Mixed results from CSL though beats on management guidance, which has historically been on the conservative side. In our previous notes, we had mentioned the likely headwinds to plasma collection as a result of Covid and the associated lockdowns. While the company did continue to expand its collection footprint across the US, it was disappointing to see a sharp decline, coming in at about 80% of 2019 volumes. Numbers wise, stellar growth across profit and revenue with revenue up 15% and NPAT up 44%.

Looking at the results in slightly more depth, this was driven primarily by Seqris and the increased demand for seasonal influenza vaccines (+44%). Importantly, gross margins continue to increase substantially, a clear sign of management discipline. There are signs of renewed life across the Albumin product line with hospitals back to 90% capacity in China and associated increases to elective surgery. Across the hemophilia market, the numbers were a little mixed, with sales flat or in some cases declining due to competitive pressures (this was expected). Ironically, the stimulus packages in the US may have been a headwind for the company (i.e. disincentivising plasma collection primarily in lower socioeconomic households). Nevertheless, management seems to have a clear vision to grow the supply network and add on collection centres (44 to be exact).

Going forward, however, management only reaffirmed earnings guidance of 6-10%, which implies that 12-20% of FY21 earnings will be generated in the second half. This is substantially lower than the 5-year average of 40%. A substantial decline in growth.

Red Flags & Risks: While a decline in collections was to be expected, the scale (i.e. 20%) is still daunting. Especially so when compared to competitors. Grifols (GRF.BME), CSL’s Spanish rival, has made significant strides in its plasma collection infrastructure, especially in mainland China (i.e. Shanghai). No further guidance or elucidation was given pertaining to the Vitaeris acquisition, which had at the time of acquisition been conducting Phase III trials pertaining to organ rejection within kidney transplants. The results across Asia also looked particularly messy with a decline of 9% in the Seqirus product line. Again, we reiterate the crucial nature of the APAC region for continued growth.

My Expectations: The company continues to be a long-term hold for me. But at $274 AUD it remains fully priced and might see some volatility especially as the market digests what is likely to be a less than stellar 2H.

Dividend Yield: 1.06% (Assuming a share price of $274.50). Expectation remains that dividends continue to grow at double digits over the long-term.

Wesfarmers (WES.ASX)

Wesfarmers continues its fantastic performance and showcases the value add of having a diverse portfolio (not many firms can pull off a conglomerate structure, i.e. GE). For those that insist that brick-and-mortar retail is dead, both Kmart and Officeworks seem to be proving otherwise (at least for now). Kmart’s revenues increased by 9% with Officeworks’ increasing 29%. Target remains a problem child, but management seems to be executing on its omnichannel strategy nevertheless with online penetration increasing to 15.9% in 1H. The numbers are similar with Kmart, increasing to 8.9%. What was interesting delving deeper into the numbers was the increased purchase size for online orders (approx. 2x), with the majority of fulfillment taking place in store.

Across the Chemicals, Energy and Fertilizers (CEF) division however, the numbers are a little less stellar with revenues declining 6.6% and an earnings decline of 7.5%. Much of this may be transitory in nature though, not least due to continued weakness in Saudi contract prices. Given our thesis around commodities such as iron ore and gold, we would hazard a guess that we will likely see a revitalisation of demand for ammonium nitrate as well as sodium cyanide (crucial for gold mining). In other news, progress has been made pertaining to the Mt Holland lithium project (JV with SQM).

Red Flags & Risks: CEF division is getting increasingly competitive, especially with Orica (ORI.ASX) opening up a new plant in Barrup. Much will be contingent on continued demand from both iron ore producers and a recovery in gold mining (closed due to Covid measures). For retail, temporary closures and continued diminishing of margins as well as rental pressures remain the key downside risks going forward.

My Expectations: Management continues to deliver. In my previous notes, we mentioned that the failed bid for Lynas (LYS.ASX) was potentially a sign of what management’s focus is likely to be going forward. The Mt. Holland project confirms this. Though, given the trends we have seen, we still feel that Lynas would have been a great addition to the portfolio. We fully expect greater focus to be placed on CEF going forward and turning it around despite increased competition. Nevertheless, kudos to management.

