Speaking to prospective and actual clients everyday, we get a fair sense and understanding as to the pulse of the market. Throughout those conversations, there are often common themes and questions. Among these, first, should we continue to own equities? Second question, where to allocate in a world of continued low interest rates? Thirdly, we keep hearing about inflation, but what does this actually mean?

While we are unable to provide advice or answer these questions directly and individually, we are able to voice our general opinions and positions on the subjects in question. For us, we continue to stay fully invested from an equities perspective. This is with the understanding that there is, as with any given market context, always the possibility of a sell-off. In doing so we prefer to make use of prudent risk-mitigation strategies such as put-options over the index as opposed to trying to time the market. Why? Simple, we aren’t smart enough to predict exactly when or where the catalyst for the next sell-off may come from (far too many moving parts). Anyone that tells you they can? Run the other way. With that bit of context, let’s get to unpacking the questions listed in reverse order.

Inflation

Author: Sid Ruttala

For those that have read previous articles, you may be aware that I am somewhat of an inflationista. Despite rhetoric and the consistent management of inflation expectations by central bankers across the planet pertaining to the transitory nature of current trends, we simply don’t buy it. This time it really may be different. This was never our base case historically, despite the doomsday predictions during the initial rounds of QE (Quantitative Easing), where commentators consistently mentioned that liquidity injections into the financial system would result in runaway inflation. This is, we feel, a rather basic misunderstanding of the process through which it takes place. Firstly, increasing bank reserves does not necessarily translate or correlate into credit growth in and of itself. In fact, one could argue that money was stuck within the commercial banking system and this was reflected through increased asset price inflation. Credit growth is what is required in bringing about inflation in the real economy, via the money multiplier effect. Instead we saw continued downward pressure on the cost of capital for businesses (reflected in margins) and the increased use of share buybacks, especially in the US, which translated into massive EPS (or earnings per share growth).

Secondly, the labor arbitrage in the form of China and the ever downward pressure on real wages as a result, combined with technological innovation, saw a perfect deflationary scenario. Something that Japan and the EU continued to grapple with until quite recently. So, what about this time is different?

What Covid brought to the forefront, we argue, is the fragility of supply chains globally. Just-In-Time inventory systems and interconnectedness that were at the heart of historic earnings and equities growth. Yes, it is true that these supply bottlenecks, as indicated by the increased shipping rates and border closures, are transitory. What is not is the increasing role that governments are playing in re-calibrating supply chains which will put increasing cost pressures on companies which will inevitably be passed on to consumers. Secondly, the labour dynamic. Labour and wages continue to be the biggest driver of inflation to this day. Historically, since the 80s, monetary policy makers have been reluctant to see what is termed in economics as secondary round inflation. That is, the increased cost of living leading to wage earners demanding higher salaries which then causes another round of inflation in a somewhat self-perpetuating manner. It is rather telling that even the RBA Governor constantly talks about wage growth (not full employment) when coming up with his reasoning for the cash rate policy. Similarly, the appointment of Janet Yellen, a labour economist, as Treasury Secretary in the US is another sign of the priorities of policy makers. There is the second point, we will likely see an increase in labour’s share of GDP in the real economy (again, inflationary). Combine this with falls in immigration and more generous social benefits which enable workers to be more discerning and increases bargaining power. This brings us to the first point to watch out for as investors, don’t just look at the headline employment data but rather the transition time in short-term unemployment. This is a good indicator of the actual nature of unemployment. Workers being incentivised to stay out of the workforce for longer because of better bargaining power is inflationary. This is perhaps the reason why we continue to hear about labour shortages in the US, for example, despite official unemployment figures staying above 5%.

Returning to the China question, we believe the Evergrande crisis may in fact be a catalyst for a rethink of policy making. The controlled exchange rates which saw the PBOC hoard a phenomenal amount of foreign currency and debt on its balance sheet may be in its final stages. The nation is the only outlier in terms of broad money growth, only annualising 8% (compare this to developed economies such as the US and Australia which remain in the higher double digits). The reason we raise this is that having pegged or managed currency limits the monetary authorities in their policy making. Currently, the RMB is allowed to operate within a band that is deemed acceptable. However, in order to do this, it is disproportionately impacted by outside influences in its policy decisions. Should this happen, there will be a short-term deflationary shock as the RMB is likely to fall on a relative basis, providing a short term boost to exports and foreign investment. But longer term, given the policy impetus, we see this aspect to be rather transitory. This aspect is perhaps the other reason for Beijing’s confrontational tone as it pertains to cryptocurrency (they more than most cannot afford an alternative to the home currency).

So, point number one, inflation is coming. Not runaway as many of the readership may currently believe, like the 70s but a secular trend. Our call is that it will continue to average around 4% for the foreseeable future. The reason we don’t say runaway is, one, that it is very likely that measurements will be changed (important as this is what markets use in any case) and, two, the aging demographic and associated excess liquidity will put a dent. Think about when the period of greatest expenditure often is in a person’s life, usually in their mid-30s and when starting a family.

