This week we continue our run through the Top Twenty by looking at the miners, beginning with BHP Group (BHP.ASX) and Fortescue Metals Group (FMG.ASX).

We remain of the view that the significant tailwinds for commodities in general will endure for some time yet given global impetus towards the green transition and fiscal expansion (which, despite roadblocks in the form of inflation, looks set to continue). We first published this view even before the recent Russian invasion of Ukraine and it has only been affirmed since. Further detail on this can be found here.

Perversely, the relentless upward pressure on the price of both WTI and Brent, despite jawboning from policy makers and the Biden administration, may in fact create a tailwind for base metals and commodities in general. Without going into too much detail, the price action not only increases global reserves (defined as economically retrievable oil) but also increases the economic incentives to speed up the energy transition (i.e. demand destruction). Even in the short-run we are likely to see tremendous momentum for iron ore (driven by demand for steel), coal (especially coking coal, steel again), copper (i.e. transmission and electric vehicles), uranium (i.e. nuclear power generation), natural gas (i.e. bridging power generation during the transition) and agricultural commodities such as potash (both fertilizer demand and uses in shale production).

With that, some price targets for the above categories over the next 12 months:

Those interested in how we reached these price targets, please don’t hesitate to get in touch.

Finally, we have seen rather disappointing price action from the yellow metal; accounting for the current geopolitical uncertainty, it could be argued that the shiny metal has shown meagre performance given its traditional status as a safe haven in times of uncertainty. Despite this and given the above prices and inflation implications (along with implications for real yields), we could argue that it may still be reasonable bet on the balance of probabilities. Price target: 2200 USD/Oz (this may seem optimistic for the more cynical amongst you given recent performance).

Note: We have intentionally left out some other crucial commodities (rare earths along with the likes of nickel, cobalt and lithium) given the group of securities being discussed discussed. We are looking towards the largest revenue streams for the companies in question.

BHP Group (BHP.ASX)

More than pleasing results from BHP with EPS of 211cps US (up +77%) and margin of 64%. Most importantly for the yield hunters, an AU $4.55 p/s dividend (estimated). For us, the company has seemingly learnt from its mistakes in terms of balance sheet discipline (many of you may remember the Capex bonanza during the peaks of the China-driven iron ore boom). The company has reduced net debt by 49% to $6.1bn US, though the payout ratio of 78% seems overly aggressive in our view. The market has seemingly rewarded the performance, the share price returning close to 20% since the beginning of the year.

Digging a little deeper into the strategy side, we maintain that the sale of the petroleum assets was a great move and allows the business to shift focus to core assets while the move into potash is rational, especially given reductions in global crop yields (we will see another long term tailwind here). On the sale front, we are certain that longstanding shareholders would be pleased given the performance of their scrip which has returned close to 50% since the beginning of the year. Looking at the segment breakdown, beats across all three major segments; Metallurgical Coal, Copper and Iron Ore. We were slightly disappointed with the EBITDA margins on coal but with a 71% margin on Iron Ore, this may be overlooked. Unit costs on the Escondida deposit of 1.2 USD/lb, well within guidance.

Red Flags & Risks: We were disappointed that the company has been rather slow in looking to new projects, especially in the copper space (has the company gone to the opposite end of the spectrum in terms of risk appetite?). The election of Boric in Chile adds a new element of risk for the Escondida mine, which remains the flagship project for the business, while headline price volatility based on newsflow from Russia could also see some risk.

My Expectations: Cost front continues to be pleasing and, while any short term peace talks with Russia could see some selling pressure in commodities, we still think the business offers a good risk reward given our outlook on prices across both iron ore and copper. For the dividend investor, certainly a better proposition for the financials. Still a hold with a price target of AU $63.

Dividend Yield: Assuming a share price of AU $51.41, then BHP has a great dividend yield of 8.2% (i.e. as expected).

Fortescue Metals Group (FMG.ASX)

The last time we wrote about this particular company we were at AU $22.26 and were of the correctly of the opinion that the business was too expensive (for those astute investors who then bought the stock close to $14 – well done). But, with the share price having bounced back to similar levels now (AU $21.66 at time of writing), it no longer seems so. What’s changed? For one, we continue to see disciplined management; the number that stands out here? Guidance of 180-185 mt shipments (this will be a new record on top of the one set last year) and 70% realisation of the Platts 62% CFR Index (this bodes well for discounts given historically lower grades). The addition of Iron Bridge, with its average 67% grades, should be beneficial in the long run for margins (i.e. lower grades and higher coking coal costs means higher discounts compared to peers whereas the opposite is true with higher average grades). In the long run, the company’s well touted ESG ambitions should make the business more palatable for bigger valuation premiums. These ambitions include carbon neutrality by 2030 and Net-Zero Scope 3 emissions by 2040 (something which we were concerned about given historic low grades).

