This week we discuss a hidden gem on the ASX and one which we believe has the ultimate investment exposure in a Covid world. With the company only listing three months ago it is yet to receive much attention from fund managers and brokers, yet it is highly profitable and on an upgrade cycle. Find out which stock below.

Author: Ron Shamgar

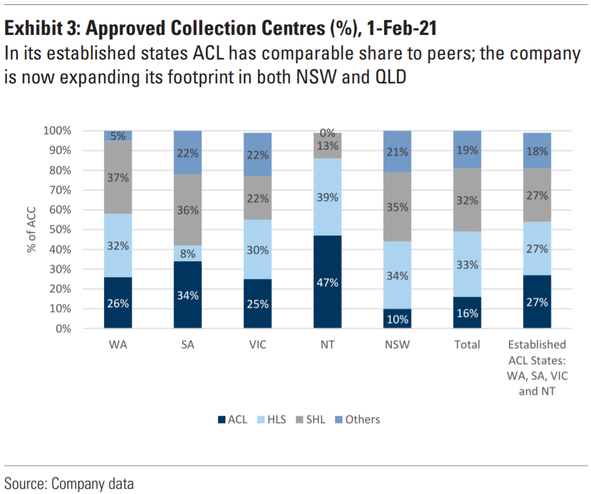

Australian Clinical Labs (ACL.ASX) is the third largest pathology provider in Australia. The pathology market is worth over $6bn annually and 80% of revenues are dominated by three main players: Sonic Healthcare (SHL.ASX), Healius (HLS.ASX) and ACL – with 16% market share. The industry is growing at approximately 5.4% per annum but Covid PCR based testing has added another layer of substantial and lucrative revenues.

Source: Goldman Sachs Equity Research

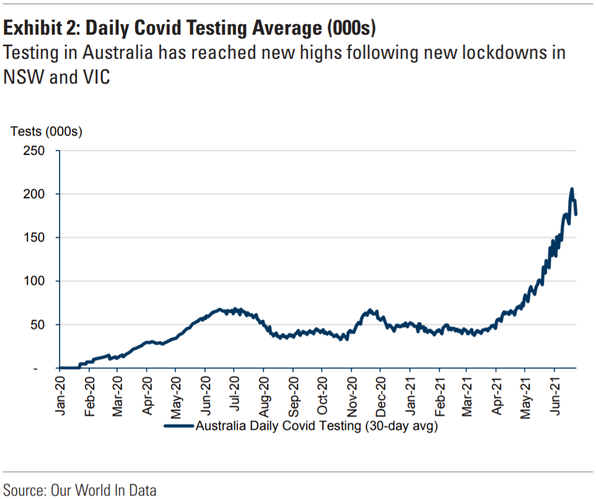

Now whether Australia reaches 80% or 100% vaccination rates, or whether we are in and out of lockdowns or completely open our borders – we don’t believe it matters for testing requirements. Whatever your stance on the situation, Australia’s Covid strategies and responses are fixated on case numbers. This means that, for better or worse, testing volumes should continue to stay elevated for a couple of years to come.

What gives us confidence in this statement is the high levels of Covid cases overseas, especially in countries where vaccination rates are high. Ongoing testing will be required for travel purposes, work related requirements, healthcare and staying on top of different strains of the virus that will undoubtedly evolve over time. More importantly, alternative antibody (antigen) testing methods so far appear to be unreliable in replacing PCR based methods. ACL are currently serving over ninety hospitals and are also running thirty specialist skin cancer clinics across Australia which are responsible for diagnosing over 15% of all reported melanomas. Hence ACL profits are sustainable for now.

Source: Goldman Sachs Equity Research

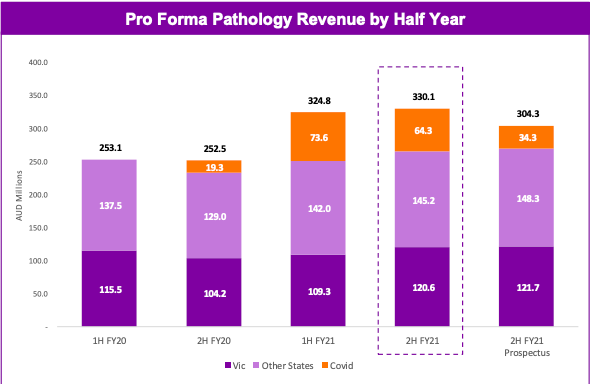

The company has significant momentum and is in the midst of a strong upgrade cycle that we believe the market is currently overlooking. FY21 prospectus forecasts were beaten by 5% on revenues (to $674m) and were over 20% ahead in the NPAT line (to $89m). Free cash flows are strong and the balance sheet ended the period with low levels of net debt ($65m).

Source: ACL company filings

All this should allow ACL to continue to make acquisitions, especially in NSW and QLD where ACL’s market share is still quite low. Unlike their larger peers, ACL should be able to make smaller acquisitions that make a meaningful impact on their bottom line. ACL’s past acquisitions have increased their presence throughout Australia and have provided significant synergies for the company by reducing operating costs and improving EBITDA margins. Watch this space.

