This week’s TAMIM Reading List explores how shifting economic signals are reshaping markets, expectations and the way people approach work and money. Oil prices have surged amid geopolitical tensions while the latest US jobs data raises fresh questions about the strength of the global economy. At the same time, some analysts warn that stagflationary pressures may be quietly building beneath the surface of current market optimism. Yet not all signals point in the same direction, with emerging markets rallying as investors reassess global growth opportunities. Looking ahead, forecasts of potential economic surprises in 2026 highlight just how uncertain the outlook remains. Beyond markets, new research on work trends and personal finance shows how individuals are adapting to a changing economic environment. Together, these articles highlight a world where economic signals, investment opportunities and everyday financial decisions are increasingly interconnected.

Markets have a curious habit of extrapolating the recent past far into the future. When a company experiences a difficult period, investors tend to assume that weakness will persist indefinitely. Yet history shows that some of the most compelling opportunities arise precisely when sentiment is weakest but the underlying business is quietly being rebuilt.

In our view, EML Payments may be approaching that moment.

Over the past two years the company has gone through a significant transition. Operational changes, regulatory remediation, portfolio simplification, and technology upgrades have dominated management’s agenda. These initiatives have inevitably weighed on near-term growth and investor confidence.

But transitions eventually end. And when they do, the market often rediscovers businesses that look very different from the ones it had previously written off.

Today, EML appears to be entering the final phase of its reset.

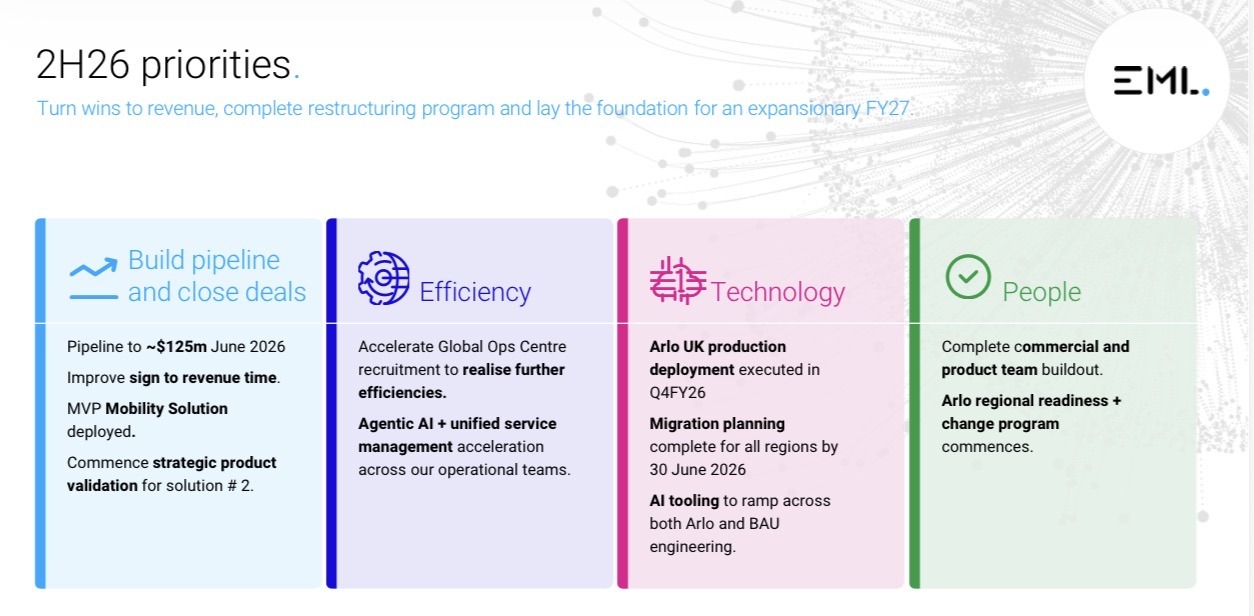

A Transitional Year Approaching Completion

Management has been clear that FY26 represents a rebuilding year. The objective has not been to maximise short-term growth but to stabilise the platform, modernise technology infrastructure, and rebuild the commercial pipeline. From that perspective, the first half of FY26 looked exactly like a company in transition.

Revenue for the half came in at $108 million, representing a 6 percent decline year on year and slightly below market expectations. The weakness was primarily driven by two factors.

