Robert Swift takes a look at the current situation around inflation and looks at how we can invest to maintain our spending power in real terms. A must read for those now receiving next to nothing for their bonds and fixed income.

Author: Robert Swift

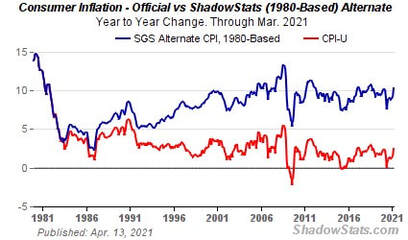

Inflation is here. It really never went away. Hedonic methods of calculating what was already an imprecise gauge of price changes, have obfuscated, and of course lowered, the official figures. If you wish to see what pre-hedonic calculations would have gauged inflation levels to be today, check out the two charts below on inflation as per the 1980 methodology and the 1990 methodology. Both by courtesy of Shadowstats whose authors provide a plethora of ‘real’ economic data.

We also have an admission of sorts that inflation is here and, woops, higher than promised. Don’t wait for any apology. It’s not entirely the current Administration’s fault. The asymmetrical approach to interest rates, inflation and sound money in general started with ‘Maestro’ and has snowballed since.

Nonetheless a perverse sort of Gresham’s Law is applying here – bad policies continue to drive out good. Inflation is the new good thing and we should welcome it. Yet as Ronald Reagan said in 1978, “Inflation is as violent as a mugger, as frightening as an armed robber and as deadly as a hit man.”

Memories indeed are short.

We are potentially near the end of the liberal era of economic policy with which Regan and Thatcher were associated? Prepare for more government, more rules, and different risks.

Since none of us is going to be in charge of macro-economic policy (at least anytime soon) and we have to invest to maintain our spending power in real terms, against this backdrop of understated inflation and carefully massaged negative real interest rates, how should we proceed?

The answer is to look at certain equities as a better inflation hedge and also a hedge against risk of catastrophic corporate failure. Essentially then do not ignore equities even if you are at an ‘advanced age’ .

Conventional wisdom states that the allocation to fixed interest should rise as you get older. A rule of thumb is that you should have your age as a % in fixed income. So at 60, you should have 60% in bonds. At current levels of interest rates and inflation, this will almost certainly guarantee an erosion in real purchasing power. Don’t do it!

Two dimensions should be used to assess which are the better equities to currently overweight if you wish to buy inflation protection:- one is Governance as in “ESG” (which we think still improperly used); the other is sector membership and the stability of revenue growth and asset base.

Below we show how and why better Governed companies have a better survival rate and thus should have a lower discount rate applied to their dividends. These companies are still currently undervalued.

We then show that in the last 40 years, the risk of catastrophic loss in certain USA sectors has been much greater in some than others. Any investor with a time horizon beyond 5 minutes should thus weight their equity exposure to companies in these sectors.

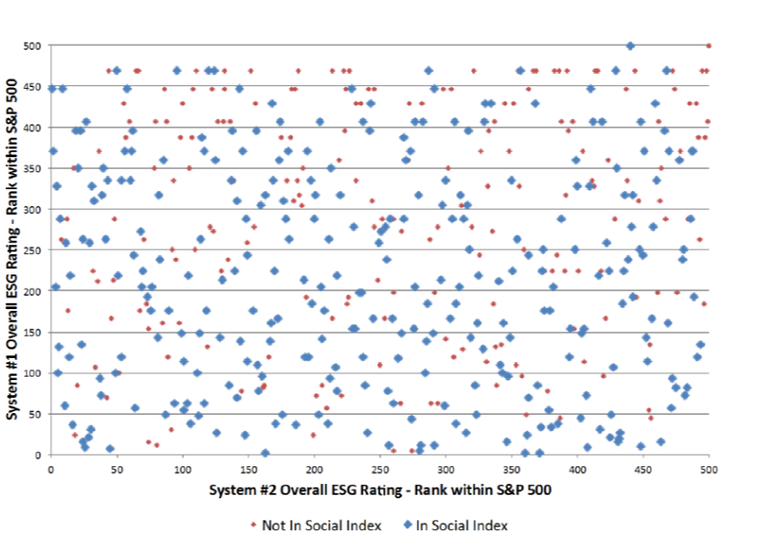

We have written before on ESG and why we think G is relevant as a risk factor but not necessarily as an alpha factor. We show again below the wide range of ESG cores from different ESG ratings agencies, courtesy of Northfield (no alignment).

This article provides a recent assessment of ESG scores and how they are barely useful.

