This week we’re looking at a small cap retail stock that is offering investors a concentrated bet on the reopening theme. In 2020 we saw a huge shift in sentiment towards stocks that were benefiting from a covid-19 environment. Companies such as Pushpay (PPH.ASX) and Redbubble (RBL.ASX), we bought both heading into the pandemic, were huge beneficiaries. Heading into Christmas, the covid winners and now the covid losers and retail stocks are starting to grab more attention. With Australia exiting lockdowns there is a lot of pent up demand for retail spending, what we like to call revenge spending.

The stock in question is the specialist jewelry retailer Michael Hill.

Michael Hill (MHJ.ASX)

MHJ has slipped under the radar in the FY21 reporting season; they saw revenues increase 13% despite 10,447 lost store trading days as a result of Government mandated lockdowns and some permanent store closures. Their Canadian segment has done very well since reopening in June/July and we see the same happening in their Australian and New Zealand segments which are showing a lot of upside.

Source: Company filings

Digital Expansion

MHJ has been shifting the company toward a more digital footprint. Their digital sales increased by 53.4% and management expects to see digital sales accounting for north of 10% of total sales within the next few years. MHJ are also expanding through digital marketplaces, now offering their products through The Iconic, one of Australia’s largest digital marketplaces. We expect to see MHJ find similar partners in Canada and New Zealand.

Source: Company filings

Loyalty Program

Michael Hill launched their loyalty program, Brilliance, and within eighteen months memberships have already grown to over 800,000. The program is clearly resonating with customers and is aiming to deliver increased frequency, larger baskets, and higher margins. The program will provide MHJ with valuable data and insights which should help increase personalisation and enable the use of artificial intelligence to deliver further growth in the business.

Source: Compay filings

Valuation + Outlook

To value MHJ we are going to look at their assets and then their earnings power. After paying down debt, MHJ is now in a significant net cash position of $72m. To be conservative, and taking into account the required working capital for the business (i.e. cash for the registers), we will use a reduced net cash figure of $65m. MHJ recently conducted a strategic review of their Canadian in-house customer credit book. The asset is held for sale and is considered probable and expected to be completed within a year, the sale of the customer finance book should bring in around $13m. MHJ is also currently sitting on inventory of around $170m, if we add the $13m of assets held for sale then we get a net cash figure of $78m. This puts MHJ at an enterprise value of approximately $310m, giving MHJ an EV/EBIT of 4.3x. MHJ’s strong balance sheet gives us a huge margin of safety if things weren’t to go as expected, an important consideration we take into account in our investment process.

Authors: Ron Shamgar

Looking to MHJ’s earnings power, we see MHJ starting to pick up up tailwinds on the back of a great FY21 result. They recently gave an FY22 Q1 update which saw same store sales up 15.5%, up from the corresponding quarter last year. Margins continue to rise on the back of their digital expansion and their additional omni-channel offerings – including Ship-from-store, Click & Reserve and Virtual Selling – all of which are higher margin channels. MHJ lost over 10,000 total trading days in FY21 and, while they lost 7,400 days in the September quarter heading out of lockdowns and into the Christmas spending season in Australia and New Zealand, they should see a surge in spending for retail across the board which should drive MHJ’s sales. There is a lot of pent up demand for consumer spending and we have already seen how it positively affected sales in Canada upon reopening. Management recently noting that “our Canadian business has been flying, delivering impressive sales and margin growth every week.” The play here isn’t like most retail store strategies, which is typically to open up new stores and expand their physical presence. The strategy here is to increase digital sales through marketplaces like The Iconic, thus driving margins and opening up their products to new customers. MHJ has also done a terrific job at growing their loyalty program to over 800k members in less than eighteen months; this will be essential to leverage their digital capabilities.

If MHJ sees the demand that we expect upon reopening and heading into Christmas, they should see $50m+ NPAT for FY22 which will put them at less than 8x earnings. All while paying a cool 4.5% dividend yield. If MHJ were to rerate to 10x FY22 earnings then this would put them at a share price of around $1.30.

MHJ is one of our favourite stocks to take advantage of the reopening theme

Last week we looked at energy markets and made the case that the recent price action was a result of broader policy failures in speeding up the transition towards a net-zero world. This week we look at the green energy market to understand the incentives, opportunities and outcomes going forward. The irony may be that our bullish case for medium term oil prices may in fact perversely create a tailwind for the broader sector, despite what this may imply for growth prospects and inflation.

Author: Sid Ruttala

Before delving further, a disclaimer. We are by no stretch of the imagination experts on the actual technology required for the changes currently taking place. What we can do however is look at it through the lens of investors and to understand where the opportunities may arise and weed out the noise from reality.

A quick summary of the progress to date

The decade between 2011-2022 has been momentous for the renewables sector with annual net renewable additions to capacity (i.e. that is new capacity accounting for retiring older assets and accounting for depreciation) increasing from circa. 120 GW (gigawatts) to a record 280 GW in 2020, which saw a phenomenal 45% increase in capacity from the previous year despite Covid and the related headaches. 2022 looks set to continue building on these gains with current trends indicating that the sector (predominantly wind and solar) accounts for 90% of the increase in global capacity.