The momentum behind the business was evident with 1H22 guidance upgraded significantly from prospectus forecasts. Revenues are now 22% ahead of the previous forecast and NPAT is a whopping 130% ahead at $53m. To put this in perspective, analysts previously had ACL earning $53m for the whole of FY22. Dividends are expected to be paid at 60%+ of profits, placing the stock on a 6%+ fully franked yield.

ACL has also invested significantly in their in-house tech and operates a national unified pathology system that allows the majority of tests, clinicians and laboratories to operate as one laboratory across the country. ACL’s unified pathology system enables operational benefits which include improved turnaround times and ability to handle demand peaks, national benchmarking to drive performance improvement and efficiencies and share innovations. Their system is a competitive advantage and has been a key factor in their ongoing and pivotal role in Australia’s Covid response. This system and the advantages it brings will serve them well if and when there is a decline in Covid testing.

Source: ACL company filings

Last year we successfully (and rather profitably) rode the wave of Covid winners in e-commerce and BNPL stocks. We see ACL as a similar beneficiary but on a more long term and sustainable level. Any slowdown in Covid testing should be replaced by increase in non-Covid business/testing resuming.

Source: ACL company filings

With SHL and HLS trading on 14-19x PE multiples, we see ACL – currently at 9x PE – as significantly undervalued. We believe that management’s FY22 guidance is conservative as was their FY21 guidance. They are assuming a sharp deceleration in test volumes and, as we said above, we don’t believe it will be quite so sudden. On the back of the conservative forecasts, we expect further upgrades through the year and further acquisitions to drive a rerate. An ASX300 index inclusion is also potentially on the cards. Our valuation is $6.00+ and ACL is currently one of our top holdings in both the Australia All Cap and Australia Small Cap Income portfolios.

Disclaimer:ACL is currently held in TAMIM Australian equity portfolios.

Our friends at Merricks Capital, an allocation in the TAMIM Credit portfolio, take a look at changing shopping and consumption habits in the wake of COVID-19. An important consideration for anyone with exposure, equities or otherwise, to these sectors.

This article was originally distributed on 20 August 2021 and has been reproduced in part with the permission of Merricks Capital.

Changing shopping and food consumption patterns have occurred as a result of the COVID pandemic and the resulting lockdowns. Some of these trends have normalised but there is likely to be a more permanent shift in some areas of food demand.

These structural shifts have implications for the entire agriculture supply chain, and we are seeing increasing investment in technology and infrastructure from some of our borrowers and the larger supermarket chains to support this demand.

Merricks Capital recently spoke with one of our borrowers, who arguably produces some of Australia’s best Wagyu beef, about the impact of the stand still in the restaurant and hospitality supply chain.

In summary the “dine in” distribution channels have come to a halt but the increase in demand from consumers for high end food product through home delivery and grocery channels has been significant.

We are currently reviewing several opportunities across the food supply chain that will support “the premiumisation” of consumers “in home” demand.

The increased investment in the industry and ongoing changes in food consumption trends will not only ensure the continued performance of our existing investments in the agriculture industry, but they will result in an increasing level and diversity of opportunity going forward.

As part of its annual results presentation this week, Coles provided an update on the impact of COVID on trends in food demand and consumption.

Sales in its supermarket division rose 2.5% on a comparable basis over FY21, and by 8.4% over 2 years. While consumer behaviours began to normalise at the end of the third quarter and into the fourth quarter, increased in-home consumption as a result of COVID-19 positively impacted sales revenue growth throughout the year.

Normalising consumer behaviours in the fourth quarter included the return of Sundays as the largest trading day of the week, customers shopping more frequently, and transaction trends improving with growth in the convenience, food-to-go and impulse categories. While basket size moderated, they remain above pre-COVID 19 levels.

Coles noted inflation in the fresh food segment (supermarket price deflation ex tobacco and fresh food of 0.8% compared to total price inflation of 0.8%) highlighting red meat as a source of price inflation due to elevated livestock prices. This is consistent with ABS data which showed price inflation over the June quarter for vegetables (+5.5%) and fruit (+4.7%), partly driven by a shortage of pickers and extreme rainfall on the east coast of Australia. Beef and veal prices rose 3.6% with farmers continuing to re-build herds, reducing meat supply. Food prices overall rose 0.7% over the financial year.

Coles and Woolworths control around 70% of the grocery market and are central to Australia’s agricultural sector. Trends in supermarket food demand can have important implications across the entire agriculture supply chain.

Around 31% of fruit and nut production is exported (compared to 71% of total agricultural production) and these industries are particularly dependent on trends in the domestic market.

Separately, food price inflation is a positive for the industry when it is accompanied by higher margins for farmers and food manufactures, ensuring the continued profitability of the sector, and our borrowers.

The Tamim Credit fund through its investment into Merricks, has exposure to the agriculture sector including the supply chain. These investments are across quality assets that will benefit from the increased incidence of at-home food preparation and consumption, including the demand for fresh pre-prepared and convenience meals, as well as higher prices.

The “premiumisation” of home cooking is a particularly interesting trend. Feedback from our wagyu production business, for example, indicates that wholesale (restaurant) demand has been largely displaced by retail and home delivery of premium beef product, and this has resulted in orders and pricing remaining steady.

Both Woolworths and Coles have indicated a focus on investing in technology, including in their online capabilities and supply chain modernisation programs. These capital expenditure plans are evidence of the commitment from the largest participants in the market to the delivery of world-class technology solutions to improve efficiencies, customer experience and a secure food supply.