First, interest income declined by 12 percent, reflecting changes in interest rate dynamics and balance structures across several programs. Second, customer revenue declined 4 percent, largely reflecting the lingering effects of program attrition that had already been flagged in earlier updates. At the surface level, those numbers understandably disappointed investors. However, focusing only on the revenue line risks missing the broader picture.

EML has spent the past year aggressively reshaping its cost base and operating model. As a result, overhead expenses remained flat at $53 million, demonstrating the company’s ability to maintain discipline despite continued investment in technology and product development.

This cost control helped preserve profitability, with underlying EBITDA of $28 million for the half, broadly in line with market expectations. In other words, while revenue softened, the business remained resilient. More importantly, the groundwork for the next growth phase continued to take shape behind the scenes.

Sentiment Weakness Created the Opportunity

Investor sentiment towards EML weakened significantly following the company’s first quarter update in November 2025. At the time, management warned that the early part of the year would be soft as customer transitions and legacy program impacts continued to flow through the system. The market reacted quickly, raising concerns that the company might struggle to meet its full-year guidance.

Yet the subsequent quarter told a more balanced story. The second quarter delivered EBITDA of $22 million, driven largely by seasonal strength in the Gifting and Incentives segment, which traditionally performs well during the holiday period. More importantly, the improved quarter provided management with sufficient confidence to reaffirm full-year guidance, tightening the expected EBITDA range to $58 million to $60 million.

This confirmation was important. It signalled that the transitional weakness was both anticipated and manageable. For long-term investors, the key takeaway was not the softness in the first half. It was the fact that management continued to demonstrate confidence in the trajectory of the business.

The Strategic Reset Is Beginning to Show Results

Behind the headline numbers sits a far more important story. Over the past year EML has been quietly executing a strategic reset that aims to reposition the company for the next phase of growth.

Four key pillars define that strategy. First, the company has been rebuilding its commercial pipeline, re-engaging with customers and partners following the regulatory disruptions of prior years. Second, EML has invested heavily in modernising its technology infrastructure, including migrating programs onto a more scalable and flexible processing environment. Third, management has expanded the company’s product capabilities, enabling new revenue streams that were not previously available within the platform. Finally, the business has pursued targeted cost efficiencies, improving operating leverage and lowering the cost to serve customers.

Importantly, these initiatives are not theoretical. They are already beginning to show up in operational metrics. And investors may begin to see the full impact as early as the upcoming August result, when the benefits of the reset become more visible in forward guidance.

Enter the Mobility Payments Opportunity

Perhaps the most interesting development emerging from the reset is EML’s entry into the mobility payments sector. This vertical, which includes fuel card and mobility expense solutions, represents a trillion dollar global payments market. It is also a space where EML’s capabilities in program management, transaction processing, and corporate expense solutions translate naturally.

The company plans to launch its Mobility Minimum Viable Product (MVP) later this year. At the same time, customers will begin migrating onto Pismo, EML’s modern processing platform. The strategic importance of this transition should not be underestimated. Pismo provides a highly scalable, cloud-native payments infrastructure that allows EML to deliver new products faster and at lower operating cost. It also enables higher-margin revenue streams driven by product functionality rather than simply transaction volume.

In practical terms, the platform should reduce the company’s cost-to-serve while simultaneously expanding its ability to monetise payment programs. That combination is powerful. Lower costs and higher margins create operating leverage that can significantly enhance profitability once revenue growth returns.

Existing Customers Provide a Natural Adoption Base

One of the advantages EML enjoys in launching the mobility vertical is its existing customer relationships. In particular, the company already services a number of salary packaging providers, many of whom operate programs that involve transportation or fuel-related expenses. Management believes these existing customers represent a natural adoption opportunity for mobility solutions.

Instead of starting from zero, EML can leverage established partnerships to introduce the new product suite. If adoption occurs as expected, the mobility offering could accelerate revenue growth over time while strengthening customer relationships. Importantly, management has emphasised that investment into the vertical will remain disciplined.

Capital will only be allocated to initiatives where there is clear commercial demand and identifiable revenue pathways. In other words, the mobility strategy is not an open-ended experiment. It is a targeted expansion built on existing capabilities and customer relationships.

