This week brings us to the last in our series on the search for quality dividend yields with Cromwell Property Group (CMW.ASX) and Worley Ltd (WOR.ASX) rounding out our journey.

Cromwell Property Group (CMW.ASX)

Given the headwinds faced by Australian office demand, in many ways catalysed or at least accelerated by the pandemic, it may sound surprising that we would consider this particular business. However, given the current valuation, this may prove to be a surprisingly solid investment proposition. First though, a little context around the business.

Listed in 1998, Cromwell tells the story of a great Australian success. Currently operating in fifteen countries and managing a total of $11.8bn in AUM. The core strategy has been to avoid highly priced office assets in CBD markets, opting instead for more reasonably priced and higher yielding secondary markets. Many of you may be more familiar with the business for all the wrong reasons though, with FIRB (Foreign Investment Review Board) stepping in to block a takeover and the CEO Paul Weightman retiring (rather conveniently) after 22 years in the business. A situation not helped by headwinds resulting from Covid and a downgrade in distribution guidance. A rather unloved proposition by the market with the share price trading at 88c at the time writing (from a pre-covid high of $1.23).

So why does this make a reasonable proposition?

Author: Sid Ruttala

Firstly, the valuation. We feel that the risks associated with the fall in office space may be a touch overdone. While it is true that bargaining power is much more to the advantage of the renters, with an NTA per share sitting around the $1.00 AUD mark, even the worst case scenario associated with rental income cannot substantiate the current valuation (remember the 88c share price, for a market cap of about $2.3bn). It is the profile of the tenants that we feel the market is not properly considering, with 40% accounted for (in terms of income) by the government and a further 15% accounted for by Qantas, who are on a 15 year lease).

Secondly, we feel that the downside risks to office space are currently overdone. It is true that there is an increased tendency to go towards flexible work or at least office hours and part-time work but there still remains a space for the traditional office environment. One could, for example, argue that in the 1990s (during the initial stages of the dotcom era) office space would have faced substantially higher headwinds given the move towards part time work and higher structural unemployment. This time around we feel that the nature of the fall in demand and unemployment (i.e. Covid-related) is more transitory and the economy will see a faster recovery in employment (and thus demand for office space) than in the past. Something which we, again, feel the market is discounting in its valuation.

Thirdly, we arrive at the management and boardroom drama. The business has refreshed its board and management ranks over the course of the last financial year. Included among the fresh faces are a new CEO in Jonathan Callaghan (former head of Investa) and Gary Weiss (of great pedigree having served on the boards of Westfield and Premier).

With that, to the numbers. Statutory profit was up 73.5% to $308m, while underlying operating profit was down by 13.1% to $192.2m. Rather messy numbers on face value but one also has to strip out one-off items, including the sale of Northpoint. Adjusting for this, the business’ operating profit was up 140bps.

So, why does it make sense now?

Quite simply, the current price. Despite the potential for continued lockdowns across her major markets, with NTA at 1.00 AUD, this seems like a good investment proposition. This, along with a seeming turnaround as a result of the change in management and the opening up (though it may not feel like it in the short-run for many of you living in lockdowns) of the economies, makes for an interesting proposition when the dividend is also considered.

Red Flags & Risks: Put simply, debt on the balance sheet. With an average weighted maturity of 3.2 years and 42% gearing, this component remains the biggest risk on the balance sheet. We would ideally like to see management locking in longer duration, even at the risk of higher debt-servicing costs.

Dividend: 8% dividend yield. Expecting this to grow by 10% in 2023.

Worley Ltd (WOR.ASX)

Coming to the last stock of the series, we look at Worley Ltd. Another engineering and services business (we have previously spoken about CIMIC and SSM). Another unloved business that we feel that the market may be wrong about.

For those that are less familiar with the company, a little context. Simply, Worley provides engineering and professional services to the oil, gas, utilities, mining and infrastructure sectors. Most Australian investors (if you have had previous experience with the company) would see it as driven primarily by hydrocarbons given that 75% of the businesses revenues used to come from that segment. Indeed, we feel that this may be the reason why, like much of the energy sector in general, the market continues to discount the business. However, WOR’s rather smart acquisitions, including Jacobs ESR, recently have seen this reliance come down significantly. Hydrocarbons now accounting for 52% and chemicals (previously accounting for 6%) increasing to 23%.

In addition, the business has global scale. Operating in over fifty countries gives WOR a scale that is difficult to replicate. Moreover, given that most of the contracts are of a cost-plus nature, the risk from project delays and cost overruns (which are the most significant risks to the sector) remain minimised.

So, why does this make a reasonable proposition?