The changing landscape in food demand and consumption means that food production businesses will need to become more efficient and less reliant on seasonal labour. This is driving the need for capital investment which is providing a range of attractive lending opportunities in the sector.

The impact of COVID-related lockdowns on agriculture markets is complex. Low population growth will weigh on overall demand, but the shifting dynamics of that demand – from restaurants and take-away to home preparation and consumption – and the investment in technology and modernisation, will continue to have implications across the agriculture supply chain. These changes will ensure a continuing flow of opportunities across a diversified portfolio of assets, which will provide investors with attractive risk-adjusted investment returns.

Disclaimer: There is currently an allocation to Merricks Capital in the TAMIM Fund: Credit portfolio. A portfolio investing into private debt and other credit opportunities with the aim of generating a steady, consistent interest income stream for investors whilst at the same time seeking to preserve capital.

This week we continue our look at dividend yielding stocks with two companies that make reasonable investment propositions. One rather unloved by the market, Aurizon Holdings Ltd (AZJ.ASX), and the other reasonably fair value, APA Group (APA.ASX), but both offering steady long-term dividend streams.

Aurizon Holdings (AZJ.ASX)

Floated in 2010, Aurizon has certainly seen ups and downs over the past decade. Before we get to the details, a brief overview of the company. Originally known as QR National, the company was established in 2004 bringing together Queensland Rail’s coal, bulk and containerised businesses. It grew by acquisitions over the following decade, expanding nationally and taking over Australian Rail Group and CRT, giving it a footprint across NSW, Victoria and WA. To put it simply, the company provides design, construction, overhaul, maintenance and management services to the mining industry with the bread butter remaining the Central Queensland Coal Network (CQCN). Given the loss of appetite with regards to coal and fossil fuels, the business has seen significant headwinds since IPO. With the likely long-term decline in its traditional business, it may seem surprising to many that we would even consider it. However, it must be viewed as a business in transition.

While we see significant declines in the market for thermal coal, we also see continued demand for metallurgical and coking coal, a key ingredient in the manufacture of steel. This is one segment that is likely to continue to see tailwinds given the impetus for spending on infrastructure globally. If spot prices are anything to go by, close to doubling in the past year, we are seeing significant pockets of value in the space. In fact, the company expects haulage volumes for 2021 to increase by 5%. Drilling down further, while we have seen flatlining or declines in crude steel production in China we are likely to see this cushioned by increases in India and across Asia (including Japan) as nations embark upon upgrading their own infrastructure. In our view, it is rather telling that the business extended its contracts with its biggest customers, including Glencore (GLEN.LON), Anglo American (AAL.LON) and New Hope (NHC.ASX).

Author: Sid Ruttala

For those still not convinced, there is a clear strategy from management that takes into account the long-term structural headwinds facing the industry. This includes declines in the demand for thermal coal with a target to reduce exposure to thermal coal to less than 20% of Above Rail revenues by 2030. This is a more than rational business decision given that the world will still require Thermal during the ongoing transition period. Look to the recent example of China, a situation which has resulted in spot prices sky-rocketing to $170 USD/Tonne (doubled on a 12-month basis). Despite the government’s adamant assertion of zero-emission targets, a heat wave in Zhejiang, Jiangsu and Guangdong (her biggest industrial provinces) saw output pushed higher and bottlenecks during peak demand. It is also quite telling that policy makers have restarted production in the Shanxi and Xinjiang provinces (a region prone to flooding, by the way). Suffice it to say, these bottlenecks mean that the AZJ’s 20% target may not be as much of a liability as we still see the economics making sense over the medium-term.

Moving away from coal, Aurizon continues to focus on its bulk business which has seen significantly higher volumes. Customers here include the likes of South32 (S32.ASX), CBH Resources and mineral resources with exposures split nicely across iron ore, base metals and agriculture (i.e. grain). All exposures that we continue to see demand for within the Green Economy.

So, why does it make sense?

We feel that it currently trades at the valuation of a pure fossil fuels play with little thought given to the active transition occurring. Management has a clear strategy for diversifying the business substantially through value add, as is indicated by the purchase of Newcastle and Townsville shipping facilities, which adds storage and ship loading capabilities along with potential for near-term organic growth prospects in the lithium and mineral sands space. Moreover the nature of the businesses, including long-contracted revenues (insulates the investor from fluctuations within the day-to-day gyrations of the spot market) and capital intensity (creates high barriers to entry) make it a reasonable risk-reward proposition.

With that, let’s quickly get to the numbers. EBITDA at $1.482bn AUD, statutory NPAT at $607m AUD, and FCF (Free Cash Flow) of $734m AUD. Interestingly, management’s guidance (and our expectations) are that we are likely to see $ 1.5bn for EBITDA. Granted, this is on the upper end of the guidance but we see no reason for this not to be the case.

Red Flags & Risks: This remains an annuity-like return stream for the discerning investor but the risk for capex blowouts remains the same as well as shorter term volatility within the coal and minerals market. Non-growth capex guidance for FY22 came in at $475-525m, however the question mark remains around the capex required for growth in the bulk side of the business.

