This week we will be talking about the recycling industry, a segment that we don’t believe is spoken about enough in this age of environmental reform. Similar to our recent article on tin, recycling seems to be a forgotten factor that investors are overlooking. We will highlight a recent recycling IPO that is growing fast and will be benefiting from industry tailwinds.

Recycling Industry

Author: Ron Shamgar

The hottest thematic currently dominating headlines is centred around environmental change and decarbonisation. Investors are looking for companies that will facilitate or participate in an emission-free economy. However, it seems recycling has been overshadowed by the likes of battery metals and renewable energy. Yet it is arguably more vital to our fight for environmental preservation.

Our planet endures an ever-growing waste management problem, the major source of this harmful pollution is single-use plastic. Single-use plastics are responsible for many of our pollution problems both on land and in our oceans. In order to transform our use of single-use plastics, governments around the world have implemented a plethora of policies and incentives to help curb the problem. These incentives and policies are huge tailwinds for the recycling industry.

Summary: Macro and Regulatory Tailwinds

Almost US $3tn (per year) of additional capital investment is required to meet increasing sustainability metrics

Continued high landfill rates for plastic and print consumables

Low adherence to recycling creates opportunities for companies to innovate and find solutions to increase overall recycling rates

Packaging producers/customers are examining more effective and efficient recovery and take back/re-use of valuable product resources to increase their “social license to operate”

Countries are beginning to ban exporting waste which creates a need to deal with it themselves rather than ship it to other countries that are likely not dealing with it in a environmentally safe manner

Chinese National Sword ban on importing mixed recycled plastic waste – this has a huge impact on Australian waste and means we need to find domestic solutions to deal with waste

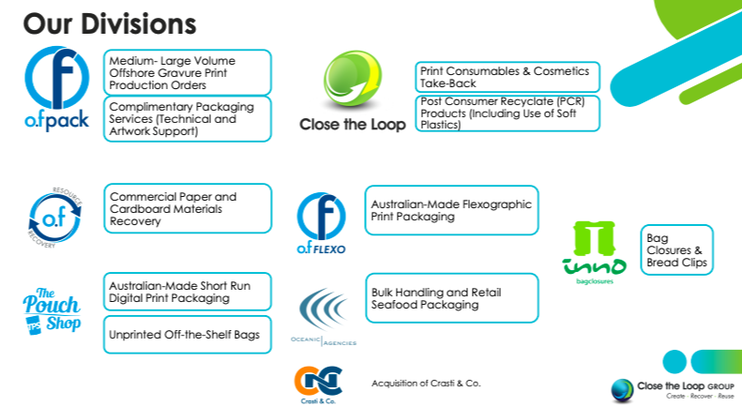

Close the Loop (CLG.ASX)

With locations across Australia, Europe, South Africa and the US, Close the Loop creates innovative products and packaging that includes recyclable and made-from recycled content, as well as collect, sort, reclaim and reuse resources that would otherwise go to landfill. From recovering print consumables, eyewear, cosmetics, and phone cases, through to the reusing of toner and post-consumer soft plastics for an asphalt additive, CLG is focused on the future, sustainability, and the circular economy.

Close the Loop consists of the merging of two secondary business groups; Close the Loop and O F Packaging. The combining of these two entities allows for end-to-end solutions across packaging and consumables to a variety of markets, with advanced innovation in product development, as well as end of life take-back and recovery systems for complex waste streams to greatly reduce waste to landfill.

