This week we visit a topic that has been all the rage in 2022. Inflation. A word we perhaps hadn’t heard of in a couple of decades but has saturated every headline this year. As we write the ASX has given back around 14% from its peak in 2021 and the ASX Small Ordinaries down over 25%, officially entering a correction, and there seems to be no respite. With that context in mind, we take a step back as is always best in scenarios like this.

We will look to briefly address a few things in this article. First, what actually is inflation and how is it calculated? Second, why has this thrown the markets off to the extent it has? Third, has the market been rational in its reaction (here we focus on equity markets)? And finally, how do we allocate given the current environment?

Keeping with tradition, we begin with the conclusion. Despite the apparent conflict of interest here given we are a funds management firm, we fundamentally believe that equities remain the place to be. This with the caveat that a well diversified portfolio has never hurt investors.

Inflation: An Overview

Let’s begin with what inflation is. Simply put, it is the general (or overall) increase in the prices of goods and services in an economy. Sounds simple enough but the question then becomes how does one measure it? The most common method and one used by central banks when determining monetary policy is CPI or Consumer Price Index. This is the price index anchored to some base year (which would have a value of 100). From here we move onto another fundamental problem, how does one aggregate this given the complexity of an economy. For example, accounting for the addition of a new technology or the fact that not all goods or services have the same weighting in a consumer’s overall expenditure (not to mention the changes that occur over time here). The easiest illustration of this is simply that something like rent accounts for a far larger portion of household expenditure than new shoes (we hope).

With the above simplistic explanation, we hope that you were able to pick up on the first point about these numbers. They are open to interpretation and by their very nature are estimates. Moreover, such ambiguity also allows some artistry, especially given the political nature of what the measure may imply. For example, the last major change Stateside came in 1990 when the federal government decided to move toward a chain-weighted measure with the intention of explicitly reducing cost of living adjustments to social security recipients and allowing for significant reductions to the deficit. Another is the accounting for so called utility. In this scenario an example may be nominal increases in the price of mobile phones but, given the increase in functionality of said devices over time, prices can in fact be adjusted and revised downwards. To give some context into how much this can impact the headline figures, if one were to use 1980 measures in terms of calculations, inflation should be averaging 4-6% over the past two decades and should be around 10.65% (as opposed to the US’ recent 8.6%, a forty year high).

Why does this second aspect matter for the investor? Firstly, it pays to be a little more cynical towards what the figures represent. Second and perhaps more importantly, the same data can have real world consequences. This is primarily through monetary policy and, by extension, the real world cost of capital. Despite the flaws in actual methodologies, it is somewhat irrelevant as long as the bond markets continue to believe it and premise their pricing on said data. What we mean to say (rather controversial perhaps), using the 1980s methodology could imply that real yields have been negative for a lot longer than the years since the GFC.

Which brings us to the now. The current (and here we are speaking of Australia) weights are as follows: Housing (23.24%), Food & Non-Alcoholic Beverages (16.76), Transport (10.58%), Alcohol & Tobacco (9.01%), Clothing & Footwear (3.3%), Furnishings Household Equipment (9.16%), Health (6.47%), Communication (2.41%), Recreation & Culture (8.64%), Education (4.63%), Insurance & Financial Services (5.80%).

You may wish to look to the ABS website to understand the methodology and the process of apportionment, you may find it interesting. However for the sake of brevity, let’s take a look at these categories.

You may notice that some of the biggest weightings are tilted towards those that have a great degree of reliance on supply chains and energy prices. While it is easy to presume that the effect of energy is limited to transport, food prices in and of themselves are uniquely exposed (i.e. fertilisers). Similarly, housing will also be significantly impacted by the same vis-a-vis utilities bills. In one way or another, every single category with the exception of education, financial services, communication and recreation will have faced significant headwinds as a result of Covid lockdowns, China’s ongoing zero Covid policy and the Russia-Ukraine conflict.