Nonetheless, good G as measured by its impact on corporate financials, IS useful. Sensible leverage, correct levels of re-investment, and staff retention are all part of any Fundamental or Qualitative assessment in deriving the correct discount rate to apply to a companies’ future earnings. Good G can produce lower discount rates through higher survival rates.

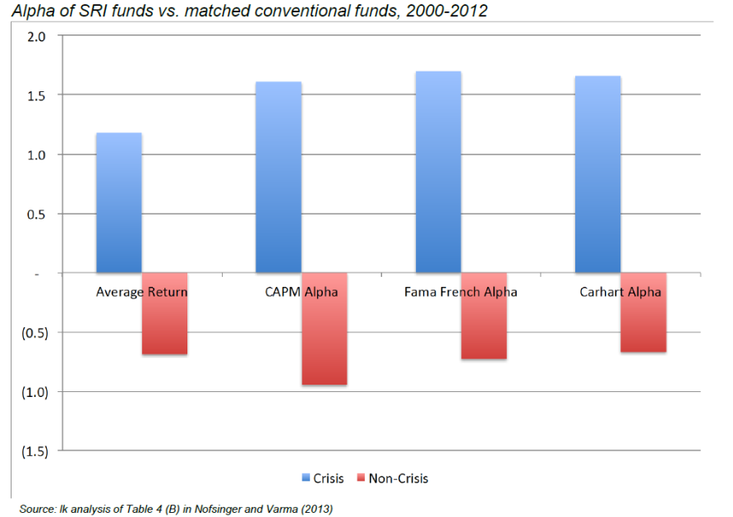

Below is some analysis of the performance of high G companies in a crisis. Think of it as built in downside protection to favour high G companies.

Sector membership matters too. It is always surprising to ask investors how long they think the average company lasts. It is not forever. Many companies fail and will continue to fail. Go back and watch any sporting event from 40 years ago. How many of the companies on the advertising billboards are still around today?

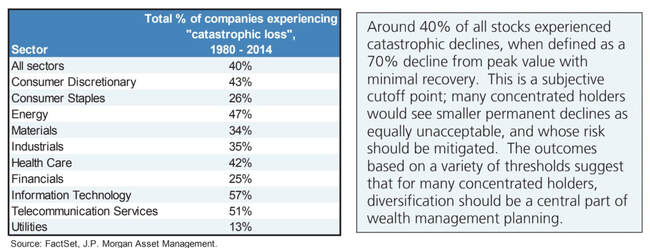

What really hurts compounding of returns is a catastrophic loss of capital; it only takes a few stocks to seriously fall for the poorly designed portfolio to suffer serious damage. So how to avoid this risk? Check out the table below:

Companies meeting these criteria are priced and behave as “index linked corporate bonds”. In this regard they are unique. They provide a decent yield compared to the pitifully low or even negative rate on ‘safe’ government bonds and the current yield on index linked bonds which of course is negative; AND they offer a measure of hedge against inflation since equities are a claim on nominal growth which conventional bonds are not. Index Linked bonds do provide a hedge against inflation but with negative yields, they are expensive. Buying an index linked bond with a negative yield of 1.5% and not a utility company with a dividend yield of 4% is giving up annually, a 5.5% return.

Equities we own in this space include AES Corporation (AES.NYSE), Quanta Services (PWR.NYSE), Johnson Controls (JCI.NYSE), OneOK (OKE.NYSE), Enbridge (ENB.TSE), Terna (TRN.BIT), ENEL (ENEL.BIT), Rubis (RUI.EPA), General Mills (GIS.NYSE), Iron Mountain (IRM.NYSE), ENN Energy (2688.HKG), Verizon (VZ.NYSE).

We view this as getting a yield in line with corporate bonds, AND the index linking of an inflation proof bond. These companies will have a greater chance of survival in the long run if history is a guide. The chances of a policy mis-step are now high so this is the time to be thinking about survivor strategies.

Currently therefore we are overweight Utilities, Infrastructure and Industrials. Given their superior survival characteristics, their lower P/E multiples and higher dividend yields they look attractive, Add in the likely buying frenzy to be unleashed as other investors scramble to get behind the newly discovered infrastructure spending plans in the USA and Europe, the best place to have risk would appear to be in these companies rather than the now very vulnerable to regulation, non tax paying, non-voting share class issuing, expensive stocks of yesteryear.