Dividend Yield: 3.31% assuming a share price of $54.29 AUD. Expectation is that this will stay stable on a nominal basis.

Continuing to work our way through the ASX20, this week we visit and review BHP Group (BHP.ASX) and Fortescue Metals Group (FMG.ASX).

Context:

Author: Sid Ruttala

At TAMIM we remain of the view that, given the global impetus for an expansion of fiscal stimulus combined with substantial increases to infrastructure spending, we are about to enter a secular bull cycle in commodities. For those of you unaware of this argument, feel free to refer to previous articles on this particular issue and the rationale behind it. However, there is a caveat. There are certain commodities that are more likely to perform better than others moving forward. Not least because the price action so far may have already baked in some of this future growth.

So what are our favourites at this stage? Copper, aluminium and oil. Not so favourable in the short-run is iron ore (despite our long-term bullish view on the commodity).

The rationale for this view? Let’s examine copper first and why we think that this is one commodity likely to go significantly higher, even in the short- to medium-term, despite spot prices now hitting close to 9, 940 USD per metric tonne at the time of writing. There are two reasons why I believe this to be the case:

The minerals game is heavily capital intensive and requires a long lead time from exploration to first production (an average of 8-9 years for greenfield projects). One of the key issues for Dr Copper has been the scale of the lack of investment in new copper production over the past decade, due almost entirely to its previous collapse in 2015-2016. Five years on, the world has seen very few new tier-1 assets come online outside of Rio Tinto’s Winu and SolGold’s Cascabel, which both BHP and Newcrest remain in contention for (though the company has been doing its best to remain independent).

All this comes at precisely the time when governments globally continue their push for new infrastructure, more specifically green infrastructure, as a way to stimulate growth. A single 660 kW wind turbine, for example, contains approximately 800 pounds of copper and a photovoltaic solar plant requires about 5.5-5.6 tonnes of copper per megawatt generated. If we assume current growth trajectory in output in terms of production and assume current rates of capex, our view is that there could be a supply gap of close to 10mT by 2031. In the short- to medium-term, we could easily see spot prices hit above $13,000 USD even on news flow related to the passage of the Biden infrastructure bill (much more consensus than the minimum wage issue and could be done via reconciliation with the current majority).

Similarly, aluminum should also see some catalysts, not only with the infrastructure spending but also the reflation trade (i.e. consumer electronics and

retail construction). In the case of oil, we have previously written about the likelihood of US shale production declining rapidly through to the end of the year and my overall bullishness due to increased demand as the world comes out of lockdowns. Reiterating my view, oil will see $80 USD per barrel before the end of the calendar year (though this may only be short-lived). For Iron ore, my view is a short-term bear market. This is despite my previous assertions that, even in the expectation of Brazil’s Vale coming back online, the demand generated by fiscal stimulus for steel should see spot prices continue higher. But at $185 USD/tonne, it is looking rather toppy despite China’s continued growth in steel production. We see substantial headwinds for Chinese demand as the CCP tries to reign in steel production and gets rid of export incentives. Long term spot prices should trend higher, but spot prices are now where I expected them to be mid-next year assuming continued global recovery, that is, not quite so soon (i.e. when I previously wrote on this the price was about $112 USD/tonne).

So with that context in mind, let’s proceed to the securities in question.