In addition, China’s confrontational approach to Australian coal exports continue to be a headwind for the markets though this has been priced in and the company has made some headway in outlining a clear strategy for alternative markets (i.e. India and South East Asia).

Dividend Yield: A stellar 7.2% and we see this continuing to be the case over the long-term on the balance of probabilities.

APA Group (APA.ASX)

Despite this series mostly focusing on unloved businesses, APA came across our radar when they outlined their strategy for the next generation of growth in renewables and expansion into the lucrative US market.

First, a brief history and overview.

Listed in 2000, the Australian Pipeline Trust is an offshoot of AGL (AGL.ASX) starting with an interest in 7,000km of transmission pipelines. APA today owns and operates over 15,000km of pipelines along with 27,000km in Gas Distribution Mains as well as storage facilities, power stations, wind and solar farms. It accounts for the transportation of a quarter of gas used in Australia. Investors in the parent must be thinking of the irony. APA with a market capitalisation of $11.5bn AUD and AGL with its market capitalisation of $4.5bn AUD, a clear showcase of value creation vs. destruction by management teams. Nevertheless, we shall stop there given that we’ve previously posited that AGL looks relatively cheap.

We see significant tailwinds for the company going forward as the domestic market transitions toward renewables and energy security. Natural gas, in our view, will continue to be a key component of the energy mix going forward. Also telling is the continued expansion domestically of the East Coast gas grid in the Southern states, despite increased regulatory scrutiny on the domestic gas market. The transport agreement with Origin (ORG.ASX) has substantially de-risked this but the very manner in which management has gone about building the business and opportunity set is a great start. So, what does this entail? Firstly, it upgrades both the South West QLD pipeline and Moomba Sydney Pipeline and enables an 25% capacity increase via compression (as opposed to building new pipelines) with Origin coming in to take some of the increased capacity and locking in incremental revenue of $190m AUD over a 3-year period for the privilege of doing so.

We see similar capacity improvements across APA’s footprint along with continued optimisation of existing infrastructure. While many in the industry have faced significant headwinds due to regulatory intervention, APA’s astute management has found themselves continuing to operate in the overlooked niches (i.e. less regulated) where they can take advantage of asymmetric information in negotiation. On the flip-side, while it is likely that there will be additional construction of new import terminals by retailers, a policy likely to be encouraged by governments seeking to increase competition in the domestic market APA’s pipeline footprint makes it an attractive and cheaper alternative at least in the short-run.

Looking to the future, management’s vision is what we find to be the most attractive proposition. First, the potential expansion of the domestic footprint looking to capitalise on the close to $68bn AUD opportunity set that is Australia’s transition to renewables by 2040. Management estimates that pipelines and associated infrastructure is worth about $8bn, $40bn AUD in generation and storage and $20bn AUD in transmission. We see APA as a leading contender for the lion’s share of the pipelines and associated infrastructure with management potentially developing additional capabilities in storage and transmission. That being said, they may not be able to ascertain outsized returns outside the core capabilities during the initial stages. We also see the business as more likely to focus on wind generation as opposed to solar in order to prevent downward pressure on prices during the day.

Source: apa.com.au

Looking beyond Australia, management has indicated a desire to enter the US market where a significantly larger $2.5tn USD opportunity is up for grabs to 2040. This includes the potential for buying out existing pipelines or a utility company during the initial stages. With the enormity of the transition taking place, they may be able to buy out a non-core asset from an energy company before expanding further. While there is obviously risk there, we feel the APA has the track-record and the expertise to move into the space. In addition to looking at diversifying the pipeline usage, one interesting idea floated was the potential to use the existing pipeline infrastructure, initially the Parmelia Gas Pipeline, for the transportation of hydrogen with the potential to export at a later date.

With that, let’s get to the numbers. First half EBITDA came in at $823m AUD, down slightly (-2%) but expected due to Covid, and, concerning energy consumption for the full year, our view is that the figures will come in at a slight decline of -1.2% for the full year ($1.6bn AUD). NPAT at $290m AUD, an estimate and based on management guidance.

A fairly valued stock but still a reasonable buy, a strong well run defensive investment with growth attributes.

Red Flags & Risks: The biggest risk remains the aggressive expansion strategy that management is likely to implement (also happens to be the most attractive attribute). Debt is likely to be on the upper end of the metric allowances for a BBB/Baa2 credit rating should they proceed with an acquisition and, while the regulated return on equity allowances in the US should they proceed remains an attractive 10%, the risk of overpaying especially given the environment remains.

Over the long-run, an increasingly confrontational regulatory environment in the Australian market remains a threat along with increased competition.

This week we look at two more unloved securities, CIMIC (CIM. ASX) and Service Stream (SSM.ASX). Both of them have been perhaps less than pleasant experiences for long-standing shareholders. With that in mind, is it potentially a good time to buy? After all, both of them sit in a strong thematic (i.e. infrastructure and commodities).

CIMIC Group (CIM.ASX)

This is one company that most Australian investors would be familiar with (or at the very least its predecessor, Leighton Holdings) and not for the right reasons. Governance issues, most recently including bribing the then Deputy Prime Minister of Iraq to secure a pipeline contract, have certainly raised some red flags. This has also been exacerbated by construction project issues, boardroom politics and slowing demand in the mining services segment. The last of these is potentially where we see the most upside and why CIMIC is even on our radar; we remain of the view that (despite the last week’s price action) we are very much in the infancy of a multi-decade bull cycle in commodities which will undoubtedly see a pick up in demand. This is also not mentioning the increased investment in infrastructure globally. To give some context, CIMIC’s last guidance indicated that they have a pipeline of relevant future tenders to the tune of $475bn AUD (up from $285bn AUD).