The point? As it’s currently calculated and given the weightings listed above, we would very much expect CPI to be high at the moment. The question that begs is how many of these outsized price movements are as the result of an extraordinary event versus being systemic? Just take a look at the YoY changes to some of the US’ CPI categories in the May 2022 CPI Report:

The Market Reaction

As with many things, it’s often easier to be short-sighted. So, let’s put everything into a little context. Since the GFC and the resulting advent of unconventional policy (i.e. QE) as a tool kit, we have been beneficiaries of what can only be termed asset price inflation of epic proportions. What we mean by this is we have seen a rise in the price of financial assets without a corresponding increase in goods and services inflation for over a decade (at least by the current methodology used to measure). We have effectively seen equity returns driven primarily by multiple expansion (as opposed to earnings growth). What appears to be occurring now is an increased awareness that the latter may not be a possibility going forward.

Why?

It seems that inflation, with some significant help from Covid and fiscal expansion, has now seeped through into the real economy. This significantly limits the ability of central banks to maintain status quo arrangements and increases the possibility of significant tightening. This is the simple explanation of the selloff. Growth via multiple expansion is no longer a viable option, hence the carnage of highflying tech stocks and the NASDAQ.

Was/is the reaction rational?

In some ways, yes. But, looking through the noise, we see an alternative perspective. We base this perspective on two key notions:

1 – Assuming that the goods and services inflation is here to stay, can policy makers actually be that aggressive given the demographics across the developed world and the significant debt burden undertaken by governments since 2008 and coming to a head with Covid? The debt servicing burden and implications are significant. We say no, it may seem aggressive given the low base we are coming from but nominal rates are still likely to be below inflation. By the way, this has been a trend ever since the GFC, the below graph shows the effective Fed Funds Rate against CPI.

Source: Federal Reserve Bank of St Louis

(Given the changes to consumption patterns, excluding Food and Energy gives a better comparison. This chart shows that the effective Fed Funds Rate has been kept below rate of inflation since GFC.)

2 – Given that this is a supply shock as opposed a demand driven inflationary pressure, we see very little room for manoeuvre unless central bankers wish to hike their way into a recession. After the effort put in to avoid one over the course of the last two years, we find this implausible. That said, there is always a possibility of policy error so we cant totally rule it out.

So, here is an alternative perspective. If nominal rates continue to remain below headline inflation, real yields are in fact negative. In that environment it would be a error to go toward traditional fixed income, which leaves cash but if the underlying thesis is secular inflation then that is a surefire way to guarantee negative returns. This leaves us to consider two asset classes, equities and real assets. Equities may not see the same degree of multiple expansion but earnings (contingent on where one is looking) should be able to keep up with inflation though wage pressures may dent overall profitability. Real assets, here we are thinking commercial or agricultural property (not residential as this is one that is incredibly sensitive to even small rises in nominal rates), that have cash flows able to move in line with CPI should put investors in good stead.

So there is our perspective, its not particularly popular at the moment but it may be that the indiscriminate selling is a little overdone. The high P/E market darlings to date, warranted. But days like those we have seen recently make us think that opportunities could be just around the corner.

Does that mean we are against holding cash?

Definitely not. But one way to look at it is to view cash as a put option against the market with the decline in value in real terms as the premia. Bargains are popping up.

With rates on the rise we turn to a pressing issue facing economies the world over; global debt. What will the implications be and is there a way to prepare for it?

We begin this weeks article on global debt with a story. This is the story of Sri Lanka which has seen and continues to see significant turmoil driven in no small part by their government embarking on a series of reckless fiscal spending measures over decades. While this was ostensibly blamed on the Covid crisis, a little investigation reveals a multi-decade story of populist measures, reckless tax cuts (not accounted for), and indebtedness to foreign powers, including China. What are the results? A government that has finally realised that it is not able to meet its basic obligations, civil unrest, the resignation of a Prime Minister and cabinet with an embattled head of state unable to dig himself out of a hole. Take a step back and one can see this story starting to play out on a much grander scale.

Think Latin America, emerging markets in Africa and across South East Asia. So, why is this an issue now? Well, unprecedented Covid-related measures have seen this peak. As the US Fed reverses course after decades of largesse (along with the ECB), we see the other impact of rising interest rates; increased debt servicing costs. This is likely to lead to austerity.