Source: CLG company filings

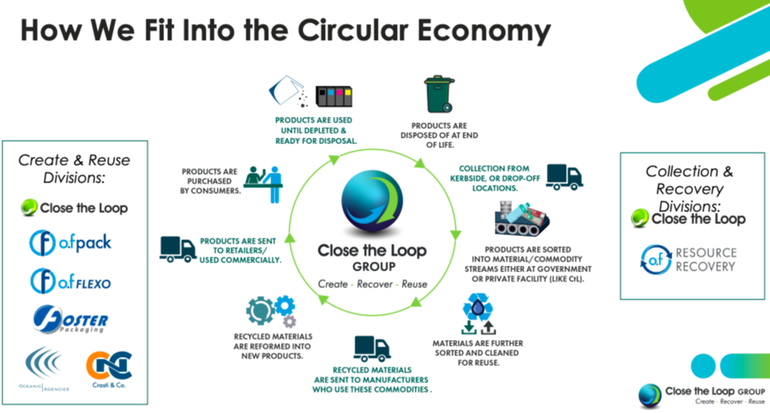

A circular economy is an economic system that tackles climate change, biodiversity loss, waste, and pollution. It seeks to correct the problems of the linear economy where consumers and businesses follow a “take, make, waste” process, meaning most products and resources become waste. The circular economy employs reuse, sharing, repair, refurbishment, remanufacturing and recycling to create a closed-loop system, minimising the use of resource inputs and the creation of waste, pollution and carbon emissions.

Source: CLG company filings

M&A

Close the Loop merged with O F packaging when listing late last year as part of their growth strategy. CLG are looking to acquire businesses that expand their business geographically, give them access to European markets, and provide cross selling synergies. Their recent acquisition of Oceanic Agencies strengthens Close the Loop’s bulk and commercial seafood packaging capability with strong cross-selling opportunities. CLG has a pipeline of M&A targets and they are sitting on a strong net cash position of over $6m, giving them room to lever up the balance sheet to accelerate their M&A strategy.

Source: CLG company filings

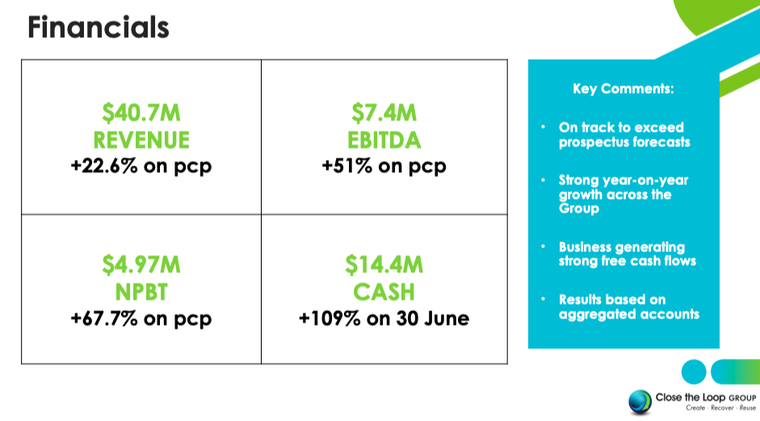

CLG grew its revenues by over 22.6% in the first half and is on track to exceed prospectus forecasts. It’s also key to note that only five months of their Crasti & Co acquisition (done earlier this year) revenue will be included in FY22 as well as only seven months from their Oceanic Agencies acquisition.

Outlook

We like CLG’s business model as it is hard to replicate and quite expensive to enter the recycling industry due to the huge startup costs. CLG has all the necessary infrastructure to operate, including over 60,000 collection sites in Australia. The business was slightly affected by covid as it is volume based and saw less volume throughout the pandemic. CLG has huge tailwinds that will further benefit their business from a macro and regulatory standpoint. On top of this, they are one of the only pure play recycling companies around. The business is profitable and trading at approximately 8x EV/EBITDA. Their future growth will be fueled by M&A and global expansion opportunities, particularly in the US and EU.

Robert Swift takes some time to look at portfolio allocation in the context of the current global climate; now focussing on investing in the ‘needs’ and not ‘wants’.

Most risk assets have had a decent fall this year. Long overdue and somewhat predictable perhaps but, as ever, it’s the most popular stocks and styles that have been hit hardest.

Author: Robert Swift

Along with the Ukraine invasion and continued Covid-induced lock downs in Asia, the rise in the US 10 year note yield has been responsible for this reappraisal of risk.