Moreover, despite the definite red flags regarding governance, CIMIC does have a reputation of a strong balance sheet and an ability to undertake large scale contract-mining and construction projects that create an effective moat when moving to tender. Substantial economies of scale allow the company to take on multiple projects and diversify across market cycles, though this could have been executed better in my opinion. Breaking down revenue as it currently stands: 65% Engineering and Construction, 25% Contract Mining and 10% Services and Property Development.

Author: Sid Ruttala

We continue to see substantial upside given the pipeline in Australia (Eastern Seaboard) and across the Asia Pacific region (where they still operate as Leighton). At the current run rate, the business has already been awarded work in hand up to $10.4bn in Australia for 1H21. To put this into context, the full year of 2020 was $6.6bn. In my view, we will continue to see this pipeline grow, especially coming out of lockdowns as governments look to stimulate growth. On a more strategic level for the business, some key catalysts to come will be the potential divestment or listing of their services arm, Ventia (the brand that does the asset management and maintenance). Returning once again to the reflation thematic, the business’ cost of financing and their debt issuance in the European markets has seen them reduce their cost of financing from 2.2% to 1.9%; given that a significant portion of this is fixed (especially the longer term Eurobonds), any uptick in inflation should again act as a transfer to the shareholders.

On the negative side, CIM’s 50% sale of Theiss, now the largest contract mining services provider on the planet, was potentially a bad move despite the rhetoric around “introducing a partner to “support growth and diversification”. Never has anyone of reasonable business acumen come to the conclusion that the sale of a business to a hedge fund would be conducive for longer term growth. The other 50%, by the way, is now effectively owned by Elliott Management (i.e. a Paul Singer outfit). Singer is the man termed by the New Yorker as the doomsday investor, a rather apt elucidation in my view.

Arriving at the numbers, revenue came in at $1.7bn and NPAT at $208m, an apparent decline of 34%. However, stripping out the Theiss numbers (due to the sale), first half numbers were actually higher by about 1.5%. Furthermore, CIMIC has maintained NPAT guidance for 2021, $400-430m AUD, and our view is that this remains on the conservative side. Assuming that this is the case, one could easily see a medium term catalyst for a re-rate on the underlying security. I make this call based not only on the unwinding of the Covid impact (delay in contract awarding) but also on the additional pipeline assuming a conversion rate in line with their historic trend. Using that as a scenario, my expectations are that NPAT will come through marginally higher than guidance at $440m AUD.

Importantly for the dividend starved investor and assuming that they keep the current payout ratio of circa. 63%, it implies a dividend yield of 4.3%.

Red Flags & Risks: The biggest red flags with CIMIC, despite their engineering capabilities, strong balance sheet and scale, are the consistent governance issues. Company politics almost always seem to get ahead of them and there doesn’t seem to be a coherent strategy for longer-term growth. It’s the classic case of a good brand, product and technical capabilities with bad optics and overall management. The focus on PPP (Public Private Partnerships) is the right move but one hopes that they don’t repeat history with how they go about this aspect of the business.

My Expectations: Cheap! Especially given the broader thematic around infrastructure and the segments CIM operates in. Despite the less than stellar performance in the share price, our fair value estimate is about $35 AUD… the potential for 70% upside.

Dividend Yield: 4.3%, assuming a price $20.30 AUD.

Service Stream (SSM.ASX)

It has been a rather eventful year so far for SSM; rather cringeworthy for the shareholders but we are of the view that at these levels it makes for an interesting investment proposition. The share price having lost close to 50% since the beginning of the year in a bull market leaves us quite certain that long term investors aren’t happy campers. For those of you unfamiliar with the business, SSM engages in asset life-cycle services to the utilities and telecommunication sectors. That’s another way of saying they design, construct and maintain much of the infrastructure that you see around you, from your broadband to your gas connection. Given the nature of the industry they operate in, scale is potentially the most important factor in terms of long-term sustainability as well as consistently locking in longer term contracts.

On the first count (i.e. scale), the business has a history of acquiring in order to diversify, initially with Comdain in 2018 which has contracts across water and transmission. More recently, SSM has managed to get their hands on the entirety of the services division of Lendlease. Herein lies the problem with the recent price action. We will start by saying that we could see this situation being handled substantially better. It started with a leak from the AFR before shareholders got to find out and price action that saw massive selling pressure preceding the announcement. It was almost as though someone knew that there was a cap raise on the books… But now let’s have a look at the deal itself. The business will now acquire 100% of the services segment with an EV of $310m. Accounting for debt the purchase price is $295m and it would’ve bought out the business at an EBITDA multiple of 6.9x. Management guidance indicates that post-acquisition synergies should lead to a strong EPS accretion of about 30%, a rather nice target for the shareholder to think about.