Off these overall numbers though, there are nevertheless some caveats. The growth over the last decade, despite the headlines that the EU and US continue to make, has primarily been a Chinese story with Vietnam being a surprise addition to the mix. China alone, for example, accounted for close to 80% of the increase in overall additions in CY2019 and CY2020; the longer term trend has averaged around 40% of global growth. Before proceeding further, it may be prudent to understand why this has been the case and what the incentives were that created said environment.

Utilities and the energy sector generally is a story of high capex and is intrinsically a regulated beast. Globally, much of the windfall for continued investments was created by the FIT or feed-in tariff mechanism, designed to offer compensation and help finance renewable energy investments. Typically this results in a difference in tariff awarded to wind power, for example, or PV sources as opposed to traditional fossil fuels. Its implementation may vary to a great degree however and can lead to substantial price differences seen by the end user. In the US it has primarily relied on legislation introduced during the Carter years, with the Public Utilities Regulatory Policies Act (or PURPA) and more recently through generous tax rebates. In the EU, led predominantly by Germany, the relevant legislation included mandated percentages of the energy mix by source. The difference in policy incentives (theoretically at least) would result in a slightly different burden in terms of cost. A mandate would inevitably lead to costs being passed on to the consumer in terms of higher utility bills while tax incentives and/or effective tariff differentials would see governments bear the burden.

With that in mind let’s return to China. The way in which this has been implemented, in classic CCP style, was a top down approach where the national target set by Beijing would effectively feed down to the provincial governments which then created different incentives in what was effectively a race to build capacity. This typically came in the form of direct subsidies/generous loan schemes. The national solar tariff was issued at about US$0.15 per kWh and various other policies created a conducive environment for the development of onshore wind power plants as well as helping struggling operators (through targeted subsidies). The tariffs for wind power, for example, were set at close to a 30% premium when compared to coal.

By this point, we hope that you are starting to get the point that policy environment and government intervention has a great degree of impact on the fortunes of the energy mix and, by extension, the returns of investors. So, why has China been an exceptional case? Here is were we bring in a few opinions. Firstly, we would argue that the question for China has not been about climate or its impact but rather the structure of the domestic economy. For one, think about the percentage of the PRC’s GDP that is made up of the industrial sector (including manufacturing), it currently stands at 30.8% compared to the US’s 10.8%. Think then about energy usage in said economy. Given industrial production, and manufacturing in particular, creates a greater need for stable supply, especially for the government in keeping unemployment low. A similar argument can be made for why Germany may have taken a greater initiative in the area in comparison to the rest of the Eurozone (i.e. manufacturing accounting for 17.82% of GDP, an outlier for a developed economy).

Moreover, China (along with much of Asia) stands as an outlier in terms of local sources of supply; their short term economic fortunes often decided not on government or domestic demand but rather on the price of global energy. In addition, this is a geopolitical issue for many countries, energy independence being a key issue around the world. Here, think of things like Russia’s influence over Europe’s supply. For China, it’s about the Malacca dilemma in reference to the Belt and Road Initiative, referring to the fact that 80% of PRC’s supply comes through the Straits of Malacca, making for some rather interesting implications on the national security front.

We see similar implications for India. Headway has been made in recent years starting under the previous Congress government in 2010 and catalysed by the Modi government who have pushed towards building out PV capacity in conjunction with the broader “make in India” policy. In fact, if it hadn’t been for the rather bi-polar response to Covid, India should have seen an additional 50% capacity added during the CY 2020-2021 period. Construction delays and grid-issues leading instead to a 50% decline over the period. We should however, assuming no further mishaps or outright bungling, see it hit all time highs soon enough.

This brings us to the next question. Does this imply that developed nations or services oriented economies don’t have an incentive? Especially given that we are likely to see a decline in Chinese growth over the coming years as government incentives are gradually phased out and the rollercoaster that has been recent energy markets settles with the onset of winter. Beijing has in fact ordered the re-opening of coal mines and created a medium term imperative to open up fossil fuels based solutions (which, unfortunately, remain vastly cheaper).

The question of incentives in developed nations – and future growth?

We would suggest that much of the slowdown in China will be mitigated and even overcome by greater demand in the developed world, led by the EU and US. However, the road will be much longer and rather messier because of an arguably more complex political environment characterised by periods of inertia (ah, the vagaries of democracy). Think for a moment about the much touted Green New Deal and the fact that it’s more ambitious aspects may need to be curtailed due to gridlock. Senator Manchin of West Virginia, a vital so-called Democratic moderate, has been the most vocal opponent (the fact that he made his fortune in coal may contribute) but any transition will firstly lead to higher costs (which can either be borne by government and indirectly by consumers or directly by them). The fact that key battleground states, including Biden’s own Pennsylvania, have a significant (and vocal!) portion of their employment in traditional fossil fuels based industries does not help, unless these industries have direct help with the transition period.