The US 10 year note yield is fast approaching 3% and the whole curve has occasionally inverted which to some ‘scribblers’ portends a recession. To put this rise in perspective, the US 10 year note yield was 0.5% in July 2020 and started this year at about 1.6%. That’s quite a loss of capital given the long duration at such low yields. Over that same 21-month period, US equities are up about +30%!

Too late, the ‘inflation is transitory’ narrative has been removed, and we now perhaps have a more aggressive tightening to endure than we would have had if action had been taken sooner? “A stitch in time saves nine” is a useful refrain to remember.

We have been told that ‘tightening’ is an imminent rise of 50 basis points in the Fed Funds rate (the short end) but also need to bear in mind that the size of the Fed balance sheet is going to be reduced. This represents an additional source of tighter monetary policy and so the effective tightening of policy is greater and quicker than most realise. This has consequences for the kinds of risk factors one should favour; put another way, a different kind of stock will do better in the next five years than in the last ten. The 30% rise of US equities compared with a 15+% fall in the value of ‘safe’ government fixed income is unlikely to continue.

We call it investing in stocks that meet needs rather than wants.

To repeat, in our view, new emerging investable themes will be: –

A) Defence, food and energy security are all now clearly priorities and are not wants but needs. The green transition couldn’t have been handled worse, as we detailed in our recent presentations (“All revolutions eat their young”). Nuclear power should be on the agenda. All this is investable.

B) De-globalisation or National Industrial Policy is on the rise as we suspected it would be. This means both a need for an increase in domestic capital investment and the involvement of government in ‘helping’ revitalise and protect strategic industries. The semiconductor industry in the USA is one such example.

C) Buy backs have to give way to capital investment incentives. This increase in capital expenditure in the name of National Industrial Policy is much needed. This inflation is different from that of the 1970s when the labour force was very powerful and not very productive (at least in the West). Then wage increases were way above inflation and fed the beast with expectations of price increases driving the next round of higher wage demands. This time it’s a dearth of supply side competition that is causing the price pressures and misguided legislation against oil companies, pipeline companies, lobbying to prevent break ups of monopolies, the shedding of defined benefit obligations, the introduction of zero hour work contracts have placed capital firmly with its throat on labour. Capital investment has been disincentivised and buy backs rewarded. This has to shift back.

D) In an era of inflation and rising mortgage rates, the consumer will become more discerning about where they spend their money since inflation has been eroding income for a long time and personal debt is high already. This again means the extrapolation of subscriber growth and price increases is naïve. Anyone for Netflix?

To us, this means one should favour basic materials, energy (pipelines are probably a better position than ‘evil’ oil?), industrials, defence, infrastructure and, increasingly, banks, especially US regional banks.

One area needs a mea culpa, one which has hurt our returns and surprised us, Japan. Japan and especially the Yen are getting sold harder than Europe and the Euro. We have been roughly benchmark weight the US and USD while being overweight Japan and the Yen and underweight Europe and the Euro. We understand that the Bank of Japan, the central bank, has signalled it won’t tighten policy and thus makes the rising yield on the USD attractive relative to the Yen, but Japan remains a massive net creditor nation and has not (yet?) displayed any excessive inflation. Meanwhile the ECB cannot raise rates for fear of sparking a new crisis in the Euro still held together by smoke and mirrors. Inflation, even in Germany, is getting serious and, at over 7% p.a. as of March 2021, is the highest since 1981.

We’ll continue with our positioning.

There is still plenty of risk and lots can go wrong with the attempt to create a soft landing. It’s not our expectation but, it’s worth bearing in mind, we can see a whole lot more intervention and confiscation.

So, be aware of risk and portfolio construction even if you wish to focus on only a few markets and sectors.

A portfolio should comprise of more than a few favourite stocks. Ten companies isn’t a diversified portfolio, nor is twenty. Probably not even thirty. Combine strategies that do different things and invest in different kinds of stocks with perhaps different holding periods; i.e. time diversification. Prepare to be content with 8% p.a. and there is still time to position away from the ‘growth at any price’ style!