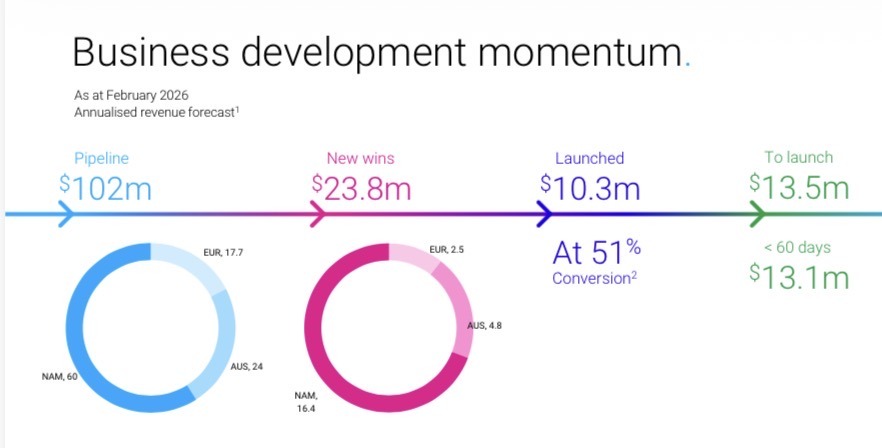

A Pipeline That Has Quietly Reappeared

Perhaps the most telling indicator of the reset’s success is the re-emergence of EML’s commercial pipeline. Twelve months ago the company’s pipeline had effectively disappeared following the disruptions of prior years. Today it has rebuilt to $102 million, exceeding internal targets.

Even more encouraging is the revenue visibility attached to that pipeline. New customer wins are expected to generate approximately $24 million in annualised revenue once fully launched during the second half of FY26. At the same time, the attrition impacts that weighed on the business over the past two years are expected to ease significantly through the remainder of FY26.

Taken together, these two factors create a more constructive growth profile heading into FY27. Management believes that roughly half of all new revenue will ultimately drop through to EBITDA. That level of incremental margin suggests meaningful operating leverage once growth resumes.

Incentives Matter

One of the most interesting aspects of EML’s story today lies not in the business itself but in the incentives driving management. There are currently 63 million performance shares allocated to the leadership team. These shares only vest if the company’s share price reaches $1.50 by August 2027. If that target is achieved, management stands to receive approximately $95 million of value.

If it is not achieved, the performance shares are worthless. Few structures align management and shareholders more clearly than that.

The late Charlie Munger once famously said:

“Show me the incentive and I’ll tell you the outcome.”

While outcomes are never guaranteed, incentive structures like this create a powerful motivation for management to deliver. With roughly sixteen months remaining before the vesting window closes, the leadership team has a clear reason to ensure that the next phase of EML’s growth story becomes visible to the market. That visibility will likely begin with the upcoming August result, where forward guidance may play a crucial role in shaping investor sentiment.

A Valuation Disconnect

Despite the progress taking place within the business, EML continues to trade at a valuation significantly below global peers. Payments companies with similar growth potential typically trade between eight and twelve times EBITDA.

EML currently trades at approximately 4.5 times EV to EBITDA, falling below four times on FY27 estimates. On management’s FY28 target of $95 million in EBITDA, the multiple falls below three times. Such valuations are typically associated with businesses facing structural decline or significant operational risk.

Yet EML’s situation appears increasingly different. Regulatory remediation has been completed. The balance sheet has improved. Technology infrastructure is being modernised. And the commercial pipeline is rebuilding. If the company successfully executes the next phase of its strategy, the valuation gap may prove difficult to justify.

Three Potential Catalysts Ahead

For investors considering the opportunity today, the next twelve months could prove pivotal. Three potential catalysts may drive a shift in sentiment. The first relates to mobility payments. News flow surrounding the launch of the mobility vertical and the onboarding of foundational clients could demonstrate the commercial potential of the new platform. The second catalyst is strategic interest. Given the company’s low valuation and improving operational profile, the possibility of a takeover cannot be ignored. Payments infrastructure businesses with strong platforms often attract interest once legacy issues have been resolved. The third and perhaps most immediate catalyst will be the August result and FY27 guidance. If management demonstrates clear revenue momentum and reiterates confidence in its medium-term targets, investors may begin to reassess the company’s growth prospects.

Looking Toward FY27

Current market consensus expects FY27 EBITDA of approximately $66 million. Based on the operational improvements already underway, we believe management may be capable of delivering closer to $70 million. If that level of performance is achieved, and the company simultaneously reaffirms its FY28 target of $95 million, the market’s perception of EML could change rapidly.

In that scenario, the valuation multiple may begin to expand toward industry norms. Even a move from the current four times multiple toward eight times EBITDA, still below global peer averages, would imply a substantial re-rating in the share price.