The case is similar in the EU which arguably has the most cohesive policy of the Western world. Given the recent spike in energy prices, led in no small part by continued grandstanding from Moscow, is a tell-tale sign that shorter term political considerations may put a dent on the more optimistic expectations. We have previously argued that it was a great failure of policy not to take these considerations into the calculus.

Nevertheless, we do see a longer term trend here. Perhaps not as immediate and with some uncertainty around growth prospects (which matters more for the investor who constantly looks at their securities). For one thing, it offers a great opportunity to create immediate employment and could also have the added benefit of bringing back some manufacturing.

Aside from this, we see the opportunity in these economies as perhaps having greater long term potential. The flipside of democratic governments is also the ability to have free enterprise which does have the added benefit of increasing commercial viability. Think for a moment about the Levelized Cost of Energy (LOCE) for solar and wind, which has fallen close to 90% and 70% respectively, and where the technology that enabled this has come about. Ultimately, as previously alluded to, the cost will determine the viability of these technologies. The biggest hurdles remain things like seasonality, weather and transmission congestion (the ability to circumvent gridlock during peak demand). These issues were rather unfortunately summed up by our own Minister Angus Taylor, who suggested that solar does not work during the night. What we hope he was getting at was the lack of commercially viable storage technology. I remain an optimist and hope that a cabinet minister (and one who looks after Energy) would have the intellectual capacity to see that.

The key to cracking the code on this will remain storage capacity. Lithium-ion batteries, while they continue to fall down the cost curve, remain (at least in the shorter term) ineffective in the deployment on a utility-level scale (too expensive). Under some estimates, we would have to see a reduction in about 80% with tech that can increase lifespan and decrease dissipation. Again, the problem remains peak demand. Without this, even increased capacity build out makes for a rather messy scenario with peak demand leading to overextension while per unit cost during off-peak continues to fall. An alternative through the transition may be a hybrid grid, where peak demand would be complemented by fossil-fuel generation. However, there is a little problem with this idea. Given that there would be very little appetite for the private sector to make the numbers work even in smaller markets, it would require government funding. The question may be what would happen in the advent of a technological breakthrough in storage given the pace of innovation currently taking place? That level of uncertainty and constant flux is also perhaps the reason why there is very little appetite for traditional generators, the potential risk of what are termed stranded assets.

So, the growth prospects are there but how do we benefit?

For those that read last week’s article, it may seem that we do not believe in renewables or the transition occurring. This is simply not the case. The previous contention was the lack of policy initiative to take dislocations and the adverse impacts into consideration. As an investor it pays to be aware of some of the nuances that are underlying the sector. For example, how does Senator Manchin in the US throwing a spanner in the works of the more ambitious proposals impact a renewables sector, and PV companies priced to perfection, impact your returns in the short run?

Similarly, how does direct policy intervention incentivised by political considerations impact a rare-earths manufacturer like Lynas? We’ve previously talked about their DoD funding to start manufacturing in Texas. Even for those that aren’t particularly interested in the space, how does a lack of capital investment in more traditional fossil fuels based approaches impact the price of those commodities which still remain vital to the economy not only in terms of growth but inflation? Assuming inflation and a more aggressive monetary policy stance, what might that do to my own portfolio with say an allocation to Alphabet or Microsoft (Hint: the discount rate changes and so does their valuation). However, we’ve also written about the broader supply chain in terms of Mineral Resources, Pilbara and broader commodities including copper?

This week we are writing about a pair of financial services companies that are growing, have tailwinds and are trading at what we believe to be bargain prices. In the wake of the 2019 Royal Commission we have seen huge changes in the Australian financial services industry. There has been a structural shift away from banks by consumers, igniting the fintech scene in Australia. Non-bank lenders have also been beneficiaries but we feel it is a sector that has been overlooked by investors and offers some quality businesses that are growing their loan books at attractive margins.

Money3 (MNY.ASX)

Money3 Corporation Limited is involved in the delivery of secured automotive loans as well as secured and unsecured personal loans. The secured automotive loans relate to the purchase of a vehicle with the vehicle as security for the loan. MNY currently has a loan book of $600m, having grown considerably over the past few years.

Funding Facility

Authors: Ron Shamgar

MNY recently executed a transformational $250m funding deal with Credit Suisse. The deal will both lower their cost of capital and allow them to expand into new car financing; given the higher value of new cars this should accelerate their loan book growth. The new facility will increase margins and allow MNY to pursue their growth strategy in the auto finance market.

Acquisitions

MNY has also been active when it comes to M&A activity. They acquired New Zealand company Go Car Finance in 2019, giving them a presence in the NZ auto finance market. Go Car now has a loan book of AU$158m, increasing over 300% since MNY acquired them. Their NZ presence opens up the opportunity for MNY to grow their loan book above $1bn and, with the cheap funding behind them, MNY should continue to scale this segment. More recently, they took over Automotive Financial Services (AFS) who have a $52m loan book and are projected to do around $2.5m NPAT in FY22.

