GDP numbers on March 1 and the focus will be on whether Australia has just experienced its first recession for 25 years. Given the September Quarter saw a negative reading, we only need one more negative quarter to push us there. So, is this likely? Well, based on currently available information our best estimate would be for a slight positive number (although we do have to acknowledge GDP numbers are notoriously unpredictable and we could be completely wrong). Our expectation is that net exports will help prop up GDP on the back of rising commodity prices and hence Australia will once again avoid the dreaded recession.

So does this mean that Australia remains the miracle economy and that we are out of the woods once again? Has the RBA been able to negotiate another slowdown successfully? We are not so sure, and when we delve below the surface of the headline numbers, we see some significant cracks appearing in the Australian Economy.

By now, most people would have heard of the “two speed” economy. It was a term first used back in 2010/11 to describe the boom in the mining states versus the more modest growth rates along the East Coast. Fast forward to today, and the term is used to describe the reverse, with mining states struggling and the East Coast booming.

The below chart looks at State Final Demand across the five largest states, this is a measure of domestic demand in each state. As you can see from below, Western Australia (WA) has a history of booms and busts; however this current bust is the greatest by some distance. For the 12 months to the end of September, State Final Demand in WA fell by a staggering 9.4% and there are very few signs of improvement any time soon. This is more like a depression than a recession.

Source: ABS

In addition, the unemployment rate in WA has risen from a low of 3.5% in 2012 to 6.6% currently, confirming its place as the weakest economy. The rise in the unemployment rate would have been substantially higher if not for a fall in the participation rate at the same time. Overall, the job market in WA has seen a significant deterioration since the end of the mining boom.

Source: ABS

What is driving the divergence between states? The end of the mining boom is an obvious reason why WA is finding life difficult however it doesn’t explain the whole story. To understand the other drivers at play we need to reference a 2007 paper written by US Economist Edward E. Leemer called “Housing IS the Business Cycle”. In this paper, Leemer looks at all the recessions in the United States since World War 2 and finds that 8 out of the 10 were “preceded by substantial problems in housing and consumer durables.” This leads him to conclude that “Housing is the most important sector in our economic recessions, and any attempt to control the business cycle needs to focus especially on residential investment.”

The only two US recessions that are exceptions to the above were the end of the Korean War in 1953, caused by a decline in defence spending, and the 2001 “Tech Wreck”. As the paper was written in 2007, we can now improve the success ratio to 9 out of the last 11 recessions following the 2008 recession, something that Leemer warned about.

The key reason Leemer gives for housing being so important to the economy is that “house prices are very inflexible downward, and when demand softens as it has in 2005 and 2006, we get very little price adjustment but a huge volume drop. For GDP and for employment, it’s the volume that matters.”

In other words, a housing cycle will typically see a drop in transaction volumes and building activity that will lead to job losses and ultimately a downturn in the economy. The multiplier effect with the housing market is large with occupations ranging from developers, builders, agents right through to financiers impacted.

So what does this have to do with Australia? Well, since 2011 the RBA has cut cash rates from 4.75% to 1.5%. They started cutting in 2011 because they saw some headwinds for the economy – most notably the end of the mining construction boom. Mining construction peaked in 2012 and has detracted from growth every year since.

This lowering of the interest rate has led to an unprecedented construction boom in housing, particularly along the East Coast and most notably in apartments. In fact, the current level of dwelling construction per capita in Australia is greater than that of the US at its peak in 2007.

The charts below look at building approvals for apartments across New South Wales, Victoria, Queensland and WA (data is rolling annual). This is a leading indicator of construction activity and we can see all four states have recently reached all-time highs.

Source: ABS

The first state to see building approvals peak was WA. WA approvals peaked in June 2015 and now residential construction is starting to detract from the WA economy. This in conjunction with the continued decline in mining investment (as the major LNG projects complete) makes the prospect of a rebound in WA unlikely.

The reasons behind the rise and fall in WA construction levels are fairly obvious. WA saw significant population growth through immigration from 2003 to 2012. Immigration is pro-cyclical, people move to where there are jobs. As a result with the end of the mining boom, that immigration has slowed dramatically. Unfortunately for WA and most notably Perth, residential developers planned on it continuing and we have had a significant overbuild. This has driven residential vacancy rates up from around 2% in 2014 to 5.1% today.