The Tamim Takeaway

Investment opportunities often emerge when companies are transitioning from a period of difficulty toward a new phase of growth. EML appears to be approaching exactly that point.

The business has spent the past two years addressing legacy issues, rebuilding its commercial pipeline, modernising its technology platform, and strengthening operational efficiency. Those efforts are now beginning to bear fruit.

At the same time, the launch of the mobility payments vertical and the migration onto the Pismo platform provide the foundation for future product-led growth. With management strongly incentivised to deliver results and the company trading at a valuation well below global peers, the coming months may prove decisive.

If execution continues and guidance begins to reflect the underlying improvements in the business, EML’s current valuation may look increasingly difficult to justify. Transitions eventually end. When they do, markets often rediscover companies that have quietly rebuilt themselves. EML may be approaching that moment.

Disclaimer: EML Payments (ASX: EML) is held in TAMIM Portfolios as at date of article publication. Holdings can change substantially at any given time.

In investing, there are moments when the market slowly recognises value and rewards patient shareholders. Then there are moments when value is crystallised suddenly through corporate action. The recent takeover proposal for ClearView Wealth (ASX: CVW) sits squarely in the second category.

ClearView has long been a fascinating case study in the Australian small and mid cap insurance landscape. For years the company traded at a discount to its underlying economics. Investors often struggled to reconcile the company’s improving operational performance with the modest valuation placed on the stock by the market.

That dynamic shifted meaningfully in the last month following the announcement that Zurich intends to acquire ClearView via a scheme of arrangement. The proposal values the company at 65 cents per share in cash, with the possibility of a fully franked dividend worth up to 5 cents per share, delivering approximately 2.14 cents of additional franking credits to shareholders.

The announcement arrives alongside ClearView’s strong first half FY26 results, which highlight just how much operational momentum has been building within the business. While the takeover proposal has understandably captured investor attention, the underlying results tell an equally important story about the company’s progress and the strength of the life insurance franchise it has built.

A Business That Has Been Quietly Improving

ClearView’s first half FY26 results illustrate a company gaining momentum across multiple operational fronts.

New business sales rose by an impressive 29 percent to $21.0 million. This growth reflects both stronger distribution relationships and increased competitiveness in product offerings. Life insurance distribution in Australia is a highly competitive space, where advisers and brokers have many product providers to choose from. For ClearView to deliver this level of growth suggests the company’s offering is resonating increasingly well with the adviser community.

Market share gains appear to be following. Management estimates that ClearView’s share of the new business market has increased by roughly 10 to 11 percent, a notable shift in what is typically a relatively stable industry structure.

Importantly, this growth in new sales is not simply a one off spike in activity. Life insurance businesses benefit from recurring revenue dynamics once policies are written. As new policies are added, the base of in force premiums expands, creating an annuity like income stream over time.

This dynamic is clearly visible in the numbers. In force premiums increased 13 percent to $436 million. This figure represents the company’s annual recurring premium base and is a critical indicator of long term earnings power within the business.

Gross premium revenue followed a similar trajectory, also rising 13 percent to $215.6 million for the half. This growth reflects both new policy additions and strong policy retention. In a sector where customer retention is essential to long term profitability, these figures point to a business with improving underlying health.

Claims Stability Supports Earnings Visibility

Insurance companies ultimately succeed or fail based on the balance between premiums collected and claims paid. ClearView’s claims experience during the period remained stable and well within management expectations. The company reported a gross claims loss ratio of 51 percent, broadly consistent with its long term average of around 52 percent.

This level of stability is particularly important for investors analysing insurance businesses. Claims volatility can materially impact profitability, especially for smaller insurers with more concentrated policy books.

The fact that ClearView continues to deliver claims ratios aligned with historical averages suggests that its underwriting standards remain disciplined. It also supports the view that the company’s earnings profile is becoming more predictable as the policy base matures and expands. In simple terms, the company is writing profitable business and managing risk effectively.

Earnings Growth Accelerates

One of the most striking aspects of the first half results was the magnitude of earnings growth. Life insurance underlying net profit after tax increased by 59 percent to $24.1 million. At the group level, underlying net profit rose 77 percent to $22.1 million. This growth reflects a combination of expanding premium revenue, stable claims performance, and operating leverage within the business model.

Insurance platforms benefit from scale. Once the fixed cost base is established, incremental policies can be added with relatively modest increases in operating expenses. As a result, revenue growth tends to translate into faster earnings growth over time.

