Ron Shamgar provides an update on a number of the companies held in TAMIM’s Australian equities portfolios. This is an excerpt from the January 2021 TAMIM Fund: Australia All Cap monthly report, you can access the full report here.

Note: Some of these stocks may have released results since publication of this report.

Healthia (HLA.ASX) provided a strong trading update and guidance for 1H21 with revenues up 45% to $64m and NPATA up 106% to $5m. Organic revenue growth of 14.5% was impressive and partially a result of pent-up demand for physio and podiatry services from the Covid lockdowns. Pleasingly the company has recruited 60 undergraduate health professionals commencing in 2021, a good sign of continued organic growth. We value HLA at $2.50.

Readytech (RDY.ASX) announced the finalised agreement to acquire OpenOffice and revised terms due to the business being shortlisted to win a $5m SaaS contract with a government agency. This highlights the quality of the OpenOffice growth prospects. We see RDY as a candidate for a profit upgrade in upcoming results. We see its major private equity shareholder selling down post-results as a positive for a share price re-rate. RDY is one of the cheapest software companies on the ASX and we see it valued at $2.80.

National Tyre & Wheel (NTD.ASX) provided another strong trading update and its third profit upgrade of the half. EBITDA is now on track for $15m in 1H. We estimate FY21 EPS of 13 cents and an interim dividend of 2 cents. The acquisition of Tyres4U is benefitting the company with good demand in the agricultural and heavy machinery sectors. NTD is a real covid winner, as border closures over the next 1-2 years will continue to see elevated demand for domestic travel and thus tyre and wheel servicing. We value NTD at $1.50.

Market freaking out about $NTD losing its distribution agreement for Cooper tyres have not read slide 11 carefully □

It clearly states the agreement is locked in until Sep 2027 □

That’s many years of profits and cash to come their way and enough time to diversify away □

Smartpay (SMP.ASX) continues to grow its Australian terminal business with transacting terminals at the end of December 2020 numbering 5,775 with quality new merchants added, higher margins and increased total transaction values. The current annualised run rate for revenue is now at $24m, with the company adding approximately 500 new terminals a month. Recent connectivity issues with its main competitor, Tyro (TYR.ASX), are only accelerating growth. We believe SMP is on track for group revenues of $100m within three years. We also believe corporate activity may emerge again later this year. Our valuation is $1.30.

Aussie Broadband (ABB.ASX) provided a trading update that was significantly ahead of prospectus forecasts. Residential broadband customers were up 86% to 313k connections and business customers exceeding forecasts, up 113% to 29.4k. Management is guiding to 1H21 EBITDA of $8.5m, which is what market analysts had for the full 2021 year. We believe ABB is taking significant market share from competitors while offering excellent customer service. Business customer connections are adding higher margin revenue. We value ABB at over $3.50.

Humm Group (HUM.ASX) is now officially the most profitable BNPL company in Australia and possibly the world. Management has given guidance of 1H cash NPAT of $43m, up 25% on the prior period. 2H of year will see increased marketing costs and investment into the entering of two new international markets. We estimate that HUM will achieve NPAT of approximately $70m for FY21 and is trading on a PE of 9x. Unfortunately, HUM is extremely profitable and investors valuing BNPL companies are ascribing higher valuations to their loss-making competitors. Eventually that bizarre paradigm will shift and the stock will re-rate to our estimated valuation of $2.00+.

Disclaimer: All stocks highlighted in this article are held in TAMIM portfolios.

This week we take a look at three stocks that are both defensive in nature but still in their high growth emerging phase of their business evolution. All stocks are high conviction holdings in the TAMIM Fund: Australia All Cap portfolio.

Authors: Ron Shamgar

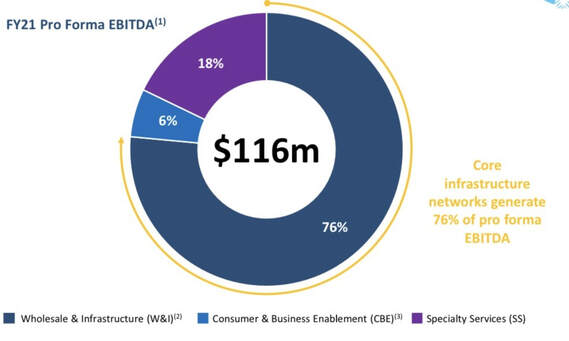

Unity group (UWL.ASX) is our top pick for 2021 and not so coincidentally one of our largest holdings. In our mind, owning UWL is like owning a mini version of the NBN but with better growth prospects. 75% of group revenues come from fibre services to residential Greenfield developments. We believe fibre should be viewed as a core infrastructure service by investors, one that is defensive and has a very long use life.