Source: SQM Research

The increased amount of rental properties has led to a significant decline in rents with house rents down 25.5% over the last 3 years and unit rents down 24.4% over the same time frame.

Source: SQM Research

So we have a situation in WA where:

Final State Demand has fallen 9.4% in the last 12 months;

Unemployment has risen from 3.5% to 6.9%;

We had a residential construction boom which is now in the process of slowing;

We have a continued decline in resource investment when coupled with the slowing residential boom leads to continued weakness in the regional economy.

Rental vacancies have increased substantially due to the residential construction boom and declining immigration;

And as a result rents have gone backwards c. 25% over the last three years.

This situation does not spell good news for the investors in the WA housing market or the holders of the associated housing debt. So when we delve into the banks and look at their arrears by state it is not overly surprising that we have seen a significant increase in WA over the last 12 months. (Clockwise from top left: ANZ, CBA, WBC, NAB).

Source: Company filings

The uptick at this stage has only been seen at arrears level. To a large degree it is remained out of the profit numbers to date but we’d expect this to change over the next 12 months. Whilst we have seen provisioning increase this year from all the banks, that has come through the corporate book, from this point we expect to see the increase in the much larger consumer book.

Moving on from WA, the next housing construction market that looks set to peak is Queensland and we are starting to see some familiar signs. Rental vacancy rates have jumped to 3.7% recently and have trended up for the last 4 years.

Source: SQM Research

Over the last 12 months, 5000 units have been completed within 5km of the Brisbane CBD, that supply is clearly having an impact. Looking at the next 12 months, that figure is set to double; adding significantly more supply to what appears an oversupplied market. Brisbane is therefore potentially 6-12 months behind Perth, but with the scale of building happening in Brisbane it is possible we see an accelerated trend in vacancy rates and rental falls which in turn lead to stress on landlords.

The reason for highlighting these issues within WA and Queensland is the structure of the Australian equity market means that the index (the S&P/ASX200) and a high proportion of individual investors are highly reliant on the banks. Financials represent over 35% of the index and banks comprise around 30%. The financial weight stands out significantly relative to the global index, the MSCI World.

Couple that with the fact that the current ASX200 weight to the banking sector is without precedent in recent decades and as a result makes a poor starting point for inclusion in an investment portfolio.

Source: Goldman Sachs

So with concerns around a sector that comprises around 30% of the index, it is our view that investors need to look elsewhere to deploy capital. Currently our fund has a zero weight to the banks and instead invests a disproportionate amount of capital into the IT sector.

Whilst the banking sector is over-represented in Australia relative to global markets, the IT sector is severely under-represented at 1.4% versus 14.6% for the MSCI World. Given that relatively small size, it is a sector that is largely ignored by large institutional investors. This provides opportunities for those willing to investigate.

When we delve into the IT sector, we actually find a number of companies (primarily specialising in software) that are significant global players within a niche segment. These companies often exhibit many of the characteristics we look for in a quality company. In particular, they have:

A high degree of recurring revenue.

Low additional costs of bringing on customers, leading to high margins.

Very low capital costs leading to high returns on capital.

Our top five holdings contain three such software companies:

Gentrack – a New Zealand based company software company specialising in billing for Utilities and Airport management software. Currently services 15 out of the top 100 airports globally.

Altium – a company that designs software for the design and manufacture of Printed Circuit Boards. They are the fourth largest player in the PCB software market globally, having grown from a 10% to 16% market share over the last year.

Integrated Research – a leading global provider of performance management software for critical IT infrastructure, payments and communications systems. Amongst their clients are the 10 largest US banks, 6 of the 10 biggest Telcos globally and 120 of the Fortune 500.

Whilst these companies have come into our portfolio through our bottom up process, it seems difficult to foresee a scenario in 5 or 10 years’ time that the IT sector remains at a 1.4% weighting in the ASX. With the structural tailwinds behind technology and automation and the amount that corporations and individuals rely on it, IT is set to be one of the fastest growing sectors. However, that is a story for another time.