2020 marked the largest one-year debt surge since WWII, Global public debt rising to approx. US $226tn (global GDP was $94.935tn in 2021). Was this Covid and was it inevitable?

Looking at the rationale for government expenditure, current wisdom (decidedly Keynsian) formulated following the Great Depression asked a simple question: Can governments intervene to smooth out business cycles and, if so, how? The solution posited is simple, save during good times via increased tax receipts and budget balance, which allows the economy to not overheat and consequently cause inflation, while the converse is true during recessionary periods. Expenditure in this sense implies creating money supply in whatever form, the famous quote in Keynes’ General Theory of Employment, Interest and Money is:

”If the Treasury were to fill old bottles with banknotes, bury them at suitable depths in disused coal mines which are then filled up to the surface with town rubbish, and leave to the private enterprise…to dig the notes up again…there need be no more unemployment and, with the help of the repercussions, the real income of the community…would probably become a good deal greater than it is.”

It seems that governments have taken this to heart in a literal sense (which may not have been the intention). What seemingly wasn’t taken onboard is the prescription for the good times. This led to a scenario where even the now so-called glorious 80s where, for example, US Federal Government deficits averaged around 4% p.a. (compared to 2% in the previously inflationary period). More recently, the tax cuts announced under the Trump administration (in the middle of one of the longest economic expansions we’ve seen) saw gasoline added to the fire. Is this a purely American phenomenon?

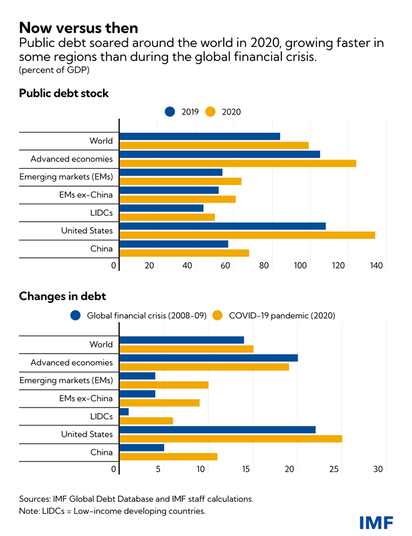

Definitely not. This was a truly global trend that peaked in the 2020 period. It also happened to be true that the inequities of the financial system were clearly visible, emerging markets continued to face financing restraints that were not felt by their developed counterparts despite seemingly similar irresponsible fiscal policies (with the exception of the GFC/Great Recession, where it was somewhat warranted). The below chart shows the actual composition of public sector debt.

Source: IMF

Assuming that developed economies, and the elephant in the room the Federal Reserve, were to go on a hiking cycle with concerns around inflation, what is the outcome? The results are arguably not equal. Ask yourself why, despite a high inflationary print, US treasuries continue to hold their safe-haven status? Public sector debt is not the same as private after all, not when that debt is issued in your own currency. It’s the reason Chinese corporates feel significant pain every time the Fed raises rates or EMs face even greater pain overall.

We come to our first point. The answer to whether increases to the Fed Funds Rate or raises by the ECB reduce overall debt is not in fact clear. Unless nations move toward austerity, which doesn’t conversely impact their GDP in a way to significantly reduce tax receipts, all we may see is a ballooning of deficits. This is especially true of asymmetric relationships like Italy or Spain in the Eurozone or LATAM nations with US denominated issuance. They may just be faced with both inflation and ballooning deficits. A double whammy.

Following on from this, we can see a caveat. Debt may decrease via an avenue that may be unpalatable to most central banks, default. Unlike the GFC, this is not private sector but sovereign default risk. Even for those markets that have issued debt in their own currency, there is a great degree of risk that yields may skyrocket beyond manageable levels so that ever increasing issuance is required, adding to inflation. And so it goes in a vicious cycle (the most recent and obvious example of this being Turkey).

The above is the likely story of EMs and developing economies but what about so-called developed economies like the US, Eurozone and Australia.