Again, returning to our commodities thesis, we stand firm that we are at the infancy stages of a multi-decade secular bull cycle in commodities. However, for the more conservative investor that wants to take advantage as well as gain exposure to thematics such as the transition to green energy, we feel businesses like Worley may be a more reasonable option (as opposed to paying egregious valuations for end producers). For the more impatient, one metric that is of particular importance is that the backlog in work is $14.5bn AUD as of March 2021 (a notable increase from $13.5bn at the end of December). In other words, we know the business has significant and sustainable cash flows from its traditional footprint over the short-to-medium term. This is important while WOR focuses and uses it to advance its longer-term ambitions, including sustainability and green energy in particular. One other metric that might be of interest is the fact that the global market for sustainable design is approximately $4.5tn USD, of which WOR’s addressable market share is 10-20% (or $900bn USD). For decarbonisation, this is around $1.5tn USD with an addressable market share of 3-5%. To put this in a little more context, the current revenues for Worley are $10bn AUD.

With that, numbers! EBITDA was down 25% to $649m, operating cash flow down 24% to $533m AUD. These may seem like rather lacklustre numbers but context is key here. We feel that this is a one off (importantly, revenues remained rather stable) with Covid related impacts the main driver and, accounting for the work backlogs, we should see this return to historic levels (assuming normalisation) within FY 2022. Moreover, the business has been deleveraging with Net Debt/EBITDA coming down to 1.9x.

Red Flags & Risks: Covid continues to be the biggest threat to the business with the situation in China and the Delta Variant creating broad risks.

Dividend: 4.7%, expecting double digit growth over the next 24 months.

Disclaimer: CMW is currently held in TAMIM’s Listed Property portfolio.

This week brings us to the second to last in our series on the search for quality dividend yield, looking at Bapcor (BAP.ASX) and G8 Education (GEM.ASX).

For one thing, the auto parts market in Australia and New Zealand remains a highly fragmented industry with BAP being a leader in consolidating across the space. Its size not only gives it economies of scale but significant buying power and the ability to allocate inventory in a manner hard to replicate by smaller scale competitors. Moreover, the take up of electrical vehicles remains in its infancy across BAP’s major markets (i.e. new car sales with no internal combustion engine currently make up less than 1% of the market) and effectively represents a rounding error within existing Australian fleets (which is what is relevant at least in the short term). This aspect gives the business enough lead time to transition towards EVs and spare parts within that market in addition to its ICE footprint. One disclaimer here is that EVs typically have fewer moving spare parts; we expect volumes to be an issue over the longer run though certain niches and non-specific categories to be consistent (e.g. windscreen wipers or lighting).

Author: Sid Ruttala

Moreover, the segment in which Bapcor operates is in our view quite defensive given that, unlike new car sales, the market for spare parts tends to be more resilient and less driven by consumer discretionary income on the downside. While on the upside stagnant wage growth perversely produces a tailwind given the likelihood of consumers sticking to their existing vehicles and buying second hand in preference for new purchases. On the upside, Covid created a catalyst for the business in two ways, one transitory and the other likely to stay into the medium term. The first is the continued government stimulus measures which saw consumers opt towards upgrading existing cars and the second being the more longer term likelihood of domestic travel in preference for international as the world continues to battle with the Delta variant (i.e. elevated domestic travel). Indeed, this is reflected by the average age of on-road vehicles. There are currently more than 14m vehicles in circulation with an average age of greater than 5 years.

With that context let’s get to the numbers! Revenue was up 20% to $1.763bn, EBITDA up 20.8% to $280m and NPAT up 46.5% to $130m AUD. Arriving at the juicy and all important part, the metric that we feel most relevant given the capital intensive nature of the business, the requirement for inventory. ROIC came in at 11.6% (up 2.31%). Leverage also continues to be managed conservatively, standing at 0.7x debt to earnings (flat).

Red Flags & Risks: Continued lockdown measures and related unemployment numbers provide substantial risks by decreasing the distance driven. The risk of online sales for non-essential parts could also act as a long-term headwind for the business though management has been investing into its omnichannel strategy. At a PE of 22x the business is also pricey.

Dividend Yield: 2.6%

This is, however, a dividend growth story and we expect them to grow in the high single digits.

G8 Education (GEM.ASX)

This is a business that continues to be deeply unloved by the market, never quite recovering from the Covid-related sell-off as uncertainty continues to persist within the broader childcare segment. Before delving further, a brief summary of the business. G8 Education is a childcare provider that currently operates around 500 facilities across the nation. Its model was primarily acquisition driven thus far, buying smaller privately owned operators within the space at a multiple of 4x earnings and issuing debt/equity at lower multiples than acquisition. A smart strategy for the time and allowed it to grow EPS in the high single/low double digits through its initial growth phase. On the flip side, this has also meant that management operated it along the lines of a listed private equity type model, stripping out costs in preference for high payouts and service quality.