So, where do we allocate?

Allocation

Before going any further, consider this fact. The current portion of the US Federal Budget that services outstanding debt stands at 7.8% as of 2021, the numbers are similar in Australia. This is with the Fed Funds rate at 0.75 – 1% (expected between now and 2023) and the RBA cash rate at 0.10%. The question then becomes what would happen to this number should rates go back to 2007 pre-GFC levels of around 5%? This would imply that close to half of these respective government budgets would be allocated just to servicing the debt without any new expenditure. So we feel certain of one thing, we will not see a “normalisation” of monetary policy for the foreseeable future. What does this mean for you? First, the implication will be that the secular run in the bond-bull market is over, with real yields quickly going negative (they arguably already are). The only way out of this pickle, returning to the inflation thesis, is that inflation will be allowed to go above the official target rates (all things equal) and inflation control will increasingly come in the form of regulatory intervention rather than through an “independent” central bank.

In real terms, this means that the nominal growth rates of company earnings will continue to outperform while the discount rate (which has always been, and will likely continue to be, the official rates) stays put. Now, this may theoretically imply infinite equities valuations but it is important for investors to be a little more discerning. That is, your growth in dividends or capital must be higher or at least on par with CPI.

For those still unconvinced, think about the centrality of asset prices to the modern day economy that was the direct result of the financialisation of everything.

At TAMIM we continue to invest the equities portfolios in real assets with fixed debt structures, industrials, M&A targets (there will be continued activity here) and infrastructure. A side note about the M&A aspect: many of you may be investors in Sydney Airport (SYD.ASX), there is a different angle you should consider when looking at potential and so-called conservative assets. Let’s use the example of a utilities company with a dividend yield of 6%. For an institutional investor looking at fixed income substitute or similar replacement, happy with say a 3% annuity-like return stream, the equities investor would have also had significant capital growth. This could potentially be both lucrative and rewarding.

This brings us to the second point, the easy returns on the index have already been ascertained. It will pay to be a little more discerning in what you look at going forward. There are certain metrics that will matter more such as 1) pricing power; 2) ROA (Return on Assets); 3) Debt (in particular composition of said debt, for example, a large proportion in long duration and fixed can act as an effective transfer of wealth from the debt holders to the equity holders); and 4) Government or regulatory intervention, for example, recalibrating or reshoring supply chains also has the effect of protecting companies from competition. Finally, chasing M&A activity could be especially rewarding.

Finally, should we continue to own equities?

The answer is a resounding yes. Are valuations beyond historic norms? Yes. Will we see sell-offs? Yes. But where else can one allocate? Cash? We argued that we do not see a normalisation of monetary policy, your purchasing power is eroding by the day. On a side-note, looking Stateside, the recent news has been the Treasury asking banks to disclose a greater amount of detail on customer transactions (i.e. to the IRS). This is a sign of where the wind is blowing. We would rather own good businesses that generate cash flow and maintain our purchasing power as opposed to what is effectively an unfunded state liability.

This week we will be writing about a small cap education stock that has undergone a huge structural change as a result of a major partnership that is transformative to the business. We believe the market isn’t giving due credit for the magnitude of this partnership and the stock is presenting as a compelling opportunity for investors.

Janison Education (JAN.ASX)

Janison is a global leader in digital exam assessments. They are an EdTech company operating in a sector that has grown significantly as a result of the shift towards digitised learning, a shift accelerated further by covid-19. Janison provides online assessment and exam management solutions for global corporations, governments and education bodies.

Authors: Ron Shamgar

Janison specialises in high-stakes, high-volume digital assessment platforms for which there are few competitors able to offer comparable levels of scale, reliability, and exam integrity with demonstrated success with governments and esteemed education institutions.

Janison provides services to some of the biggest examination bodies in Australia and worldwide. Some of their key customers include the National Assessment Program (Naplan), a series of exams I’m sure at least some of ours readers are familiar with, while they also deliver ICAS Assessments, a suite of school tests, and most recently Janison entered into an exclusive partnership with the Organisation for Economic Co-operation and Development (OECD) to deliver its Programme for International Student Assessment PISA for Schools test. We will return to this later.

Source: Company filings

EdTech

Spending on EdTech and digital expenditure is expected to grow by 2.5 x between 2019 and 2025, reaching a total market size of $550bn. As a result of covid-19, the estimated market size for EdTech has expanded by a further $85bn in the past year. The short-term increase in spending through COVID is expected to remain in the long term as education departments uplift infrastructure capability to provide the devices and networking standards required for digital adoption. Schools are more equipped than ever to adopt digital assessments now that teachers are more familiar with technology; schools are expanding the infrastructure necessary to deliver digital exams on a large scale. Janison’s digital assessment solutions address the changing needs of the educational sector, covid-19 has emphasised and validated the advantages of digitisation in education and Janison is well placed to execute its strategy in this market.