So, does this make sense? In our view this further diversifies the business revenues, away from just telecommunications and utilities, to now broader capabilities in specialist design and construction. Not to mention a customer base which includes some of the largest public and private sector clients in Australia. Overall, it was done at a reasonable price and makes a great deal of sense from a strategy perspective. Personally, I would love to see them make a play for Ventia (mentioned above) which would make the group a force to be reckoned with but that is perhaps a pipe dream as the addition of Lendlease should keep the business busy for a while yet.

Returning to the bread and butter of the business, we like what we see. The contracts are reasonably long in duration and the business should have greater diversity in customers following the Lendlease acquisition. On the teleco side, their most important agreements are the NBN Unify and the Telstra field operations which are cumulatively worth $1.3bn AUD over an 8 year period. On the utilities side, the business has continued to secure contracts, the most recent being SEQ Water and NSW Operations.

Getting into the numbers, first half EBIDTA of $40.2m AUD and strong cash flow generation with working capital remaining at 1.3% of revenue. The business also maintained its payout ratio which, in retrospect given the acquisition, may have been a little on the ambitious side. Though Covid put a dampener on revenues, especially in the telecommunications segment with delays in client procurement, we should see continued recovery throughout 2021 with perhaps the exception of NSW. Interestingly, the acquisition of Lendlease should see combined revenue now at $1.7bn AUD and EBITDA of $120-125m AUD (management guidance). On the flip side, the company would have added close to $123m AUD in debt, manageable if things go according to plan.

Red Flags & Risks: The biggest risks come from the integration process and their ability to retain existing customers as well as find cost outs. Continued Covid related risks also persist, especially in NSW now, which does place stress on the telco segment.

My Expectations: When one considers the business’ current market capitalisation in comparison to the forecast group EBITDA, we think that SSM could be exceptionally cheap. We don’t expect payout ratios to stay within the current 50-60% range for another 12-24 months but, at the current share price, the investor will potentially lock in a yield of 10-12% over the longer term.

Dividend Yield: The most recent dividend was 0.025c per share but post-acquisition we expect (perhaps hope is more appropriate) that further distributions will be delayed for the year. After that, and using the current share price of 90c, a yield of 10-12%.

For those of you looking to get in, it may be worthwhile to hold out for below the SPP at 90c.

As markets across the globe continue to test record highs – whether it’s equities, property or even these new fangled digital assets that very few people seem to understand – many think there are very few modestly priced opportunities out there. This week we will be talking about a corner of the market that, ironically, hasn’t received any attention. Here we are referring to the media sector and will be looking at three small caps, two of them NZ based, that few would be looking at.

Author: Adam Wolf

These three companies have flown under the radar and might now be starting to look like attractive investments. All three of these companies are strengthening their balance sheets and will have opportunities to create value through capital management.

Sky Network Television (Dual Listed: SKT.NZX & SKT.ASX)

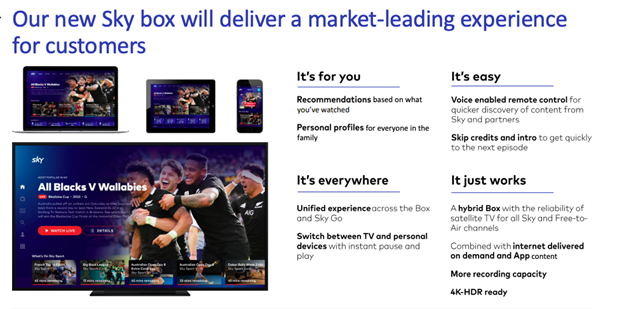

Sky Network is a broadcasting company based in New Zealand. They provide pay television services, media streaming services and, more recently, broadband internet services. Sky Network is essentially New Zealand’s Foxtel (those of you familiar will recognise the hardware, below) , providing people access to TV shows and, most importantly in New Zealand, rugby coverage. Over the years SKT has done everything but create shareholder value but we now see a possible turning point. They have made big changes to their management team, strengthened the balance sheet and have a significant cross selling opportunity.

Source: Sky

Sky Box

Sky box is NZ biggest pay television service with 566k customers. To get a Sky box you need to be a Sky starter member which costs $26 a month, from here you can stream these channels on any device and can add more channels, such as sport. Like Seven West Media (SWM.ASX), Sky Sport had rights for the Olympic games and provided a much more comprehensive coverage compared to free to air coverage; this would have been a big tailwind for Sky box customers, specifically increased sales of the sports package. Sky Sport also has exclusive rights for All Blacks and Super Rugby games, a huge draw card in NZ. Sky also became the owner of global streaming app Rugbypass which has a reach of over 40m people a month.

Source: Sky

Broadband

Sky Network’s latest venture has been establishing a broadband service to provide households across NZ with high quality broadband. The broadband offering is a big value add and a huge cross-selling opportunity. The pricing structure will favour existing Sky customers at $80 a month. SKT is aiming to provide broadband to at least 8% of Sky box customers; if they achieve this it will add approx. 53m of ARR to SKT (that’s using conservative estimates). Sky made a strategic partnership with Vocus New Zealand to provide the internet network, with Vocus providing technical expertise and the network backhaul.

Improving Balance Sheet

Earlier this year SKY retired $100m of debt using existing cash reserves; this will increase bottom line earnings by about $5m. They have also been divesting assets. They sold their OSB assets (outside broadcasting) and are in the process of selling two out of three of their site buildings located in Mt Wellington, a smart move given the shift to working from home. These divestments should build a decent net cash position on SKT’s balance sheet.