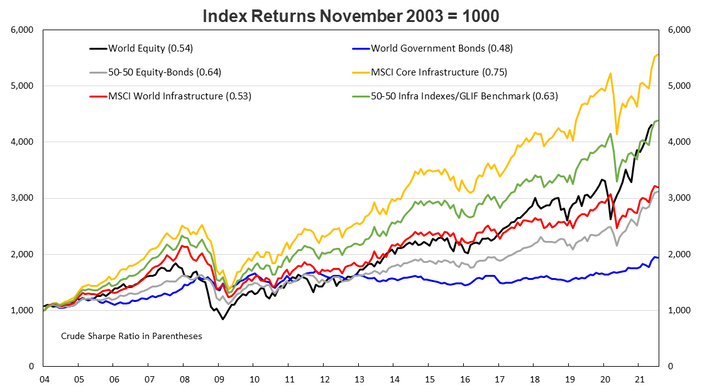

Lastly here is a slide of returns over the last 18 years accruing to equities, government bonds, infrastructure equities and blends of each. Even during this period of ‘growth’ equity excitement, one didn’t lose out too much by having exposure to defensive stocks in sectors with high chances of surviving a shock.

The great thing about the stock market is that complacency, one trick ponies, and luck, get found out over time. Betting on price momentum with an absence of thoughtful rigorous analysis on valuations, risks, and portfolio construction tools and without any knowledge of long term history, is a disaster waiting to happen.

Robert Swift manages TAMIM’s Global High Conviction portfolio. A portfolio of global equities from major developed global exchanges, it holds 50-80 of the best ideas from Robert and his team. The portfolio uses a systematic and consistent approach to stock selection and portfolio construction to deliver strong risk adjusted returns while focusing on attempting to preserve the wealth of our clients.

Today we are writing about the fast growing sports betting industry emerging in America and a mid cap that is well positioned to benefit. PointsBet (PBH.ASX), one of 2020’s hottest stocks, is an online bookmaker offering sports betting services in Australia while also launching operations in the sport betting market in America. They currently have market access to fourteen US states and are looking to capitalise as an early mover in the new online gambling market in the US. Ever heard the saying “the house always wins”? PointsBet might be the opportunity for investors to win from gambling without the “house cut”.

Author: Adam Wolf

US Sports Betting Market

In 2018 the US Supreme Court passed a judgement that effectively ended the federal ban on sports betting. Since then, twenty states have legalised online sports wagering and 80% of states have either legalised sports betting or introduced legislation to do so. The legal sports betting market presents a rather compelling opportunity for participants, with the total addressable market at maturity predicted to be in the vicinity of $53bn USD. By legalising sports betting state governments can benefit from the enormous taxation revenue gambling brings. Given the large budget deficits governments have amassed as a result of the Covid-19 response and relief, this is something that may be rather appealing. Legal sports betting will also deter people from illegal gambling which cannot be taxed or regulated, a major benefit for state governments and we expect to see most states legalise some form of sports betting in the next few years. The main players in the industry include DraftKings, FanDuel and BetMGM, PointsBet are looking to capture a small piece of a very big pie by achieving a 10% market share in the states they operate in.

Key Financial Metrics

Market Cap: ~$2.2bn AUD Cash and cash equivalents as of March 31: $328m Q3FY Revenue: $65m (up 246% QoQ)

Source: PBH company filings

NBC Partnership

In 2020, PointsBet announced a 5-year deal with NBC worth over $500m AUD. NBC are one of the biggest broadcasters in America and have over 180m viewers, they also hold the largest sports audience in the US. This deal provides PointsBet with a spectacular runway to execute their strategy and scale their platform in the US. NBC were also issued a 5% stake in PointsBet and hold options for a further 66m shares; they are well incentivised to ensure PointsBet becomes a dominant player in the market.

iGaming Opportunity

PointsBet have developed their own igaming platform inhouse. They recently launched their inaugural igaming product in Michigan, which will offer customers access to online casino games. They expect to launch igaming in New Jersey later this year. JP Morgan sees the igaming industry eclipsing $4.6bn USD by 2025.

Banach Acquisition

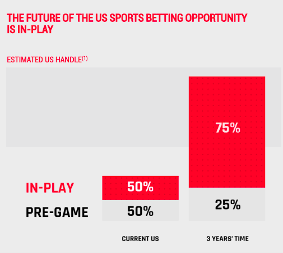

In April, PointsBet announced the acquisition of Banach Technology, funded through cash and script consideration worth $43m USD. Banach is a leading provider of ingame betting products across multiple sports, allowing customers to place ingame wagers. The acquisition will increase PointsBet’s product offerings and contribute to a higher gross margin. The real strategic value in this acquisition is that Banach currently provides services to some of PointsBet’s biggest competitors. PointsBet will honour the contracts and then cease to provide these services, keeping the IP for their own platform. This will put PointsBet’s ingame offerings ahead of their competitors and will force competitors to build their own models. Within three years PointsBet sees in-play betting representing 75% of all wagers, up from the current 50%. Banach is also part of PointsBet’s focus on building a strong inhouse tech stack. This is proving to be important as PointsBet management highlighted that they were one of the few operators not to have technical issues during the Super Bowl.

