This week we thought it would be valuable to highlight Ron Shamgar’s recent monthly report. Ron has delivered a stellar return for our investors over the last couple of years, managing the portfolio through the covid crisis with aplomb.

Author: Ron Shamgar

During the month of February the ASX300 was up +1.48% while the Small Ords was up +1.55%.

The TAMIM Fund: Australia All Cap portfolio continued its strong outperformance for 2021 and finished the month up +4.30% net of all fees.

Calendar year to date, the portfolio is up +10.44% net of fees. The strategy has now delivered +20.37% p.a. since inception. More recently, the portfolio has returned +39.73% p.a. over the last two years.

February was a busy period as companies reported their half year results. In most cases, due to covid disruptions, many companies have regularly updated investors on their financial performance. Therefore, the devil was in the detail, so to speak.

One key feature of this reporting season and the first half of FY21 generally, was the way companies adapted their businesses to the new covid environment. In most cases cash flows were quite strong as management teams focused on working capital and cutting costs. This resulted in increased dividend payments which will flow on to investors from March.

Covid has forced companies to operate more efficiently and invest in digital capabilities in order to manage a remote workforce. We see these efficiencies remaining in the future even with the full reopening of economies and easing of restrictions.

Overall, our holdings delivered strong results. We added some new positions and cut some underperforming ones where we have lost confidence in management. We are seeing a lot of new opportunities and value emerging in many companies that should benefit from a post-covid world.

Finally, the biggest topic of discussion and concern for investors this month was long term bond yields increasing due to expectations of inflation. Generally speaking, higher yields lead to lower valuations of growth stocks as investors use this metric to value these businesses future cash flows. We have somewhat anticipated this shift and have recently moved away from some of the “Covid Winners” we have previously discussed and into companies that should benefit from the reopening trade in a post-covid world. We remain focused on the fundamentals of the businesses we own rather than macroeconomic noise. We see that alone, as the ultimate recipe for long term performance.

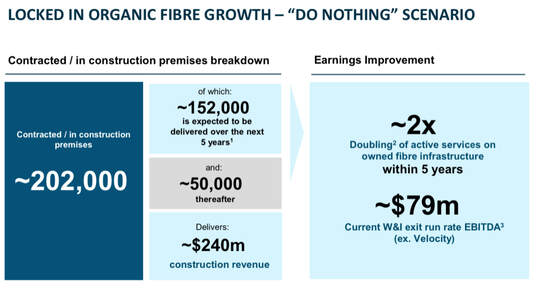

Uniti Group (UWL.ASX) delivered a pre-released result with 1H21 a revenue run rate of $200m and EBITDA of $116m while free cash flows are estimated at $72m. More importantly, approximately $100m of EBITDA will be generated by the high quality and long term wholesale and fibre division.

Source: UWL company highlights

We keep comparing UWL to a higher quality and higher growth mini version of the NBN. As such, we believe the company should be valued as a core infrastructure asset rather than a generic telco. In addition, management highlighted that over the next five years EBITDA should double to $200m purely by executing on the contracted future pipeline of fibre connections. Investors are slowly catching on to the upside and growth story in UWL and the stock has slowly re-rated towards our near term valuation of $2.50.

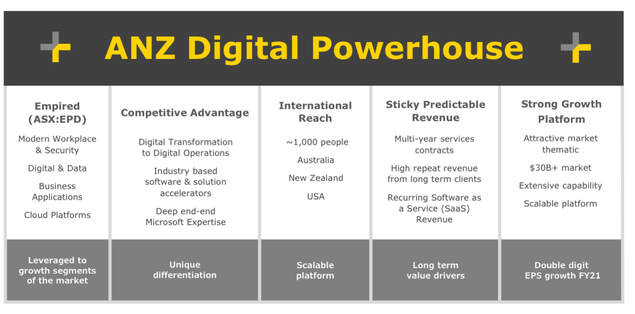

Empired Group (EPD.ASX) delivered a stellar result with revenues up 7% to $90m, EBITDA up 107% to $16.2m and NPAT of $7.7m. Operating cash flows were strong at $17.5m and the company is in a net cash position of $6m. A 1.5 cent interim dividend was also declared for the first time in six years. EPD is a beneficiary of the digital transformation undertaken by large corporates and government agencies. In addition, there is less competition from offshore IT services providers due to border closures.

Source: EPD company filings

EPD expects strong Business Applications growth to further strengthen in 2H21 with an outstanding pipeline of material contract opportunities. We see EPD delivering approximately $32m EBITDA in FY22. This translates to $15m NPAT and makes EPD look cheap at 8x PE and EV/EBITDA of 3.5x. Our valuation is $1.00.

Cardno (CDD.ASX) is a professional infrastructure and environmental services consultancy. 1H revenues were down 11% to $434m while underlying EBITDA was up 10% to $25m and NPATA was $14.m. We expect full year EPS to be in the range of 6-7 cents which makes the stock look incredibly cheap at the current price of 47 cents. Our entry was 33 cents. CDD’s strong balance sheet and cash flows allowed the company to buyback 10% of shares on issue during the half. Accordingly, management declared a 1.5 cent franked dividend.

Source: CDD company filings

We see CDD as a beneficiary of the reopening trade in the post-covid world. Management also provided an upgraded guidance of EBITDA range of $45-50m (a 10% upgrade). We believe CDD is a potential takeover target if the shares remain undervalued. We value the stock at about 70 cents.

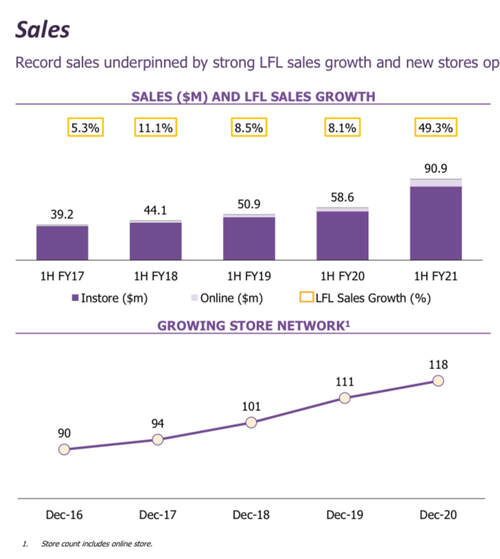

Dusk (DSK.ASX) results came in at the top end of their guidance as, like many retailers, DSK benefitted from covid consumer demand for home fragrances and decor. Sales were up 49%, online sales up 120%, and EBIT of $28.3m (excluding JobKeeper) which was up 194%. DSK also has a net cash balance of $35m. An interim dividend of 15 cents was declared. Pleasingly, management also provided a trading update for the first six weeks of 2H with sales up 55%.

Source: DSK company filings

DSK opened six new stores during the half with the store network now up to 118. Another four new stores and the refurbishment of thirty-six legacy stores is also planned for this year. Longer term, we believe DSK will have to show investors that the company can expand beyond Australia and NZ and into other markets in order to receive a higher valuation compared to peers like Lovisa (LOV.ASX). We took some profits above $3.00 as we have almost doubled our investment since our entry at around the $1.60 mark.