Source: MNY company filings

Valuation + Outlook

MNY has been a post covid winner and, with second hand car prices at highs, they are benefiting from increased value of their loans. MNY has a clear path to grow their loan book on the back of their new loan facility, which will see them expand their new car lending, and the Go Car Finance acquisition ,which has given them a position in the NZ market. There have been issues with vehicle supply shortage, slowing loan origination, but that will normalise as the world returns to normal. MNY has been able to acquire struggling competitors that don’t have the same access to funding that Money3 has. We can see MNY achieving a loan book of $1bn by FY24. We estimate that this will yield approximately $80m in NPAT which would put MNY on a forward PE multiple of around 8x, all while they continue to distribute strong dividends. We can see MNY being worth double their current share price if they achieve that $80m of NPAT by FY24.

Last week we saw Money3’s peers Plenti (PLT.ASX) and MoneyMe (MME.ASX) provide strong updates and they have both seen good growth in loan originations. We expect MNY to do the same, their upcoming annual general meeting on November 16th could be a catalyst as they provide an update on their outlook for FY22. We expect them to do over $50m of NPAT in FY22 which would put them at a PE of around 14x.

Source: MNY company filings

Resimac Group Limited (RMC.ASX)

Resimac Group is a residential mortgage lender and multi-channel distribution business specialising in Prime and Specialist lending. RMC operates in targeted market segments and asset classes in both Australia and New Zealand. As a non-bank financial institution, they have developed a high quality lending portfolio, loan servicing capability, and funding platform predominantly through organic growth.

Resimac is a quality business that has mostly slipped under the radar. They are attacking a huge market and are achieving huge growth in their loan book with AUM (assets under management) now at $15bn. Resimac are currently investing heavily in their digital capabilities to develop a customer centric organisation that is data-driven, powered by a modern digital platform providing cost-effective, scalable and rapid growth.

Resimac has benefited from the consumer shift away from traditional lenders. In a post-Royal Commission world consumers are better informed and have started to favour alternatives in finance solutions, the recent rise of fintechs is a testament to that. Resimac has a number of competitive advantages over their traditional bank competitors; by offering superior service, systems and approval procedures they have established themselves as one of the biggest non bank lenders in Australia. Simply, Resimac has the quickest loan settlement turnaround time.

Resimac has been diversifying into asset finance under the newly acquired Resimac Asset Finance brand. RMC will look to leverage their existing digital expertise in scaling their asset finance business. Given the growth in their home loan portfolio, the asset finance business should be highly accretive to Resimac’s AUM.

The key drivers of Resimac’s earnings are their AUM and their net interest margin (NIM). Resimac has benefited from a lower cost of funding which has led to a huge increase in earnings. Their funding comes from issuing residential mortgage backed securities (RMBS). The older bonds were issued at a higher rate and, as they mature, the new bonds they will be issuing will be at a lower rate. Their NIM was 207bps in FY21, up from 190 in FY20. Resimac will have very favourable funding costs for FY22. Looking to their AUM, they grew their home loan book by 11% in FY21. If they continue to deliver a superior service, growth in NZ as well as their diversification into asset finance, their earnings power is huge.

Valuation + Outlook

In current market conditions Resimac has seen multiple tailwinds that have accelerated their business. Resimac posted a 37% return on equity in FY21, an almost unheard of result for a company trading at less than 10x earnings. Looking ahead, we see Resimac continuing to benefit from low cost of funding in the short term. Resimac have a tiny portion of the Australian lending market and there is plenty of room to grow AUM in both home loans and asset finance. Resimac should also see their NIM remain above 200bps for HY22. Considering growth in their loan books and a strong NIM, Resmac should be trading at closer to 6x earnings in FY22.

In their most recent presentation, Resimac said they are targeting $8bn in annual settlements by FY24 for the home loan segment. They are also targeting $1bn in annual settlements by FY24 for the asset finance business. These targets would see Resimac achieve strong growth in their originations and, at a PE of less than 8x, there is huge upside for multiple expansion.

Source: RMC company filings

Finding a quality business like Resimac that is trading at less than 8x earnings, paying a dividend and growing their business is hard. Resimac is being overlooked by the market and, at current valuation, Resimac offers huge upside. They are a very profitable company that is attacking a huge addressable market.

Disclaimer: MNY and RMC are both currently held in TAMIM portfolios.

This week we take a dive into energy markets, in particular the likely medium to long term outlook for the sector. We have previously written on the potential dislocations both in uranium spot prices (which we wrote off last year) and the potential upward trajectory in oil prices. The former has seemingly played out (though it may still be very much in its infancy) and the second seems to be playing out in real time with Brent futures trading at US$85.45 per barrel and WTI at US$83.73 per barrel. Many would also be aware of the sheer scale of disruptions in the UK and broader shortages of LNG in the Eurozone heading into winter. Even more recently, the headlines have been taken over by blackouts in China in the face of increased demand.