Personnel Changes

SKY has changed up their management team, something that can really turn a business around especially in the microcap space. They have appointed Keith Smith to the board. Smith is chairperson for Goodman Group (GMG.ASX), one of the best performing REITs on the ASX. They have also appointed the Chief Commercial Officer, Sophie Moloney, as CEO. In addition, they have appointed a new Head of Investor Relations while Andrew Hirst has stepped into the interim CFO position as they look for someone permanent. Sky is in need of a big turnaround and the company looks to be heading in the right direction after these executive changes. They are now heading into a significant net cash position and are now debt free; the new management team should have a strong balance sheet to create significant shareholder value.

Capital Management

Given that Sky should be entering a huge net cash position, management will have some important capital management decisions to make and, with FY21 results released at the end of the month, we should have more clarity as to what they will be doing. We see a share buyback as the best way to return capital to shareholders, as opposed to dividends, given the share price is close to an all time low. Sky could retire a significant amount of shares for a small consideration. At a share price of $0.15, Sky can buy back more than 10% of the shares on issue for less than $30m.

Thesis

Sky has been unloved but we can see SKT being a great turnaround story. They have a fresh management team and, after they finish divesting their property portfolio, they will have a huge net cash position which can be used to drive the share price through share buybacks. They are currently sitting on an EV of around $230m (this does not include the sale of their OSB and property assets) and their guidance for FY21 is approx. $170m EBITDA which would put them at an EV/EBITDA of circa 1.35x, a figure that seems too good to be true for most investors. Another key development is that SKT has received a number of approaches around potential transactions. Sky has appointed Jarden as an advisor for these matters and we wouldn’t be surprised to see some corporate action here given how cheap SKT shares are at the moment.

Seven West Media (SWM.ASX)

Seven West is a national multi-platform media business based in Australia. SWM has had a great first half of 2021; they won 12/24 weeks for total viewership and this doesn’t include their Olympics coverage. SWM secured the rights to broadcast the 2020 (2021) Tokyo Olympics, Paralympics and the Winter Olympics in February next year. SWM has been shoring up their balance sheet and, on the back of the lockdown and Olympic tailwinds, we believe they are well positioned to deliver significant shareholder value.

Source: SWM company filings

Olympics

SWM has been a big beneficiary of the recent lockdowns. They had the rights to broadcast the Olympics, which will be the biggest digital event of the year, and with so many people in lockdown the Olympics were drawing in huge viewership. As well as this, brands are investing more in TV advertising as a result of lockdowns. They grew their 7 Plus user base from 6.4m to 9.2m, a 43% increase. On the back of this user growth, SWM will have the opportunity to run targeted advertising campaigns as well as maintain the user base with more sporting events to come. In February next year Seven will be broadcasting the Winter Olympics which, while not as big as the Summer counterpart, will have another bumper effect on 7 Plus users.

Google and Facebook Deals

SWM has recently signed deals with Google and Facebook. The agreements bring the premium news content Seven produces from newsrooms across Australia to Facebook and Google. In their most recent trading update SWM said they expect their digital earnings to contribute $60m of EBITDA for FY21; with these deals in the bag they should add around $60m of incremental revenue in FY22.

Capital Management

Seven have been focusing on cutting costs, reducing debt and divesting non core assets. They achieved a $35m cash saving from the Olympics, existing content agreements and Cricket Australia. They have been retiring huge amounts of debt ($195 m in the second half to date) with more repayments to follow, substantially reducing their interest payments. They have reduced Net Debt from over $400m to approx. $275m. SWM have sold their WA newspaper business, Pacific newspaper business and their Osborne Park facility for $75m. SWM have strengthened their balance sheet position significantly and can now start to think about returning capital to shareholders, whether that’s through dividends or share buybacks remains to be seen.

Source: SWM company filings

Thesis

SWM have been a big winner from the latest lockdowns and benefited significantly from having Olympic coverage, growing their user base substantially. They have the winter Olympics next year and the Ashes at the end of the year to hopefully retain users. The management team have been very conservative and are focused on reducing net debt. SWM will soon be in a position to resume paying dividends and pursue M&A opportunities. They are trading at an EV/EBITDA of circa 4x. When compared to NEC (as above), Seven West looks like a far better opportunity with more upside.

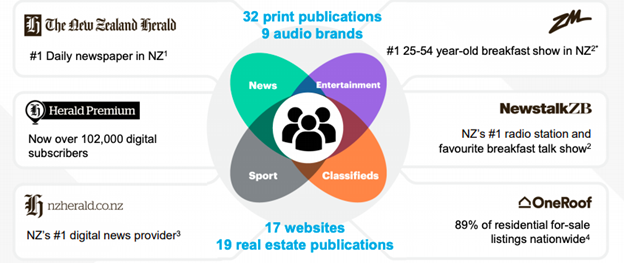

NZME (Dual Listed: NZM.NZX & NZM.ASX)

New Zealand Media is one of the biggest media companies in NZ. They boast the number one newspaper and have huge market share in all aspects of media including news, audio brands, radio stations and real estate publications. This company has been a quiet performer that has slipped under the radar. Yes, the newspaper industry is dying but NZME have been monetising their digital assets and gaining digital subscribers to more than compensate for this.