BHP Group (BHP.ASX)

Stellar results from BHP with EBITDA of $14.7bn USD (up 21%), margin of 59% and, most importantly for the yield hunters, a 101c US p/s dividend. This was pleasantly higher than expected and supports my thesis of the business being an effective substitute for the banks for the income starved investor. On the flipside, the company’s copper production declined 9%, unfortunate given the high demand globally but somewhat expected due to short-term declines in production at Escondida though cost guidance has been lowered going forward. The grades are also likely to lower as the mine continues through its maturity. Somewhat surprising however was Olympic Dam which continues to maintain production. Petroleum production continues higher with about 9%. Importantly, BHP’s increased interest in the Shenzi platform – a deepwater oil and gas field in the Gulf of Mexico with a processing capacity of 100,000 barrels per day along with a handling capacity of 50m cubic feet of gas – should see production continue to increase through ‘21-’22. This is an exciting prospect. That being said, we would have liked to have seen more acquisitions within both petroleum and copper but stellar results so far with costs being kept minimum.

On the coal front, metallurgical (met) coal production increased slightly by 1% while thermal continued its dismal performance, -17% year on year, driven by strikes and labour issues in Colombia. Mt Arthur’s wet weather also didn’t help. There has been little progress on the divestment of the coal assets which, in my view, remains a headache for the company going forward and the sooner this takes place the better. Though any divestment deal would probably have to be sweetened with better performing assets (perhaps even on top of the Bass Strait Gas assets as mentioned six months ago). An IPO/bundle and spin out of the assets could be on the cards but I have doubts that the market would pay a decent multiple given how the space has been tracking recently.

Red Flags & Risks: Many of my red flags remain the same. While BHP remains diversified in terms of commodities, weakening demand for steel production in China could hamper future growth and much will be contingent on maintaining cost discipline. The divestment of the coal assets and a strategy around this still remains the biggest issue. Chile’s recent proposals to change the tax laws pertaining to mining remain a big risk for the company, though we doubt passage is likely with a staunchly conservative President.

My Expectations: Management continues to deliver and has pleasantly surprised on the cost front. We would like to see more corporate development, especially in Copper and especially in LATAM. Ecuador remains a key focus for the firm but we have yet to see significant acquisitions. One would hope to see a resolution on the coal business before the beginning of the new year but I don’t have much optimism. Nevertheless, this is one I would personally continue to hold.

Dividend Yield: Assuming a share price of $48 AUD, then BHP has a great 4.1% dividend yield.

BHP remains a credible substitute for the banks from an income perspective.

Fortescue Metals Group (FMG.ASX)

Fortescue continues to forge ahead but remain too expensive compared to their peers for my liking. Numbers-wise, a mixed to decent result. There was some weaker than expected production in March with shipments flat YoY, a new record EBIDTA of 6.6bn for H1FY21, a gross margin on iron ore of 71%. Importantly for the dividend hungry investor, a $1.47 interim dividend per share, representing a payout ratio of 80% (slightly higher then the 77% mentioned in my previous write up).

In terms of capex and additional projects, the increase is likely to be 10% more than expected. The EnergyConnect project, which aims to decrease the firm’s carbon footprint by investing in hybrid solar-gas transmission infrastructure, though going according to plan is likely to increase capex to around $4bn USD, though the guidance has been to $3.4bn USD. I base this on likely additional cost escalations in Iron Bridge. The firm retains close to $4.3bn in debt. Going forward in the short- to medium-term, FMG remains fair value at $22.26 AUD per share.

Red Flags & Risks: FMG is a leveraged exposure to the iron ore spot price. Personally, I remain convinced that the spot price is relatively overvalued (on a short- to medium-term outlook). FMG also trades at a significant premium to NAV (1.4x) compared to counterparts BHP and RIO. That being said, I remain a big fan of Elizabeth Gaines (and Twiggy), who cannot be faulted in her execution or cost discipline. In the medium- to longer-term the overreliance on Chinese steel manufacturers might hurt prospects. As mentioned, there is a marked push to move production out of China.

My Expectations: While Vale production still remains below market expectations, I remain a little uncertain about the price action for iron ore. FMG remains a good long-term investment but, nevertheless, it might pay to take some profits in order to buy back at a later date (hopefully lower).

Dividend Yield: The current dividend yield stands at an exceptional 13%, assuming a price of $22.26 AUD.