Here the outcomes are a little more nuanced. Take the US for example, an increase in the Fed Funds rate may increase debt servicing costs but, because of the dynamics above, it may be that the subsequent rise in the USD (remember fiat is a relative game) might lead to further deterioration of the trade balance (by making imports cheaper). Thus exacerbating unemployment and assuming a further feedback loop into the political space, faced with two year election cycles, increase public sector deficits which may then perversely create further inflation.

In Australia the situation may require an even better and more nuanced dance. The majority of the debt in this country is household, driven by the residential market. Even incremental increases to the cash rate can have disproportionate impacts upon debt servicing abilities. Even assuming lenders have adhered to the golden rule of ensuring that mortgage payments only make up 28% of the households disposable income, a 50% increase in this cost (i.e. what an increase of 3% to 4.5% in the mortgage rate) would be seriously detrimental to overall consumer health.

So, will debt decrease? Under the current trajectory and policy environment (which should theoretically decrease it), on a balance of probabilities, we are likely to see an increase. This is with the cherry on top that it may not actually tackle inflation as hoped.

Is there a way out?

Using history to try navigate in uncharted territories is always a dangerous strategy. Looking to the 50s where the US, coming out of WWII, saw its debt decrease from a staggering 110% in 1945 to around 50% by 1959; how though?

Mainstream thought suggests that it was immense fiscal discipline but lets look at the numbers. The Fed effectively pegged the short rates and continued to actively cap long-term yields at 2.5% until the spring of 1951. What was the CPI over the same period? An average of 6.5% p.a.. Wage controls were dismantled and, when they kept up with rises in inflation, government receipts increased. At a deeply negative real yield for close to 15 years, it doesn’t take long before it was decreased.

But what about the global sphere?

History buffs may be familiar with the Bretton Woods Agreement that effectively ensured a certain degree of coordination between most of the so-called free markets through the maintenance of the peg to gold. This ensured that, despite the immense amount of capital required in the reconstruction effort both in Japan and Europe, that nations saw similar declines. There was no default. There was no Great Depression. What was required was great degree of coordination.

For the investor, what’s the point of knowing all that?

If we can assume that Covid measures have significantly increased risks to the global financial system in the form of sovereign default risk, debt has ballooned out and the only way is through financial repression (even if it’s not in the immediate term). Then we can safely assume which asset class provides the biggest risk: bonds (including sovereigns & Cash). At the same time, we can also look at those which provide the best possibilities for preservation of capital. We’re looking for any asset with two attributes; 1) that can take advantage of financial repression to ascertain capital cheaply (at least in real terms) and 2) have bargaining power where increases to cost of production can be passed on to consumers. On the second point we include property in the agricultural or commercial space which can generate cash-flow at pace with CPI, allocations to equities like healthcare, infrastructure, defense and consumer staples. The only exception to this, in our view, are businesses or sectors that are likely to benefit from increased government intervention Here we are looking at those linked to the green transition or transportation infrastructure as well as associated industries, including materials supply.

This week we continue our examination of utility markets. Last week we looked at prices and what has been driving them higher, this week we look to one company in the sector that has also been all over the headlines, AGL (AGL.ASX).

By now we’re quite sure that most investors would be somewhat familiar with the AGL story, a story that has now led to the resignation of four board members and the CEO while leaving the company in a state of flux. This security offers up a number of different narratives; a prime example of management incompetence, an illustration of the rather messy transition in the broader energy markets and finally perhaps even an opportunity.

We can only describe the strategy and activities undertaken by the now previous management as a painful bungle. Last week we described some of the challenges that are inherent in the sector both from a regulatory and operational perspective. AGL, a business encumbered with legacy coal power generation assets and thus significant greenhouse gas emissions (i.e. 10% of the nation’s total), was always going to be a tough proposition for any management team to navigate. Fundamentally, the business needs to address two issues. First, to ensure reasonable cost of capital given the lack of investor appetite for fossil fuels based exposures going forward and, the second, to transition towards a more sustainable portfolio mix. Given the majority of AGL’s energy mix is coal based and the declining profitability of the sector, speed being of the essence may also be considered a third factor.

So, how did AGL perform?