Source: UWL company filings

Since UWL has 18% market share versus NBN in its sector, we think the stock should be valued more like a core infrastructure asset rather than a telco. UWL recently acquired the Telstra Velocity fibre asset for $180m. This will add Telstra as an internet service provider on the network and will increase group EBITDA to $120m. UWL is currently trading on a one-year forward EBITDA multiple of 12x but we believe it should be closer to 15x. Our valuation is approximately $2.50, so we see another 30% of potential upside.

Smartpay (SMP.ASX) is a high growth payments and terminal provider. By now we all know that Covid-19 further accelerated the take up of electronic payments and, like its bigger competitor Tyro (TYR.ASX), SMP has benefited accordingly. The merchant terminal market in Australia is around one million terminals and growing at 3% p.a.. About 30,000 new terminals are added each year and the banks dominate 90% of the market, followed by TYR (approximately 5%) and then SMP with about 5000 terminals of their own.

Source: SMP company filings

There is a pool of about 300 000 small merchants that SMP is targeting. On their current run rate SMP is adding over 5,000 terminals p.a.. Every 5000 terminals equates to approximately $20m of annual recurring revenue. Recently TYR has been having a serious connectivity issue with its terminals and this provides SMP with a unique opportunity to grab market share. At the moment SMP’s market cap is ~$200m and, based on current growth rates, we believe that SMP can add up to $150m of value to shareholders each year. With the sector consolidating, SMP is a takeover target and we think the stock will double over the course of 2021.

Healthia (HLA.ASX) is an allied health rollup of podiatry, physiotherapy and optometry clinics around Australia. The business plays into thematic focused on the aging demographic around the country with 650 Australians turning 60+ every day. Accordingly, we see further increased demand for HLA services. We estimate that HLA is on track for $180m revenue and $40m of EBITDA in Financial Year 2022.

Source: HLA company filings

So why do we like HLA:

Management are ex-Greencross (GXL, now privately held), which was a very successful vet clinics roll up that eventually got acquired and delivered significant value to shareholders.

HLA has now hit scale financially and has delivered a track record of execution since listing over two years ago.

The sector is consolidating. We see HLA as interesting because they could be both an acquirer and/or a potential takeover target in future.

Lastly but most importantly, HLA is cheap. Trading on 11.5x PE multiple, 6x EV/EBITDA multiple, and offering a 5% gross dividend yield. We value HLA at approximately $2.50

What an eventful year 2020 was! But with a change in administration Stateside we thought we should take a moment to dig out the crystal ball and try to grapple with what this means for us in the year to come and the markets in general. As with all predictions, please take this with a grain of salt.

Author: Sid Ruttala

Some Context

Since the days of FDR, any Presidency or change in administration has been seen and judged on the first hundred days. Roosevelt had inherited issues ranging from a close to collapsed banking system, the Great Depression and a tumultuous time when the fabric of American society was seemingly tearing itself apart. With large segments of the population questioning the notion of capitalism and US institutions. Sounding somewhat familiar? Roosevelt moved with great speed initially, getting the Federal Deposit Insurance Scheme passed through Congress and large swathes of legislation that formed the basis of the “New Deal”. A Presidency that saw the great man give “fireside” speeches and radio broadcasts directly to the American public in order to build back trust and reiterate what had been accomplished in his first hundred days via the now unforgettable broadcast of July 11, 1933.

The Biden administration inherits the nation and the state apparatus in similarly tumultuous times. Domestically, the nation is seeing some of highest unemployment since the GFC, a divided political landscape, a crippled economy, new debt issued since the advent of Covid-19 reaching the tune of 27% of pre-crisis GDP. Foreign policy-wise an expansionist China, a Russia unbalanced by protests whose cooperation is still required for its foreign policy agenda, allies who have been left in limbo by the former Tweeter in Chief and will inevitably consider any deals inked with the current administration up for debate by the time the next one comes along.