This week we will be talking about a little known Australian micro cap company, K2Fly (K2F.ASX). K2F is an enterprise software company that is looking to capitalise on a major transformation in the mining industry. K2F offers SaaS (software as a service) solutions helping mining companies improve their ESG (environmental, social and governance) standards. They also provide consulting and tailored advice for asset intensive industries including mining, utilities, infrastructure and government.

Why SaaS Business Models Are Attractive

Author: Adam Wolf

SaaS revenue models are especially attractive for investors as their revenue is mainly recurring almost like an annuity. Another feature of SaaS revenue is that it is typically quite sticky. This simply means that their customers will have a hard time shifting away from already integrated software, a costly exercise often requiring consultants, which makes these segments of K2F’s revenue highly sustainable. There are plenty of SaaS companies on the ASX but K2F stands out from their SaaS peers as they offer exposure to both commodities and an emerging thematic.

Key Financial Metrics | K2F

K2F’s annual recurring revenue sits at just under $3m with their total contract value over $9m. After the completion of a $7.25m placement in April, K2F now has $8.75m cash plus $1.5m in receivables with no debt. Their market cap is currently sitting just north of $42m.

Source: Company filings

K2F has grown their ARR 80% from Q3 FY20 to Q3 FY21.

ESG As A Thematic

The shift to ESG practices has become a thematic the world over. We now see a greater emphasis on companies having a plan for sustainability as well as taking responsibility for their societal impacts. As a result, we have seen institutional investors allocate more money towards companies that are more sustainable and have better ESG credentials. On the flip side, this drains capital from companies that are perceived to have poor sustainability and negative impacts on the environment such as oil and coal producers. K2F offers investors an opportunity to benefit from the rise of ESG investing.

Recently we saw RIO Tinto blow up a 45,000 year old indigenous cave system which led to the firing of the CEO and a few other key executives. Losing their jobs due to ethical wrong doings is front of mind for many C-suite mining executives around the world and there is increasing pressure from stakeholders in mining companies to engage with their surrounding communities, disclose mineral resource information and to minimise their impact on the environment. K2Fly is looking to address and capitalise on these issues.

(As a side note, RIO recently entered into an agreement with K2F worth $720,000 to integrate K2Fly’s community and heritage software).

K2F Product Offerings

Over the past few years K2F has a built a well-rounded arsenal of ESG software solutions for mining companies to:

Accurately report their mineral resources in compliance with their respective exchanges

Enable geology teams to streamline and automate pit block outs, spatial data, logging, sampling, and assay results to better understand material grade and behaviour

Help improve compliance and provide the visibility to reduce risks and support accurate disclosure as well as helping environmental, rehabilitation, community and mine management teams globally to improve relinquishment, tracking of closure and achieving rehabilitation targets

Manage their tenements in regard to cultural heritage and surrounding communities (i.e. avoiding a RIO repeat…)

K2F’s Strategy: Land and Expand

K2F have expanded their product offering for mining companies through acquisitions. This has been part of their strategy to “land and expand”, that is to leverage existing relationships with top tier miners to then cross sell their complementary solutions. K2F’s customers are comprised of high profile tier one clients, including 3/4 of the iron ore majors and 5/10 gold majors. Their solutions are used in 54 countries across 45 different commodities.

At the back end of last year, K2F’s solutions were endorsed by SAP, the biggest enterprise software company in the world. K2F is one of just twelve companies globally to be awarded the certification which is an amazing achievement given the size of K2F. SAP have relationships with 98/100 of the biggest mining companies and are now incentivised to sell K2F’s products. This provides K2F with a big runway to execute their “Land and Expand” strategy.

Recently, K2F acquired Decipher which was developed and operated by WesCEF, a subsidiary of Wesfarmers. Decipher offers award-winning cloud-based software-as-a-service monitoring and compliance solutions in tailings management and rehabilitation for mining industry customers. This has not only expanded K2F’s offering but also put Wesfarmers on K2F’s share registry as a substantial (10%) holder .