The business seemed to have a plan to begin with, hiring an outsider in the form Andy Vesey. He formulated a plan to address the everchanging business conditions but apparently that was where it stopped. He was ousted pre-emptively with a helping hand from the nation’s Treasurer at the time, Fryndenberg. Vesey was replaced by Brett Redman who seemed to move the company in the other direction, doubling down on the existing coal exposure and extending the life of the producer plants. In our overview of the market last week, we did mention that this is one sector that continues to have outsized political influence. This begs the question of the rationale for matching a potentially multidecade strategy to suit the requirements of stakeholders with a much shorter warranty. Nevertheless, we look to the results.

Through all this, management continued to fail to invest meaningfully in the next phase of the industry. Coal may have been cheaper but was it the future?

AGL posted a record $2.27bn hit to the bottom line in February 2021 with the cherry being an unprecedented shareholder revolt, 55% supporting a motion to set climate targets in line with the Paris Climate Accords. Management shortly thereafter came up with an innovative solution which was to split away the coal assets from the retail business. Supposedly refocusing the business and make the transition easier. Going back to our dual targets and lowering the cost of capital, this was to apparently make it easier to ascertain liquidity for the retail business which could then focus on shifting toward renewables. That is, since it would no longer be encumbered by coal assets it was reasoned that bankers would be more amenable to injecting liquidity. Unfortunately for management, shareholders took a similar view to us on the idea of duplicating functions and dispensing with the potential of using cashflows from the retail business to help with the transition. All this and shareholders continued to see the pain. The board continued to disregard concerns around the proposed demerger and kept on its path.

Despite the continued and relentless fall in both profits and shareprice, the only statement of note from management was that, according to CEO Brett Rodman, there was and continues to be ‘considerable uncertainty’ of the company’s operations. If shareholders were not content on that statement, Peter Botten, then the Chair, graciously admitted that leadership had not been able to factor in the sheer scale and speed of the changes that have occurred in the sector.

Source: Google Finance

Enter MCB.

It is within this context that Mike Cannon-Brookes made his initial failed bid for the business. His ideas were clear, he was intent on speeding up the transition away from fossil fuels and he made a play for one of the largest of the lot. While we disagree with what can only be considered a ridiculously low offer, the silver lining was to put a decidedly incompetent management team and board on the backfoot. Despite shareholders consistently voicing concerns about the direction of the company and the decisions being made, the previous board and CEO showed a blatant contempt for the owners of the business they work for. There isn’t really another way to describe it.

After the initial rebuff and much ado, Cannon-Brookes took an alternative route to shaking up the business. He effectively became the largest shareholder in the company and convinced his fellow investors, both institutional and retail alike, to oppose the de-merger while at the same time collecting some scalps in the form of four directors, the Chair and the CEO.

After providing us with a perfect example of management incompetence and the broader bungled energy transition, what Cannon-Brookes will actually seek to do next with AGL is still a question for the market. Herein lies the potential opportunity. We’ll have to wait and see.

Disclaimer: TAMIM currently holds AGL (AGL.ASX) in a number of income-focussed individually managed account portfolios.

This week we have a trio of guest contributors. All three were given an ASX-listed stock to write briefly on; the stock in question is former market darling The a2 Milk Company (A2M.ASX).

The a2 Milk Company (A2M.ASX)

Source: Google Finance

View #1

As America’s infant formula shortage hits the headlines, investors are seeking to trade the news and capitalise on the U.S.’ need to import formula.

The nationwide formula shortage was created by a shutdown of Abbott Nutrition’s plant due to contamination issues, which accounted for +40% of the market, along with ongoing pandemic-related supply chain issues. In response, the Food and Drug Administration (FDA) is fast-tracking approvals to import infant formula.

Bubs Australia (BUB.ASX) bagged a widely reported deal to provide 27.5 million bottles of infant formula to the U.S. government, as tweeted by President Biden. The stock rallied 40% in response.

With hopes of replicating these gains, investors may now be looking to Bubs’ peers.

The a2 Milk Company Limited (A2M.ASX) is one that’s making watchlists. The company, which sells milk products containing the a2 protein type, has also applied to the FDA to supply formula.