With a cashed up balance sheet and no debt, we expect to see more acquisitions that are accretive to PointsBet’s growth in the US market. Most recently, PointsBet acquired Premier Turf Club to strengthen their foothold in the US racing market. This is a timely acquisition given that New Jersey are in the process of legalising fixed odd betting on horse racing.

Source: PBH website

Upcoming Legislation:

Canada

On April 22nd the Canadian House of Commons passed bill C-218, the ‘Safe and Regulated Sports Betting Act’. Now sitting with the Senate, there are still some final hurdles to get through before the parliamentary session ends on June 25th but it is looking like Canada has seen the revenue potential like their southern neighbours and are heading in the same direction in terms of legalisation. This would provide PointsBet with another huge addressable market to enter and it would appear that they have every intention of doing so. PBH hinted at the Canadian sport betting opportunity in their half year results presentation. PointsBet are well positioned to enter the Canadian gaming market after announcing a multiyear deal with the NHL as their official sports betting partner. Canadians love their hockey and PointsBet will have its name all over the upcoming hockey season.

(26 May 2021 Note: Bill C-218 made further progress in Tuesday’s Senate meeting, it was adopted at the second reading and was sent to the Committee of Banking, Trade and Commerce which will convene in the coming days.)

New York

Source: PBH Advertising | PointsBet have taken to partnering with legendary sports names like Allen Iverson (pictured) and, more recently, Shaquille O’Neal

We recently saw New York legalise sports betting. As one of the largest population centres in the country, this is obviously a stupendous opportunity for operators. Unfortunately, New York will only award licenses to a few operators and will tax them at 51% of their revenues. PointsBet will most likely not receive a license even though they do have a second skin agreement with a tribal casino in NY. Given the expenses involved and the heavy taxation, it’s not the end of the world if PointsBet doesn’t get immediate access to the New York market. We see New York issuing more licenses in the near future as they will face functionality issues with a lack of competition in their market.

Arizona

Arizona legalised sports betting in April and will issue up to twenty licenses through tribal casinos and sports teams. PointsBet should announce a partnership with one of the casinos for market access and they may even look to partner up with one of Arizona’s sports teams, as they have done with the Detroit Tigers. Arizona will be a big opportunity for PointsBet if they get market access as all participants will be starting from scratch. Arizona is one of the few states that hasn’t legalised daily fantasy sports. That is to say that Draft Kings and FanDuel will have no existing databases to work off, giving PointsBet a good opportunity to achieve more than their targeted 10% market share.

Florida

Florida have made huge progress towards legalising sports betting after reaching a deal with the Seminole tribe that would earn the state government annual payments of $500m USD. The Seminole tribe will continue to control the state’s gambling activities and details about how many operators will be participating are still unknown. There are some final hurdles to get through. Florida will be the largest state (by population) to legalise sports betting and a license to operate would be a huge addition to any bookmaker looking to capture a share of the overall US market.

Louisiana

Louisiana lawmakers moved forward on a bill to legalise both in-person and online sports betting, the session ends on May 31st but it is beginning to look likely that they will pass the bill before then. PointsBet have already secured market access in Louisiana and the hope is that first bets will be taken before the end of the upcoming football season.

Thesis

The past few weeks have been rough for all gaming stocks, including PointsBet, with PBH down 36% over the past three months. We believe PBH is starting to look like a compelling proposition at its current market cap of ~$2.2bn. PointsBet are establishing a position in a huge market that will only increase in size as more states pass legislation to legalise sports betting. It is also pleasing to see that they are building a strong suite of their own in-house technology, bolstered by their Banach acquisition mentioned above.

On the back of their partnership with NBC they have access to 180m viewers and we would back them to achieve at least a 10% position in the states they operate. In their latest quarterly, management said they are aiming to be operational in eighteen states by the end of next year which, three times the amount of the states they currently operate in.