As can be imagined, Covid and the related lockdowns turned out to be significant headwinds for the business. The firm cancelled dividends through last year. With that in mind, it may be surprising that we would consider GEM, but here is the flipside. G8 operates in an industry that should see significant tailwinds from a policy and demographic perspective with a growing population of 0-5 year olds and government support for the sector. Currently, around 60% of childcare costs are subsidized at the federal level which continues to increase thanks in no small part to Australia’s short election cycles. And, with an aging demographic, we feel that this is one area where there is broad policy and economic consensus as childcare will be increasingly crucial in boosting productivity and participation rates amongst the half of the population taking on primary care responsibilities.

Given the above tailwind, we believe that the business has hit critical scale to focus more on organic growth as opposed to its historic strategy (many of you may be familiar with ABC Childcare and that particular debacle in the GFC). Here is where we feel that management can add the most value, especially within the context of competition from the not-for-profit sector and the highly fragmented nature of the industry. There is scope for improvement in improving quality of delivery and balanced cost outs especially through the implementation of smart-rosters, reduction of direct consumables (which make up about 10% of the cost base) as well as better negotiation of lease agreements. We will continue to watch those metrics. From a dividend perspective, given the fiscal incentives provided by the government during lockdowns we feel that it was a good move to suspend on an interim basis but expect reinstatement through 2022.

Now, let’s get to the numbers (which will be in comparison to 2019, as opposed to 2020).

Revenue was down 2% to $421m, EBITDA down 6.1% to $102m, NPAT up 83.1% to $25m AUD. Honestly, quite messy numbers but the metrics seem to be stabilising across the business given the significant 244m loss in 2019. Moreover, with management raising equity capital in 2020 and retiring all its existing Net Debt, we feel that the worst of the turbulence is now behind them. Liquidity remains strong with undrawn facilities amounting to $400m.

So, why does it make sense?

Quite simply, the current price. Despite the potential for oversupply in the market, we feel that the sell-off is overdone. Especially when considering a likely stabilisation in the business and, as the population continues to get vaccinated, we should hopefully see lockdowns ease heading into next year. We also see dividends coming back in CY22 and, assuming previous payout ratios, with the reduction in leverage it gives investors the potential to lock in an approximate 4% yield with the potential for longer-term growth given the tailwinds in the sector.

Red Flags & Risks: Given the centrality of subsidies to the sector, the business remains uniquely exposed to any changes in government policy. Continued lockdowns and oversupply also remain key threats in the short-to-medium run.

Dividend: 4.1% (expected) dividend yield, assuming continued recovery into next year.

Disclaimer: BAP & GEM are currently held in TAMIM portfolios.

This week we will be talking about one of our three pillars and a key theme in our Global Mobility portfolio; the pillar centred around electrification of vehicles and a stock we believe is well-positioned to capitalise on the significant increase in lithium demand.

Author: Adam Wolf

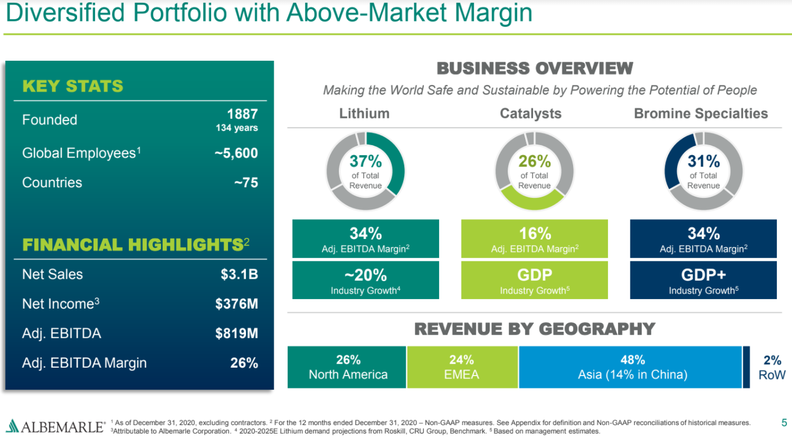

This year we have seen a lot of action in the lithium space, with the price of the alkali metal doubling and stocks like SYA and VUL seeing 1000%+ gains. We also saw the likes of BMM and CHR surge 250% after listing on the ASX. The company in question today is Albemarle Corp, listed in the US and trading at a $30bn market cap. Unlike a lot of the lithium stocks you come across, Albemarle is involved in multiple projects that are already producing lithium. They are the largest producer of lithium in the world.

Albemarle Corporation (ALB.NYSE)

Albemarle is a global specialty chemicals company based in the US. The company operates through three segments: Lithium, Bromine Specialties and Catalysts. The Lithium segment develops lithium-based materials for a wide range of industries including the manufacturing of the lithium ion batteries used in electric vehicles. ALB’s Bromine Specialties segment is focused on bromine and bromine-based business, which includes products used in fire safety solutions and other specialty chemicals applications, while their Catalysts segments are used in the downstream oil process to refine oil. ALB controls the strongest vertical position in the lithium industry; they have the technical expertise for both processing lithium and specialty product manufacturing.