Source: Company filings

PISA for Schools

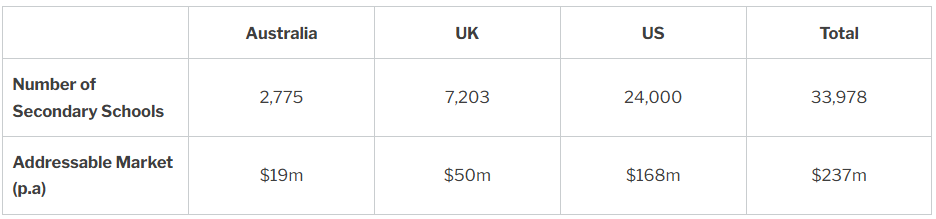

In May 2019 Janison announced that they had entered into an exclusive agreement with OECD to be the provider of PISA for Schools globally. PISA for Schools is providing educators with the best available evidence, drawn from the best available data sets to inform best practices in their schools. The PISA for Schools test will be powered by the Janison Insights platform which offers educators an enhanced dashboard and streamlined reporting structure alongside a suite of practical features enabling schools to explore their own data and compare their results to those of other schools and countries around the world. PISA is the gold standard in international assessments for global benchmarking. This deal will see Janison deliver the PISA for Schools to up to ninety countries (they currently are rolling out across fifteen) and gives them a huge addressable market to capitalise on.

PISA for Schools Revenue Model

Janison’s revenue model for providing the PISA for Schools test will depend on whether they are the National Service Provider (NSP) or the International Service provider (ISP) for the country in which they are rolling the platform out. As the national service provider, Janison will sign up schools themselves through sales representatives and will receive $7000 p.a. from each school they sign up. As an international service provider they will give the platform to a distributor who will then sell the testing platform to the schools, bringing in around $500 p.a. from each school. By rolling out the platform themselves and being the national service provider, Janison can see a much bigger profit margin. This is what they have been doing in major countries like Australia, UK and the US

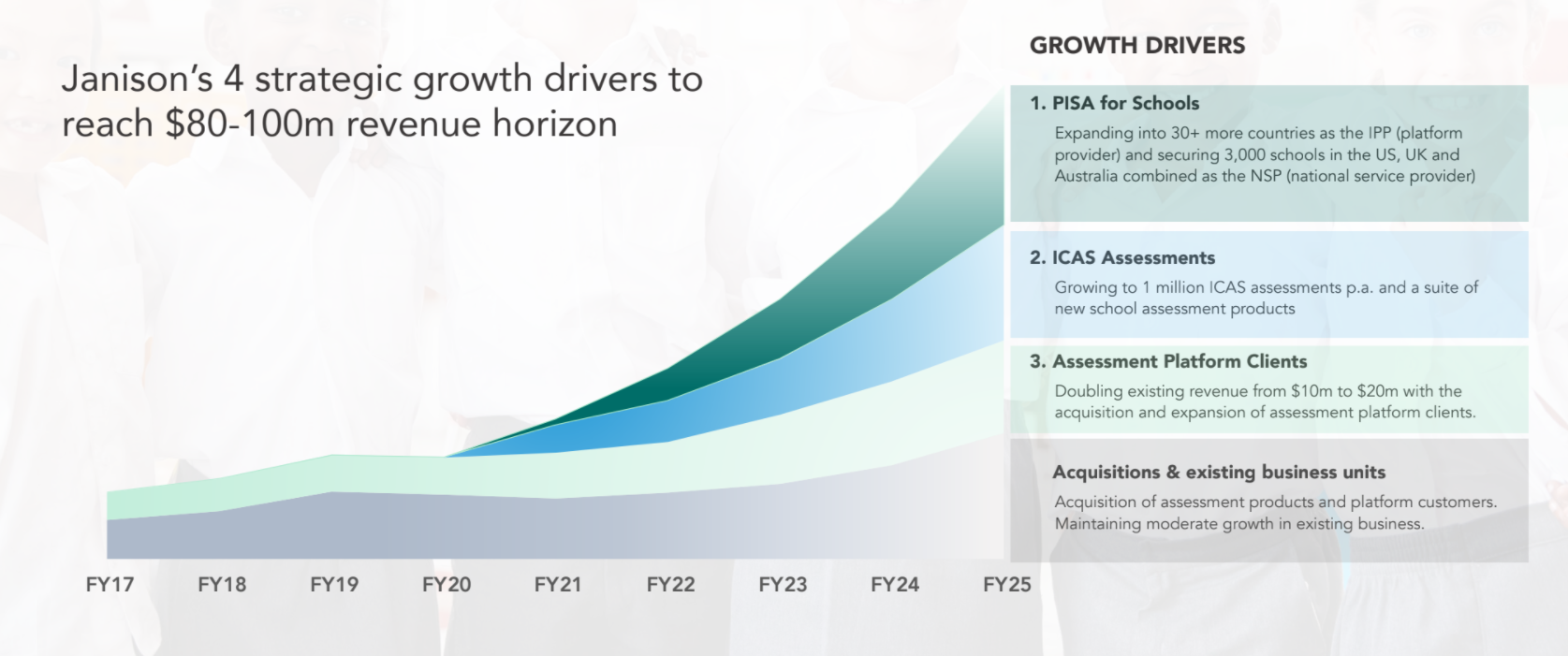

By becoming the NSP in the UK and the US, Janison’s addressable market is huge and it is all recurring revenue. The PISA partnership is transformative for Janison, management has projected that it will add approx. $30m of ARR. This is a conservative estimate given the size of the market.