With this in mind, we come to the present. To quote Roosevelt himself, “The more you know about the past, the better prepared you are for the future.” Like Roosevelt before him, Biden too will look to act fast. The vast array of new incentives will focus on domestic issues including boosting unemployment, infrastructure spending and tackling climate change which remains a central issue especially to those further to the left of the party. So what does this mean for Australia and the Australian investor?

US Senate Committee on The Budget Chair Bernie Sanders at the Biden inauguration

Boosting Domestic AD (Aggregate Demand) & Employment

Many of the recent headlines have been dominated by the sheer scale of the proposed stimulus bill (to the tune of US $1.9tn), something that has already seen substantial pushback from the Republicans. Many have consistently said that, given the fact that the current $300 weekly unemployment benefit expires in Mid-March, for the sake of expediency and given the lack of Republican support we might see a much watered-down version of the same being passed. This is because in order for any legislation to be filibuster proof in the Senate, the numbers required are around 60 votes and not the usual 51 majority. For those of you unaware of what this means, the simplest explanation is that there is no time-limit on how long a senator can spend on speaking on an issue (any issue, a Senator could read fairy tales if he/she chose). If a cohort of the Senate wanted to block certain legislation, they could choose to speak on any topic they chose for an indefinite period of time one by one, blocking said legislation. That is, in the absence of a three-fifths majority (i.e. 60 votes) bringing the debate to a close by invoking cloture. Given the time constraints, some commentators have assumed that there will be an inevitable watering down in order for legislation to pass.I, however, would make the call that legislation in the first hundred days will be speedy and spending bills will be passed in Democrat favour irrespective of the filibuster rules. In the case of the budget, the bill will simply be put to “reconciliation” whereby a certain committee, in this instance the US Senate Committee on The Budget, can be called upon to “change spending, revenues, or deficits by specific amounts.” The committee puts together the bill with an ability to pass with 51 votes with the newly minted VP Kamala Harris breaking any tie. By the way, guess who happens to be the new Chair of the Budget Committee. None other than the internet’s favourite Senator from Vermont, Bernie Sanders. We all know how the Honourable Senator Sanders feels when it comes to budgets (and ensuring a steady supply of welfare to the American people).

\We will therefore likely see the requisite stimulus bill passed with potentially more to come. While Covid will continue to wreak havoc on large parts of the economy, the stimulus we expect should feed through into underlying Aggregate Demand and Expenditure within Q4 this year (given the lag time). With vaccine rollout underway we are likely to see a resurgence of pent up demand towards the backend of this year and first half of next year (in the absence of changes to Fed policy stances).

It was interesting to us that Biden’s pick for Treasury was Janet Yellen and much has been said about her subsequent wording when it came to USD and fiscal deficits. We see her interviews as validation of our view that not only will fiscal deficits continue to be blown out, but we are likely to continue to see policy makers prop up domestic demand at the expense of the US dollar. This is a trade off. To put it bluntly, this new focus on domestic demand will likely see a weakening of the USD in the medium to long term as well as new deficit spending, effectively being underwritten by the Fed. The trade off is effectively trashing the US dollar or the US economy.

What was rather telling was the fact that Ms. Yellen has clearly indicated that a focus will be placed on nations trying to manipulate their own currencies for commercial benefit, an eerily Trumpian policy stance. This seemingly innocuous statement was taken by the market to mean a bullish scenario for the USD. What I took away though was an awareness that more QE or movement toward YCC (Yield Curve Control) is likely to be required and the focus has to be on managing the pain when it comes to the inevitable pressures on the US currency.

For the Australian investor, this isn’t necessarily a bad thing given this nation’s reliance upon commodities which, all things equal, have an inverse correlation with the USD. For the currency traders amongst you, this presents the likely scenario that there is a bull case to be made for the AUD on a relative basis. A scenario that leaves our own policy makers some breathing space when it comes to managing inflation and the RBA’s often forgotten mandate of “stability of the currency.”

Infrastructure Spending

Within the whole context of stimulus, this is one area where there actually remains bipartisan support. And for good reason. According to even most optimistic estimates, according to the Council on Foreign Relations, the US infrastructure deficit is to the tune of close to $2tn by the year 2025. Here there are two important names to remember and they are the Secretary for Transport and the Secretary for Energy. The first nominee being Pete Buttigieg and the second being Jennifer Granholm.