Source: ALB company filings

Source: ALB company filings

Lithium is the primary component of lithium-ion batteries (LIB), which are rapidly gaining traction due to their wide applicability in energy storage solutions, in particular solar and wind energy projects, and the strong demand in the electric vehicle (EV) sector.

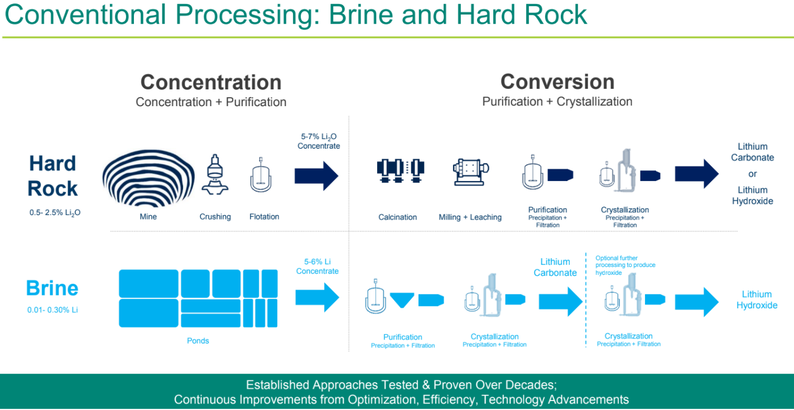

Lithium is very difficult to process and requires significant capex on necessary infrastructure to produce and manufacture it into specialty products. Data from Benchmark’s Lithium Forecast shows a projected annual lithium supply deficit of up to 225,000 tonnes in North America and 500,000 tonnes in Europe by 2030. To incentivise the right amount of investment in new mines there is going to have to be a sustained period of elevated prices. Bringing deposits into production is a time consuming process and can take years to undertake all the feasibility studies and actually construct a mine. Lithium deposits can either be produced from brine or spodumene rock production. Brine production is far cheaper and significantly more environmentally friendly.

Source: ALB company filings

Our outlook for robust lithium demand is primarily predicated upon increased demand for electric vehicle batteries. Albemarle produces lithium from both salt brine deposits in Chile and the US and hard rock joint venture mines in Australia.

Battery Innovation Center

Recently ALB completed their Battery Innovation Center in North Carolina, the centre will enable ALB to research new materials and processes and incorporate them into battery cells for performance testing. With this new resource, ALB will be well equipped to optimize their lithium materials for a drop-in solution that helps them deliver high-performing cost-effective batteries for customers in the rapidly growing electric vehicle market. ALB isn’t like any other lithium company that produces the concentrate and sells it through off take agreements; they are a fully integrated company from the production of the metal to manufacturing of the battery and are innovating their end solution.

Bromine

Albemarle is also one of the world’s largest producers of bromine. Bromine is used as a flame retardant that provides properties in order to keep our electronics safe. Bromine will be a winner from the transition to 5G, a thematic that we also have exposure to in the Global Mobility portfolio. The shift to 5G relies on printed circuit boards to transmit signals, all the materials involved will need fire retardants like bromine to keep consumers safe.

Why Albemarle?