For those that have read previous iterations of this exercise, you may be aware that MQG is one security that we have always insisted offers a credible (if not better) substitute for the Big Four. Very rarely do we find businesses, especially in the financial services landscape, that can maintain the culture/mentality of a small firm in a large organisation. So, with that let’s get to the numbers; which may provide answers as to why this may be the case.

BFS (Banking and Financial Services) offered up a 12% contribution to 1H22, showcasing improvements across every single service line with highlights including a +4% growth in deposits, +8% growth in home loans, +12% in car loans and a significant +4% growth in funds on platform. More important (for us), is the AUM growth in MAC (Macquarie Asset Management). This is one division that always has our attention given its highly sticky revenue and annuity like return streams. AUM grew to AU $750bn or +2% in 3Q22 while private markets grew to $160.1bn equity under management with a significant $8.1bn in equity raised during the quarter. This is another attractive proposition, private markets are simply notoriously sticky given their long duration and relative insulation from market gyrations.

Looking further, to the Commodities and Global Markets division (CGM), the business continues to maintain momentum. Given the state of the energy markets across its key markets, including gas, we should see continued momentum here especially in the structured lending side of the business. CGM currently accounts for a tidy 43% of the total 1H22 earnings. Macquarie Capital has also seen significant deal flow although this is one division we have never been fixated upon given that it is exceptionally pro-cyclical in nature.

Risk wise, MQG’s CET1 ratio has increased to 15.4% (compared to 12.6% at the time of our previous notes) and the balance sheet remains stellar. Overall, the business seems to be ticking boxes and continues to offer an attractive risk-reward proposition. Asset gathering continues to be the most attractive attribute and, given the infrastructure pipeline globally, we see a secular growth story here and an ability to maintain annuity-like revenue streams that offer an exceptional buffer. To give a little context on the opportunity set across infrastructure and the green transition, the numbers stand at approximately US $75tn according to the firm’s own briefing.

Red Flags & Risks: The big risk for Macquarie is the headwinds faced via a bullish AUD. Despite recent price action given our view on commodities, we think that there is upside risk here despite interest rate parity. The fee structures that are so attractive to shareholders could also be detrimental in the long run and risk cannibalising the book.

Expectations: MQG remains a fair substitute for the Big Four with a well-diversified business and is an arguably greater risk-reward proposition. When we wrote about this security previously, we thought it may be fairly valued at AU $149.540. At AU $200.72 per share, it continues to be expensive from a purely PE perspective. Nevertheless, investors may have to continue paying a premium given the prospects.

Dividend Yield: The current dividend yield stands at a not so exceptional 2.8%, assuming a price of $200.72 AUD. But this may be a dividend growth story.

Telstra Corporation (TLS.ASX)

When we last looked at this company we were of the opinion that, despite the historic value destruction it has brought many shareholders, this was one security that may have hit an inflection point. The major contention was that the industry-wide race to the bottom, as represented by aggressive market share acquisition strategies, may be behind the sector and that the revitalisation strategy undertaken by CEO Andy Penn ticked the right boxes. It has been proven true on all counts, if not even better than expectations. It has been a rather eventful year for the business with many surprises.

The first surprise was the mobile network sharing agreement between arch rivals TLS and TPG, whereby TPG pays the business for access to a significant portion of Telstra’s regional footprint. This not only allows incremental growth in its wholesale earnings but allows for increased quality across its metro and regional networks. Interestingly, wholesale prices will be increased by mid-year while inflation indexed pricing will be added on (this is a significant development for investors looking to find some cover against the ever increasing inflation story). This story will be the one to watch out for when looking at the business, at least with regards to the mobile division. Conversely, fixed enterprise continues to be a concern for us and this is where the business comes in direct competition with NBN. Although the company has made some strides in offering value add, it still has a way to go especially in managed data and, quite simply, evolving away from its public sector mindset.