Source: Illinois Gaming Control Board

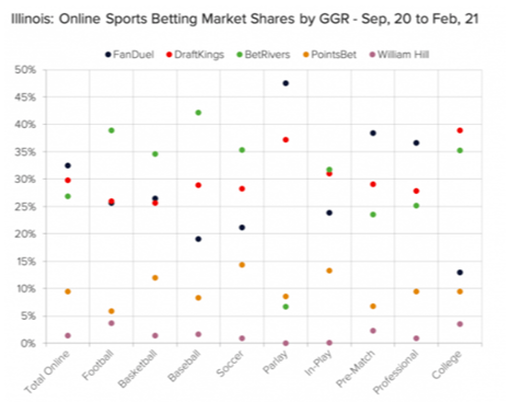

Illinois’ wagering handle in March revealed that PBH had achieved a 8.3% marketshare and the recent cessation of online signups in Illinois will work in Pointsbet’s favour as they have the closest registration site to Chicago.

Source: PBH company filings

There are a variety of catalysts coming into play. Assuming they execute, the pending legislation in Canada, the expansion of PointsBet’s igaming product as well as new states in the US passing legislation should all provide decent tailwinds for PBH.

PointsBet’s biggest competitor, DraftKings, are currently sitting on a $22bn market cap, ~10x that of PBH. This valuation makes PointsBet look very cheap given their market access and partnership with NBC. You would think that PBH would look to list in America at some stage alongside their competitors – DraftKings (DKNG.NASDAQ), Penn National Gaming (PENN.NASDAQ), Caesers Entertainment (CZR.NASDAQ) – who are all worth many multiples more than PBH, a US listing could see a much more generous valuation.A theme we saw in the Australian sports betting market was the consolidation of sports betting providers as the market started to mature. M&A activity in the industry could also lead to a significant re-rate of PBH or potentially a takeover offer from a bigger player. The management team, lead by CEO Sam Swannell, have shown that they are more than competent at executing their US strategy and have provided early shareholders with enormous value since listing in 2019. They are the only Australian based sportsbook to be operating in the US market and have made plenty of key partnerships with sporting teams and organisations along the way. If PointsBet are able to execute their strategy in the US and Canada whilst remaining competitive in Australia, we can see them becoming one of the top tier sports betting companies with a market cap closer to the likes of DraftKings and Flutter Entertainment (FLTR.LON).

Disclaimer: PBH was previously owned in TAMIM portfolios but is not currently held. The author of this piece maintains an exposure to the stock having first bought at approximately $3.50 in April 2020. Price target: $20+ Spetember 2022.

This week we take a quick look at three companies that should benefit from borders reopening and the resumption of travel around the world. Typically, investors consider the Flight Centres (FLT.ASX) and Webjets (WEB.ASX) of this world when thinking of travel beneficiaries, but in this case we are examining a few tech-based businesses that, perhaps more indirectly, we believe will benefit.

Authors: Ron Shamgar

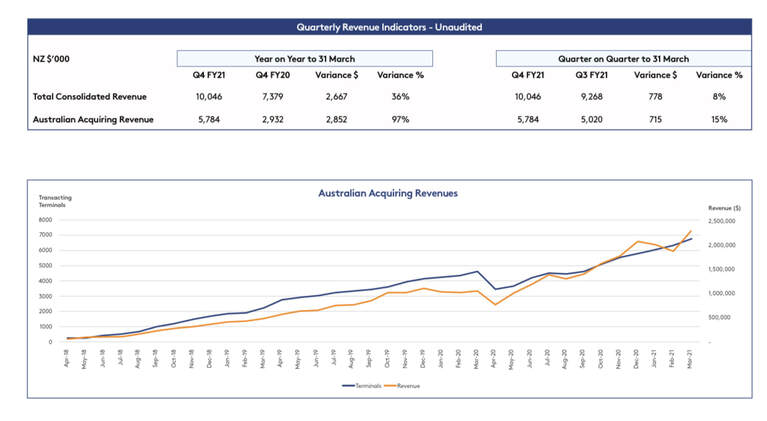

Smartpay (SMP.ASX) provides merchant terminals to small businesses in Australia and New Zealand. Their recent quarterly update in April showed growth continuing with 1,000+ new terminals added to their Australian base for the quarter. SMP is currently annualising $28m of revenues in Australia alone. In NZ, SMP generates $18m from terminal rentals and has about 25% share of the terminal market.

Source: SMP company filings

As travel resumes between NZ and Australia (and eventually other countries), we see retail spending for smaller merchants like convenience stores, cafes etc. increasing. A development which should benefit SMP. Prior to Covid, the NZ business received a $70m offer from Verifone and we believe another offer may emerge this year. Regardless, there are 1m terminals in Australia which provides a long runway for growth. We value SMP at $1.30.