Valuation + Outlook

Jansion is currently trading at an enterprise value of $200m, in FY21 Janison did $23m in ARR. As we have said many times before, we love businesses with good earnings visibility that have a recurring revenue model. The majority of Janison’s revenue is from providing assessments to schools through their partnerships with ICAS, PISA for Schools and others. PISA for Schools has provided Janison with a significant runway to scale their ARR. Janison’s cost base from rolling out the exams won’t increase a whole lot and, as they sign up news schools in the UK and US, their EBITDA margin will skyrocket.

Source: Company filings

Looking forward, Janison are in the process of rolling out PISA for Schools across fifteen countries, they are the NSP in six of them. We can see Janison exceeding $100m ARR by 2025, considering the growth in the EdTech sector and the incoming ICAS/PISA for Schools rollout (both of which are international exams that will provide significant scale for Janison).

Janison have also been active on the acquisitions front. They look for businesses with an existing customer base that will provide cross selling opportunities. This week Janison announced the acquisition of Quality Assessment Tasks. The rationale behind this deal is that QAT comes with a bank of past assessments and exam questions which have monetary value within Janison’s school assessment offering. It also introduces a network of over 250 highly skilled test writers and reviewers, supporting Janison’s strategy of developing and refreshing its digital library of assessments and items to the highest quality standards. Janison is in a net cash position of about $20m and no debt, they are well funded to continue M&A activities.

For an enterprise value of ~$200m, Janison is looking like a great proposition. We believe the market isn’t ascribing enough value to the potential upside of the PISA for Schools rollout; Australia, UK and the US are a $237m p.a. opportunity alone and that doesn’t include the eleven other countries in which PISA is being rolled out.

We estimate that Janison’s EBITDA margin will go to around 30-40% when they achieve their ARR of $80-100m, at those levels we see the valuation as multiples of the current market cap. In the short term, we value JAN at $1.60 or around 10x FY22 ARR.

Disclaimer: JAN is currently held in TAMIM portfolios.

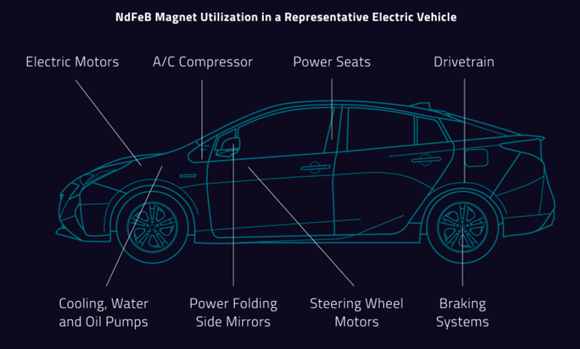

This week we are tackling the subject of rare earths, their applications for electric vehicles and how TAMIM’s Global Mobility strategy aims to benefit. The rare earth elements are composed of a group of seventeen metals that are each just as hard to pronounce as the next. They are becoming increasingly vital to a carbon free economy with applications for both electric vehicles and electrical efficiencies.

Author: Adam Wolf

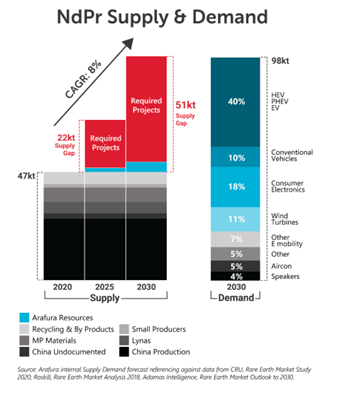

Right now, China is producing over 80% of the world’s rare earth supply. As a result of this, the US is pushing towards domestic production of these elements. Our holding, MP Materials, stands to benefit.

MP Materials (MP.NYSE)

MP Materials owns and operates Mountain Pass, the only integrated rare earth mining and processing site in North America. The Mountain Pass mine is in Nevada, a top tier mining jurisdiction. Mountain Pass is blessed with one of the world’s highest quality deposits of rare earths, allowing MP to be a global low-cost producer The Mountain Pass mine contains more than 800k tons of recoverable rare earth oxides with an average 8% ore grade, one of the highest quality (known) deposits in the world. Mountain Pass is designed as a zero-discharge facility, featuring a dry tailings process that allows recycling of ~95% of the water used in the milling and flotation circuit. The sustainable features of the mine are very favourable given the current ESG-driven environment when it comes to valuation.

