This week we return to our Top Twenty series. Six months since our last review, we look to provide an update on the companies. This week, Commonwealth Bank and Westpac. Read on!

Again, a disclaimer before reading further, this is the just first part of my notes on the top twenty securities by market capitalisation. Please also note, this does not necessarily mean that we currently hold any of them, especially given our domestic equities mandates are broadly ASX ex20.

Author: Sid Ruttala

Context

Perhaps one of the most important characteristics of successful investing (in my view) is the ability to accept when you may have gotten something wrong, figure out why and learn. When it comes to the Australian banks, it is one area that I got wrong. For many of you that may be familiar with my previous writings, you may know that I have consistently had a broadly bearish view on the sector given the monetary policy and regulatory environment not only post-covid but pre-covid with the conclusion of the Royal Commission. Much of my previous thesis was predicated upon declining NIM’s (Net Interest Margins) as well as, the (in)ability of the RBA to maintain a positive cash rate.

On both counts the markets have defied expectations. Not only did Lowe maintain the stance of not taking rates negative bound or even 0 as his counterparts globally were so willing to do, the banks have been adept in ascertaining and taking advantage of lower funding costs. This, combined with the Term Funding Facility, has meant that firstly the sector was provided a tailwind of 5bps on the deposit front (which should move further should term deposit rates move downward toward the headline cash rate of 0.1%) and the TFF which added another 4bps.

All this combined with a more than buoyant property market has seen stellar growth in the loan books and has stabilized the Big 4 respective PPOP (pre-provisioning operating profit). On top of this, kudos to the management teams for ensuring that over 80% of the total mortgage book remains variable (de-risking the portfolio). On top of this, the better than expected pickup in economic activity in the broader market, furthered in no small part by the fiscal largesse, has ensured that much of the mortgage deferrals, which were the major issue during much of last year, have been improving considerably. And thankfully, the public with its rather short memory has put the findings of the Royal Commission behind it (thankfully for shareholders that is).

Commonwealth Bank of Australia (CBA.ASX)

Despite management commentary being on the conservative side and provisioning sitting 1.8bn above its scenario modelling, CBA has continued to deliver. Unchanged PPOP, lower bad debts and increased payout ratio (a boon for the dividend starved investor) were the main highlights. Numbers wise, 1H21 cash earnings of $3.886bn, net interest income came in at $9.371bn compared to $9.26bn in the previous half. More importantly costs have been kept in check with the biggest highlight being the strong capital position, standing at 12.6% (this has beat my expectations slightly given that even with the sale of non-core assets I expected 12.5%).

Nevertheless, while the results have surprised me on the upside, the statutory NPAT of $4.877bn AUD (a decline of 20.8%) does show the toll that Covid has placed on the business.

Red Flags & Risks: NIMs continued to fall from 2.04% to 2.01% (above the expectations of 1.8%-2.0% that I gave last year). This will, in my view, stabilise. However, the competitive nature of the mortgage market in this nation will offer considerable headwinds going forward with the potential for downward mortgage repricing. The current valuation also ignores the impact of lower rates and is already focusing on dividend yield.

My Expectations: Cash NPAT will remain broadly flat but the payout ratio should increase in order to catch up. The firm’s recent foray into BNPL, though still in its infancy, shows that management is looking to keep abreast of changes in the economy. The offering of lower charging (1.4% vs. APT’s 3.8%) is unlikely to be enough to eat away at APT’s market share substantially though. What it is likely to do however is further increase customer retention and increase the profitability per customer by offering more holistic services. Its ability to ascertain better credit data gives it a unique advantage over its competitors (though if NAB’s Klarna is anything to go by, this will not be substantive).

Dividend Yield: 4.09% (assuming share price at $88 AUD and a 68% payout ratio – in absolute terms $3.60 AUD per share).

Westpac Banking Corp (WBC.ASX)

This was perhaps one of the bigger surprises of the year so far given WBC’s penchant to be the perennial laggard. Not only were 1Q21 revenues 100bps higher than the previous quarterly, it has been a story of turnaround in every single notable metric. This includes expenses down by 2%, CET1 up by 74bps from the previous quarter (though substantially lower than CBA) and bad debts benefit of $501m. Numbers-wise, statutory net profit was $1.7bn and cash earnings were $1.97bn, up 54%.