With that, to the numbers. EBIDTA of US $4.8bn. Importantly (and rather pleasingly), gearing came in at 23% (given FMG’s history this is one metric that has been satisfying to see). The business continues to rapidly cut costs in order to keep up with peers, including BHP and RIO. Operating cashflow stands at US $2.1bn while the payout stood at 70% of NPAT.

Red Flags & Risks: FMG is a leveraged exposure to the iron ore spot price and Chinese growth. As such, the biggest risks will be a potential slowdown in Chinese growth, escalation in Covid related policies and property related slowdown (i.e. construction). While spot prices were certainly catalysed by sanctions on Russia, we still feel that any pullback, even in the most optimistic of scenarios around peace, will be short-lived.

Expectations: FMG seems to be ticking all the right boxes and, with Vale (VALE3.BVMF) still going through its own issues, we think that the medium to long term outlook for the price of ore remains promising. What must be watched however is China (to give some context about where they are in the cycle, the PBOC is the only outlier amongst major economies in terms of having an expansionary monetary policy). The price also remains somewhat at a premia compared to peers but this may just be a long-term investment. We remain fans of Liz Gaines.

Dividend Yield: The current dividend yield stands at an exceptional 8%, assuming a price of $21.66 AUD (as expected).

Disclaimer: FMG is currently held in TAMIM individually managed account (IMA) portfolios.

This week we will be writing about an underappreciated metal that is crucial to the energy revolution and shift to electrification. Regardless of your position on the timeframe, just about anyone could tell you that electric vehicles are the way of the future. The real question is do we currently have enough supply of the crucial commodities needed to develop and produce these vehicles on a mass scale?

The metal we are focusing on here is tin, an often forgotten commodity in the hype surrounding the incoming proliferation of electric vehicles. We will be covering two listed tin producers, the only two producers listed on “first world” exchanges.

Source: Elementos (ELT.ASX) company filings

Tin and Electric Vehicles

When a lot of people think of tin the first thing to come to mind is the tin can. However, tin is a key electrical contact in electronic circuits (solder), printed circuit boards and semiconductors, accounting for 50% of tin demand today. It is the electric glue connecting key components. Tin plays a role in battery chemicals, battery anodes, alloys and, obviously, the humble tin can (i.e. tin plate).

We are currently in the midst of a global semiconductor shortage like never before which has seen billions of dollars enter the sector in an attempt to rapidly close the gap. Yet, it seems that no one cares about investing in additional tin supply to meet this demand. Tin is commonly known as the ‘spice metal’ because a little tin is in virtually everything.

The main focus for tin is in the positive anode electrode of lithium-ion batteries, usually made from graphite on a copper foil today. Tin will also play a big role in renewable energy with solder ribbon being used to join solar panels. Current global consumption of tin is around 360,000 tonnes p.a. but the International Tin Association is forecasting a 60,000 tonne increase in demand by 2030 for lithium-ion batteries, a whopping 16% increase in consumption. That’s just accounting for electric vehicles.

Source: Rio Tinto (RIO.ASX) company filings

Tin Supply

As you can see, the demand for tin is seeing significant tailwinds. But what about the supply side? Tin deposits are few and far between, the pipeline of projects is underwhelming and the fact that there are only two listed Tin producers in the world says it all. There are two main sources of tIn: alluvial mines, usually found in places like Indonesia, and hard rock mines. Tin from alluvial mines is extracted from clays and is very low grade. Currently, half of our tin comes from these mines. Hard rock mines are much higher grade but most of the easy ore has been mined and finding new economically viable deposits isn’t easy given how hard it is to process. Mine disruptions due to the pandemic have cut supply from the 350,000t p.a. range to around 320,000t. With demand for tin forecast to skyrocket, we are staring down the barrel of a supply deficit for yet another EV metal. Right now there are four countries that produce ~85% of tin concentrate globally. This includes Myanmar and China, both of which are probably not sources the world can rely on.