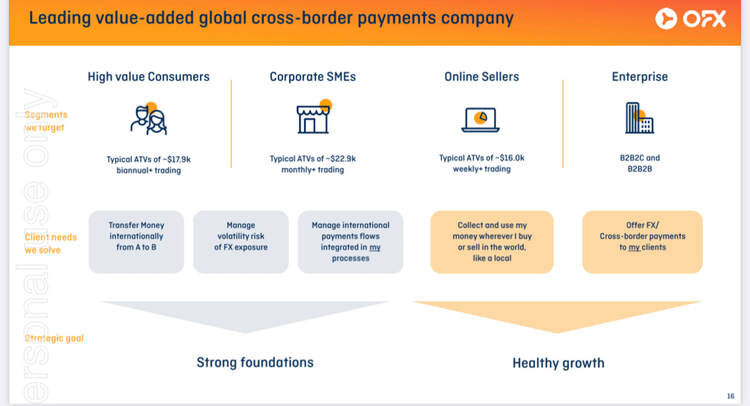

OFX Group (OFX.ASX) is an international payments platform that allows consumers and businesses to make payments and exchange currency around the world. Half of the business is in Australia, which competes against the major banks, while the rest of the business is focused on the US and European markets. OFX processes $25bn in transactions per year and will generate $130m of revenue and $35m EBITDA this year (March 2021 year-end).

Source: OFX company filings

Apart from trading at an attractive valuation of 9x EV/Ebitda, OFX will benefit from consumer demand to exchange money for travel and the emergence of online sellers on global marketplaces, like Amazon and eBay, that require currency exchange when they buy and sell their products. As 2H earnings accelerate, we think the market will react positively to OFX’s year-end result at the end of May. Our valuation is currently $1.60+.

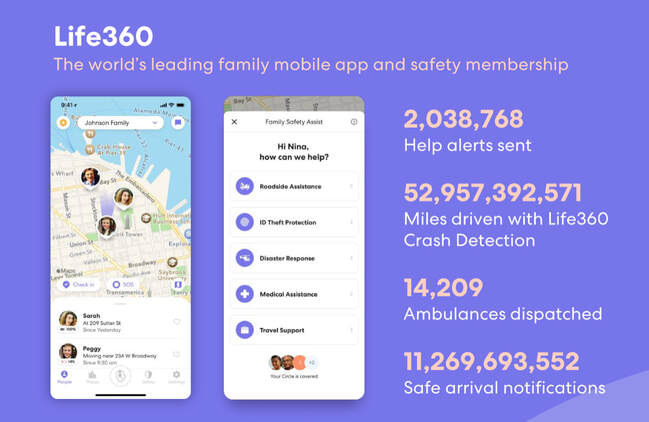

Life360 (360.ASX) is a US based technology business that provides an app, primarily for families, that allows them to locate each other, drive safely and call for help in case of an emergency. They currently have over 28m users globally and are on track for USD $110-$120m of revenues in CY2021. The company is trying to bolster its ability to monetise their member base with premium plans and we think the reopening of borders and easing of restrictions around the world, whenever that may be, will accelerate user growth.

Source: 360 company filings

Life360 is also targeting further acquisitions and a US listing, possibly through a SPAC vehicle, later this year. We view this development, if and when it eventuates, as a significant catalyst for their share price on the upside.

Disclaimer: All three stocks are held in TAMIM portfolios.

Once again, Sid Ruttala continues his journey through the ASX20. This week his notes visit and review Woolworths Group (WOW.ASX) and Macquarie Group (MQG.ASX).

Author: Sid Ruttala

If you have missed some of the earlier parts to Sid Ruttala’s latest Talking Top Twenty, you can find them here:

WOW continues to please with its recent announcement of the demerger of Endeavour Group. Shareholders are set to receive about a 70.8% share of the company with WOW and Bruce Matheson holding 14.6% each. For the yield starved investor, the new company is set to have a payout ratio of approximately 70-75% of NPAT.

Numbers wise, group sales were reported at $16.56bn AUD. More pleasingly, online sales growth continued its upward momentum with Q1 sales up 90.5% vs. the 69% reported in my notes six months ago. This is one area that remains a key metric for management given its omnichannel strategy. The big headache seems to be the NZ business, contracting -7.5%, with a -6.9% for transaction growth. However, even here online penetration continued to grow at 37.9%. What surprised on the upside however was the performance of Big W, seeing sales growth of 20%.

Overall, management continues to deliver on its outlined strategy and we remain convinced that it has a better investment thesis/case than Coles.

Woolworths is the anchor tenant in the TAMIM Property Fund: Fairfield Heights

Red Flags & Risks: Management continues to be disciplined when it comes to cost management and balance sheet discipline. The big question mark when we last undertook this exercise was the uncertainty around the divestment of Endeavour. Pleasingly, this has now been resolved. Big W continues to surprise on the upside though we remain of the view that it may be better off sold than remaining a part of the broader group.