While the bank remains substantially less well capitalised when compared to CBA, what has been quite interesting for me was the fact that NIMs stood at 2.06%, not only is this higher than CBA but it is an increase of 3bps from the previous half. It showcased a clear turnaround story in the making for me.

Red Flags & Risks: Much of the recovery is predicated on continued housing growth and continued momentum in the cost cutting measures. The bank is also unique in its concentration of exposure to the NSW housing market compared to the loan books of their competitors.

My Expectations: This is one firm that I have done a complete 180 on in terms of my expectations. Not only did the NIMs improve, as opposed to my forecast last year of 1.6-1.75%, but management has continued to deliver on its cost cutting measures and de-risking its balance sheet. The bad and doubtful debts (BDD) has also continued to see substantial improvements. All round, this is a management story and Peter King has proven me wrong. Apparently appointing insiders in times of upheaval isn’t all that bad after all.

Dividend Yield: Expected yield of 7% (assuming a share price of $24 AUD and a payout ratio in line with 2019).

I remain of the conviction that management are likely to be incentivised to play catch up this year. This remains a better bet then CBA in my view from a dividend perspective.

Next week, NAB and ANZ!

Disclaimer: CBA and WBC are currently held in the TAMIM Australia Equity Income portfolio.

In a previous article, we gave a rationalisation for why, despite seemingly irrational valuations, we remain overweight equities here at TAMIM. This week we continue to explore this but with a caveat, that is the potential for inflation and the reasons why it might pay to be more discerning in your asset allocation. And what are some of the businesses we have invested in to take advantage?

Author: Sid Ruttala

We remain in an environment where leverage continues to grow at a considerable pace. This was perhaps best illustrated by the Archegos fiasco which showcased that, despite the GFC and the regulations that followed, risk was transferred from one area (i.e. namely the banking sector into the shadow banking and non-financial sector). This, combined with a whole generation off new investors seemingly driven by FOMO, should give us pause to take a step back and take time out to think.

Context

Despite the rhetoric coming out off most central banks across the planet (including Stateside), who continue to maintain a view that any inflation is rather transitory and normalisation of policy is unlikely, we would like to take a contrarian approach. No, its not the “this time it is different” line that is a surefire way to pain but rather understanding what has been happening. For the investors amongst you who have lived through the last great recession, you are probably aware off the doomsday-sayers who, at the time, predicted runaway hyperinflation when non-conventional policy was first implemented. But where the so-called pundits got it wrong was, I believe, a fundamental misunderstanding of the way and manner in which QE actually works. So, let us begin with that.

QE is simply put a mechanism by which the central bank effectively buys longer duration assets in return for liquidity into the financial system. For those off you not quite aware of how the financial plumbing works, please refer to my previous article where I did my best to explain in simple terms how the central banking system works and how cash rates are set in practice, you may be in for a surprise (I did get one particular call about the cash rate being taken to zero wrong though).

While QE does increase money supply in theory, it is not in the way in which you’re thinking. When you deposit cash with say ANZ or CBA, the bank is required to pay you interest. The bank has two options in this instance, the first is to lend against said deposit or alternatively buy interest bearing securities, say treasuries for example, which are still considered risk-free, and pay the differential in that. The problem occurs when commercial banks choose the second option and accumulate treasuries since the central bank will effectively swap them again in return for liquidity. And so, the cycle continues and money accumulates within the financial system as opposed to being seen as credit growth in the real economy. This is the reason credit growth across the EU and Japan has been stagnant through much of the last decade, as shown was shown by the first negative mortgages underwritten in Denmark a few years ago.

Unfortunately, what is required in this instance is the continued expansion of deposits despite the low rates. Although money supply seems to grow on face value it is in fact trapped in the financial system, the ultimate liquidity trap that also creates deflationary pressures. Ironically, Australia has avoided this scenario in many ways given the uniqueness and centrality of the property market to our psyche. We arguably created the ultimate “too big to fail” asset bubble, but it got the liquidity out of the commercial banking system.

So, what has this got to do with equities and what we are talking about here? For one thing, this context has also created some rather unforeseen headaches. Ironically, in their fixation to avoid inflation at all costs, the design of QE has created another problem: asset price inflation. More particularly, the lack of return in risk free assets has in many ways pushed liquidity into riskier asset classes. This is perhaps the reason why Credit Suisse and Nomura, both institutions that are domiciled in jurisdictions which have seen this happen, were so willing to take outsized bets on a single entity in Archegos (apart from the magnitude of the counterparty risk not showing up on the balance sheet). The lending, apart from showing up in the real economy, has shown up in margin lending and swaps to date. The below graphs shows margin debt-to-GDP. In Australia’s case this has shown up in household debt-GDP (more important metric given the centrality of property).