The team at DMX, managers of the TAMIM Australian Equity Small Cap IMA, take a look forward to 2017.

2017 Outlook: Value well placed to shine

Summary:

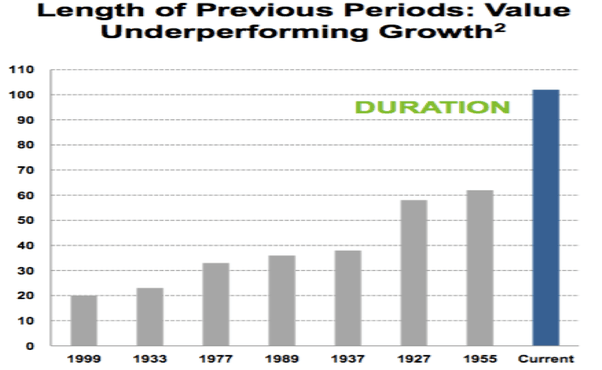

As passionate value investors we believe buying under-valued and largely unknown smaller companies is a sensible long term investment strategy, and a key driver behind the significant out-performance of the All Ords since launch 21 months ago. We view the current valuation differential between value and growth stocks, as well as the global macro backdrop, as particularly supportive of value stocks in the year ahead. We believe our investors are well placed to benefit.

Value Investing at an Extreme:

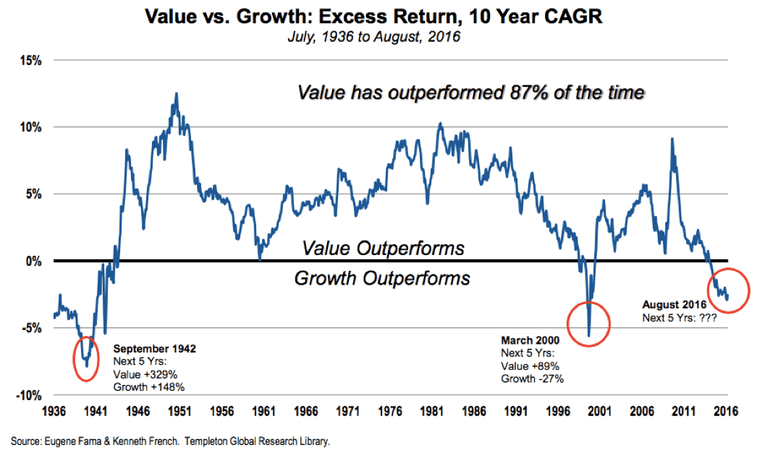

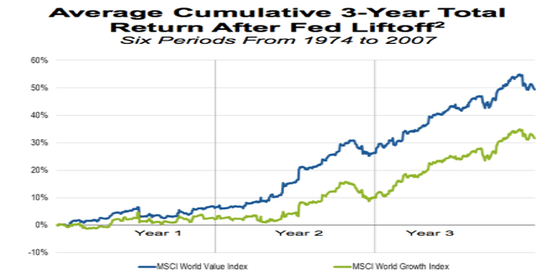

As a starting point let’s look at the very long term performance data regarding value versus growth investing. Value investing as a strategy has out-performed growth investing 87% of the time over the past 80 years as shown by the most recent Templeton analysis using 80 years of data:

However, value investing has dramatically under-performed growth investing since the global financial crisis, and the recent under-performance of value versus growth has been extreme:

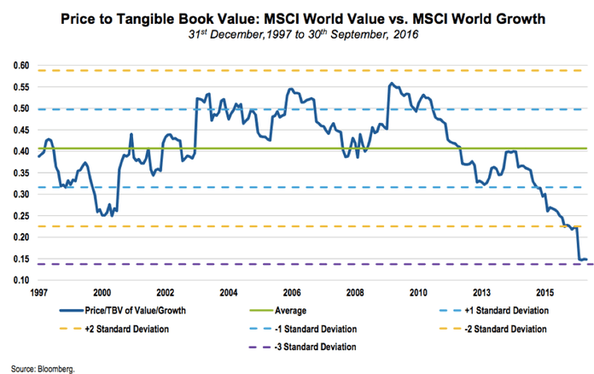

As a result, the valuation gap between value and growth stocks is currently at a long term extreme:

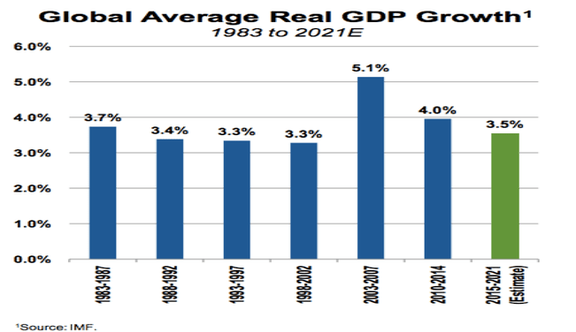

At a time when global economic growth is relatively stable/normal:

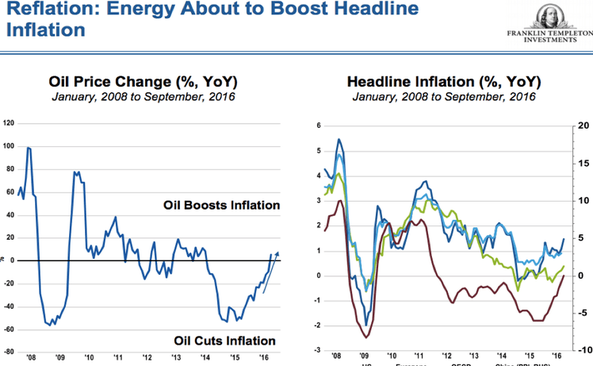

Inflation has started trending upwards (source: Templeton):

And interest rate risk is now clearly on the upside as highlighted on numerous recent occasions by the Fed. Historically, a rising interest rate environment has dramatic implications for value investing as growth stock valuations tend to suffer in the face of a higher discount rate which forces investors towards the cheaper end of the investment spectrum:

The unusually long period of growth out-performance versus value looks to have ended, which bodes well for value investing as a strategy looking forward. We view the current market environment as ideally suited to a disciplined and focused value strategy.

Source: Templeton

Conclusion:

We remain committed value investors in our underlying smaller companies’ fund and believe the outlook for value investing as a strategy is particularly attractive at this stage. With interest rate and inflation risk now clearly on the upside, investors are likely to focus more on underlying valuations looking forward. The outstanding out-performance of the All Ords over the past 21 months has been achieved despite the value investing headwinds evident throughout this period. We look forward to a period with value investing tailwinds behind us.

This week the team at DMX, managers on the TAMIM Australian Equity Small Cap IMA, review some of their portfolio holdings following AGM season. They discuss their positions in Fiducian, Konekt, SDI, Pioneer, Paragon & Joyce Corporation.

Small Cap AGM Season Review

November saw some significant news flow and material share price movements across the portfolio. Key positive contributors to the November results included ASX:KKT and ASX:FID, while ASX:SDI and ASX:ENN were key negative contributors.

Our cash levels remain elevated at month end which is a function of exiting/reducing several positions during the month, and in part to provide funding for some opportunities we have committed to in December.

Annual General Meeting season for ASX listed companies continued through November. Below we comment on AGM highlights and trading updates from a selection of our previously discussed positions.

Paragon Care Limited (ASX:PGC) Paragon Care Limited (ASX:PGC), a leading provider of consumables and equipment to hospitals and aged care facilities, advised that it had enjoyed a strong start to FY17.

Strong growth was being delivered across key financial metrics. In the first quarter of FY17, the company’s EBITDA on a like for like basis was 12% up over the prior corresponding quarter.PGC reaffirmed expectations of strong earnings growth for FY17, with FY17 being the first full year of earnings capture from it 2015 acquisitions. Paragon is targeting strong growth in FY17 across all key metrics.

PGC also provided medium term ‘targets’ for revenue of $250m and EBITDA of $37.5m, to be driven by strong double digit organic growth and value accretive M&A transactions. This would represent a significant step up from FY17 expectations(Revenue: ~$120m, EBITDA: ~$17m).