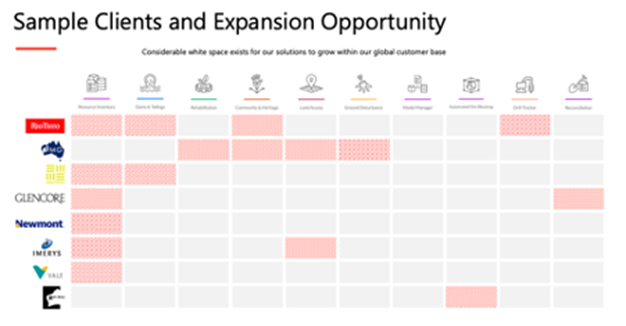

The sample below highlights the opportunity K2F has to cross sell their products to existing costumers. The grey boxes represent cross selling opportunities. This sample alone shows that only 20% of their products are being utilised. As K2F continues to develop new solutions and seek strategic acquisitions, this opportunity will only get bigger.

Outlook and Thesis

On the back of their endorsement by SAP, K2F can capitalise on the relationships that SAP has with the top tier mining companies and look to cross sell their solutions. The management team has experience across the mining and software industry and is led by CEO Brian Miller who co-founded AMT-Sybex, a software company providing services to the energy and utilities sector who were taken over for $150m+ AUD in 2014 (delivering tremendous shareholder value).

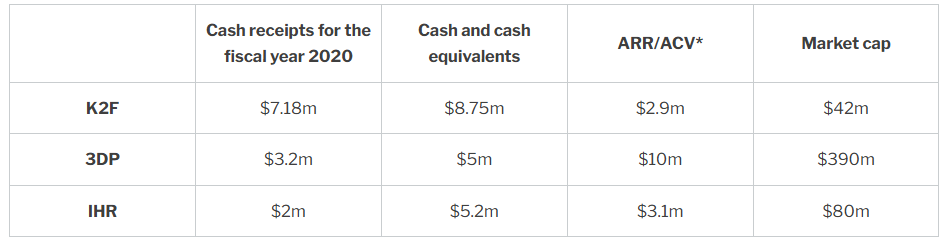

A comparison with geospatial data company Pointerra (3DP.ASX), which K2F is affiliated with through the integration of 3DP into their new acquisition Decipher, and cloud based software IntelliHR (IHR.ASX) is rather compelling and gives some food for thought on K2F’s current valuation. The table highlights how low a cash flow multiple K2F is trading at and what a cornerstone investor like Bevan Slattery can do to a company’s market cap (he took $2.5m positions in each of 3DP and IHR in 2020).

* Note: We used annual recurring revenue for K2F/IHR and annual contract value for 3DP

The thesis here is fairly simple, K2F is at the forefront in benefiting from a major shift in the mining industry whilst also having a positive impact on society, something that investors are beginning to value more and more. At a market capitalisation of just $42m with $9.25m in cash and receivables, K2F offers material upside as they look to add new solutions and use their existing relationships with miners as well as their partnership with SAP to cross sell their products and increase annual recurring revenue. In addition to this, there has also been a run up in commodity prices and a lot of talk about a “commodity super cycle”. This will only benefit K2F as more mines are brought to production, increasing the demand for mining services companies. K2F have provided strong updates to the market and are in advanced talks over further contract agreements. They are cashed up and can use the money for further acquisitions that could expand their product offerings as well as develop their own solutions tailored to the feedback of current customers. We also expect K2F to begin looking for products to offer to the oil and gas sector which will increase their addressable market significantly.

Disclaimer: K2F is personally owned by the author of this piece. It is not owned in any TAMIM portfolios.

This week we take a look at one of our top performing investments from the last year, a stock we wrote about on multiple occasions. This week we would like to explain our investment journey; why we backed the company then, our entry and exit prices and ultimately what changed our mind in January and February this year that caused us sell the stock.