Source: thefelderreport.com

So Where to Next?

The case till now sounds as though I am arguing against equities but here is the kicker. It was covid and the related selloff that has made me rather more bullish. Not for the reason you’re thinking, Personally, I’ve never believed in the V-shaped recovery and I don’t kid myself into believing that the world fits such idealised textbook models but rather my argument is predicated on what liquidity is doing and inflation is likely to do. Remember that the central part of my argument is that QE ended up trapping liquidity in the financial system, it did so because there was no mechanism for MS (Money Supply) to enter the real economy which is why we didn’t see core CPI pick up. What happens however when, because of say a pandemic, governments start to enter the spree?

A spree that, given current electoral and geopolitical imperatives, is unlikely to see financed by tax increases (at least on an income tax basis)? When direct stimulus, whether through infrastructure or legislation, puts upward pressure on wages? All this at a time when the biggest deflationary catalyst of the past century (not innovation), China, not only moves up the wage curve but is flexing its geopolitical and economic muscle? So, “we have a localisation of supply chains, increasing share of labor in GDP and liquidity that enters mainstream, including a lot of the new generation of leaders asking for a “bailout” of “mainstreet”. If these aspects aren’t inflationary, one must really ask what is.

Combine this with loose monetary policy, remember central banks (aside from ensuring the stability of the financial system) are also their respective nations’ bankers and (increasingly) primary lenders, and we might have a rather changed investment environment. Why does this make me bullish on equities? Simple, show me a better option to preserve wealth.

How to Invest

Across most of our portfolios we have pivoted away from growth and toward a reflation trade. The high growth stocks that we have become used to might not have it in them to 1) substantiate their valuations; and 2) to continue their trajectory in the face of increased government intervention. The liquidity will continue to grow (there is not much of a choice for the central banks) but it will flow in different directions.

The likely uncertainty around corporate tax (not income, corporate), anti-trust, increasing share of labor in profits and government scrutiny will probably impact the top-end of the market disproportionately, which may just answer the question as to why Mr Bezos was so forthcoming in arguing for a higher tax rate. What looks particularly attractive, even from a valuation perspective, are the so-called old-world industries – sectors like Energy, Real Estate, Consumer Discretionary and Infrastructure – which should not only benefit from the tailwinds of increased consumer demand but are a tried and tested way to hedge inflation. Additionally, they are usually a great way to generate consistent dividend yields. Having said all that, here are a few Energy companies we own.

Exxon Mobil (XOM.NYSE)

With a dividend yield of about 6.3% and P/E of x10.3 Exxon not only looks cheap but, given my conviction on a continued rebound in oil prices through the rest of the year along with supply constraints across US shale production, this is one stock that should be on the radar of any dividend hunter with substantial upside as the company continues to prove its emissions and green credentials (essential for institutional flows with the continued rise of ESG).

Enbridge (ENB.NYSE)

For those of you unaware of the company, Enbridge owns and operates the largest footprint of crude oil and liquid hydrocarbon systems in North America. It has been caught up with some recent political grandstanding with the Governor of Michigan seeking to decommission Line 5, which crisscrosses the Great Lakes, despite Enbridge’s exceptional track-record in safety (it has been operating it since 1953). However, given the support it has received from Trudeau in stating that the issue was non-negotiable we think it is somewhat de-risked, even with the change in the US’ administration. The dividend yield stands at a stellar 6.3% and, perhaps more importantly, a growth rate of 7% for the past ten years (we expect this to continue).

TC Energy (TRP.TSE)

This one’s mainstay is a humungous natural gas pipeline network that now extends to over about 93,000km and transports close to 27% of North America’s LNG demand. It also accounts for 20% of Western Canada’s exports. More importantly, TC Energy has a dividend yield of 7% and a growth rate in the high single digits (9.34% p.a. over the last 5 years).

Disclaimer: All three stocks are held in TAMIM portfolios.

In general, the market and investors like companies that make acquisitions. Acquisitions that add scale and capabilities and are done at attractive valuations can be very accretive to a company. There are some companies that are definitely more acquisitive than others. Whether a company makes a large or small deal, some acquisitions can be more strategically beneficial and transformational than others. With this in mind, we discuss three companies we own that made very strategic deals last week.