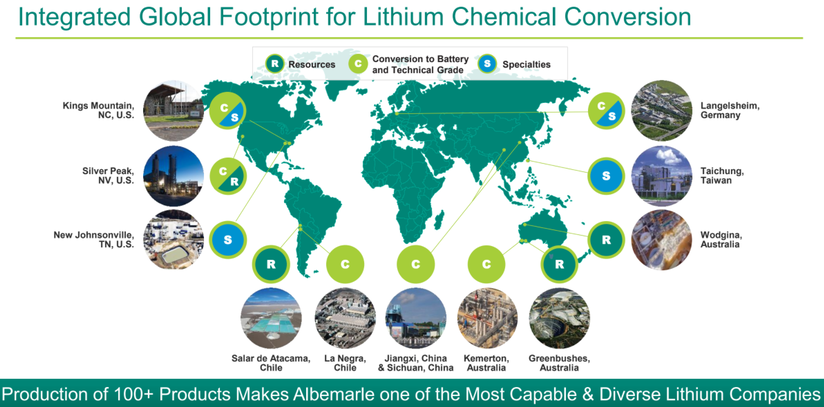

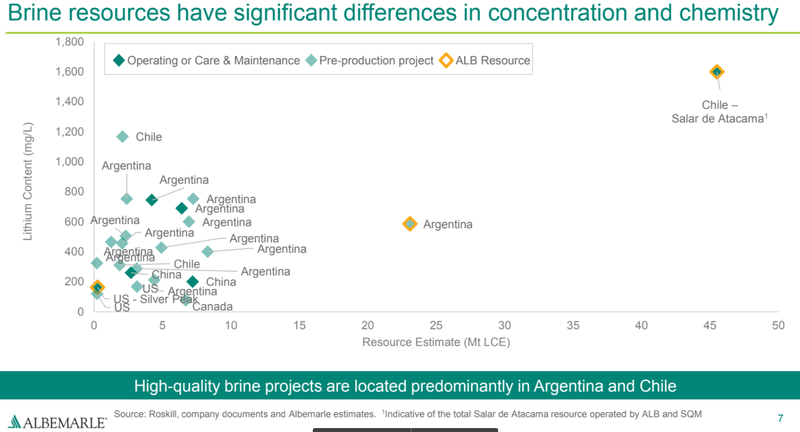

Many people would look at ALB and conclude they are an overvalued stock. But! We believe their technical expertise and the runway for lithium more than justifies the premium. Unlike in other mineral industries, ALB has been able to establish a dominant position in the lithium market due to their technical expertise in processing, allowing them to achieve significant economies of scale across their operations. ALB has a lithium footprint spanning the globe covering key markets. They have multiple joint venture interests in producing lithium projects; both in South American brine projects as well as interests in rock projects in Australia and China, which is a low cost jurisdiction. They also have production plants in Germany, giving them a fully integrated supply chain and access to the car makers in the heavily environmentally mandated EU jurisdiction.

Source: ALB company filings

ALB is on track to produce 125k tonnes of lithium hydroxide this year and has interests in a number of advanced projects in Australia, America and China which will head into production over the next few years as part of ALB’s stage 3 and 4 plan. They are aiming to be producing 450k tonnes of lithium hydroxide per annum. To put in perspective how big that is, Vulcan Energy are currently conducting a DFS on their brine projects in Germany to produce just 40k tonnes per year.

Source: ALB company filings

There are many companies one could invest in to gain exposure to lithium but how many of those companies can say that they have grown their dividend for 27 consecutive years and are delivering over $800m of EBITDA at a margin of 26%? ALB is the clear leader in lithium production and processing, they have low cost brine projects in South America and they have the balance sheet to pursue their lithium strategy and are innovating the lithium ion battery. There are no other lithium focused companies that have the technical expertise and access to the cash and credit necessary to scale their operations. ALB recently sold their fine chemistry business for $570m USD and this will enable them to focus on their core lithium strategy, pursue more M&A opportunities, acquire more interests in lithium projects and invest further in their development processes.

We see ALB as a company that has significant leverage to the lithium upside but at the same time has other profitable businesses in their Catalyst and Bromine divisions. This enables them to return cash to shareholders while also funding their lithium operations without diluting shareholders like many pre-production lithium companies are doing. As mentioned, it takes years to bring a lithium project into production and a lot can go wrong in that time. ALB is already one of the largest producers of lithium and has high quality, proven and large scale projects. They are achieving significant cost benefits as a result of their technical expertise and vertical integration. ALB offers full exposure to the lithium product cycle from the ground all the way to the battery in your electric vehicle.

Source: ALB company filings

Using ALB’s estimates of future production, their lithium segment could be contributing well over $1.5bn of EBITDA to the business. It is worth noting that this is assuming their margins don’t increase as a result of lithium price appreciation.

ALB is a profitable company that ticks all the boxes for the investment focus of our Global Mobility fund. They will benefit from the increased production of EVs through their lithium operations, this increased production is effectively being mandated by governments around the world via green initiatives and targets, tax breaks and rebates. Regardless of your personal opinion on electric cars, it’s happening. While not quite the opportunity afforded by lithium, ALB will also be a winner from the rollout of 5G and IoT through their Bromine division. Rather than buying companies in the exploration stage, we are looking to buy and hold established players in the industry that have the skillset and the funding to capitalise on the rise of EV production. We see ALB dominating the lithium production and processing market while also expanding their scale through near-production projects and potentially via M&A activity.

Disclaimer: ALB is held as a long position in TAMIM’s Global Mobility portfolio. The TAMIM Global Mobility strategy seeks to to capitalise on the ongoing $7 trillion autonomous and electric vehicle revolution.

As can be imagined, the business was in the front lines during the Covid-related sell-off and, although the recovery has taken place, the market continues to significantly discount the business based on the prospects of continued lockdowns. Especially given a significant portion of her revenues come from the food service and QSRs (Quick Service Restaurants). However, management has been gaining momentum in inventory reductions and further streamlining of the business.

Author: Sid Ruttala

In terms of catalysts for the future, the business is focusing on specific niches including the premium market as well as private label product innovation. ING’s divestment of non-core assets, most recently its dairy feed supply business, is a good move in our opinion. The most important metric in our view are the margins, which have continued to increase with gross margins at 23.4% (compared to 19.6% in 2020). With that, let’s get to the numbers.

Revenue was up 5.5% to $2.3bn, EBITDA up 15.8% to $208m, NPAT up 26.9% to $100m AUD (this takes into account the change in accounting regulations, i.e. pre-AASB 16). Arriving at the juicy and all important part, cash flow conversion continues to be a stellar 102%. What is also pleasing to see is the 3-9 month forward cover when it comes to feed, with the likely continued volatility in both soy and wheat prices as well as the recent gyrations of the AUD.