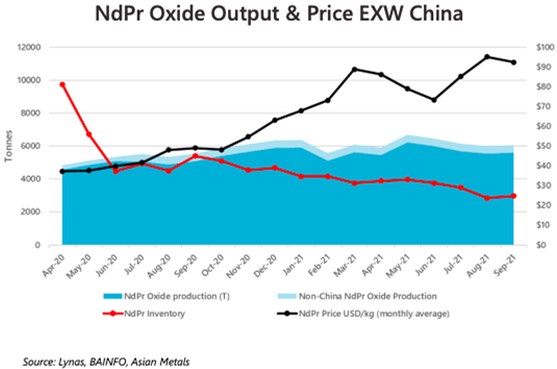

MP currently produces ~15% of the global supply of rare earths, currently in the form of an intermediate product — rare earth concentrate — that requires further processing in Asia. It currently sells its output to China-based, and 8% shareholder, Shenghe Resources for further processing but this is subject to change once MP implements their upcoming expansion strategies at the Mountain Pass mine. The company plans to reinvest the free cash flow generated from operations into expanding MP’s US capabilities, including restoration of domestic refining capability at Mountain Pass by next year. MP Materials will relaunch its onsite processing facilities, setting the foundation for a renewed, self-sufficient US rare earth industry. MP Materials shares have more than trebled since listing on the New York Stock Exchange in November 2020.

Rare Earth Elements

Rare earth elements are far more abundant than their name suggests but extracting, processing and refining the metals poses a range of technical, political and environmental issues. Most of the rare earth deposits are found along with radioactive materials that contribute to ecosystem disruption and release hazardous byproducts into the atmosphere. As a result, it is often difficult to receive the necessary environmental approvals to develop a rare earths mine. Environmental regulations are often more stringent than inside China which is why the country dominates the rare earth industry, producing over 80% of global supply as mentioned.

Having a single country, particularly one like China, dominating the supply of such critical elements poses a number of issues for the US. This is especially the case given the current geopolitical environment and the supply chain issues that are not only threatening inflation but also causing shortages in electronics and other industrial goods. President Biden signed an executive order requiring the US Government to review supply chains for critical minerals and other identified strategic materials, including rare earth elements, in an effort to ensure that the US is not reliant on other countries, i.e. China.

Electric Vehicles

With electric vehicles being one of the three pillars of our Global Mobility fund (along with autonomy and sharing/connectivity), we look for companies that will benefit from the imminent growth in electric vehicle production by participating in the ecosystem that is being built around the industry. While the US intends to shift away from China to source their rare earth supply, without domestic production this would have a significant effect on American consumers as domestic demand for batteries and electric vehicles ramps up. The pace of demand growth is expected to rise rapidly over the next few years as sales of electric vehicles are slated to reach 12.2m in 2025, according to data from IHS Markit.

Source: MP Materials company website

Rare earths are going to be a vital component in humanity’s shift towards cleaner energy. Not only will they be integral for electric vehicles but they are also used for things like wind turbines. Neodymium and dysprosium are the key components of the magnets used in modern wind turbines

” The wind turbine market is anticipated to account for ~30% of the global growth in the use of rare earth magnets from 2015-2025. Using rare earth metals prevents the use of gearbox. Rare earth magnets make the turbines lighter, cheaper, more reliable, easier to maintain and capable of generating electricity at lower wind speeds.”

– UBS Research, 23 July 2018

Stage II + III Strategy

As it currently stands, all of MP’s rare earth production requires further processing in Asia, something that the US is clearly anxious about. Following the acquisition of the Mountain Pass mine in 2017, the mine’s production is approximately 3.2x greater than the highest ever production in a twelve-month period by the former operator using the same capital equipment. That was the first stage of MP’s strategy. The second stage of MP’s Mountain Pass strategy will see MP Materials relaunch its onsite processing facilities, setting the foundation for a renewed and self-sufficient US rare earth industry. This would mean that MP Materials no longer has to send their product for further processing in Asia, they will now be able to sell their concentrate to end users which will have a huge cost-benefit. MP is aiming to finish their second stage in 2022. Stage III would be downstream integration, to be completed via either building a captive integrated magnet supply chain or investing in this capability via an acquisition, partnership or joint venture. The integration of magnet production would establish MP as the first and only fully-integrated source of supply for rare earth magnets in the Western Hemisphere. In addition to offering end-market magnet customers a complete Western supply chain solution, MP believe downstream integration would also create a material incremental value creation opportunity.

Outlook & Thesis

We see MP Materials as a company with multiple tailwinds moving forward. The shift toward a self-sustained supply chain in the US will obviously have a favourable outcome for US rare earths miners and provide further support for future projects. The demand side for rare earths is looking strong with electric vehicle production ramping up as well as other applications in things like electronics and wind turbines. Looking over at the supply side, due to the radioactive material that is usually found with rare earths, these mines are hard to bring into production so our outlook for the price of these elements is very strong. The completion of MP’s Stage II plans will be a major catalyst for the company, it will make them the only US company that can provide a rare earth end product to consumers. This will not only be cost-effective but will give them sizable leverage when negotiating off take agreements with US consumers.