Authors: Ron Shamgar

EML Payments (EML.ASX) announced the acquisition of Sentenial and its subsidiary Nuapay for $110m plus a $60m earn out. The deal, funded by partial cash and debt, is not huge in size for EML but significant and transformative as it enables EML to enter the fast-growing open banking sector. Open banking is taking over the payments world; driven by regulatory changes and customer demand. It allows customers and merchants to make instantaneous account to account payments, thereby reducing costs to merchants and fraud. For consumers it is a more convenient way to pay than using a card.

Since open banking is bypassing the card scheme operators like Visa and MasterCard, these payment giants are concerned as some estimates predict that 30% of all future payment revenues will go to the open banking sector. Visa, for example, agreed to acquire leading open banking fintech Plaid in early 2020 for $5.3bn, double their then most recent private valuation. The acquisition was blocked by the competition regulators in January this year. Just three months later Plaid is now valued at $13bn.

Source: EML company filings

For EML, the Sentenial deal adds a key growth vertical that will help them not only disrupt and stay relevant in the payment world, but also add $23m in EBITDA three years from now. We estimate that Sentenial alone adds over $2 per share of value to EML and our valuation increases to over $8.00 as a result. EML is currently a holding in our Australia All Cap portfolio.

Spirit Technology Solutions (ST1.ASX) acquired telco business Nexgen for $50m last week. The deal adds $36m of revenues and $7.5m of EBITDA. More importantly, 80% of revenues are recurring and are contracted for an average of 4.5 years. The combined group will double its SME customer base to 10,000. We see the deal as transformative for ST1 not just because it adds scale and profit. Nexgen brings with it a sales team of 100+ personnel that can now cross sell ST1’s other services to its wide and freshly expanded customer base, offering products for cyber security and data. Following the deal we now estimate ST1 is has run rate revenue of $150m and approximately $20m of EITDA. Our valuation is 55 cents. ST1 is currently a holding in our Australia All Cap portfolio.

Source: ST1 company filings

SG Fleet (SGF.ASX) announced the acquisition of one of its largest competitors in Australia, Leaseplan. The deal is transformative as it creates a fleet management and car leasing group with 250,000 vehicles under management. Management is estimating $20m worth of cost synergies over the first three years which in turn will be 20% cash EPS accretive for shareholders. The deal will see the combined group become by far the largest player in the local Australian and New Zealand market, managing approximately double the number of vehicles of to their nearest competitor.

Source: SGF company filings

By adding Leaseplan, SGF improves its recurring revenue profile to 70% of group sales. We believe this will command a higher valuation multiple from investors over time. We value SGF at $3.50 and we own the stock in the Small Cap Income portfolio.

Source: SGF company filings

Disclaimer: All three stocks are held in TAMIM portfolios.

Robert Swift takes a look at the shift in language coming from central bankers and finance ministers and, more importantly, the implications for equities and bonds.

Author: Robert Swift

Confirmation bias is a common problem for portfolio managers. You have a thesis and then look only for news flow and data that confirms that thesis.

Since there always lots of news and data available, this bias is commonplace. However sometimes, you’re right and the news flow is supportive because it is meaningful.

One such example now is a subtle shift in language coming from central bankers and finance ministers, representative of a shift in macro policy from monetary to fiscal. For a number of reasons they will never say the last twenty + years of continued monetary incontinence has a) been a mistake and b) a mistake that has gone on too long in the face of evidence that illustrated its shortcomings, but at least we are seeing a shift? We think so at least and have positioned the portfolios accordingly. This has implications for the kind of risks that should be in your portfolios.

Here’s where we think the language has shifted and how it points to more fiscal; and the flip side, a continued steepening of the US yield curve with that of certain other countries to follow.

This is the start of a global paradigm shift or pivot.

John Williams the President of the Federal Reserve Bank of New York, one of the 12 Banks in the Reserve System effectively stated recently – we may have had interest rate policy that unduly benefitted wealthy people.

Janet Yellen, the Treasury Secretary in charge of spending and budgets, stated in selling the $1.9 trillion package to Congress, that with this fiscal package we now have a chance to come out of this recession strongly rather than the anaemic recovery we had from the GFC in 2008. In other words monetary easing alone did ‘naff all’ but raise debts.

And the dog in the night that still doesn’t bark – there was no mention of Yield Curve Control by Jerome Powell in his latest testimony to the House Financial Services Committee in February.