Source: NZM company filings

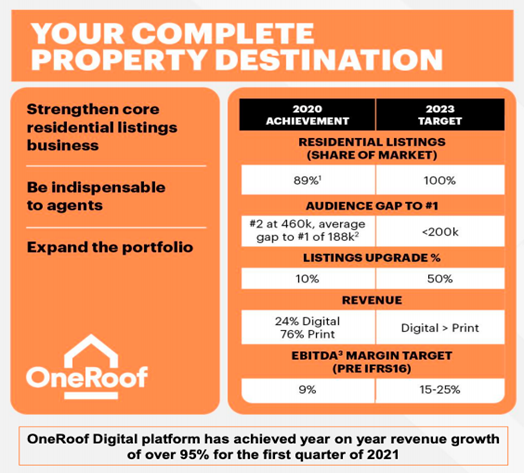

Real Estate – OneRoof

Unlike Australia, NZ has no truly dominant online players in property listings. NZM’s OneRoof is the number one residential listing site in Auckland, it has the potential to replicate the Australian success of Domain and REA Online in the NZ market. OneRoof is NZM’s hidden gem; they have been doubling their revenues. 89% of NZ residential properties for sale are listed on OneRoof. NZME are aiming to provide a complete property destination and are targeting an EBITDA margin for this segment of 15-25%. A business like this would typically trade at much higher multiples than what their parent NZM is trading at.

Source: NZM company filings

Strategy

As mentioned, NZM’s print business is declining (as expected) but they have been aggressively cutting costs to maintain margins through a workforce restructure. NZM are in the process of selling their ecommerce platform, GrabOne, which could push them into a net cash position. They are focusing on converting their customers to digital subscribers which is not only cost effective but gives them an opportunity to add value. They are growing their audio brands and realising their opportunity to become the leading property listing platform in NZ through OneRoof. Their strategy doesn’t require any significant capex but if a value accretive acquisition opportunity were to come about they will consider it.Dividend PolicyNZME intends to pay 30-50% of Free Cash Flow in dividends subject to being within its target leverage ratio and having regard to NZME’s capital requirements, operating performance and financial position. The target Leverage Ratio of 0.5 to 1.0 times rolling 12 month EBITDA. NZM’s leverage ratio was 0.6x in H120 and we expect it to be within the range in FY21, allowing NZM to resume paying dividends. In CY2020 NZM’s free cash flow was around $40m (excluding government grants); if they were to pay 30-50% of this in dividends, their yield would be 6-10%.

Thesis

The thesis here is fairly simple. NZME are the market leader in news coverage in NZ, they have huge market share in all areas of media and are best positioned to be the market leader in residential home listings through OneRoof. They run a very profitable business, recording $67m of EBITDA in CY20. They have over 2.4m digital monthly users but only around 50k are monetised. Assuming they execute their strategy in growing digital customers and monetising them, they look like a steal in the current investment climate. They are trading at an EV/EBITDA of about 3.1x (which will be lower once they have sold GrabOne) with a Free Cash Flow yield of 21.5%, they present a great value opportunity and are likely to resume dividends this financial year.

All three of these media companies are cash generative companies going through structural changes and are focused on strengthening their balance sheets. Through good capital management decisions these companies can create significant shareholder value. The market will take time but it will get it right.

Disclaimer: SWM and NZM are both currently held in the TAMIM Australia All Cap portfolio.

Author: Ron Shamgar

Author: Ron Shamgar

Floated in 2010, Aurizon has certainly seen ups and downs over the past decade. Before we get to the details, a brief overview of the company. Originally known as QR National, the company was established in 2004 bringing together Queensland Rail’s coal, bulk and containerised businesses. It grew by acquisitions over the following decade, expanding nationally and taking over Australian Rail Group and CRT, giving it a footprint across NSW, Victoria and WA. To put it simply, the company provides design, construction, overhaul, maintenance and management services to the mining industry with the bread butter remaining the Central Queensland Coal Network (CQCN). Given the loss of appetite with regards to coal and fossil fuels, the business has seen significant headwinds since IPO. With the likely long-term decline in its traditional business, it may seem surprising to many that we would even consider it. However, it must be viewed as a business in transition.

Floated in 2010, Aurizon has certainly seen ups and downs over the past decade. Before we get to the details, a brief overview of the company. Originally known as QR National, the company was established in 2004 bringing together Queensland Rail’s coal, bulk and containerised businesses. It grew by acquisitions over the following decade, expanding nationally and taking over Australian Rail Group and CRT, giving it a footprint across NSW, Victoria and WA. To put it simply, the company provides design, construction, overhaul, maintenance and management services to the mining industry with the bread butter remaining the Central Queensland Coal Network (CQCN). Given the loss of appetite with regards to coal and fossil fuels, the business has seen significant headwinds since IPO. With the likely long-term decline in its traditional business, it may seem surprising to many that we would even consider it. However, it must be viewed as a business in transition.

Despite this series mostly focusing on unloved businesses, APA came across our radar when they outlined their strategy for the next generation of growth in renewables and expansion into the lucrative US market.

Despite this series mostly focusing on unloved businesses, APA came across our radar when they outlined their strategy for the next generation of growth in renewables and expansion into the lucrative US market.