So, why does it make sense?

Firstly, management has continued to maintain discipline in its balance sheet management. This business has deleveraged to around 1.2x from 1.8x and, with the business churning out great cash flows, we should continue to see reasonable dividends and dividend growth in future. ING’s agreement with WOW looks set to be renewed though we would like to see the finer details before making further comment.

Returning to our thesis around inflation, Inghams could also be seen as a hedge given its strategy to optimise the core and cost-outs (i.e. higher margins).

Red Flags & Risks: The biggest risk continues to be further disruption as a result of Covid, not only to the domestic market but also broader supply chain and export markets. Higher feed costs and biosecurity issues could potentially have disproportionate long-term impacts.

Dividend Yield: At current prices, ~4% with expectations of high single digit growth on an annualised basis.

Monadelphous Group (MND.ASX)

For those of you that have been tuning in recently, it may be obvious that we’re onto a thematic here. That is, businesses and industries in defensive sectors and/or those that are likely to be solid inflation hedges. Having acknowledged that, let’s get to another business that should see substantial tailwinds despite what the recent price action in the spot market may suggest. To summarise MND very quickly, they operate across two verticals: engineering construction and maintenance/industrial services within the resources and energy sectors. Yes, the business has started to diversify revenue streams into water, power and marine infrastructure to deal with the cyclical nature of the mining industry but as it currently stands over 73% of revenues are tied to the fortunes of the iron ore industry.

This is one business that has never quite recovered from the Covid related sell off – not yet recovering to the $16+ mark it was trading at in February 2020 – despite the recovery in spot prices and we feel that the market has overlooked the potential for continued growth. Before proceeding further a disclaimer that, despite the sell-off in ore prices from a peak of $222 USD/T to $156 USD/T at the time of writing, we remain long-term bulls when it comes to the price given the infrastructure pipeline globally as governments continue to spend in order to resuscitate nascent aggregate demand. It must also be remembered that even at these prices, it still remains a viable proposition for businesses to place additional capex (which is arguably what matters for MND). If anything, the tight labor market and wage inflation across the resources sector broadly is an indication that the sector continues to expand. Combined with our thesis around an oil price recovery to approximately $80 USD/barrel given supply constraints in US shale production, we believe that any turbulence in MND’s revenue streams should be compensated by continued recovery in the business’ energy sector exposure.

Before proceeding further, the numbers. Revenue up 18% to $1.953bn. Of this, the outperformer (as one could guess) was the engineering and construction division with a stellar 51% increase on pcp. Basis. EBITDA was up 18% to $108m and the all important NPAT was up 29% to $47.1m AUD. Of concern was the decline in maintenance and industrial services revenue by 7%. Nevertheless, going forward the company has secured a pipeline of $470m in renewals and extensions as well as a significant $100m in new contracts in oil and gas. As that particular market recovers we should see momentum building.

Ichthys Project Onshore LNG Facilities – MEC 2 Package – Bladin Point, Darwin

Source: monadelphous.com.au

So, why does it make sense?

Despite the jitters caused by the sell-off in ore prices, it must be remembered that the business is not as directly impacted given the contracted nature of the revenues and, with a continued recovery in crude, we should see substantial tailwinds feed on through for the business. MND continues to be pleasingly disciplined and targeted in securing new contracts. Should we be correct in our prediction of a secular bull cycle in commodities broadly, the business should continue to benefit substantially while not being as exposed to the gyrations of the spot markets (in terms of revenue streams).

Red Flags & Risks: The biggest risks for the company are centred in project delays and continued volatility in commodity prices. The business also operates in a rather competitive backdrop and investors have to pay particular attention to contract growth and retention.

Dividend Yield: 4.3%

Sidenote: Telstra (TLS.ASX)

Finally, briefly revisiting Telstra. We know many of our readers are or have been holders and I have previously written on the business in the Top 20 series. In this I mentioned that it was looking to be a potentially attractive proposition. Since then the market capitalisation of the business has gone up by circa. 15% so we thought it may be pertinent to see whether it remained a buy still. The questions posed related to where TLS is going in terms of the bottom line, we do prefer some vision for the future of the businesses we invest in after all. Below are the CEO’s recent comments on what he sees going forward:

“Thank you for your questions. FY21 was an inflection point for the financial performance of our business, with strong momentum in the second half leading to sequential growth in underlying EBITDA. We have confidence this momentum will continue, and we have provided guidance for FY22 underlying EBITDA in the range of $7.0-7.3b which represents mid to high single digit growth. There are three key drivers – (1) Mobile, for which we expect to see ongoing service revenue and EBITDA growth, (2) Enterprise, for which we expect revenue and EBITDA growth in FY22 across mobile, fixed and international, and (3) productivity, with a $430m cost out target for FY22. We are also focused on diversifying our growth across other verticals including in Energy and Health, while our investment in Foxtel is well positioned for the future following recent exceptional subscriber growth. We will communicate our strategy for the future at our Investor Day on 16 September 2021. This strategy will be firmly focused on continuing to improve customer experience, driving growth and leveraging the foundation and capabilities we have built through our T22 strategy over the last three years.”