Management-wise, we were surprised by Andy Penn’s departure. We were particularly fond of him and his overall handling of the headwinds faced by the business. He will be replaced by industry veteran and CFO VIkki Brady. The board didn’t look far and may have learnt from the Sol Trujillo fiasco; we will see what she has to offer and if it will be a substantial diversion from the Penn/T22 years. We would like to see some outside the box thinking in terms of value add. Perhaps content? Similar to the business’ American counterparts or even Optus.

Looking at the numbers, the aspirational AU $7.5 – 8bn EBITDA target for 2023 now almost looks to be a given. Financial metrics were certainly less than pleasing for 1H22 with EBITDA coming in at AU $3.5bn (down -14.8%) and NPAT of AU $700m, this masks the one-off events as a result of the restructure and the stabilisation as well as growth within the primary segments, including mobile. We have seen consistent delivery in the cost-outs as a result of the T22 strategy, which mitigated the earnings hit by AU $2.3bn. We will also see significant tailwinds in the form of market leadership in the transition to 5G. Simply put though, the business is well positioned to hit the ground running going forward.

Red Flags & Risks: The industry has finally stabilised with rationalised market shares and consolidation. The risks going forward will be uncertainty around management and the potential for change in strategy. CFOs typically have great track records delivering efficiencies but not necessarily with customer acquisition or retention. We feel that the company continues to underestimate the headwinds for its fixed enterprise divisions, especially with competition from niche providers.

Expectations: The company continues to be an attractive risk-reward proposition given its valuation, despite being significantly higher than our previous writing. Given guidance, we think the surprises may be to the upside.

Dividend Yield: Expected dividend yield stands at an exceptional 4.02% assuming a price of AU $3.98.

This week we will be looking at the US cannabis industry and talking about a stock in the ‘picks and shovels’ side of the industry, a real blue jeans to miners story. US cannabis stocks have been in a relentless bear market, hovering near all-time lows despite the industry showing huge growth.

Before we continue, this is not an industry that TAMIM currently invests in and it may never be. That being said, we do acknowledge the potential in the industry and, given its current changes in legalisation, it currently presents as a perfect example of the benefits of identifying ‘picks and shovels’ or ‘blue jeans to miners’ companies.

Cannabis operators face enormous constraints as a result of cannabis not yet being legal at a federal level. These constraints include higher taxes, no access to capital and an inability to list on the primary exchanges. The ancillary companies that provide services to the industry get the benefits of the industry growth without suffering the constraints.

Ancillary Companies

An alternative way to gain exposure to the growth in cannabis is to invest in ancillary companies; the companies that provide goods and services to the cultivators. They are the ecosystem that facilitates the growth of the cultivators. As the cannabis industry grows, it’s not only the operators that grow and sell cannabis that will benefit. The companies providing finance, equipment, and other goods and services will also be winners. Farming businesses have never been overly attractive; they tend to be cyclical, reliant on external factors like weather and so much can go wrong. On top of this, the risk of crop contamination is always present. As many of these cannabis companies are essentially just farmers, investors may prefer to allocate to the companies that provide equipment or even software to optimise crop growth. These companies typically come with less risk and, since they don’t grow or sell cannabis, they usually can trade on the primary exchanges.

Scotts Miracle-Gro (SMG.NYSE)

SMG manufactures and sells products to the consumer lawn and garden market, the company was founded in 1951 by Horace Hagedorn and is now run by his son Jim Hagedorn. SMG is a family-run business with the Hagedorn’s owning around 27.1% of the business still. While SMG has been a steady business that benefited from Covid, what we are interested in is their ancillary cannabis segment, Hawthorne. Hawthorne has built a portfolio of leading hydroponics companies (i.e. the systems used to cultivate cannabis in a greenhouse). Hawthorne supplies the nutrients, lighting equipment, and other essentials to cultivate the crop. As the industry grows, so does Hawthorne. With the rapidly expanding footprint of cannabis legalisation across the east coast, where cannabis needs to be cultivated indoors, Hawthorne will further benefit from increased demand for their products

Source: SMG company filings

SMG is a safer way to gain exposure to the cannabis sector and it’s listed on the primary exchanges. It has an Apple-like presence in the lawn and garden industry. SMG also has first-mover advantage when it come to the picks and shovels in the cannabis space, their Hawthorne segment has quickly grown to a billion-dollar business.