Here again, the priorities given by the new administration were telling. Mr. Buttigieg is, again, a rather free-spending democrat but one with a gift for developing consensus. His rather breezy confirmation hearings and speech as pertaining to the ailing transportation infrastructure were taken well across the spectrum. We are likely to see him as a further catalyst for increased spending and given infrastructure is one with quite possibly the greatest fiscal multiplier (i.e. the amount of GDP added for every dollar spent) we will see this remain a focus. Ms. Granholm, previously the Governor for Michigan, has historically prioritised labour and providing jobs to her constituents. Her appointment yet again highlights that the second priority beyond infrastructure is labour. And, by the way, Janet Yellen is not a traditional central banker even when she was at the Fed, coming from a background of labour economics.

Within the context of infrastructure spending, we see continued emphasis on labour markets and green infrastructure in particular. This is especially the case given the pick for the EPA, Michael Regan who has been a career EPA official with brief stints working for the North Carolina Department of Environmental Quality and an NGO, the Environmental Defense Fund. A marked change from the previous administration which first nominated a lifelong critic of the EPA and second a coal lobbyist. This, combined with a nomination of the stature of John Kerry to the newly minted position of Climate Envoy, rejoining the Paris Accord and an Executive Order halting work on the Keystone pipeline, tells us that the life of the shale industry might have just got a little more complex.

This is a sign that is likely to see production and capex tick lower sequentially over the long run, especially given the reluctance of finance to play within the space. A situation likely to see continued upward pressure on the price of the Black Gold. For the Australian investor, Woodside or Horizon anyone? Similarly commodities such as Copper are likely to be further catalyzed with for example, wind turbines requiring 3.6 Tonnes of copper per megawatt generated.

Foreign Policy & Asia in Particular

Perhaps the most important relationship when it comes to foreign policy under the new administration will be the evolution of the Sino-US relationship, a relationship that is likely to determine the 21st Century. But before we go any further, let me tell you a little story. The year is 2008 and Wall Street, along with the rest of the world, is in the throes of the Global Financial Crisis, it was in this time that the Bush administration is preparing for one of the most audacious plans to bail out the financial services sector through the Troubled Asset Relief Program (TARP). However, there is a hurdle. The sheer scale of the project would entail the flooding of the Treasury market and new issuance to finance it. The answer was to send the ambassador in Beijing to ask the government of the day to silently buy up the new issuance. Within the space of a month, the PBOC had bought up close to $700bn in US treasuries.

What the above scenario illustrates is a relationship of mutual reliance (however uncomfortable), the Chinese could not afford to have their largest export market or the global financial system fall over and the US could use back-channels to save face. This scenario is however rapidly changing, initially under the Obama administration with the introduction of the now infamous TPP (Trans-Pacific Partnership) which, though a free trade agreement on face value, was a step in counterbalancing an expansionist China in the region. The tensions peeking under the Trump administration with his America First policy.

Though recent rhetoric by Xi Jinping in Davos placed emphasis upon multilateral cooperation, we somehow doubt that there is appetite in Washington to normalise relations any time soon. As we wrote about in our previous articles around Trump’s ‘trade war’, the question is not about current account surpluses but leadership, in particular leadership of the new industrial revolution (industry 4.0). China’s vision to no longer rely on labour arbitrage (labour is no longer cheap in China) and move up the value chain has created a scenario where American business, which has benefitted (in terms of the bottom-line) and historically erred on the side of caution when it comes to the hawkish policy or rhetoric, has endorsed a more confrontational policy. With Wall Street having close to three lobbyists for every congressman, we have no doubt that there will push for a more confrontational approach.

We will continue to see a disentanglement of supply chains, the building up of spheres of influence (through projects like the Belt and Road Initiative) as well as more aggressive security policy on both sides. Australia will unfortunately have to navigate this with great nuance given that China remains our largest export market and the US remains our largest source of investment. Australia, meet a rock and a hard place. In fact, the process has already begun with Lynas, for example, receiving $60m USD from the Pentagon to build a heavy rare-earths facility in Texas and Australia being seen as key to the US’ supply of commodities essential to the green economy. For the discerning investor however, this creates immense opportunities, creating artificial profits within companies that are seen as vital to the broader foreign and security policy. Think for example of the fact that Weibo has come to dominate the search market in China for the simple reason that Alphabet is unable to compete. Or the subsidies that Tesla continues to receive along with companies such as Boeing. This also happens to be one reason that we don’t see antitrust laws used against the tech giants even though there is probably an argument to be made there.