Yet so far, of the 26 companies that have applied to import tins, only two have been approved. And, as of this week, Abbott’s plant is back up and running so there is little certainty around how long the supply issues will last.

I won’t speculate on whether the FDA will grant a2 Milk approval — that would make it one for the punters.

Investors, on the other hand, should evaluate a2 Milk on its current operations. If a U.S. government deal does eventuate, it would come as a bonus (although given its market cap, the relative upside is smaller than Bubs’), rather than a reason to invest.

On that basis, a2 Milk is not without issues.

The company generates around half of its revenues from China, presenting the usual political and legislative risks, plus challenges such as a declining birth-rate and a government push to lift domestic infant formula production.

The share price is at 5-year lows and has been in a downtrend since peaking two years ago. Rather than offering value, its earnings have also sharply declined over that period, and it is trading on a PE ratio of 142x, as compared to the industry’s ~28x.

The author does not hold any positions in the company.

View #2

Most that have followed the ASX for the past 5+ years know what The a2 Milk Company (A2M.ASX) do. In that time A2M has gone from market darling to one of the most disliked stocks on the ASX. A2M was one of the few stocks to hold up well (relatively) during the initial Covid selloff, however the market was overlooking the fact that a key driver of their business to date was international students from China buying up baby formula and sending it home, an arbitrage that hedge funds would be jealous of. Without the usual influx of new and returning international students, A2M has suffered.

In 2020 the A2M Chairman was seen selling shares just before an earnings downgrade. This is a massive red flag for shareholders and understandably sparked huge controversy. More recently, there was a class-action lawsuit brought against A2M on behalf of shareholders as a result of their poor governance and disclosure. A2M are also experiencing inflation headwinds as input costs rise.

There is a massive shortage of baby formula in the US and competitor Bubs (BUB.ASX) has been a huge beneficiary, winning a deal to supply 1.25m tins of formula to the US. A2M hopes to join BUB and recently submitted an application to the FDA. This is awaiting approval and could be a short-term catalyst to boost A2M’s falling share price.

A2M are a shadow of the business they were pre-Covid, suffering numerous setbacks since 2019. There is a potential short-term catalyst in winning a contract to supply formula and they should see a boost as international students return. That said, it’s hard to see much real upside. A2M will begin to taper on marketing costs which should see boosts to the bottom line but it would be a hold/sell. By no means would it necessarily be a short but, looking at it from an opportunity cost perspective, there are far better opportunities out there.

Just an opinion, make sure you do your own research!

The author does not hold any positions in the company.

View #3

One to put out to pasture?

A2M produces and sells liquid and infant formula milk (IFM) from cows who produce only the A2 protein (supposedly gentler digestively), as opposed to those who produce both. This is the company’s key differentiator and justification for premium pricing.

Key markets: China (46% of revenue); ANZ (43%); USA (5%) and the remainder to other. IMF is 71% of total revenue.

Historically, the Company benefited greatly from the “Daigou” trade into China, which is individuals physically transporting the product via travel to China. While the Company worked on official channels and distribution, its “dirty secret” was its heavy reliance on Daigou which was brutally exposed by the onset of the pandemic when borders were closed to non-essential travel. The Company hasn’t recovered from this and was required to take inventory write-downs and the subsequent fall in the share price has led to a class action lawsuit.

Results for H1 FY22 compared to H1FY21 revealed 2.5% decrease in revenue to NZ$661m but a 45% decline in EBITDA to NZ$98m due to the significant marketing spend required for sales through official channels. At the H1 FY22 run rate, that is an 8 June 2022 EV/EBITDA multiple of ~16x (based on AUD values).

In July 2021 the Company closed the acquisition of 75% of Mataura Valley Milk, a NZ dairy nutrition business, for NZ$268m. For the five months to 31 Dec 2021 it contributed a NZ$10m EBITDA loss on NZ$39m of revenue.