So, what has happened? Especially after coming off negative prices in the middle of 2020 and a seeming supply glut in oil.

Context

Author: Sid Ruttala

For those that have watched recent price action, there has seemingly been an upward trajectory in spot prices despite bearish signals. Per the last EIA report, US crude inventories building close to 6m barrels and doing so within broader expectations of drawdowns, while gasoline and distillates drew down approximately 2m barrels. Combine this with US production bouncing back to 11m barrels and this would usually indicate rather bearish signals. However, there is a catch, the underlying data isn’t necessarily what is important, rather how the market reacts to said data. In this instance, it is a clear indication that the market is seeing something that we may be missing.

Before we go further, understand that shorter term spikes may be due to certain intricacies and quirks of the calendar. For example, the price action and moves earlier this month (on 11 September) may have been due to Columbus Day. The nature of the futures market is such that traders have to consistently roll contracts in order to maintain positions. Days like that, when the futures market remains open whilst the banks close, will inevitably mean a little manipulation (i.e. same day settlement requirement while banks remain closed).

But, taking those exceptions out of the equation, we are clearly seeing signs that we may be in for a bumpy ride. For those that have read our previous articles on this issue, our base case was that when demand does inevitably pick up post-covid we are likely to see supply bottlenecks precisely at a time when demand started to pick up. This was during the depths of covid when prices became negative and when the question became where to store the product; we saw the flip side with an increasing lack of investment in the western world (due to climate policy), high cost of production for shale in the US (which saw increased shut ins). What we were perhaps wrong on was the resurgence of US production, which beat even our most optimistic expectations.

So, what has led to this situation?

We are by no means climate change sceptics nor are we against renewables, the infrastructure for which still requires investment in the underlying technologies and associated capital for commercialisation and global scale. What we have found bizarre is the sheer lack of nuance and understanding of the dislocations that may take place. Take for example, the recent International Energy Agency (IEA) report whose STEPS model presents the below case:

Demand (for oil) levels off at 104 mb/d in the mid-2030’s and then declines slightly to 2050;

Oil in transportation increases and peaks around 2025 at 97 mb/d and declines to 77 mb/d in 2050;

Oil falls by around 4mb/d in countries with net zero pledges between 2020 and 2030 which is then offset by an increase in 8 mb/d in the rest of the world;

Coal exports from Australia will fall by 5% to 2030;

Oil prices will rise to around US$77 per barrel in 2030.

The above seems plausible aside from some fundamental assumptions that don’t sit well with even the most basic understanding of how economies transition or political incentives operate. For one thing, it assumes that nations with net zero targets stick to their goals. After the recent blackouts in China and the long queues at petrol stations (in the UK) we don’t think the transition occurs quite so smoothly. Secondly, there is also the assumption that 45% of the energy mix in the Asia region will be accounted for by renewables, as some of these emerging markets move into middle income countries. In fact, it is assumed that energy consumption will flatline or decline in emerging markets such as India. History, however, tells us that it is simply not true, consumption increases exponentially as people and nations move into middle-income.

The problem? A lot of these assumptions not only determined the policy environment but also the flow of investment and capital. Think for a moment about the yield on bonds for coal or oil producers such as Newcastle Coal (yielding 10.29%) or AGL’s inability to find requisite debt financing. Can you really blame investors? Think for a moment about a bank trying to finance said deal, requiring capex that typically has a pay off over a multi-decade period. Assuming that at some point the transition occurs and the market has dried up, what then happens to said assets? They are what is termed stranded assets.

Many have commented on the ability of nations such as Saudi Arabia or Russia to increase production, especially given their low cost of production. Saudi for example has a cost base of US$2.80 per barrel. What we feel is that investors should rather use what is termed the budgetary breakeven, which is the breakeven price in order to run a balanced budget (especially in the absence of taxation) which currently stands at US$67.80 per barrel for the Kingdom. Suffice it to say, OPEC broadly has an incentive to keep supply limited in order to drive gross margins and profitability.

Here is where the IEA may be onto something. It makes the conclusion that producers are incentivised, given the uncertainty around the future, to focus on existing production (as opposed to bringing on new production) in order to generate the highest possible profits. So, what does this mean?

Put simply, we will see a massive disincentivisation to bring on additional production, despite demand as the world transitions over a twenty year period (the IEA’s most optimistic forecast). Given this base case and assuming current trends continue to stay at status quo, we are likely to see increased oil prices. We previously made the call that we would see this happen this year. We very much see this still in its infancy with triple digits quite possible in the near-term.

What are the implications?

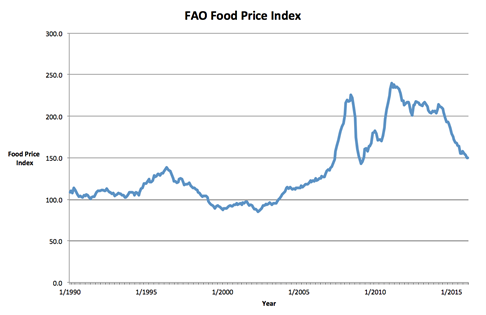

When we talk about the price of oil, many immediately equate it to the price paid at the petrol station. Consider the broader implications of this. The chart below shows the FAO Food Price Index, a measure of the monthly change in international prices of a basket of staple food commodities, between 1990 to 2015. The highest period of per annum growth? Between 2003 to 2008. The price of oil during the same period? Went from US$20 per barrel to a peak of US$140 per barrel.