Source: International Tin Association, 2021

There are some that argue that these prices for EV metals are unsustainable as they will make electric vehicles unsellable due to higher prices. An EV battery typically uses around 1.5kg of tin, which would cost $64.5 per EV. The price could quadruple from here before making a material impact on prices.

Metals X (MLX.ASX)

MLX is one of few listed tin producers in the world. Metals X owns a 50% equity interest in the Renison Tin Operation through its 50% stake in the Bluestone Mines Tasmania Joint Venture (BMTJV). Renison is one of the world’s largest and highest grade tin mines. It currently has about 120,000 tonnes of Proved & Probable Reserves of tin at a 1.4% grade. Renison is located on the west coast of Tasmania, approximately 15km north-east of Zeehan and has access to fully sealed roads to the Burnie port.

Over the past twelve months the mine has produced 8,452 tonnes of tin at an All-In Sustaining Cost (AISC) of $22,248 p/t. The mine is expected to ramp up to producing 10,000t p.a. and, with tin prices today hovering around $43,000 p/t, MLX’s 50% stake will bring in around $175m of EBITDA to the business.

MLX are also progressing the development of their significant growth opportunity in Rentails, a tailings stockpile accumulated from previous Renison processing, i.e. Ren(ison)tail(ing)s. Rentails is the second largest undeveloped tin deposit globally when measured by tin content in the mineral reserve.

Nickel Spinoff

MLX divested their nickel assets, including the Wingellina Nickel-Cobalt Project located in Western Australia and the Claude Hills Project located in South Australia. The assets were divested in the recent IPO Nico Resources (NC1.ASX) and MLX conducted an in-specie distribution of NC1 shares to shareholders. This divestment makes MLX a pure play tin producer, it is often a positive when mining companies sell off non-core projects, it usually means they have something really good they want to focus on pursuing.

Market Cap

Cash

Conv. note receivable +

Debt

EV

EBITDA Run Rate*

EV/EBITDA

$616m

$46m

$31m

$3.5m

$542m

$170m

3.2x

* assumption based on 10,000t p.a. production at current tin prices

Alphamin Resources (AFM.TSXV)

Alphamin Resources is a low cost tin concentrate producer from the Bisie Mine, a high grade deposit in Mpama North. This is on its mining license and it has an additional five exploration licenses covering a total of 1,270sqm in the North Kivu Province of the Democratic Republic of Congo (DRC). Alphamin is currently responsible for producing 4% of the world’s mined tin. They are sitting on a world-class tin reserve of 3.33m tonnes at 4.01% grade for 133,000 tonnes of tin.

Source: Alphamin company filings

DRC is home to some of the highest quality mineral deposits in the world, including the Matunda cobalt mine. The mining sector in Congo was ignited by Israeli businessman Dan Gertler and his partnerships with Glencore but Gertler’s deals were found to involve corrupt practices and saw him take advantage of the Congolese people. Congo has proven to be a tricky jurisdiction for many, however Alphamin have proven they can operate there with few issues.

Alphamin’s current operations at the Bisie Mine are on a run rate of yielding 12,000 tonnes of tin for Alphamin at a AISC of circa US $15,000 p/t. At current tin prices this puts Alphamin on an EBITDA run rate of over US $300m.

Source: Alphamin company filings

Mpama is home to multiple ore bodies that are currently being explored to add to Alphamin’s development pipeline. Their near-term prospect in Mpama South is currently being drilled out to upgrade its resources as part of further feasibility studies. The initial scoping study indicated that Mpama South could be producing over 7,000 tonnes of tin p.a., adding $180m of EBITDA p.a.

Market Cap

Cash

Debt

EV

EBITDA Run Rate*

EV/EBITDA

$1.45bn

$90m

$17m

$1.377bn

$300m

4.59x

* assumption based on production at current tin prices

Closing Remarks

Both MLX and Alphamin are trading at cheap multiples. Both are sitting on strong balance sheets (both in a net cash position). Tin deposits take time to bring to production and given that there are only two “first world” listed tin producers in the world, you would think that Alphamin and MLX might trade at higher multiples due to the sheer lack of quality listed tin companies. Tin prices have more than doubled over the past year and, with EV demand stepping up continuously, it’s easy to see prices soaring higher. Both MLX and Alphamin are bringing in plenty of free cash flow at current prices and have practically paid off all their debt which means they can return capital to shareholders through dividends and/or continue to invest in their development pipelines.