MP are currently sitting on over US$1.1bn in cash, enabling them to execute their strategy at the Mountain Pass mine while also allowing them the opportunity to make further acquisitions or JV agreements, further increasing their production and presence in the future. In their last quarterly announcement, MP had an underlying EBITDA of 64%. Considering the cost benefits of their Stage II implementation and their increased bargaining power in terms of off take agreements, MP is sitting on a highly profitable mine. MP Materials is another company in TAMIM’s Global Mobility portfolio that will benefit from the shift towards decarbonisation through electric vehicles and clean energy applications. We see MP Materials dominating the rare earths industry in America and they will be the only US based company that has the ability to provide an end product to consumers without relying on Asia.

Disclaimer: MP Materials is currently held as a long position in TAMIM’s Global Mobility portfolio. The TAMIM Global Mobility strategy seeks to to capitalise on the ongoing $7 trillion autonomous and electric vehicle revolution.

This week we look at two stocks that are growing through strategic acquisition plans and are set to benefit from Australia’s imminent reopening and easing of restrictions. While they are both in very different industries, they have been performing well and we believe they are good companies to own heading into the reopening tailwinds.

The stocks in question are Healthia and People Infrastructure.

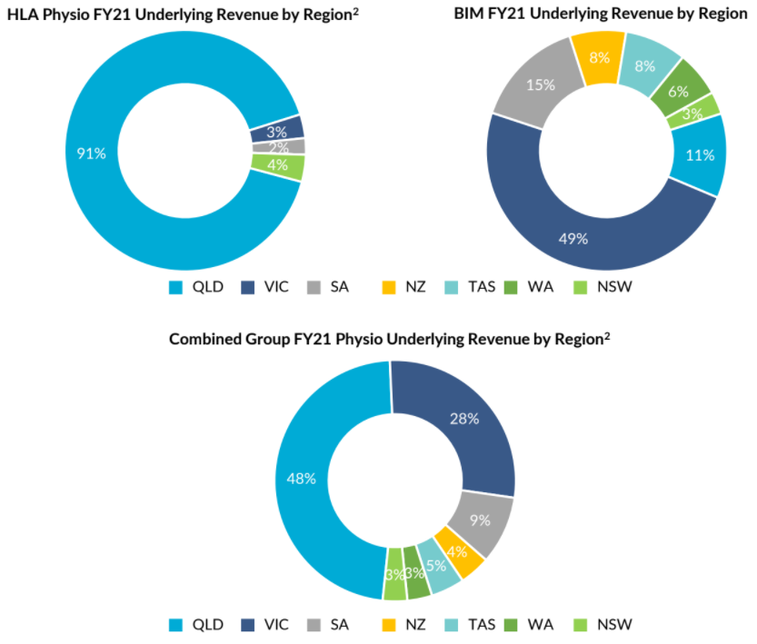

Healthia (HLA.ASX)

Healthia is an integrated allied healthcare organisation that includes networks of optometry, podiatry, and physiotherapy clinics across Australia. The physio/podiatry industry is a fragmented one that has allowed Healthia to grow through an aggressive acquisition strategy, giving them a strong presence throughout Australia. Following their most recent acquisition of Back in Motion (BIM), HLA is now positioned as the largest provider of physio services in Australia with 122 clinics.

Reopening Tailwind

Authors: Ron Shamgar

Most of Healthia’s clinics have remained essential services, which saw them continue operations throughout lockdowns. The lockdowns would’ve caused many people to delay visits to a lot of Healthia’s clinics; we can see there being a huge backlog of people waiting for restrictions to ease to go to one of Healthia’s broad range of health services.

Acquisitions

As mentioned, HLA has been undertaking an aggressive acquisition strategy to grow the business. They have been rolling up clinics throughout Australia which have all been earnings accretive. Their most recent acquisition of BIM, for a consideration of $88m, was a transformative one. Simply, it gave HLA a presence in new markets; BIM had a presence in New Zealand and Western Australia. BIM will add 64 clinics to the group and generated $12.3m of EBITDA, increasing the group EBITDA by approximately 57%. The acquisition is earnings accretive and was bought for circa 7x EV/EBITDA.

Source: HLA company filings

Healthia are typically paying in the range of 3-7x EBITDA for their acquisitions, which have been conducive to their growth strategy and enhancing value for shareholders. Bad acquisitions are an investor’s pet peeve and can destroy shareholder value if they don’t compliment the core business or are done at too high a price.