USA Banks’ Supplementary Leverage Ratio or the ability to use Treasuries, was NOT renewed by the Fed, and will end on March 31st. This ability was conferred as part of the Covid response and shows the confidence in the economic recovery. It may also see the banks sell Treasuries.

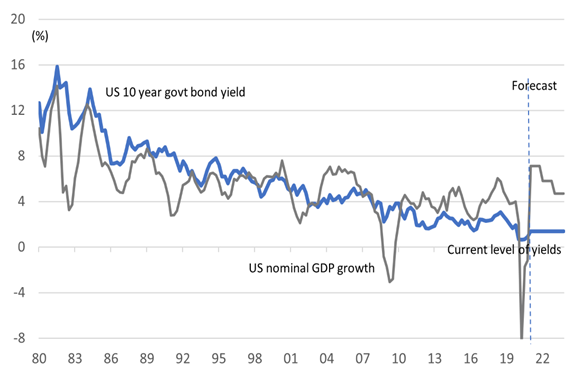

With economic growth at 4, 5, maybe 6% annualised, the 10 year note has no business being at 1.6%. Typically nominal long term bond rates mirror nominal GDP. So, we should be approaching at least 3%?…assuming we revert back to long term trend growth after the easy comparisons are over?

See the chart below from our colleagues at GCIO in Singapore, with whom we run an Asset Allocation service.

Source: GCIO

Japan may be following – we also know that central bankers talk to each other and was it a coincidence that the Bank of Japan, announced recently that it is now pulling back from asset purchase programmes (monetary injections) by removing guidance on ETF buying AND it widens the band for long bond yields albeit by a very small amount

The ECB won’t and so we fully expect the Euro to weaken from here as interest rate spreads widen. This also makes the financing of the 20% US budget deficit (yes that’s right) easier since yield spread will attract foreign buyers of US government paper.

See the chart below for the spread between US and German backed Euro bonds.

Source: Bloomberg

Powell is a genius tight rope walker here. He can’t abuse the notion of fiat money much more than it has been in the last 20+ years. Greenspan, Bernanke and Yellen did that to excess during their tenures, leaving with him with a nasty condrum – the markets need the opium of easy money and a free put option; this dependency is not good for their long term health; weaning them off it may cause a tantrum.

However at 100% debt to GDP he can’t really let rates get too high as he administers ‘cold turkey’ since debt service costs will be usurious as a drain on the budget. By using calming language now and talking UP the economy, he is tempering the inflation threat early; calming the markets about his attitude to fiat money and their elevated prices, and yet letting some element of doubt or risk back in. If you are calmed by his thoughts on inflation and how it isn’t present (oh yeah?), then remember that NO asset price crash has occurred without the CPI or PCE being ‘under control’. Essentially they have to deflate this bubble WHILE stating that the economy is on a sound footing AND prepare us for a shift in macro policy away from what has clearly not worked. We hope we can be talked down calmly.

(If you want an apology about the horrible policy errors conferred on us all, forget it).

(The inflation statistic is a horror show once you try to understand what is in there and frankly horribly adulterated. So if you don’t look out for ASSET bubbles then you will miss the danger signs. I think it was Bismarck who said that the 2 things you should never see being made are sausages and the law. I think we can add ‘inflation statistics” to that?)

So how much higher do rates go?

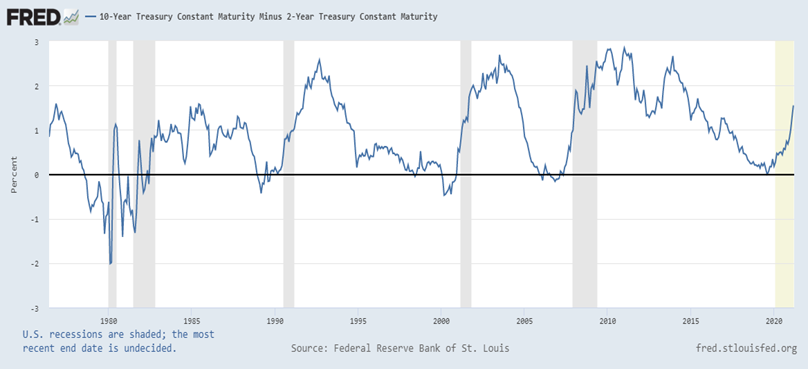

We are nearer the end of the long rate rise vs short rates than the beginning but they ain’t going down below 1.5% again.Charts from ‘FRED’ or the St Louis Federal Reserve Bank, show the average 10s vs 2s spread is about 1.2% over the last 50 years…we are just above average now.