Fiducian Group Limited (ASX:FID)

Fiducian Group Limited (ASX:FID), the financial planning and funds management group, advised that it has significant capacity and strategies in place for further growth in its traditional revenue base. It expects its funds under administration to continue to grow and, in particular, benefit from recent financial planning acquisitions.FID advised that its unaudited profit for the first quarter of FY17 is ahead of budget, and funds under administration have grown since June as a result of both good inflows and funds performance.

Medium term growth for FID will be delivered by:

Growing funds under advice organically and through strategic acquisitions of financial planning businesses;

Expanding its platform administration servicesto IFAs and capture of market share where value accretive;

Building its SMSF services and continuing to deliver superior investment performance through its funds and attracting IFAs.

Konekt Limited (ASX:KKT)

Konekt Limited (ASX:KKT) advised it had commenced the first four months of the year strongly, with revenue more than 35% ahead of the prior corresponding period (which only had marginal acquired revenue included). KKT had previously advised that it expected FY17 revenue of between $50m – $53m driven by both organic growth and the full year impact of acquisitions completed in the year. KKT now upgrade this to a range of $51m – $53.5m.Despite a significant investment in a range of business improvement initiatives in the first half of FY17, KKT expects to hold its EBITDA margin for the first half at around its FY16 level (10%). On the back of these first half investments, KKT expect a strong improvement in margins in the second half, such that full year EBITDA is expected to be in the range of 10.5%- 11.5%.

We attended the KKT AGM, and noted that the company was very confident of further growth. The CEO, Damian Banks, advised that “more upside remains available to us and we have a strong company leadership group building our business”.

Pioneer Credit Limited (ASX:PNC)

Pioneer Credit Limited (ASX:PNC) advised at its AGM that it was excited about the way in which FY17 had commenced, and that another year of high quality growth was underway.

PNC has approximately 85% of its forecast investment of $50m for the year under contract, and about 40% of its expected investment for the following year also contracted – a significant improvement in visibility on prior years. PNC reiterated its guidance for the full year of statutory NPAT of at least $10.5m.

PNC continues to work towards the launch of a range of new financial products, with the launch of a white label credit card nearing finalisation. The expansion of PNC’s new venture focused on funding, Pioneer Credit Connect, is taking shape as can be seen from its new website: http://www.pioneercreditconnect.com.au/.

SDI Limited (ASX:SDI)

Prior to its AGM, dental products manufacturer SDI Limited (ASX:SDI) reported that not-withstanding good sales growth, it was on track to report a lower first half profit than the previous year.A key reason for the disappointing fall in profit was surprisingly strong sales growth in the UK (+18% on PCP) resulting in relatively lower gross margins due to the weakness of the pound. Currency translation and tax timing issues also are expected to impact after tax profit – unfortunately this was not clearly disclosed to the market by SDI in its trading update, and its share price fell materially.

The core investment thesis for SDI remains unchanged: it is a growing, vertically integrated global dental manufacturer with quality IP, high margins and a strong pipeline of new products.

However, the episode certainly highlights (again) the need for improved market communication from SDI, and re-focuses the market on the currency risk inherent in the business and the resultant impact on profit.

Joyce Corporation Limited (ASX: JYC)

Investment company Joyce Corporation Limited (ASX:JYC) noted at its AGM a strong start to the year, maintaining a relatively high rate of revenue growth for the first quarter.

Total written sales across the JYC businesses (including franchisee sales), is expected to be within the range of $180m- $200m in FY17. “At this early stage it appearsto be tracking toward the higher end of this range.” This represents an upgrade on the previously advised level of $170m.

In FY17, JYC will benefit from the earnings contribution from its Lloyds business (~$1.4m EBITDA), and (from January 2017) savings of $380k p.a. when it moves into its new wholly owned property, and we expect its FY17 NPAT to exceed $3m (FY16: $1.9m; +58%). The company continues to hold a large cash balance and property assets and is on a +7% dividend yield.

JYC remains very cheap, but suffers from poor liquidity, complicated accounting and poor market awareness. With its strong balance sheet, JYC has the capacity to acquire a further business with EBITDA of up to $1.5m without taking on any operational debt. A fourth business would further diversify revenues and put JYC on target for an NPAT (after minorities) of north of $4m.