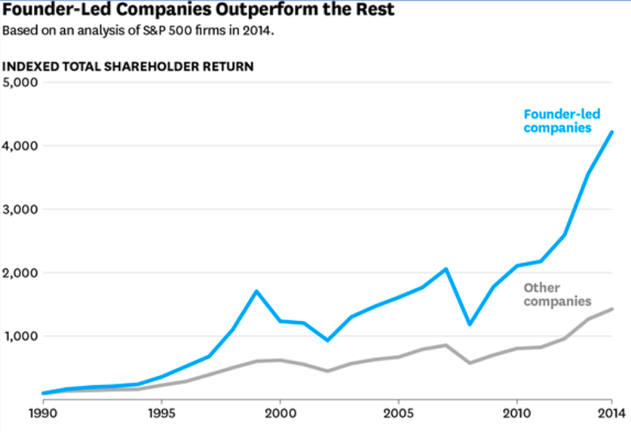

This week we will be talking about founder led businesses and why they tend to outperform. A number of the companies in our portfolios are founder-led; it is a factor we consider when assessing a company. So, we decided to dive deeper into what is driving their outperformance and, in doing so, we will highlight a founder-led chemical manufacture and waste management company that is beating prospectus forecasts, has a strong moat and is growing through an aggressive M&A strategy.

DGL Group (DGL.ASX)

Author: Ron Shamgar

DGL is a well-established, founder-led, end to end chemicals business that manufactures, transports, stores and manages the processing of chemicals and hazardous waste. The company operates a network of sites, both owned and leased, across Australia and New Zealand.

The key operations of the group include:

Formulation and manufacturing of specialty chemicals

Collection, transportation, storage, and logistics

Treatment, recycling and disposal

The company was listed in May of last year, raising $100m.

The Case for Founder-led Businesses

When assessing the merits of a company’s management team it can often be positive if you discover they are a founder-led business. There have been numerous studies about founder led companies and why they tend to outperform. Founders are typically more aligned with shareholders, usually having a significant amount of their own wealth tied up in equity. This alignment makes them more of an owner of the business which deters them from diluting shareholders.

Founders have been found to have a front line obsession. This typically shows up in a love of details and a culture that values those at the front line of the business. Employees at founder led companies typically feel more engaged. Bain & Company’s research found that engaged employees are 3.5x as likely to solve problems themselves and invest personal time in innovation as unengaged workers.

Founders also have more attachment to the company than your typical CEO. After all, the success of the business is essentially their legacy; it’s “their baby”. Founders are typically more prudent with accounting methods and capital allocation; a good example is DGL’s prospectus forecasts (see below). They were extremely conservative and ended up being exceeded by quite a margin. Many of the biggest tech businesses of the last couple of decades have been founder-led; think Apple, Microsoft, Amazon, Facebook, Tesla etc. While they aren’t a tech company, Andrew “Twiggy” Forrest deserves a special mention here in Australia. Given all of the above, we are starting to see a number of venture capital (VC) funds, Andreessen Horowitz for example, voice their preference for investing in companies where the founder is the CEO. DGL’s founder and CEO, Simon Henry, currently holds 53% of the company and recently bought another 500,000 shares for a consideration of $1.43m!

Source: Bain & Company

M&A Strategy

As part of DGL’s ambitious growth plans, they are embarking on an aggressive M&A strategy. During the half, DGL made seven acquisitions and all have been integrated well so far. DGL is looking to acquire companies that will unlock cost synergies for the group as well as broaden their services to create cross-selling opportunities. The more businesses they acquire, the more clients they acquire to cross sell to. A good example is recent acquisition Australian Logistics Management (ALM), which offers safe and reliable transport for dangerous and hazardous materials, focusing on sampling, specialised packing, compliance, and freight service of product samples. This acquisition expands DGL’s service offering while also giving them the opportunity to cross sell this service to existing clients. DGL is also looking to acquire properties to establish their processing facilities, as seen recently with their acquisition in Rocklea, QLD. It isn’t easy to build the infrastructure required for chemical and waste management on leased sites so DGL will continue to acquire properties to facilitate its growth strategy. DGL have typically used a mixture of cash, debt, and scrip to make their acquisitions; they like including scrip to ensure the acquiree remains aligned with DGL.