It is important as investors that we take advantage as the situation evolves, diversify geographically and not get caught up in the hype. Simply put, we do not see normalisation of policy. However, we do see the Biden administration as a reversion to the mean and likely to revive and continue on with the policies of the Obama administration (almost Obama 2.0 when one thinks about it). As for China, much has been said about Chinese expansionism and assertiveness, but my view is to look at it from the opposite perspective. Imagine if one were sitting in Beijing and looking out across the region, the below is what I would see. Military bases from Australia to Japan to South Korea to the Philippines. One would probably have reason to be cynical or at least uncomfortable…

Source: The Coming War on China, 2017, John Pilger

As with most things, there will be winners and there will be losers. It is up to us as investors to stay on top of the news and identify what these companies will be. In Australia, we will have to focus on walking the tightrope between China and the US and the opportunities it presents on both sides. As a materials heavy economy there may be a pivot to cater to the US’ green initiatives including rare-earths, energy (including nuclear). We make the call that given our commodities heavy investment landscape, we call an outperform for the ASX (excluding financials), we are the beginning of a secular commodities bull cycle as both superpowers look to build out their respective infrastructure and resource capacity. This also places us in the nice position of upward catalysts for the AUD and using this as a way to look to invest in sensitive sectors such as Technology outside of Australia and to back both horses (US and Asia).

To wind up the year we decided to take a tongue-in-cheek look at the year that was. There were a number of predictions being widely thrown around by those in the industry to start the year, unfortunately many of them turned out to be unfounded. So, let’s dive into 2019 in review!

Wow, it’s the end of 2019 and, while a full year has passed, it seems like yesterday that the markets were supposedly melting down after a ten year upward trajectory. A meltdown that thankfully never eventuated and (hopefully) will not be forthcoming in the near future. Granted, hope is a rather perverse emotion when it comes to looking at the markets objectively, but then again it is Christmas and we would rather end on an optimistic tone. Below are some predictions for 2019 that we never made but have been everso forthcoming by our esteemed counterparts in not only the financial press but the buy-side at large.

Prediction 1 – Central bank policy will reverse course and normalise

There was a healthy debate on this one in the TAMIM office leading into 2019, ultimately we came to the conclusion (by a narrow majority) that it would not be the case. It would be fair to say that, given Powell’s past and rhetoric in the lead up to taking his place as the Fed chair, most in the industry expected a clear break from the policy of his predecessors. While it did seem to have substance, this did appear rather presumptuous in retrospect. A freeze in the overnight credit markets and a rather bloody market sell-off and it seemed that they blinked immediately. As we have been saying consistently throughout, monetary policy is caught between a rock and a hard place so to speak. They will not only find it exceptionally difficult to reverse course but, in the absence of any catalyst, will find it hard to substantiate a normalisation of rates or the balance sheet.This trajectory/trend has now come closer to home where the RBA not only lowered the cash rate to historically abnormal levels but might very well undertake unconventional measures in the forthcoming year. It seems that Central Bankers having weak legs is a global phenomena. After all, it took Lowe a good two months from categorically ruling out QE to coming down to “maybe, it’s in consideration”. We wait with bated breath for him to throw the ball firmly in the governments’ court and blaming a lack of fiscal stimulus for any market corrections in terms of real assets.

In essence, the pundits were right, they did reverse course but unfortunately for that particular prediction it was a 360 degree turn and the end result is the same old, same old. While it was not called QE, the actions by the Fed in September this year with regards to the Repo markets came quite close to it (as we pointed out). As a gentleman that we were speaking with put it: “If it looks like a duck, swims like a duck and quacks like a duck…”

Prediction 2 – Active Management is dead

Here is one that we never hear the end of. It seems that because of the underperformance of a great deal of active managers in the current market environment, the whole industry is in decline and does not add any value. The problem is, this is contingent on time frame and how you look at it. Yes, value managers have found the current environment quite hard to perform in but that is just one component of the entire active management industry. As we have consistently said, different styles work in different contexts. Try looking at the performance of growth managers over the past ten years. Then it seems the counter argument is over the very long-run, the market outperforms. And here there is substance, because markets can survive centuries but managers unfortunately are constrained by a little thing called lifespan.