ClearView’s results demonstrate this dynamic clearly. Underlying earnings per share increased 84 percent to 3.5 cents for the half, highlighting the strong operating leverage embedded within the business. For long term investors who have followed the company over several years, these results represent the culmination of a multi year effort to reposition and strengthen the business.

Balance Sheet and Embedded Value

Another area worth highlighting is the company’s balance sheet and underlying economic value. ClearView reported surplus capital of $11.3 million at the end of the half, alongside total net assets of $348.4 million. On a per share basis, this equates to approximately 55.9 cents per share.

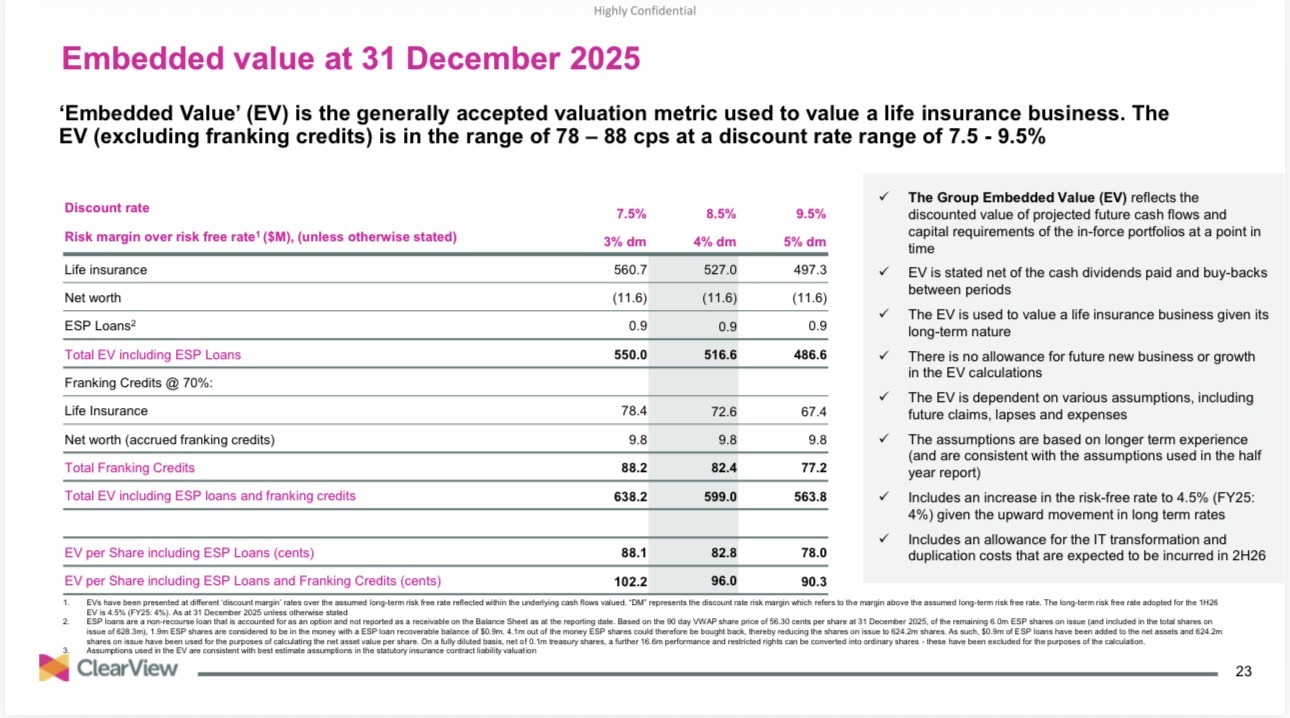

However, the more relevant metric for many life insurance businesses is embedded value. Embedded value attempts to estimate the present value of future profits expected from the existing policy book.

For ClearView, embedded value excluding franking credits was estimated at between 78 and 88 cents per share. This figure is particularly notable when compared with the current takeover proposal of 65 cents per share. Even before considering the value of franking credits attached to potential dividends, the offer sits meaningfully below the company’s embedded value estimate.

From a purely financial perspective, this suggests that Zurich’s proposal captures ClearView at a relatively modest valuation relative to the future profits expected from its existing policies.

Technology Transformation Underway

Beyond the headline financial metrics, ClearView has also been undertaking a significant technology transformation designed to simplify and modernise its operating platform. Historically, many life insurers have operated with complex legacy systems built over decades. These systems can create operational inefficiencies and limit the speed at which companies can innovate or introduce new products.