Authors: Ron Shamgar

Redbubble (RBL.ASX) is an e-commerce marketplace that connects consumers with artists globally. The business model is one we like; it enables shoppers to choose from many different designs and product categories and get it printed on demand. This business model is favourable as it carries no inventory risk and the company receives the purchase payment upfront while paying artists and fulfillers after.

In mid-2020 we took a position in RBL at around the $3.00 mark. As we articulated last year on many occasions, businesses that facilitated and enabled consumers to shop online during lockdowns and restrictions were amongst our so called “Covid Winners”.

Source: Yahoo Finance

Unlike many of its peers, RBL was cashed up and profitable. It also operated on a global scale which meant it wasn’t limited by its addressable market like some of its land constrained peers, Kogan (KGN.ASX) and Temple & Webster (TPW.ASX).

During 1H2021, RBL reported strong sales growth and profitability was on track to hit $60m of EBITDA by 1H. Cashflows were strong with cash balances ballooning to over $100m. RBL was not only benefitting from consumer demand for online shopping, but also from reduced marketing costs and higher gross margins in (temporarily high demand) products like face masks.

We understood from day one that RBL would likely struggle to maintain elevated sales growth in 2H2021 and beyond. We did however believe that, due to the global nature of its business, RBL could maintain growth and profitability, albeit at a lower level. We also expected management to begin paying dividends to investors. Our valuation over 1H2021 increased to $7.00 based on consensus estimates. We also had a bullish best-case scenario valuation of $10.00 had RBL achieved our estimate of $100m EBITDA in FY21.

During January 2021 the stock exceeded our valuation of $7.00 and we sold down substantially to secure profits for our investors. We maintained a small position going into the Q2 update.

There are many sayings in investing, but one that never fails is that “good news travels fast”.

The market (and us), were expecting very strong sales and EBITDA figures for Q2 and there was an expectation that management would update the market by late January. As the news never came, we became concerned and reduced our holding even further at $7.00+ as the risk/reward trade off was no longer balanced.

RBL reported Q2 results during its half year result in late February and although sales were as expected, gross margins were significantly below expectations as competition increased. We exited our holding above $6.00 on the day. Overall, RBL was one of our top performing stocks in 2020.

Last week, RBL provided a Q3 update to investors and laid out a new strategy for investors under the reign of recently appointed CEO Michael J. Ilczynski. As we no longer owned the stock, we looked on with interest from the sidelines.

Unfortunately for investors, the update was disappointing as sales growth slowed down and profitability completely disappeared as margins were heavily impacted by discounting and increased marketing spend. To make matters worse, the new CEO laid out a strategy of reinvestment and lower profits for the next two years to drive top line growth.

The ultimate reward for investors is a $1.25bn sales target beyond 2024 and EBITDA margins of 10-15%. Essentially, or in other words, the company now needs to spend more on marketing to stay competitive and relevant. Investors were not impressed and sent the stock to $4.00.

So, does RBL now present a buying opportunity

At this stage we don’t believe so. There are serious headwinds for the company for the remainder of CY2021. These short term hurdles include cycling the elevated sales from the lockdowns from April to December last year and a persistently stronger AUD, which has appreciated 17% against the USD (RBL’s main sales currency).

To make matters worse, RBL was added to the ASX200 index just three days before the disappointing update. It is now likely that RBL will be removed from the index on the next rebalance, adding more artificial selling pressure to the share price.

Overall, we did well out of RBL and we may re-enter the stock at some point in the future. Experience has taught us that there is no immediate rush to do so, and we will want to see a material discount to our updated valuation of $4.50, based on consensus forecasts for the next two years.

As promised, this week we continue to look through some of the key highlights, and my notes, on the top end of the market. The securities this week are NAB and ANZ.

National Australia Bank (NAB.ASX

NAB has started off in stellar fashion this year with the key highlights for the first quarter being an increase in cash earnings by 47% over the preceding average, to $1.65bn. The caveat here being that revenue grew only slightly above 1% (though the headline might show otherwise (i.e. -3%), this was a result of MtM losses in markets and treasury income). The cash earnings were driven primarily by a decline in bad and doubtful debts (BDD) to the tune of 98% to $15m and the business continued to see a substantive decline in loan deferrals with home loan deferrals declining to $2bn and $1bn for business loans.