For us, maybe it did prove correct. Our benchmark in Asia is up 14.95% and we only did 17.72% (CYTD at 30 November 2019), a negligible performance if you ask me. This is even more so in our domestic equities portfolios where the ASX 300 is up 26.33% in 2019 so far and we have only managed a paltry net return of 53.52% in our Australian All Cap strategy (at 30 November 2019), an even greater gross underperformance. We would formally like to apologise for being foolish enough to attempt active management.

Humor aside, we still firmly believe that (taking away market context) there is always a place for human skill and intellect when it comes to managing portfolios. Think about the market as an ocean with currents, rising and falling tides. The key is, it is all well and good to go up on a rising tide, but it pays not be left standing naked when the tide retreats – that is where a good active manager might help.

So… Active management is dead, long live active management!

Prediction 3 – Trump will act like an absolute statesman as he grows into the role

Alright, no sane person quite made this particular prediction. But in all honesty, the Trump presidency has created significant buying opportunities for the markets. Not for the reason he seems to think but the sheer impact the Tweeter-in-Chief has had on day-to-day market sentiment. The key to understand is that most of it might be noise and look to the fundamentals or the outcomes. In terms of trade, most of the negotiations when it comes to details are ironed out behind closed doors by the likes of Lighthizer and his counterparts in Beijing with, in all seriousness, very little input from the President and we would go so far as to say, intentionally so. The mood of most the chaps at the US State Department is not likely to be nearly as hawkish as the President might like to make it seem.As far as we are concerned they have done an exceptional job in terms of navigating the intricacies of the phase one deal despite their top man seemingly working against them. This issue will not have a short-term solution but will lead to a gradual disentanglement of supply chains which, for the discerning investor, creates massive opportunities. Mayhaps a bit of active management might be required picking the right sectors and companies within them?

Aside from trade, the very nature of the Trump Presidency and its divisiveness is, believe it or not, not necessarily a bad thing. We got the corporate tax cuts and the sugar high as a result, deregulation that is (in the very near term) great for the markets. Sometimes, politicians not being able to do much as a result of legislative gridlock is a blessing in disguise. Mayhaps, the logic here is, the markets got what they wanted and might be happy to let Capitol Hill bicker over everything else so that on the flip-side there is at least a guarantee that there won’t be policy shifts that will be detrimental for the markets in the medium-term.

Prediction 4 – The property market is in for downturn

Simply put, nope. Didn’t happen and in the absence of a surprise economic downturn, not likely to happen. Granted, there might be headwinds that lead to certain dislocations, namely fluctuations in credit growth, but property prices are rather sticky even in a downturn. We continue to see steady population growth in metropolitan areas, especially on the Eastern Seaboard and to a lesser extent Tasmania. We might not necessarily achieve the same returns that we have been used to in the past but the quest for yield when the risk-free rate of return (i.e. RBA Cash Rate) is zero-bound should allow the market to steady. In some cases the opposite has been true with some of the best performing sub-groups of the ASX being REITS which have seen their yields compressed but their valuations appreciate to historic levels.We firmly believe that continued consolidation of the property market will create opportunities especially within commercial and industrial contexts. And, as we have demonstrated with our recent property transaction, you can still sustain a reasonable yield on a risk-adjusted basis if you are discerning about the matter.

Prediction 5 – We are in for another GFC

History is an interesting thing. As humans, our minds tell us to look for similarities in various situations in order to draw meaning and provide some semblance of a clue as to what is going on. After all, this is the reason why when we are young and shown a cat we are then able to extrapolate that information and look at other cats and know they are cats. It is why we think of a lion or tiger as a big cat and not a (house) cat as a small lion/tiger, context and reference points are crucial. Same with history, however there is a limit, history rhymes but it does not repeat. It is understandable that people have a sour taste in their mouths following the GFC and what that did to their wealth and savings. Trying to find similarities between now and then and making predictions that, just because there are some correlations, we will have the same outcome is a rather futile exercise. Correlation is not causation as my statistics professor used to say. As the graph below shows, if that were the case, than the rise in average global temperatures is a direct result of the fall in piracy.

That is not to say that we are suggesting there will never be a market correction but trying to time it or predict when it might be is a rather pointless exercise. More people have lost money trying to time the market than they have by staying invested through the tough periods. How many people panicked and went to cash (or a significant cash position) at the beginning of this year? And what did the market return this year? We can learn from history and understand the causes of specific events and identify catalysts that might be similar in nature so as to avoid them. We do so by being rational and reasonable, having a diversified portfolio across geographies and asset classes. When we say that, we are not talking about having a bunch of underperformers that hammer returns but true diversification where one can reasonably justify lower correlation.