Valuation + Outlook

We recently saw 1300 Smiles, which ran a similar strategy to HLA except with dental clinics, get taken over by Abano Healthcare for approximately 15.5x EV/EBITDA. At below 8x EV/EBITDA, we see significant upside in HLA and the potential for multiple expansions on the back of their aggressive acquisition strategy. Heading into a post-covid world, we expect to see a backlog of people that will be booking appointments at HLA’s clinics. We like businesses like HLA that have good earnings visibility, their clinics typically have around 85% client retention and are pretty essential services. Buying a quality business like HLA on the back of a transformative acquisition at below 8x EV/EBITDA looks cheap heading into the country reopening.

We can see HLA trading at $3+.

People Infrastructure (PPE.ASX)

People Infrastructure Ltd is an outsourced recruitment management business dedicated to the growth of Australia’s infrastructure and construction sector. Services provided by the group include recruiting, on-boarding, contracting, rostering, timesheet management, payroll, and workplace health and safety management. The four main sectors PPE is targeting include healthcare, community services, industrial services and information technology. People Infrastructure has a track record of successfully acquiring and growing businesses through leveraging its core capabilities in the sourcing, skilling, deployment and management of workforces.

Source: PPE company filings, 2 June 2021

Reopening Tailwind

PPE was well placed heading into the lockdowns given the diversity of their clients, low client concentration and the critical nature of many of the services that their clients provide. While construction has mostly continued through lockdowns, it hasn’t been at full capacity and, as a result of labour shortages and lack of overseas workers, human capital is in high demand. When you combine these factors with easing restrictions, demand for PPE’s services could lift considerably. With healthcare making up a huge chunk of PPE’s EBITDA we can also see the pent up demand for elective surgeries being a huge driver of PPE’s business when restrictions ease. As well as this, there are huge fiscal stimulus plans in play where a lot of the money will go towards infrastructure development, another tailwind for PPE.

Acquisitions

PPE has a strong pipeline of acquisitions and is well funded to pursue them with $50-70m of available funding through debt and free cash; given their strong funding the strategy is non-dilutive to shareholders. Their past acquisitions have been earnings accretive and have expanded the industries PPE operates in. Their most recent acquisitions, Techforce Personnel and Vision Surveys, increased earnings per share by 19% and the combined deal was done on a valuation of circa 3.7x pro forma EBITDA. Their acquisition strategy opens up new regions for PPE to capitalise on and creates a much bigger addressable market for the group, as seen by their move into the healthcare recruitment space.

Source: PPE company filings, February 2021

Valuation + Outlook

PPE has been a consistent performer since listing in the backend of 2017; they beat their initial forecasts and have grown their earnings significantly. The company has strong cash flows and isn’t capital intensive. They are well funded to execute their acquisition strategy which, to date, has proven to be accretive to earnings growth.

Souce: PPE company filings

PPE is currently trading at an EV/EBITDA of 10x. The company has proven they can grow through their acquisition strategy and expand their services into new industries. Heading into a post-covid environment, PPE will gain from the current labour shortages and upcoming infrastructure spending. As mentioned above, the pent up demand for elective surgeries is huge and PPE is now a top two provider of healthcare recruitment in Australia, benefiting from the demand in healthcare workers due to covid-19.

Source: PPE company filings

We see PPE as a company that is not only cheap but also well placed to benefit as the country opens back up. Our valuation for PPE is $5.

Disclaimer: Both HLA and PPE are currently held in TAMIM portfolios.

This week we thought it may be pertinent to revisit our thesis around iron ore and in particular look at the big three players given the brutal nature of recent sell-offs of all three. Is it perhaps time to buy?

A Little Context

Author: Sid Ruttala

We’ve previously – late last year – made the bull case around the spot prices for iron ore (when the ore was trading at approx. 120 USD/T). Our reasoning here was summarised in a twofold explanation; 1) demand due to the likelihood of steel output staying consistent due to flooding in China; and 2) the increased fiscal expenditure globally, largely on infrastructure, which should see a disentanglement of the spot prices from Chinese demand.

Recent price action, however, suggested otherwise with spot prices tumbling from a peak of 228 USD/T in May to now trading at 117 USD/T (at the time of writing). So, what’s happened and why the decline?

The elephant in the room remains China. With China accounting for 70-75% of iron ore imports globally, any changes in demand have outsized impacts upon the global market. Beijing recently imposed caps on steel output as a result of and in the lead up to the 2022 Winter Olympics in the hopes of cutting emissions and controlling pollution. With domestic output having been allowed to expand beyond these caps through 1H21, we are likely to see continued declines until at least February of next year when the Winter Olympics are to be held. Combine this with some production coming back online in the form of Vale (Brazil), we have what may be considered a perfect storm.