Now maybe we should be using the ratio rather than the arithmetic difference since the steepness is relevant, and if so then we are certainly closer to the above average point.

Source: FRED

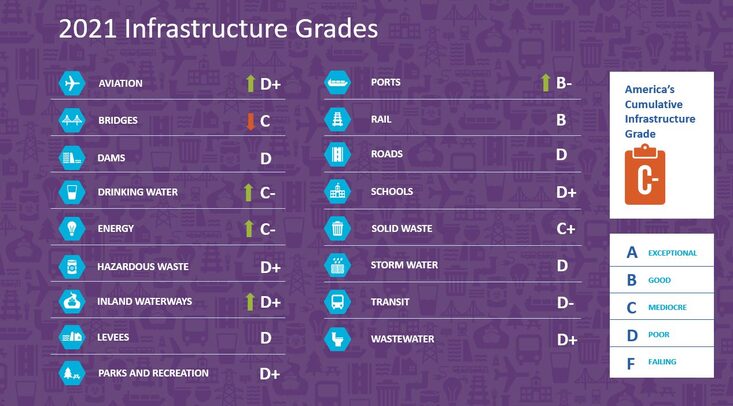

So, while fully cognisant of the difficulty in predicting long rates, we guess at 2.5% as the new average on the 10 year with maybe an overshoot if the recently announced additional $3 trillion package is passed. Yes $3 TR

ILLION. It was only about 20 years ago, by the way, that government debt to GDP was at about 50%. And to think that doubling that debt while having nothing to show for it; except more wealth inequality and a fail grade in Infrastructure, is not deserving of an apology!!

Source: American Society of Civil Engineers

Implications for equities and bonds are (we think) clear:

The SHAPE of the yield curve will benefit dividend paying companies

More fiscal spending will benefit industrial companies and smaller companies

More regulation and higher taxation may take away some of the tailwind to equities of the last few years

The targeted fiscal programme will benefit US Infrastructure stocks (a theme we have been boring everyone on for a few years now) and it will be more than Utilities that benefit – we own Quanta, Johnson Controls, and others whose products will be essential as the grid and capital stock are upgraded.

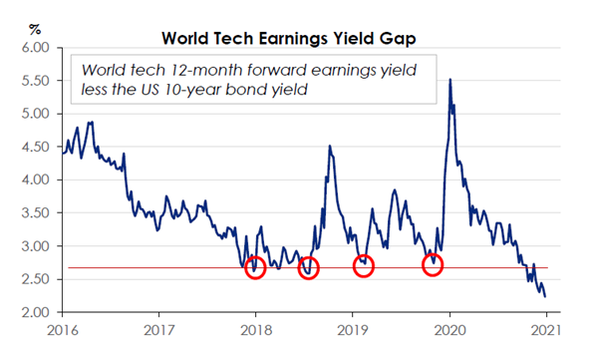

Add in the geopolitical shifts with the Quad alliance and Japan becoming a key partner, then Japan continues to look very good – here we have long argued that Japanese technology is ludicrously overlooked especially in the area of Semiconductor Production Equipment – here we have owned Advantest, Tokyo Electron, Ibiden etc for a while. It’s not too late. While ‘Technology’ may be vulnerable to this shift in macro policy, not all Technology companies will be. Valuation spreads are wide, business models different, and balance sheets and cashflows too.

In short Technology is a sector in which stock specific risk will be rewarded – if your manager has skill. If you have a manager who buys all of it regardless, we show the chart below. You have been warned!

Do not be greedy about equity returns. Profitability is above average, wages relative to profits must rise, companies have underinvested and need to catch up, taxes should go up, and the world is becoming less price efficient as trading blocs are fragmented by political alliances.

This week we would like to revisit the topic of asset prices. More specifically, in reference to the latest RBA meetings and the IMF World Economic Outlook. A topic that is particularly important to us in perhaps elucidating whether we are in the beginning of (another?) bull market or in the final stretches of irrational exuberance. Most importantly, what does this mean for your investing going forward?

O Bubble, Bubble, wherefore art thou Bubble?

Deny thy consequences and refuse thy name.