The business has been helped along by Australia’s ever-buoyant property market as well as a favourable policy environment with initiatives like the first home loan deposit scheme. Management has continued to increase asset quality as reflected by the fall in credit impairment charges and existing deferrals better than the previous year’s guidance. The bank continues to remain well capitalised at 11.7% (CET1), slightly higher than the previous 11.6%. Management has continued to demonstrate a desire to keep up with the times, introducing the first interest free credit card in an effort to keep up with BNPL. Though we don’t see this as substantive, in a similar manner to CBA’s own program, it allows for customer retention and should increase overall profitability per customer.

On the matter of the bottom line, management has continued to deliver on its cost cutting measures with expenses falling 1% in 2H2020 and guidance of a further limitation of 0-2% on expense growth going forward. That said, NIM’s have continued to disappoint slightly, being similar to CBA in reporting a decline.

Red Flags & Risks: Although the market has seemingly forgotten, remediation costs (or them being higher than expected) could continue to plague the business dispite the sale of the MLC business. In addition, much relies on management successfully executing on expense management and strategic initiatives with uncertainty around the commercial lending book.

My Expectations: We remain consistent in our expectation of NIMs to stabilise at 1.55% over the coming eighteen months. On one aspect, we were pleasantly surprised. That aspect is the continued focus on cost reduction by management. Predicated on the others following suit, if NAB moves its online savings deposits more in line with the RBA cash rate then this should add another 3-5bps to their NIMs.

Dividend Yield: Expected yield of 3.7% (assuming a share price of $26.9 AUD).

ANZ Banking Group (ANZ.ASX)

Going straight to the numbers, NIMs were surprisingly up, up to 1.63% (an increase of 5bps vs. 2H20), though still a laggard among their competitors. This is a great sign to us, especially given the environment surrounding the sector as whole. This was driven primarily by lower funding costs and, most important of all, revenue grew by a stellar 4%. This number excludes the markets division which was our biggest concern through much of last year and remains the big question mark. What has been pleasing to see, however, was that the group reported higher margins on the institutional asset (custodian services, capital raisings, trade finance etc) business.

From a cash profit perspective, the results came in at a stellar $1.62bn while expenses came in flat, showcasing continued discipline when it comes to the balance sheet and operations. The group remains well capitalised and CET1 came in at 11.7%, comparable to NAB. More importantly, 98% of its home loan deferrals pre-covid have returned to payment with restructuring accounting for 1% and transferals to hardship accounting for another 1%. Within the business loan segment, the numbers stand at 90% of deferrals returning to payment with a further 7% restructured with 3% transferred to hardship. Looking at asset quality, the bad debt benefit remained at $150m. We remain of the view that ANZ’s comparatively more diversified balance-sheet and their remaining institutional business somewhat de-risks the business.

Red Flags & Risks: The NIMs are by far the biggest concern when it comes to ANZ and, while management’s improvement in this aspect is to be applauded, they remain substantially lower than their peers. We had previously predicted that the commercial business might get messy and this has turned out to be rather prescient, though it has been much better than expected.

My Expectations: We had previously expected NIMs to stay flat but the business has proven me wrong and now has momentum behind it. We now expect ANZ’s NIMs to play catchup to their peers over the coming quarters.

Dividend Yield: 3.4% expected yield, based on a share price of $29.10 AUD.

Author: Sid Ruttala

An update to my takeaways from six months ago:

Leanest and meanest of the lot: CBA (no change)Cheapest of the lot: Westpac

Previously: NAB. WBC now has momentum behind it.

The laggard of the lot: NAB

Previously: WBC. NAB has continued to deliver as a business, more to do with the fact that Westpac surprised on the upside and is no longer as comparatively cheap.