Not bad Telstra, not bad.

Disclaimer: ING, MND & TLS are currently not positions in the TAMIM portfolio’s

This week we discuss a hidden gem on the ASX and one which we believe has the ultimate investment exposure in a Covid world. With the company only listing three months ago it is yet to receive much attention from fund managers and brokers, yet it is highly profitable and on an upgrade cycle. Find out which stock below.

Author: Ron Shamgar

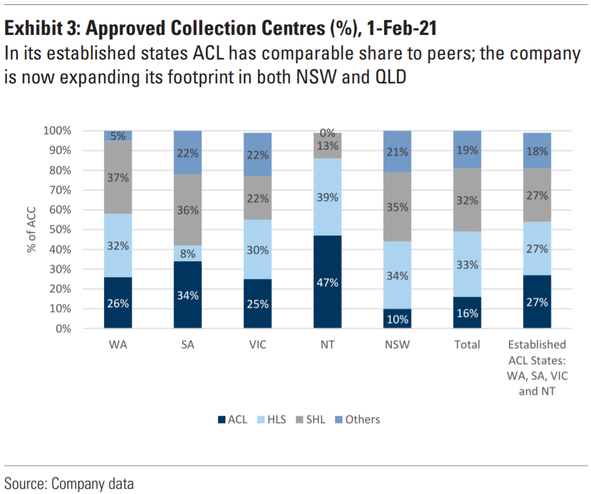

Australian Clinical Labs (ACL.ASX) is the third largest pathology provider in Australia. The pathology market is worth over $6bn annually and 80% of revenues are dominated by three main players: Sonic Healthcare (SHL.ASX), Healius (HLS.ASX) and ACL – with 16% market share. The industry is growing at approximately 5.4% per annum but Covid PCR based testing has added another layer of substantial and lucrative revenues.

Source: Goldman Sachs Equity Research

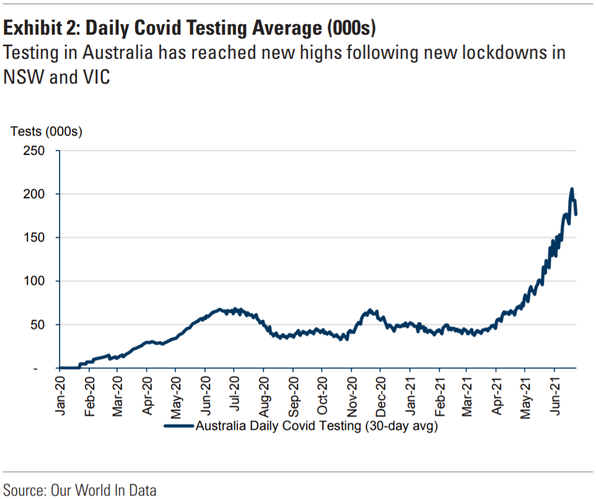

Now whether Australia reaches 80% or 100% vaccination rates, or whether we are in and out of lockdowns or completely open our borders – we don’t believe it matters for testing requirements. Whatever your stance on the situation, Australia’s Covid strategies and responses are fixated on case numbers. This means that, for better or worse, testing volumes should continue to stay elevated for a couple of years to come.

What gives us confidence in this statement is the high levels of Covid cases overseas, especially in countries where vaccination rates are high. Ongoing testing will be required for travel purposes, work related requirements, healthcare and staying on top of different strains of the virus that will undoubtedly evolve over time. More importantly, alternative antibody (antigen) testing methods so far appear to be unreliable in replacing PCR based methods. ACL are currently serving over ninety hospitals and are also running thirty specialist skin cancer clinics across Australia which are responsible for diagnosing over 15% of all reported melanomas. Hence ACL profits are sustainable for now.

Source: Goldman Sachs Equity Research

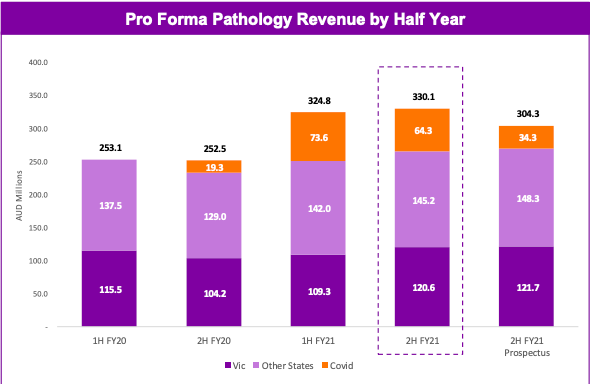

The company has significant momentum and is in the midst of a strong upgrade cycle that we believe the market is currently overlooking. FY21 prospectus forecasts were beaten by 5% on revenues (to $674m) and were over 20% ahead in the NPAT line (to $89m). Free cash flows are strong and the balance sheet ended the period with low levels of net debt ($65m).