In addition, last-delivery remains an issue for the business with much being reliant on management turning existing stores into effective distribution centres (DCs).

My Expectations: In the right context, WOW remains a buy with management continuing to execute on its strategy. Their footprint across regional areas gives them a competitive advantage in comparison to pure-play online retailers. The company’s demerger of Endeavour is, in my view, a good move.

Dividend Yield: The current yield stands at 2.6%, assuming a share price of $43.50 AUD.

We remain convinced that this will stay at $1 AUD per share (give or take 0.2c) for the foreseeable future as the business continues to reinvest in order to keep up with competition and margin pressure.

Macquarie Group (MQG.ASX)

Macquarie continues to deliver with NPAT up 10% to $3.015bn and CET1 ratio of 12.6%, it remains well capitalised with a stellar balance sheet. Nevertheless, guidance from management suggests that FY22 is likely to be flat. Division wise, MAM (i.e. Asset Management) continued to deliver stellar performance fees of $660m AUD. While this was down from the previous year, to the tune of 20%, it was certainly better than expected. The decrease in AUM (Assets Under Management) was slightly concerning; this was probably a result of a strong AUD and the reduction in contractual insurance assets though.

Of particular interest, CGM (Commodities & Global Markets) continued to deliver with operating income increasing by 22% to $4.7bn AUD. BFS (Banking and Financial Services) remained broadly flat however. Again, a strong AUD remains a problem for the institution, given that 69% of their revenues are derived globally, as mentioned in my notes six months ago. A 5% swing in the spot rate will result in a 3.5% swing in the NPAT (either way).

Red Flags & Risks: The big risk for Macquarie is the headwinds faced via a bullish AUD, with AUM remaining a key concern. There continues to be downward pressure on EPS with the need for management to be diligent in increasing AUM going forward. Would also have liked to see more clarity around the strategy for increasing FUM on the MacWrap platform.

My Expectations: Remains a fair substitute for the Big Four with a well-diversified business and is arguably a greater risk-reward proposition. However, at a $149.540 AUD share price at the time of writing, it remains fairly valued.

Dividend Yield: The current dividend yield stands at an exceptional 3.15%, assuming a price of $149.540 AUD.

As long-term investors in Taiwan we prefer to look at the investment flows by Taiwanese companies into China as an indicator of the state of relations and not media speculation regarding the prospect for military hostilities. If China were going to invade Taiwan it would have happened years ago. The financial relationship between China and Taiwan is strong and growing. It is that financial relationship which will ultimately guide China and Taiwan to a sensible compromise regarding political differences.

Taiwan has been in the news a lot recently, especially with media headlines highlighting the apparent threat of invasion by China. In Australia we have seen this being used as a justification for increased military budgets in part to support the defence of Taiwan. We have been investing in the market in Taiwan since it opened to international investors in the early 1990s. Taiwan has some world class companies and was recently awarded four of the top one hundred places in the survey of global innovation published by Clarivate, not bad for a small island population of 23.5m people. We expect to continue to invest in world class companies that are headquartered in Taiwan and prefer to focus on the flow of investment money that takes place between Taiwan and China rather than speculation about imminent invasion.

April was a month of very mixed performance in the Asian region, by far the strongest market was Taiwan where the small to mid-sized stocks increased by 13.1% bringing the return over one year +75.8%. The broader measure of market performance in Taiwan for large capitalisation stocks increased by 7.7% during the month of April and +82.3% over one year. This was despite “The Economist” announcing Taiwan as the most dangerous place on Earth. “The Economist” was highlighting risks of military action by China to seize control of Taiwan. While China has been increasing incursions into Taiwan’s airspace, their way of testing responses, this is not anything new, China has a long history of this behaviour and we do not see this as the move towards an invasion of Taiwan.

In recent months we have seen China objecting to the United States Navy movements through the Taiwan Straits. In February there was tension between China and the United States when the destroyer USS Curtis Wilbur sailed through the Taiwan Strait, with China suggesting that the United States was undermining regional peace and stability. The United States sends their Navy vessels through the Taiwan Strait on a regular basis in a show of support for Taiwan, this however is a token show of support. The official United States policy of formal defence of Taiwan ended in 1979 when it ceased with recognition of the Republic of China as “China” and started referring to it as “Taiwan”. This change of status occurred when the United States recognised the People’s Republic of China as “China” and all relations with Taiwan then became informal.