Source: FAO

Consider the follow-on impact on CPI and inflation in an era where monetary policy is likely to be curtailed due to the sheer size of debt issued over the decade since the GFC. Consider also the implications for large energy importers such as India and China, who are heavily dependent on the sector and the consequent lower growth prospects in the broader global economy.

How do we profit? We’ve previously written on Woodside (WPL.ASX) and continue to feel that this is a fantastic prospect. Buying larger companies (i.e. further up the maturity curve) with existing low cost production is the more reasonable way to generate returns (as opposed to smaller ones unless looking at M&A prospects). Looking globally, those looking like good buys are Exxon Mobil (XOM.NYSE), Enbridge (ENB.TSE) – pipelines – and APA Group (APA.ASX). These businesses should continue to generate massive cash flows over the next decade.Looking more broadly, as upward pressure on inflation continues despite lower real growth rates, focusing on defensive plays should be beneficial. BHP’s recent venture into potash and price action in fertilizers is rather telling. Defensive here means generating revenues that are correlated to inflation (as opposed to growth,which has consistently done well for investors in the past two decades).This morning WPL released its quarterly guidance, where the realised price stood at US$59 per barrel and sales revenue up 19% despite a slight decline in production (by 2%).

This is the market’s incentive. Focus on margins through higher price realisation while at the same time flatlining or downward pressure on production.

Disclaimer: WPL.ASX and XOM.NYSE are both currently held in TAMIM portfolios.

A few weeks ago we covered a key holding in the TAMIM Global Mobility portfolio, a fully integrated lithium company called Albemarle (ALB.NYSE) that is poised to benefit from increased production of electric vehicles. This week we revisit lithium and take a look at three heavyweight ASX stocks that are shaping up as market leaders.

Author: Adam Wolf

The lithium space has received a lot of attention recently with investors sending any companies with lithium exposure to sky high prices, similar to what we have seen with uranium. Lithium is the primary component of lithium-ion batteries (LIB), which are rapidly gaining traction due to their wide applicability in energy storage. In particular, solar and wind energy projects and the increasing demand from the electric vehicle (EV) sector. With the push for green energy and rise of electric vehicle production, everyone can see the upside in lithium. While the easy money may have been made, these lithium companies still pose an interesting proposition to investors looking to gain exposure to the broader electric vehicle thematic.

Source: Albemarle company filings

Data from Benchmark’s Lithium Forecast shows a projected annual lithium supply deficit of up to 225,000 tonnes in North America and 500,000 tonnes in Europe by 2030. To incentivise the right amount of investment in new mines there is going to have to be a sustained period of elevated prices.

Source: VUL company filings

Bringing deposits into production is a time consuming process and it can take years to complete the necessary feasibility studies and actually construct a mine. In order to understand the merits of a lithium deposit we first need to understand the difference between brine and hard rock deposits. Lithium deposits can either be produced from brine or spodumene rock production. Brine production is typically cheaper and significantly more environmentally friendly. Brine deposits are typically found in South American countries like Chile and Argentina. However, there is a catch with producing carbonate from brines. Although lithium carbonate can be converted into lithium hydroxide (what is used to make the batteries for EVs), it comes at an additional cost. This is causing brines to look less attractive to battery producers, leading to industry players scaling up or increasing their hard rock mine assets. Although brine deposits are cheaper to extract they require more processing and are typically used in lower density batteries, the batteries that enable electric vehicles to drive for long distances require higher density lithium which is found in hard rock and is therefore better suited. The lithium explorers in Australia are looking for hard rock lithium.

Source: newagemetals.com

Mineral Resources (MIN.ASX)

Mineral Resources Limited is a mining services company with a portfolio of mining operations across both lithium and iron ore. Their mining services segment comprises of crushing/processing, mine construction as well other services. The mining services/engineering sector has typically attracted very little attention from investors and historically trades on very low multiples as a result of cyclicality and the nature of their revenues, which are contracted. More recently we have seen higher labour costs due to labour shortages which have impacted margins. MIN offers more upside than your usual mining services company through their iron ore and lithium operations yet they are still trading on low multiples alongside other mining services companies.

MIN is a top five global exporter of lithium, they have interests in two lithium mines and a lithium hydroxide plant in Perth. In 2019, MIN sold 60% of its ownership in the Wodgina lithium hard rock mine, a Tier 1 asset, to US based Albemarle (a holding in our Global Mobility portfolio, as mentioned). The Wodgina mine is currently under care and maintenance, the mine would be a 750,000 t/yr operations. The JV is also building a processing operation and the 50,000 t/yr Kemerton lithium hydroxide plant, under development southwest of Perth. Through its shareholdings in Mt Marion and Wodgina, Mineral Resources has access to significant amounts of spodumene, which can be used as feedstock for much higher margin lithium hydroxide production.