H1 Results

Source: DGL company filings

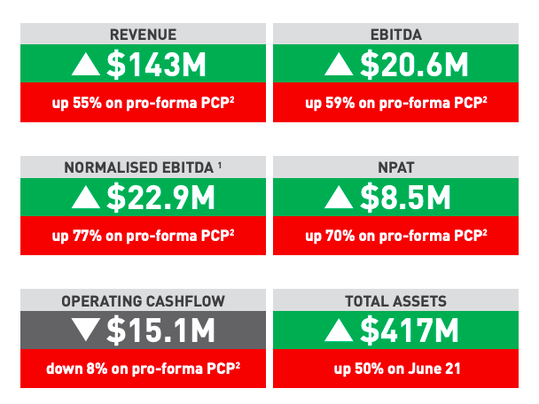

DGL reported a strong 1H result with their revenue up +55% to $143m and EBITDA up +59% to $20.6m. They have also been able to navigate supply chain issues well and saw their active customers double in 1H. More than doubling their active customers in the past six months hasn’t just expanded DGL’s business significantly but it has also de-risked their customer concentration. The increase in the number of clients only broadens the massive opportunity to cross sell services as they expand their offering through M&A. Their largest customer now makes up 10% of their revenue, compared to 19% previously.

Source: DGL company filings

Outlook

The advantage of being an incumbent in the chemical waste industry is that there are very high barriers to entry. The CAPEX required to start operations is high, it is expensive and quite difficult to obtain the licences required to operate in the sector. DGL has a broad portfolio of licences, accreditations, and regulatory approvals which are hard to replicate.

DGL has far exceeded its FY22 prospectus forecasts; they released FY22 guidance of $343m revenue and $54m EBITDA compared to the prospectus forecast of $210m revenue and $29m EBITDA. DGL has a huge pipeline of M&A opportunities and will continue to acquire more companies in the half; they still have 25% of their borrowing facility unused and are happy to go to a leverage ratio of 3x (currently at 2x). Most of DGL’s targets to date have been fairly small so a larger acquisition could get a lot more attention from the market.

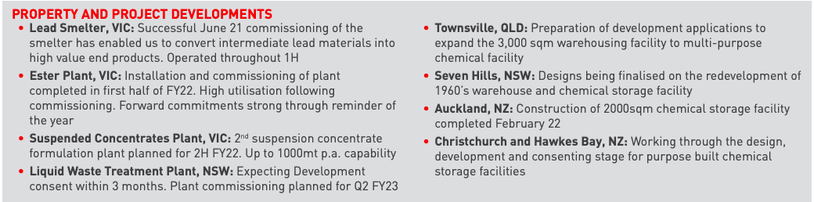

DGL currently has nine projects under development, some of which have been completed in February with others expected to be completed some time this year. These developments will significantly improve their chemical storage and manufacturing capacity.

Source: DGL company filings

Their environmental solutions segment is seeing significant tailwinds too as the recycling sector receives huge benefits from the government and the shift to a carbon-free economy puts more pressure on businesses to engage in recycling measures. DGL is currently trading at 17x EV/EBITDA. Some might think that’s expensive but we are happy to pay a premium for a quality business with a huge moat that is founder led and growing rapidly, also bolstered by a strategic M&A strategy.

Disclaimer: DGL is currently held in TAMIM portfolios.

This week we continue with the Talking Top Twenty series by rounding out the Big 4 banks, looking at National Australia Bank (NAB.ASX) and Australia and New Zealand Banking Group (ANZ.ASX).

To recap on what we look for when it comes to valuing the banks, there are broadly two metrics to look at; 1) volume growth and 2) the market’s views on interest rates.

National Australia Bank (NAB.ASX)

As always, we begin with the numbers. As expected, NAB continues to deliver and build upon expectations since we last wrote. 1Q22 earnings up to $1.8bn, +12% on the previous quarter and +9.5% compared to 1Q21 (largely in line). What was above expectations however was the large surplus in capital, coming in at $8bn (approximately $5bn above CET1 ratio range). This creates a significant buffer for the bank and bodes well for maintaining future distributions. Speaking of distributions, based on guidance, we now expect distributions for NAB to be in the range of $1.35 p/s, or approximately 4.2% using the share price at time of writing. Turning to the all important NIMs, we saw a decline of 5bps to 1.64%; this was primarily driven by a negative impact from M&T (i.e. Markets and Treasury), offset somewhat by lower funding costs. This is one metric we feel that investors should continue to pay attention to.