Source: SMG company filings

SMG’s business will also benefit from changing demographics; millennials have been proven to spend more on their home as opposed to boomers. Pandemic-related stay-at-home orders resulted in a lot of consumers developing new hobbies, igniting the huge shift towards DIY driven by millennials. These trends will support SMG as well as boost their ecommerce activity. Scotts Miracle-Gro’s recent Super Bowl ad was leaning into this growing demographic: the millennial gardener.

Source: SMG company filings (ORC Engine, January 2022)

SMG saw its share price come down from US $250 on 1 April 2021 to around US $117 today. Their core business was a huge beneficiary from Covid with the shift to DIY but their Hawthorne segment has struggled with the oversupply of cannabis and fractured supply chains, leading to a 38% decline in sales for the first quarter. SMG provided a $150m convertible loan to Canadian cannabis investment company RIV Capital (RIV.CNSX) who have taken stakes in a portfolio of different Cannabis-related companies. This convertible note gives SMG shareholders further exposure to the broader cannabis theme.

SMG is currently trading at about 12x NTM EBITDA. When you compare this to other hydroponics companies like Hydrofarm (HYFM.NASDAQ), who are trading at 17.2x EV/EBITDA, you can see that there is some value here with the Hawthorne business. At current prices, the market isn’t ascribing any value to the Hawthorne business; investors are essentially paying for a steady gardening business with the potential upside of cannabis exposure.

Potential Catalysts:

Further/ongoing legalisation throughout the US

Uplisting of cannabis stocks from OTC markets to the bigger exchanges – i.e. the value of their investments through RIV Capital will go up

Spinning off of Hawthorne; this would come with a few dis-synergies but, if done at the right time, it could create serious value for shareholders

Continuing our Talking Top Twenty series, this week we take a look at a pair of retailers, Woolworths (WOW.ASX) and Wesfarmers (WES.ASX), and a biotech giant in CSL (CSL.ASX).

CSL continues on the mixed results train though broadly in line with guidance and expectations. What has been pleasing is the return of plasma collections to pre-covid levels (up +18%). Longer term, the number to watch is the immunoglobulin portfolio and diversification of revenue streams. Plasma alternatives will act as secular headwinds for the business’ traditional revenue streams and, in our view, higher margin speciality and niche verticals will be where the next generation of growth is. The recent acquisition of Swiss headquartered Vifor Pharma for a price tag of about $16.5bn (pending regulatory approvals) fits nicely within this broader move, Vifor being crucial in building a significant renal franchise (i.e. kidney disease related).

Getting to the numbers, group revenue was up +4% to $6.041bn while NPAT declined -5% to $1.427bn over 1H22. Looking closer, of particular concern was declines in albumin (immunoglobulins) in the EU and less then stellar numbers in the US, though China has seemingly offered some respite. This is one number we will continue watching. On the other hand, specialty was rather pleasing with sales up +2% and hospital products back to pre-pandemic levels.

Overall, while results are mixed, we think that management has been doing a competent job on delivering in an increasingly competitive environment with added supply constraints (Covid-related). With that in mind, CSL presents as a good allocation in any portfolio over the long run with forecasted high single to double digit revenue growth along with a stellar R&D pipeline, the most interesting being a licence agreement for a late stage haemophilia B gene therapy candidate.