Outlook

Mineral Resources recorded an EBITDA of $1.9bn in FY21. Yes, this was inflated by sky high iron ore prices but if you look at a more normalised environment with lower iron ore prices, a cheaper labour market and accounting for the production that the Wodgina Project will bring once brought back online, a sustainable EBITDA of $1bn is certainly not out of the question. This would see MIN trading on an EV/EBITDA of less than 8x. MIN also have 5.5% stake in fellow lithium producer Pilbara Minerals.

Pilbara Minerals (PLS.ASX)

Pilbara Minerals is an emerging lithium company producing spodumene concentrate with operations in the Pilbara region in Western Australia. PLS has 100% ownership of the world-class Pilgangoora Lithium-Tantalum Project (“Pilgangoora Project”), the largest independent hard-rock lithium operation in the world. PLS is looking to become a fully integrated lithium raw materials and chemicals supplier. The significant scale and quality of the operation has attracted a consortium of high quality, global partners including Ganfeng Lithium, General Lithium, Great Wall Motor Company, POSCO, CATL and Yibin Tianyi. PLS is one of Australia’s largest lithium focused companies and with good reason. They have made several strategic moves that have separated them from the other lithium producers, some of which we will delve into.

Battery Materials Exchange

Pilbara Minerals executed an agreement with GLX Digital Limited (a private company) for the launch of a new sales and trading software platform for the Pilgangoora Project, providing flexibility to transact by auction, tender process or bilateral sale. This battery metal exchange serves as an auction house to bid for Pilbara’s offtake from the Pilgangoora project. So far the exchange has yielded prices far above the spot price of lithium.

The excessive prices PLS has fetched so far is a testament to how limited the supply of quality hard rock lithium really is. The battery metal exchange is a huge competitive advantage for PLS and provides them with greater flexibility in terms of selling their product that has so far maximised their margins. This is yet another well executed strategic move by the PLS team, the next auction is on October 26 so all eyes will be on whether PLS continues to achieve such premiums on the exchange.

Altura Project Acquisition

In late 2020, PLS announced the acquisition of the Altura Project for a consideration of $175m USD. The Altura Project is located on an adjoining tenement package immediately to the west of Pilbara Minerals’ Pilgangoora Project. The operation is part of the same mineralised system that underpins the Pilgangoora Project and uses similar open-pit mining methods, processing flowsheets and mining equipment The acquisition of the Altura Project should provide Pilbara Minerals with a unique opportunity to realise tangible operational synergies by consolidating the two neighbouring projects into a single integrated operation. Of particular interest to the PLS is the opportunity to mine that section of the Altura orebody that is otherwise sterilised without access being granted to Pilbara Minerals’ ground to undertake mining activities.

Downstream Opportunity

PLS entered into an agreement with POSCO (005490.KRX) where PLS will have ownership of up to 30% in a downstream JV for a lithium chemical conversion facility in South Korea. This joint venture will give Pilbara Minerals significant exposure to one of the world’s most dynamic and fastest growing markets for lithium chemicals. This downstream opportunity would shift PLS up the value chain which could see them get higher margins and earnings from their offtake. The project is still subject to a final investment decision and approvals but the proposed facility will have the capacity to to produce approximately 40k tonnes of lithium hydroxide p.a., enough to produce the batteries of one million electric vehicles.

Outlook

PLS produced 280kdmt (thousand dry metric tonnes) of lithium in FY21. PLS expects to be producing 580kt p.a. by mid-2022, this is more than doubling their production and it’s all at a measured capex. Simply put, PLS ticks all the boxes. They are operating in a world class mining jurisdiction, they have long mine life of more than twenty years, it is open pit (cheaper and easier to mine), they have cost advantages over the brine operators in South America (who are producing an inferior product) and they have significant synergies to be realised through their acquisition of the neighbouring Altura lithium. PLS are expanding their capabilities through both midstream and downstream operations which should add significant value to their final product, increase their margins and give them even more flexibility with their offtake.

Source: PLS company filings

Vulcan Energy Resources (VUL.ASX)

VUL has been one of the market’s biggest winners over the past year (up 1000%+). Vulcan is developing the world’s first and only zero-carbon lithium process and plans to produce battery-grade lithium hydroxide from geothermal brines pumped from wells with a renewable geothermal energy by-product. VUL are currently conducting a definitive feasibility study for their lithium project; this is the final step before commencing construction on the operation. Everything Vulcan touches seems to turn to gold. Recently, we saw their spinoff KNI reach multiples of its offer price after listing. To understand why VUL has been one of, if not the hottest stock on the ASX we first need to make sense of how geothermal energy works.