Let’s now return to the second part of our argument; the disentanglement of spot prices from Chinese demand. Here we are seeing signs of reprieve. Take, for example, German import prices released by the Federal Statistics office, which saw the largest increases in import prices in close to forty years. Although this may be a result of supply bottlenecks, we are seeing increased demand for raw materials, with iron ore cost and end steel rising 95.8% in August, a period in which China’s imports of the product also hit peak. This indicates to us two things; first, Beijing may have coordinated a scenario where first half production was intentionally pushed above caps to taper off in the second half in the lead up to the Winter Olympics and, second, there is still surging global demand for the product on a longer term basis. This second aspect seems to be at play here. Major steel-producing provinces and regions are seeing inventory declines even during the offseason, with higher transaction volumes than would typically be the case in off-season markets this time of the year.

All this is to say that we are likely to see demand pick up with a vengeance coming out of the Winter Olympics and a rather messy situation in the lead up. This may be somewhat mitigated by shorter-term supply issues in the form of Vale, the most recent of which being 39 miners getting trapped in an underground mine at Totten. Nevertheless, we are still likely to see negative price action in 2H21 (or at the very least a consolidation pattern sideways) with 90 USD/T a great possibility.

Looking to the Longer-Term

Looking to the longer term, however, our thesis broadly remains intact. That is, the continued fiscal impetus globally should see a rather massive tailwind for raw materials and steel. The oft touted Green New Deal Stateside is, in our view, likely to gain momentum in some form despite the recent gridlock in Congress. The more liberal wing of the democratic party may get its way with the stimulus bill despite facing an uphill challenge in the Senate. Why do we say so?

The political imperative remains strong. Think for a moment about the voting patterns of the so-called Rust Belt and where US steel production is likely to take place should some semblance of the expansive infrastructure package be rolled out. These remain key and decisive swing states, Pennsylvania being one and Indiana, a key Republican stronghold and the largest producer of US steel, being another. All things equal, we are likely to see some incentive and political consensus especially when it comes to this aspect. What does this have to do with iron ore? Simple, we are likely to see further demand increases from the US.

Looking more globally, other key players continue to be the EU, where the marked shift to renewables is gaining traction for better or worse (most recently it has been in the news because of supply bottlenecks in traditional fossil fuels and an inability to cope with increased demand during winter). Nevertheless, we continue to see increasingly aggressive targets set by the Commission which formulated a directive to have 32% of energy consumption come from renewables by 2030. This came with a clause for upward revision in 2023 and carbon neutrality by 2050 (i.e. Renewable Energy Directive 2018/2001). Looking to emerging markets such as India where, notwithstanding recent cyclones that have buffeted steel producing states like Andhra Pradesh, we are seeing what could be termed as an infrastructure boom enabled by the government. Longer term, we see continued impetus on infrastructure spending, specifically transport infrastructure. We have seen the most recent union budget allocating close to $32bn US to the sector and new initiatives to wean the country off its reliance on diesel. Again, a focus on renewables also bodes well for the demand for iron ore. This remains a longer term play however, with ore imports still facing stiff competition and the steel industry being very much in its infancy.

So, buy now or wait it out?

For the purposes of this article, let’s limit ourselves to the big three, BHP, RIO and FMG. All three have seen incredible declines from peak to trough. -32% for BHP, -43% for FMG, -28% for RIO. We make the case that, given the above rationale, the market may have overdone it. But, even assuming a 90 USD/T base case, we would still extrapolate a return to investors of 25% for BHP at this price (inclusive of dividend yield and assuming continued payout ratios of 90%). This is within the context of the spin-off in the petroleum business, continued upward pressure in the other aspect of steel production, coking coal, and BHP’s recent move into potash which we estimate should give an internal rate of return of 15% over the next 5 years (this is above management guidance (12-14%) given where we see agricultural markets going, but that is an article in and of itself). So, BHP? Perhaps a good buy.

Let’s get to Rio which continued to sell off, perhaps not as aggressively as the other two but consistent nevertheless. We also found this to be a little overdone and the market seems to have misplaced or overlooked the fact that this particular business has some of the largest uranium mining operations in the world. Given our thesis around that particular commodity (which we wrote about last year), we think RIO presents as a solid buy at the current price of $96.89 AUD. This implies a dividend yield of 10.9%, however, let us strip out the recent price action in iron ore and in fact go with the lower bear case of 90 USD/T, assuming current payout ratios hold we would still expect a yield of 8%.

FMG, the pure play iron ore major, is another interesting story. Given the lower grades, it sits in the firing lines when it comes to any moves by Beijing to cut emissions. We do however contend that management has always had, and continues to have, good relations with the broader business community and has done a stellar job at managing its relations in that particular context. For those that have joined us in our line of thought around spot prices and the longer term potential, FMG offers a higher risk-reward play. At current prices, the implied dividend yield is a ridiculous 24%. Let us again use the lower for longer base case scenario of 90 USD/T. Assuming production stays consistent, we would still expect a grossed up dividend yield of approximately 11%.

So, basically, sell offs have been painful if you where an investor but all three present opportunities going forward in our view. BHP and RIO offer good value at current prices while FMG offers exceptional value if (and only if) you agree with our contention around the future of iron ore prices.

Disclaimer: BHP, FMG, RIO are currently not held in TAMIM portfolios.