Late in 2020 Beijing made an explicit warning that independence for Taiwan “means war”. China’s Taiwan problem dates back to 1949 when the Communist Party seized control of the Mainland and the displaced Kuomintang (KMT) government relocated to Taiwan. China has never renounced the use of force to take control of Taiwan, however, overt verbal threats of conflict are rare. The current ruling party in Taiwan, the DPP previously talked about “independence”, however, that word has been quietly removed from the narrative employed by the party. Relations with China tend to worsen when the DPP hold power and improve when the KMT hold power which is somewhat ironic given that the KMT were the original enemy of the Communist Party during the civil war that concluded in 1949. We can expect better progress towards a form of political accommodation between China and Taiwan the next time the KMT hold office in Taiwan.

A good deal of the recent tension regarding Taiwan can be attributed to the former US Administration under Donald Trump due to increased military equipment sales and US Navy activity through the Taiwan Strait. We expect the Biden Administration to adopt a lighter touch with respect to Taiwan. We have already seen Vice President Wang Qishan indicating to a delegation of US representatives that common interest outweighs differences with the United States. A period of relative stability with respect to trade and an end to the arbitrary Trump imposed tariffs will be taken very positively by markets.Taiwan’s President Tsai Ing-wen responded to “The Economist” headline assuring everyone that the government is fully capable of managing all potential risks and protecting Taiwan from danger. President Tsai went on the speak about responding prudently to regional developments and overcoming the challenges posed by authoritarian expansion in a reference to China without naming China. The equity market in Taiwan was much more interested in the news that the local economy grew by 8.16% in the first quarter, the fastest growth recorded in a decade and well above consensus expectations. The positive growth surprise was driven by stronger domestic manufacturing and demand for exports. Two of Taiwan’s major semiconductor manufacturers have recently announced large investment programmes aimed at alleviating the worldwide shortage of semiconductors needed in the automotive industry and consumer products. Taiwan is expected to achieve economic growth in excess of 5% for the full year of 2021.The table shows officially sanctioned investment that have taken place by Taiwanese companies investing in China. From the start of 1991 to the end of 2020 there have been 44,400 investments from Taiwan into China totalling USD 192.4 billion. By way of context, China received a total of USD 141 billion of foreign direct investment in 2019. Typically, “Hong Kong” appears as a major contributor to investment in China and this is usually money from Taiwan that has to be channelled via entities in Hong Kong. China’s official policy position is that Taiwan is a domestic province of China and therefore investment flows sourced from Taiwan should not be treated a foreign source of investment.

Source: Investment Commission, Ministry of Economic Affairste investment funds from Taiwan to China have slowed from the USD 14 billion annual peaks in 2010 and 2011, the figure in 2020 approached USD 6 billion and remains a substantial number. It is also important to note that the 2020 level showed a substantial uplift from the 2019 number which was a response to the then President Trump’s habit of surprise tariff restrictions being applied to China. For a while China was the predominant area of manufacturing investment by Taiwanese companies, the cost savings from manufacturing in China were too tempting to resist. The rising cost of labour in China and then Trump’s trade war prompted a sensible diversification of investments by the Taiwanese to ensure that China did not end up putting their supply chain at risk. The cost savings of manufacturing in China available a decade ago are much less pronounced in the current environment.

An example from our portfolio in Taiwan is Novatek Microelectronics, a leading fabless chip design company specializing in the design and development of a wide range of display driver integrated circuits required for sophisticated flat panel displays and audio/video applications for all digital devices. We originally acquired our position in Novatek at an average price of TWD 102 in late 2018, those shares recently reached the TWD 600 level. We have taken profits along the journey and remain a happy shareholder in a business that is attractively valued especially versus global peers. We acquired the position on a p/e ratio of 11x, since then profits have expanded from TWD 6 billion in 2018 to more than TWD 20 billion in the current year, putting the company on 14x p/e and a net yield in excess of 4%. Novatek has eight of their eleven global sales offices located in China, their relationship with China remains crucial to the prospects of the business. Novatek opened their first office in China ten years ago. Going forward, the company expects to achieve significant growth in Japan and South Korea in addition to ongoing development of sales in China. Novatek typically invests the equivalent of 14% of revenues on R&D, a significant and ongoing commitment to the intellectual capital of the business. In the field of display driver integrated circuits, Novatek has global market share of 20%, second only to Samsung at 30%.

In conclusion, as long-term investors in Taiwan we prefer to look at the investment flows by Taiwanese companies into China as an indicator of the state of relations and not media speculation regarding the prospect for military hostilities. If China were going to invade Taiwan it would have happened years ago. The financial relationship between China and Taiwan is strong and growing. It is that financial relationship which will ultimately guide China and Taiwan to a sensible compromise regarding political differences.