Looking more holistically however, the business seems to be delivering on its franchise momentum (i.e. could result in higher surprises going forward on non-interest income). We also strongly support the proposed acquisition of Citigroup’s Australian consumer business and the divestment of the BNZ Life insurance business (i.e. this should see CET1 decline to 11.3% however, which may explain the more aggressive share buy-back).

Red Flags & Risks: As always, the biggest risks continue to be NIMs. Rather telling was the rise (granted, arguably short-term in nature) in expenses by 2%. The higher exposure for the business toward the Business segment should see it disproportionately exposed to continued supply chain disruptions and inflationary pressures (vis-a-vis deterioration in credit quality).

My Expectations: NAB was our preferred bank exposure when we previously visited the topic and, while it is no longer as cheap as it was, its higher exposure to Business banking should see it well placed to take advantage of the recovery economy and act as a cushion to any slowdown in the volume growth for residential mortgages. Indeed, the economic recovery has seen NAB’s Business and Private banking arms exhibit solid growth. This comes at the same time as management making significant progress in the area of customer experience.

Dividend Yield: 4.2%, assuming a share price at $32.37.

Australia and New Zealand Banking Group (ANZ.ASX)

ANZ has been in the headlines lately and for all the wrong reasons. This involves issues around corporate governance, an ex-employee pointing to the use of wholesale deposits for CET requirements and sexual harassment claims. Not ideal but it’s not for us to delve too much into, given it is hardly likely to make a difference both in terms of share price performance or the bank’s broader corporate strategy. With that, let’s get to the numbers. The all important NIMs continued to fall, another 8bps, to around 1.57% (second half of fiscal 2021). The bank continues to face some inefficiencies in growing the home loan book – flat lined performance despite the market growing +6.5% over reported period – or offsetting lower margins. This broadly comes down to the approval process with the business continuing to lose market share. The only reprieve, it seems, is the institutional book which has, pleasingly, been the outperformer. One should expect this given that it has no great competition in the space in the domestic market. On the operational expenses front however, we have seen some stabilisation (broadly in line with expectations).

Assuming the current run rate holds, we expect 2022 earnings of approximately $5.2bn, a decline from $6.198bn in 2021. The bank remains a laggard in comparison to competitors both in terms of approval times and automation of backend. Last time we undertook this exercise we found this to be the least risky of the Big 4 given a well-diversified revenue stream by way of an institutional book. While this his been the saving grace, there isn’t all that much in our view for the market to be particularly excited about. CET1 remains the lowest among the peers and, using APRA statistics, the bank continues to lose market share (13.6% vs 14.6% a year ago).

Red Flags & Risks: Aside from NIMs, which clearly remain the lowest (in comparison to her peers), the biggest risk seems to be a lack of delivery on its transformation. Operational costs continue to be substantially higher than forecast, market share being forfeit. We don’t see a clear strategic or tactical vision for the business going forward.

My Expectations: ANZ has now become the least preferred of the Big 4. We expect that the share price will continue to underperform in comparison to competitors though the bank, like all the Australian banks, remains well capitalised, enough to maintain a reasonable payout ratio. But, even at 75%, this is not something that is sustainable in our view. Management has to do something to keep alarmed shareholders in line though.

Dividend Yield: Assuming the unsustainably high payout ratio of 75%, then the current dividend yield stands at 5.1% (at $27.88 share price).

Disclaimer: NAB and ANZ are currently held in TAMIM individually managed account portfolios.

This week we will be visiting the world of semiconductors and looking at why the equipment providers may be a compelling way to gain exposure to the sector. We are currently in the midst of a massive global shortage of semiconductors at a time when demand is skyrocketing as a result of aggressive digitisation and the rise of tech like electric vehicles. The stock in question is a SATS (Semiconductor Assembly and Testing Services) company.

Advantest (6857.TYO)

Advantest is a Japan-based ancillary semiconductor company; they are an essential part of the ecosystem to develop semiconductors. Advantest provides a one-stop shop for the test systems, test handlers, and device interfaces which are essential to semiconductor package testing. From locations around the world, they provide equipment to support globally distributed semiconductor supply chains. Simply put, they ensure that the production lines are working and production yields for chip makers remain as high as possible. They are most well known for their automated test equipment which tests chips after the wafer is diced.

Advantest continue to be the only tester provider that can provide solutions for all producers and all test processes in both DRAM (a type of semiconductor memory that is typically used for the data or program code needed by a computer processor to function) and NVM (a semiconductor technology that does not require a continuous power supply to retain the data or program code stored in a computing device).