We end our little tongue-in-cheek tirade with one final remark:

Markets are great at head-faking people, just when you think you understand them they shape-shift. The key is to enjoy the new shape and, if you can or if you’re really good, see what the next shape might be. If you’re not, just enjoy the spectacle.

Over the past few weeks we have tried to elaborate upon what is turning out to be one of the most interesting and dynamic secular growth stories of the coming decades and perhaps century. And so, we would like to use this article as a conclusion of sorts, namely addressing the why? And more importantly, why now?

Author: Sid Ruttala

If you wish to read the preceding articles, you can find them here:

I won’t beat around the bush any further, let’s get right into it.

Why?

For those of you somewhat familiar with previous articles, you are probably aware of my fascination with Kuhn and the notion of the paradigm shift. The transformations currently occurring across mobility are, in my view, just such a shift. A once in a generation change and opportunity. The fourfold schematic that we’ve elaborated upon so far is a simplistic and I hope effective way to distinguish the opportunities that are available for the discerning investor.

But coming back to the question of why (and it’s not complicated), here are a few numbers:

€20 billion

The amount of penalties that automakers face going into 2021 if they don’t meet new stringent CO2 emission targets9 Countries (and counting)

The number of nations currently discussing the total ban on internal combustion engines by 2030$2.5 trillion

The minimum value of the new ecosystem of businesses and services that are emerging within the segment by 2030

$8 – 10 trillion

The overall opportunity set over the next 50 years.

62%

The percentage of automotives that are used as Robo-Taxis in China (hint as to why this is a game-changer: think about the traditional automobile sales and private ownership).

$1.1 trillion

The most conservative projection for market revenues generated by mobility services in China

900 billion

Total sales of autonomous vehicles (projected to make up 40% of new vehicle sales by 2040).

If the above statistics are not incentive enough for the reluctant investor, have a look at the below video around the Hyperloop and think about the implications for domestic air carriers if such technologies are commercialised.

The point here being that just as the advent of the internet had vast implications in industries ranging from retail to media, the impact of which took anywhere between months and decades to play out, so too will changes in mobility be a thematic. The implications and questions are not limited to whether Tesla is overvalued or not, but what does it cost for me not to have some sort of exposure or at least awareness? You might have exposure to energy, telecommunications or even a supermarket chain, if you think that this thematic wouldn’t impact you, then think again. Taking the supermarket as an example, think for a moment about what it takes to get fresh produce from farm to shelf? For those that aren’t willing to adapt to new technologies and recognise efficiencies within the supply chain, what does their future look like? Think of retailers like Nordstrom or JCPenny. We’re quite sure that most investors in these companies didn’t look to the WWW (World Wide Web) while still in its infancy and see it as a threat to them.

Why Now?

I am not a believer in trying to time the market (I prefer the old-fashioned time in the market), but sometimes it is good to be aware. The best time to have invested in technology stocks would probably have been 2003 after the massive run-up in the dotcom bubble. After the bubble burst, you would’ve bought the capex that had been invested, the R&D and everything that went with it for pennies on the dollar.

1. Business Insider, https://www.businessinsider.com.au/self-driving-cars-at-peak-of-gartners-hype-cycle-2015-8

2. Forbes, https://www.forbes.com/sites/enroute/2018/08/14/autonomous-vehicles-fall-into-the-trough-of-disillusionment-but-thats-good/

3. Business Insider, https://www.businessinsider.com.au/waymo-says-it-will-start-giving-rides-without-safety-drivers-2019-10

My rule of thumb is always this: let someone else pay for the exploration and I would ideally like to buy at a valuation below whatever has been spent.

The mobility segment is at such an inflection point now (though one wouldn’t recognise it just by looking at the price action of Tesla or Nio Inc.). The more adventurous capital has already been spent (think about the $5bn cap raise just committed by Tesla in the past year). Further up the supply chain, across components like semiconductors, we have seen consistent capital outlay and we are beginning to see the commercialisation. This is helped in no small part by existing regulation (catalysed not only by the EU but by now a Democrat win in the US and across every major developed and developing economy, including China) and policy incentives.

The time is now. And if we have another sell-off, get even more aggressive (the adventurous capital is also the most flighty).