Author: Sid Ruttala

Anyone that has seen the hot property market, including the recent “best month in 32-years”, might feel a little uncomfortable and scratching their heads at what has been happening. You wouldn’t be alone. The RBA minutes have shown that the board has been watching this particular area quite closely. The case is not isolated either, the S&P500 Stateside has hit all-time highs, the Asian markets continue to roar ahead and Vancouver now has the distinction of being the second-least affordable housing market on the planet (that particular example is apt given the Canadian economy’s similarity to Australia, both being commodities driven). Anything with scarcity value, from crypto to artwork or even pokemon/sports cards, have seen their owners gain immense fortunes. All this, at a time when the market is still recovering from a global pandemic. Policy and geopolitical uncertainty continues to haunt the peripheries but we continue to seemingly ignore it. All this might suggest that we are in the midst of a bubble and you would be partly right. The problem might be in how we investors assess a particular thing and what we are assessing it against.

Let me elaborate. It is true that equity market valuations have hit all-time highs and asset valuations continue to skyrocket, but against what? That is where the question becomes more nuanced. Since the beginning of the covid pandemic, money supply indicators, including broad money, have shown double digit growth, 20% USD, 11% AUD, 10% in the Yen and the numbers continue across most of the world.

Going back to a view that I have previously touched upon, is it valuations going up or money (in this instance the commodity that those valuations are measured against) being devalued? It was Friedman who said that inflation everywhere is a monetary phenomenon, he forgot to mention that also translates to asset price inflation. Is it any wonder that Bitcoin, which has a finite supply of 21 million, remains a scramble. Even if you don’t agree that it has any intrinsic value, you must accept the premise of the argument. By the way, I continue to believe that the argument of intrinsic value in this instance is a fallacy and I say so despite my reluctance to trade that particular asset class. Gold’s valuation far outstrips its actual useful or practical value, a large chunk of the valuation is simply in its role as a store of value. By an extension of that logic, a luxury good, say a Rolex, should have no more value than any other watch assuming the same quality. You are just paying a premium for a belief and a mental programming that says said product makes a statement.

So that is the first point, for the much older investors, the markets may not be as irrational as they may appear. Coming back to the RBA and IMF. There were two things that the board addressed and the IMF corroborated. The first, you get the feeling that they feel asset valuations are a cause of concern though the Governor didn’t go that far as to explicitly state it (and neither should he) but even if this were the case that should not necessitate a normalisation of rates. Rates being the most important factor when it comes to asset prices.

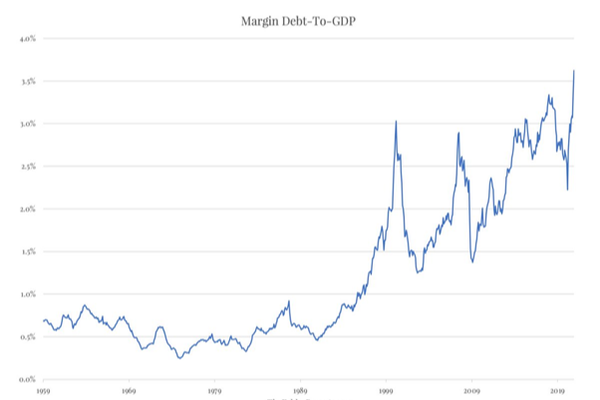

Even pertaining to equity markets, take a look at the below graph. It showcases that US investors had borrowed close to $814bn USD against their portfolios as of late February (the biggest monthly increase since 2007).

Coming then to the second point both seemed to agree upon, addressing the problem will have to be through non-interest-rate regulatory tools. What are those regulatory tools? Typically, think about credit checks or buffer requirements. Think about minimum deposit requirements or interest only loans. To see how this might have a direct impact upon asset prices a quick example might be Hong Kong. When then CEO Carrie Lam, fighting declining approval ratings, lowered the minimum deposit requirements to 10% for properties up to $8m HKD (as opposed to the previous $4m HKD). While this did undoubtedly help many people afford their own properties, especially first home buyers, it had a secondary impact of putting a boost on property prices when the policy was brought in (Q4 2019, though they subsequently cooled off after, well, we all know what happened).