A Look into the Semiconductor Industry

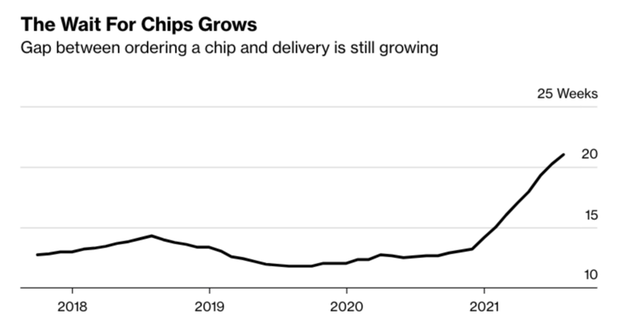

If you were to go to a car dealership tomorrow and try to buy a new vehicle, there is a decent chance that you won’t be able to take that car home for the next six months. The pandemic has caused a multitude of supply chain issues that have ultimately led to a shortage of semiconductors which are an essential component of just about every electronic device. They are so instrumental to our daily lives that the governments of Japan and South Korea compare them to rice.

Source: Susquehanna Financial Group

We are currently in a generational shift to a more sustainable future filled with electric vehicles that require significantly more semiconductors than a traditional internal combustion engine (ICE). At the same time, we are in the middle of a massive supply deficit for semiconductors; many believe it will last for years to come. While some disagree on the timeframe, just about anyone can tell you that electric vehicles are going to be a pivotal pillar of the future. What fewer people are talking about is the lack of supply of all the critical inputs needed to manufacture them at large scale; this includes cobalt, nickel, copper, tin, manganese and, importantly here, semiconductors!

A couple of decades ago not having a mobile phone was no big deal. In today’s world however, not having a smartphone almost puts you at a disadvantage; you simply won’t have access to things. The ongoing digitisation of our economy, which includes smartphones, IoT, 5G etc., requires an enormous volume of semiconductors just to power the things we rely on in our everyday lives.

What many people don’t realise is that semiconductors are also a key piece to the puzzle when it comes to some of the complex geopolitical situations we are seeing unfold right now. China lags behind in terms of their semiconductor capability which means they simply don’t have the best technology. Their neighbour Taiwan though, is home to the most advanced semiconductor manufacturing company in the world, Taiwan Semiconductor Manufacturing Corporation. China isn’t looking to potentially invade Taiwan for their famous street food, they want to get hold of their ground-breaking semiconductor capabilities.

Already under immense pressure due to covid-related supply chain issues, the current Ukraine/Russia conflict will further exacerbate the chip shortage. Ukraine produced over 50% of the world’s semiconductor-grade neon, a crucial input to produce chips. As a result of the conflict, suppliers in Ukraine have halted operations.

Testing Tailwinds

Source: IC Insights

There is a growing need to ensure the reliability of semiconductors due to their increasing complexity. The expansion of semiconductor demand has also continuously boosted the demand for testers. The challenges of semiconductor miniaturisation, advancing complexity, and power consumption reduction have continually raised the bar for improving test efficiency.

Due to higher costs associated with larger wafer fabrication factories (fabs), manufacturers are mostly inclined toward outsourcing semiconductor assembly and testing services to third party providers. Leading fabless companies will continue to outsource everything, including testing, assembly, and packaging. This is a huge driver for testing companies like Advantest.

We are also seeing governments across the world giving huge grants for semiconductor companies and investing in bringing production onshore. They know what is at stake and the pandemic was a huge wakeup call for the US, who are starting to bring industrial production back onshore as a geopolitical and national security imperative so they are less reliant on overseas supply chains, China in particular. As part of Biden’s $2tn infrastructure plan, $50bn will be invested in boosting semiconductor competitiveness. China, who are about 5 years behind TSMC, are spending hundreds of billions to try and catch up.

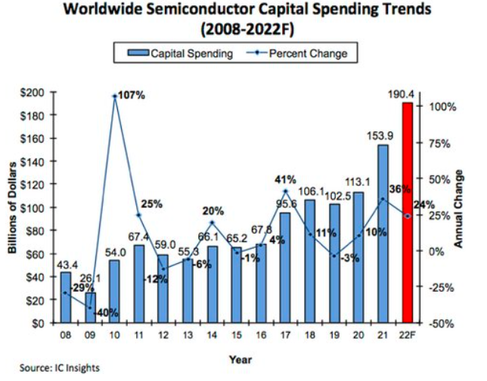

In order to meet the surge in demand and close the supply gap, semiconductor manufacturers are set to spend $190bn on capex in 2022, a 25% increase on 2021 levels. TSMC are in the process of building a new fabrication plant the size of 22 football fields in southern Taiwan. This new plant will produce three nanometre chips which will be the latest generation and are expected to be up to 15% faster. The increased investment from manufacturers will understandably benefit equipment providers like Adventest.