Source: ACL company filings

All this should allow ACL to continue to make acquisitions, especially in NSW and QLD where ACL’s market share is still quite low. Unlike their larger peers, ACL should be able to make smaller acquisitions that make a meaningful impact on their bottom line. ACL’s past acquisitions have increased their presence throughout Australia and have provided significant synergies for the company by reducing operating costs and improving EBITDA margins. Watch this space.

The momentum behind the business was evident with 1H22 guidance upgraded significantly from prospectus forecasts. Revenues are now 22% ahead of the previous forecast and NPAT is a whopping 130% ahead at $53m. To put this in perspective, analysts previously had ACL earning $53m for the whole of FY22. Dividends are expected to be paid at 60%+ of profits, placing the stock on a 6%+ fully franked yield.

ACL has also invested significantly in their in-house tech and operates a national unified pathology system that allows the majority of tests, clinicians and laboratories to operate as one laboratory across the country. ACL’s unified pathology system enables operational benefits which include improved turnaround times and ability to handle demand peaks, national benchmarking to drive performance improvement and efficiencies and share innovations. Their system is a competitive advantage and has been a key factor in their ongoing and pivotal role in Australia’s Covid response. This system and the advantages it brings will serve them well if and when there is a decline in Covid testing.

Source: ACL company filings

Last year we successfully (and rather profitably) rode the wave of Covid winners in e-commerce and BNPL stocks. We see ACL as a similar beneficiary but on a more long term and sustainable level. Any slowdown in Covid testing should be replaced by increase in non-Covid business/testing resuming.

Source: ACL company filings

With SHL and HLS trading on 14-19x PE multiples, we see ACL – currently at 9x PE – as significantly undervalued. We believe that management’s FY22 guidance is conservative as was their FY21 guidance. They are assuming a sharp deceleration in test volumes and, as we said above, we don’t believe it will be quite so sudden. On the back of the conservative forecasts, we expect further upgrades through the year and further acquisitions to drive a rerate. An ASX300 index inclusion is also potentially on the cards. Our valuation is $6.00+ and ACL is currently one of our top holdings in both the Australia All Cap and Australia Small Cap Income portfolios.

Disclaimer:ACL is currently held in TAMIM Australian equity portfolios.

This is a business that continues to be deeply unloved by the market, never quite recovering from the Covid-related sell-off as uncertainty continues to persist within the broader childcare segment. Before delving further, a brief summary of the business. G8 Education is a childcare provider that currently operates around 500 facilities across the nation. Its model was primarily acquisition driven thus far, buying smaller privately owned operators within the space at a multiple of 4x earnings and issuing debt/equity at lower multiples than acquisition. A smart strategy for the time and allowed it to grow EPS in the high single/low double digits through its initial growth phase. On the flip side, this has also meant that management operated it along the lines of a listed private equity type model, stripping out costs in preference for high payouts and service quality.

This is a business that continues to be deeply unloved by the market, never quite recovering from the Covid-related sell-off as uncertainty continues to persist within the broader childcare segment. Before delving further, a brief summary of the business. G8 Education is a childcare provider that currently operates around 500 facilities across the nation. Its model was primarily acquisition driven thus far, buying smaller privately owned operators within the space at a multiple of 4x earnings and issuing debt/equity at lower multiples than acquisition. A smart strategy for the time and allowed it to grow EPS in the high single/low double digits through its initial growth phase. On the flip side, this has also meant that management operated it along the lines of a listed private equity type model, stripping out costs in preference for high payouts and service quality.

Source: ALB company filings

Source: ALB company filings

In an investment world that seemingly cares little about cash flow generation and debt, Inghams came across our radar as a business that generates great FCF, continues to reduce debt and operating leverage as well as sits in a reasonably defensive industry with good tailwinds. For those of you less familiar with the business, Inghams is one of the largest producers and suppliers of poultry and feed in the country. They count chains like McDonalds and KFC as customers as well as supermarkets like Woolworths. Going to the tailwinds, chicken meat consumption and demand continues to grow at a reasonable pace over red meat as the market continues to be more health conscious.

In an investment world that seemingly cares little about cash flow generation and debt, Inghams came across our radar as a business that generates great FCF, continues to reduce debt and operating leverage as well as sits in a reasonably defensive industry with good tailwinds. For those of you less familiar with the business, Inghams is one of the largest producers and suppliers of poultry and feed in the country. They count chains like McDonalds and KFC as customers as well as supermarkets like Woolworths. Going to the tailwinds, chicken meat consumption and demand continues to grow at a reasonable pace over red meat as the market continues to be more health conscious.