For a further walk down history lane, it was precisely these requirements apart from the Fed Funds Rate that enabled one of the largest expansions in the US real estate market pre-GFC. This time we are likely to see the opposite happen. Lending standards and capital requirements are likely to see tightening as the economy recovers with the implicit hope of cooling off credit growth. From an allocation perspective, we are unlikely to see any changes to the headline cash rates globally. This however, despite what has been said, is not a choice but necessity. As we have elaborated upon previously, covid has brought about fiscal deficits across most of the western world that we have not seen since the World Wars and the case is similar across most emerging markets. Even slight increases in headline rates will have immense implications upon the debt-servicing requirements and consequent tax burden. To give you a context of the magnitude, the central bank balance sheets of the US, BoJ, RBA and ECB expanded more in the year 2020 than the five years following the GFC.

Stateside this will likely continue under the new administration, an additional $2tn earmarked already. At home, don’t forget an upcoming election down under. If the recent trends regarding longer-term yields are anything to go by, we are probably going to see most of the new spending and debt-issuance end up on central banks’ balance sheets given little appetite from alternative investors.

So, what does this mean for us investors? The first is simple, the outstanding returns of the past year across asset classes may be just that, an outlier recovery fuelled by loose monetary policy. We have probably seen the easy returns made. As policy makers change tack and work toward trying to taper off some of the risks associated with ever increasing asset prices, investors might need to be a little nuanced in how they allocate. This is necessary, given that the ramifications have broader implications than just from an investment perspective. Take income inequality for example, one of the unintended consequences of covid policy has been a record number of billionaires added to the Forbes list, about one new one every 17 hours. For the investor, expect the asset classes that you have become used to seeing incredible growth in see tightening, including property and the higher growth segments of equities markets.

As for the question of a bubble? Maybe we are in one, but it is potentially the wrong question all together. The more apt question is, given the incentives for policy makers, government and the amount of liquidity that is driving this, what are the likely outcomes? Take the example of income inequality, one might then ask themselves the question, what does this mean for luxury goods? Or within property, what does this mean for high-end vs. low-end properties? If the cash rates stay low and regulatory tightening occurs on the lending side, what does this mean for my bank shares? This core part of so many Australian portfolios is an interesting one. Anecdotally, a home loan specialist at one of the big banks recently told one of our team that they have rarely been busier than in recent months. Many Aussies have taken advantage of the current situation to lock in low rates. What happens when the banks’ NIMs get squeezed further though? And their loan book growth if lending standards are tightened? This might not happen any time soon (maybe when those locked in rates roll off and become variable in five or so years though?) but it is definitely a consideration for many of Australia’s retiree population. The Australian retiree that has the vast majority of their wealth in a “diverse” selection of property and bank shares is placing a lot of faith in what is essentially one big bet. If the property market finally takes a dive, it will take the banks along for the ride. Given the Australian index’s reliance on and weighting toward the Big Banks, a dive from the property market (and the accompanying problems for the banks) could trigger a much broader sell off across Australian equities. This is perhaps the best argument for ensuring you are also diversifying into international equities.

From the fiscal side of the equation, if we are likely to see increased government spending, what might this mean for infrastructure? This has been one of the big thematics for our global equities manager Robert Swift for a number of years now, a theme kicked into overdrive by covid stimulus. Or what about the effect of direct stimulus upon consumer discretionary spending? A segment that our Australian equities manager Ron Shamgar has been very much on top of this past year.

So going back to the original questions, in this particular author’s humble opinion. Bubble? Possibly by historical standards but there is a little more nuance to this than first meets the eye. Irrational exuberance? No, when you consider the nuances mentioned above. Are we at the beginning of a bull market? Probably, might be a lame one though.

EML Payments (EML.ASX) announced the acquisition of Sentenial and its subsidiary Nuapay for $110m plus a $60m earn out. The deal, funded by partial cash and debt, is not huge in size for EML but significant and transformative as it enables EML to enter the fast-growing open banking sector. Open banking is taking over the payments world; driven by regulatory changes and customer demand. It allows customers and merchants to make instantaneous account to account payments, thereby reducing costs to merchants and fraud. For consumers it is a more convenient way to pay than using a card.

EML Payments (EML.ASX) announced the acquisition of Sentenial and its subsidiary Nuapay for $110m plus a $60m earn out. The deal, funded by partial cash and debt, is not huge in size for EML but significant and transformative as it enables EML to enter the fast-growing open banking sector. Open banking is taking over the payments world; driven by regulatory changes and customer demand. It allows customers and merchants to make instantaneous account to account payments, thereby reducing costs to merchants and fraud. For consumers it is a more convenient way to pay than using a card.