The Company has guided to increased revenue growth in FY22 H2 but, critically, not a corresponding increase in earnings. This combined with a slowing birth rate in China, a non-performing acquisition and the distraction of three class action lawsuits means, on a multiple of 16x, it is one to avoid until earnings growth can be demonstrated.

The author does not hold any positions in the company.

This week we have a pair of guest contributors. Both were given an ASX-listed stock to write briefly on; the stock in question is agricultural Nufarm (NUF.ASX).

Nufarm (NUF.ASX)

Source: Google Finance

View #1

Nufarm, and more broadly the agriculture sector is going through a notable purple patch. Inventories of grain and seed are at their lowest relative levels in decades due to an unusual combination of poor growing conditions, supply chain bottlenecks and labour constraints. As a result, demand for Nufarm’s crop protection and seed technology has risen rapidly, with the business increasing underlying earnings by 41% in the first half of FY22.

Any short-term reprieve to the supply glut looks unlikely. Protectionist rhetoric has ramped up, particularly in developing nations where food security is a key priority. India, which holds 10% of global grain reserves, recently banned exports of wheat. Meanwhile, Russia’s invasion of Ukraine has led to gridlock in the Black Sea, placing further upward pressure on prices.

The long-term thesis for Nufarm is also positive. Per the United Nations, the world will need to feed on average an extra 60 million mouths per year until 2060. With negligible cropland growth, farmers will rely on double planting and herbicide improvements to increase yields. While still nascent in its adoption, the company has developed the first plant-based Omega-3 which is expected to be a major growth opportunity.

Despite the favourable tailwinds supporting Nufarm, investors should be cautious over-extrapolating current market conditions. Agriculture remains a cyclical industry prone to peaks and troughs. Corn, soybean and wheat futures curves are in backwardation (when the current price is higher than prices in the futures market), implying an eventual return to normalcy as weather extremities and logistic constraints abate. Subsequently, management has flagged a weaker second-half after buoyant grain prices pulled forward first half sales.

Trading on an earnings multiple of 15, Nufarm is neither cheap nor expensive. If the current market tightness persists, Nufarm will continue to outperform. However, investors need to be cognisant of initiating a position at the top of the cycle.

The author does not hold any positions in the company.

View #2

Nufarm (NUF.ASX) is an agricultural chemicals company headquartered in Australia. As the Ukraine/Russia crisis seemingly continues with no end in sight and with Western sanctions likely to continue over the long-run, Nufarm is a security that potentially stands to benefit from the turbulence.

The Ukraine invasion has placed immense pressure upon agricultural commodities worldwide. Given the centrality of both nations to the global supply of wheat and canola as well as broadbased agricultural commodities, this scenario has had a twofold impact. The first, forcing cultivation of those essentials and, secondly, a resultant increase in demand for fertilizer and biofuels (given the higher oil price) to levels not seen since the early to late 2000s post-Iraq invasion. Assuming this scenario and the associated increases to the Food Price Index (FPI) drags on, Nufarm is one company that stands to benefit.

Broadly speaking, the company operates in two categories: crop protection (i.e. herbicides etc) and crop/seed technology. Across both these categories we have seen immense global demand. Revenue was up to AU $2.16bn in 1H22 (+31% compared to 1H21) while EBIDTA showed an increase of +41% to AU $330m. The business has been prudent in taking advantage of a lower interest rate environment over the last year, saving 9% in interest expense while decreasing net debt by 6%. The numbers reveal another important consideration: the differential in the increase in revenue vs EBIDTA indicates an expanding margin despite a challenging environment for logistics costs. Dividends have also been reinstated at 4c/s, the overall yield to be approx. 2.3% p.a.

Could this be a buy? Across every category the business operates in we see potential for expanded margins. This includes canola (Russia is the 5th largest producer globally), sunflower (Ukraine being the worlds largest producer) and carinata (an effective biofuel, important given the price of Brent). The associated expansion of margins should more than offset any disruptions and increases to supply chain costs. This is a dividend growth story and, using the 2000s as a model (when the oil price and FPI increased along a similar trajectory), we could see high double digit growth in both earnings and dividends over the next decade.

The author does not hold any positions in the company.

Source: IMF

Source: IMF