Source: VUL company filings

Geothermal Energy

Geothermal lithium offers a more sustainable and less impactful way of extracting lithium. Geothermal lithium mining has nearly zero environmental impacts and leaves a marginal ground or water footprint. While traditional lithium brines rely on evaporation processes to collect the precious metal, in geothermal plants lithium-rich brine is pumped to the surface from geothermal reservoirs. The heat carried by the brine is used to produce renewable energy and the brine is re-injected in the reservoir. A geothermal plant can not only produce lithium but also produce renewable energy, giving Vulcan two different streams of revenue.

Source: VUL company filings

The onset of ESG-focus has changed the way investors allocate capital and has led to the rise of a green premium for lithium amid heightened demand for more environmentally friendly resources. Given VUL’s zero-carbon process they have received a huge premium from the market.

Gec-Co Acquisition

Gec-Co Global Engineering is a consultancy company focused on deep geothermal projects at surface. Gec-Co has a highly credentialed scientific team with 100+ years of combined world-leading expertise in developing geothermal projects, from exploration to production. Motivations are fully aligned: to decarbonize heat and power in Europe with geothermal development in the Upper Rhine Valley in Germany. The acquisition is part of Vulcan’s plans to rapidly grow its development team in Germany and accelerate its Zero Carbon Lithium project towards production

Processing Hub

In line with other producers like PLS, VUL will be developing their own processing hub which will add value to their lithium end product. The Central Lithium Plant is intended as a processing hub, processing lithium chloride from multiple combined geothermal and lithium sorption plants into lithium hydroxide. VUL secured a site just outside of Frankfurt with the location allowing for low carbon transport options from their nearby project areas, as well as renewable energy to power the proposed plant, which underpins Vulcan’s commitment to minimising their carbon footprint at each step of their process.

Source: VUL company filings

VUL’s Zero Carbon Lithium project is located in Germany, the company owns Europe’s largest JORC-compliant lithium resource. The project is located in what Vulcan describes as the heart of the European lithium-ion battery industry, VUL are looking to address Europe’s decarbonisation needs. Europe is the largest growing lithium market in the world and hosts many of the biggest car manufacturers yet they don’t have any local supply of Lithium hydroxide.

Note 2: Based on electric vehicle sales and lithium-ion battery production growth

Source: VUL company filings

VUL is planning to produce 40k tonnes of lithium hydroxide p.a. as well as produce 74MW of renewable electricity. This week VUL signed yet another offtake deal for its hydroxide with Umicore, a leader in cathode materials production used in lithium-ion batteries for electrified transportation. We expect that VUL’s final product will command a premium over market prices due to the environment-conscious nature of the project.

OutlookVulcan’s Zero Carbon Lithium project is arguably the most interesting lithium production plan in the world. Not only will they provide lithium hydroxide for electric vehicles but they will also produce renewable electricity, you can’t get a more net positive mining operation than that, can you?

Their project is also in a convenient location. Being in the heart of Europe gives them the opportunity to benefit from the EU’s growing environmental mandates. VUL is also well funded following their recent cap raise with $331m in cash. This gives them more than enough cash to expand via the acquisition of other projects. They are planning to have operations underway in 2024. Their energy and lithium projects have a post tax NPV of over €2.6bn.

The share price was under $1 in 2020 and is now over $13.50. It is easy to say that the market has priced in the upside for VUL but, given the significance of this project and the rapidly growing thematics they are targeting, at a market cap of $1.6bn who knows where this will be in a few years when they actually start producing lithium hydroxide and renewable energy. VUL also announced they will be dual listing on the Frankfurt exchange, giving them access to European investors; we expect to see a lot of news flow over the next few months. When VUL releases the results of their definitive feasibility study the market will know in more detail the true economics of the project. In the current environment, the market is rewarding companies for sustainable operations and Vulcan’s commitment to minimising their carbon footprint is attracting lots of interest from investors and offtake partners. If they execute their Zero Carbon Lithium operations, they could be a global pioneer in lithium.

Summary

Through its applications in electric vehicle batteries and green energy storage, there is no doubt that lithium will be an essential component of the decarbonisation process. The rapid rise in carbon mandates and electric vehicle production has seen demand for the metal rise significantly, sending supply for lithium into a deficit and prices flying as a result. When looking for exposure to lithium, investors have a plethora of opportunities and a lot of junior miners are pivoting their focus to look for lithium deposits. The companies mentioned in this article each have their own merits but most of all they have the resources to become the BHP-equivalent in the lithium production industry alongside our Global Mobility holding and largest lithium producer in the world Albemarle. All the stocks mentioned in the article are developing their mid and downstream capabilities which will enable them to deliver a higher value product. While MIN may not be as enterprising as PLS and VUL, they offer a cheaper entry into lithium exposure hiding behind their not-so-sexy mining services business. As for PLS and VUL, they are both making strategic moves in the industry and have considerable competitive advantages over other players.

Disclaimer: Albemarle (ALB.NYSE) is held as a long position in TAMIM’s Global Mobility portfolio. The TAMIM Global Mobility strategy seeks to to capitalise on the ongoing $7 trillion autonomous and electric vehicle revolution.