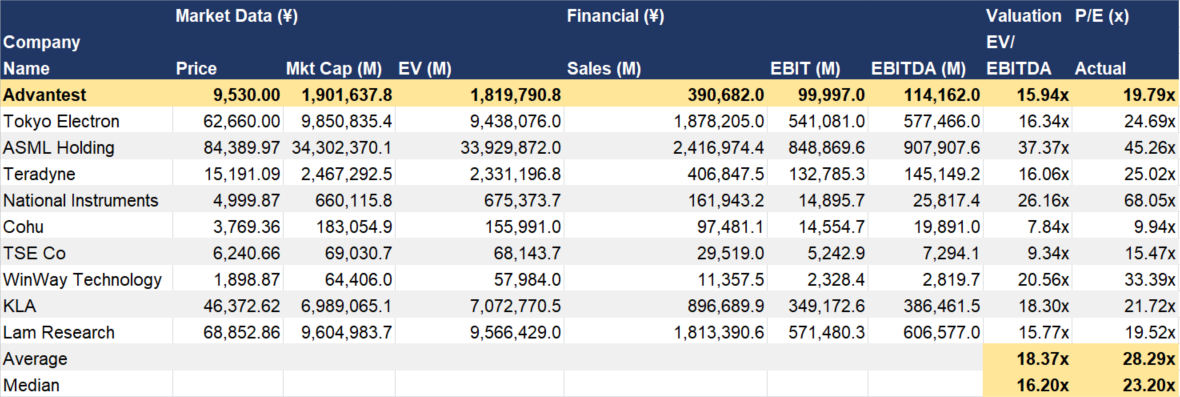

Valuation & Outlook

Advantest are expected to grow their revenues by 32% in FY22 and a further 15% in FY23. They continue to invest significantly in R&D (around 13% of sales) and have become one of the leading SATS companies in the world. Their EBITDA margins are strong at 35% and will be a big beneficiary from the shift towards digitisation as well as the widespread shortage of semiconductors.

Source: Factset, TAMIM

Advantest are currently trading below the average multiples for semiconductor testing companies. Not only do they look cheaper than their peers but we believe they have a better outlook than most of their competitors. Their main competitor, Teradyne (TER.NASDAQ), is heavily reliant on Apple (APPL.NASDAQ). Apple are developing a three nanometre chip for their next line of iPhone and Mac products. Apple are looking to launch this next line of products after 2023 which impacts Teradyne’s FY22 forecasts significantly, leading most brokers to downgrade their outlooks. One of the reasons why Advantest will fare better this year.

While most people would look to the well-known chip makers to gain exposure to the space – i.e. Intel (INTC.NASDAQ), TSMC, Samsung (005930.KRX), Nvidia (NVDA.NASDAQ) etc. – but we are always looking for companies that don’t see the same coverage yet have a strong foothold in the thematic we are targeting and therefore are leveraged to the tailwinds but trade at a cheaper price. Advantest trades at a cheaper price and will absolutely benefit from semiconductor tailwinds.

Advantest will continue to ramp up their investment in R&D and M&A. At the back end of last year Advantest completed the acquisition of Altanova, a testing equipment manufacturer in New Jersey. The acquisition will expand their test and measurement solutions across the continuously evolving semiconductor value chain. Altanova’s engineering and manufacturing capabilities, excellent customer base, and first-rate technical team will complement their semiconductor test equipment business as well as give them a bigger presence in the US. We expect more deals like this in future.

Like most listed Japanese companies, Advantest is in a strong net cash position with little debt. Their strong balance sheet affords them the opportunity to potentially lever up their balance sheet to increase returns for investors. Their ROE is currently over 30%, imagine what leverage could do to that figure. Advantest are on track to reach their goal of ¥400bn in sales and continue to grow their dividend payments each year.

Disclaimer: Advantest is currently held in TAMIM portfolios.

Author: Ron Shamgar

Author: Ron Shamgar

Source: IC Insights

Source: IC Insights