Red Flags & Risks: At the time of our previous notes, our biggest red flag was the rate of plasma collection. This time around we move to the competitive landscape, Roche’s (ROG.SIX) Hemlibra in haemophilia for example. The business faces significant headwinds and uncertainty in its primary plasma market. CSL’s historic investment in this infrastructure could leave it vulnerable to newer treatments and alternatives. Even on the collections front, CSL’s main competitor, Grifols (GRF.BME), is set to substantially increase its own collection centres to 520 by 2026 (compared to CSL’s 306).

Expectations: The company continues to be a long-term hold in our view. Target: AU $280.

Dividend Yield: 1.11% assuming a share price of AU $262. Expectation remains that dividends continue to grow at double digits over the long-term.

Wesfarmers (WES.ASX)

Despite management patting themselves on the back after the results, the market (as holders may be aware) wasn’t having it. The security was down almost -7% on announcement. So, what were the numbers? Revenue down -0.1%, NPAT down -12.7% to AU $12.7bn and EPS down -14%. This business has been a rather disappointing watch. Particularly interesting was the lack of disclosure around Target’s performance (it was consolidated into Kmart Group), Target, as we have said before, is the problem child. Add in the fact that very little detail was given in terms of the core Bunnings business and the intrigue levels get higher.

While the Covid-related operating environment has been a little messy for brick and mortar retailers, we still didn’t expect the results that were put forward. The one upside was the CEF business; this is one positive aspect of having a conglomerate structure (if done well). Fertilizer revenue in particular growing +35.6% to a AU $183m. On the positive side, we do expect the numbers to stabilise given a rather buoyant consumer propelled by generous stimulus and a still expansionary monetary policy. That said, the business does seem overvalued at 27x earnings despite the sell off.

Red Flags & Risks: The biggest issue for us was the nature of the earnings presentation, the lack of insight into the specifics of divisions and a rather self-congratulatory tone. Target remains a problem for the business while supply chain disruptions and a softening housing market also doesn’t necessarily bode well for the flagship Bunnings business.

Expectations: Disappointing overall, at the time of our previous examination we were particularly positive on management’s vision. The business seems to be a little shaky and the lack of disclosure and self-congratulatory nature in which a less then pleasing result was couched didn’t help. In any case the business remains overvalued in our view.

Dividend Yield: 3.36% assuming a share price of AU $48.51. Expectation is that this will stay stable on a nominal basis.

Woolworths Group (WOW.ASX)

WOW continues to please with its recent announcement of the demerger of Endeavour Group. WOW now represents a pure-play food retail exposure. While the Covid-related supply chain issues and inflation have presented a challenge, management has shown the capacity to move forward. We expect that the business offers a uniquely defensive proposition given their much more localised supply chain and ability to pass on price increases, which been reflected in the results.

Getting to the numbers, EBIDTA down -6% to AU $2.485bn while sales was up +8% to $31.814bn. This may seem less than stellar but it showcases the nature of the issues faced by the business; it would be rolling off a particularly high comparable half in 2020 (Covid-related hoarding and short term spike) as well as major supply chain disruptions. What was pleasing is the reduced inventory turnover and clear strategy on the part of management in terms of omnichannel.

All that said, food retail remains a competitive business in Australia, especially given the Coles-Ocado deal along with increased market share taken by the likes of Aldi. We feel that the wiser focus would be in regional and sub-regional along with a focus on convenience. This will be especially hard for pure-play online retailers and newer entrants to replicate.

Overall, management continues to deliver on its outlined strategy and we remain convinced that it has a better investment thesis/case than Coles.

Red Flags & Risks: Having exited liquor and fuel, WOW is now a pure-play food business and with that comes the risks associated with a less diversified revenue stream. The cost pressures from the likes of Aldi and Coles (COL.ASX), as well as the potential entry of global giants like Amazon, could continue to exert significant margin pressure going forward.

Expectations: Top notch management that continues to deliver and offers a considerable inflation hedge for a portfolio. Strong earnings stability while future upside will be contingent upon cost efficiencies in logistics and supply chain.

Dividend Yield: The current yield stands at 2.6%, assuming a share price of AU $48.51.