ClearView is addressing this challenge through a migration to a single cloud based core insurance platform. This transition is intended to reduce system complexity, streamline operations, and lower long term costs.

A new digital front end platform is scheduled for release during the second half of FY26. This system is expected to enhance the experience for both advisers and policyholders by improving application processes and policy management.

At the same time, legacy systems are gradually being decommissioned. Removing these older platforms reduces duplication and allows the company to operate with a simpler and more scalable technology architecture. These initiatives may not capture daily market headlines, but they play a crucial role in shaping the long term competitiveness of the business.

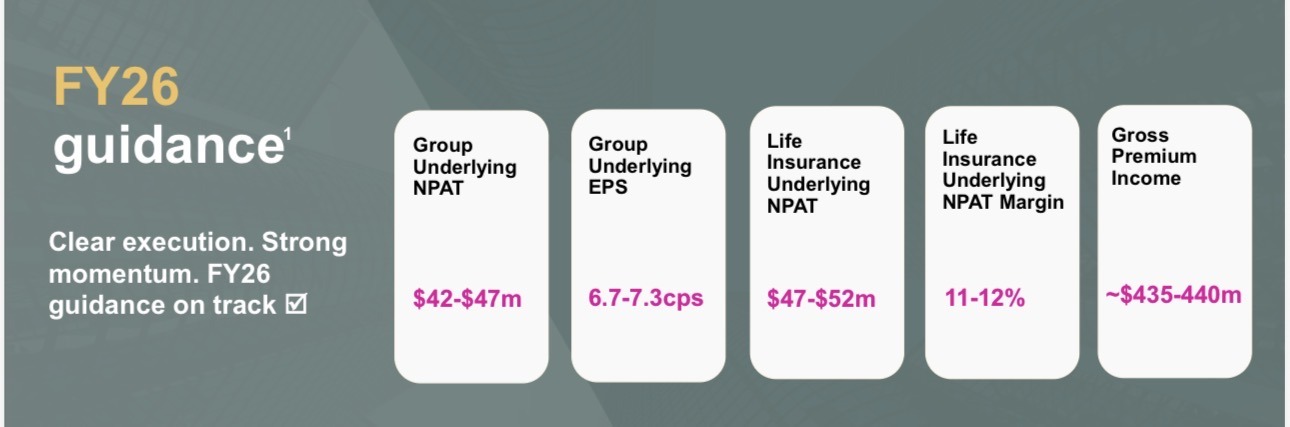

FY26 Outlook Remains Positive

Looking ahead, management has reaffirmed a constructive outlook for the remainder of FY26. The guidance incorporates the February 2026 industry repricing cycle and suggests continued premium growth. Gross premium revenue for the full year is expected to fall between $435 million and $445 million. Given that in force premiums have already reached $436 million, the second half of the year is expected to begin with a strong revenue run rate.

Group underlying net profit after tax is forecast to land between $42 million and $47 million for FY26, with earnings per share expected to reach between 6.7 cents and 7.3 cents.

At the proposed takeover price of 65 cents per share, this equates to a forward price earnings multiple of approximately 9.3 times at the midpoint of guidance. For a business delivering double digit revenue growth and significant earnings expansion, this valuation appears modest by most standards.

The Zurich Proposal

Against this backdrop, Zurich’s takeover proposal takes on greater significance. The scheme of arrangement offers shareholders 65 cents in cash per share, valuing the company’s equity at approximately $415 million. The proposal also allows for up to 5 cents per share in fully franked dividends, which would add approximately 2.14 cents of franking credits for investors.

ClearView’s board has unanimously recommended that shareholders vote in favour of the scheme. The company’s largest shareholder, Crescent Capital, which holds roughly 53 percent of the shares, has indicated its intention to support the transaction.

The proposal remains subject to regulatory approvals from both the Australian Competition and Consumer Commission and the Australian Prudential Regulation Authority. If these approvals are received, a scheme meeting is expected to take place around mid August 2026.

Is There Room for a Higher Bid?

While the Zurich proposal represents a clear pathway to liquidity for shareholders, it also raises an important question. Is this the best price ClearView could achieve?

Based on the company’s embedded value estimates of between 78 and 88 cents per share, the current offer sits at a meaningful discount to the estimated long term economic value of the business.

The offer also represents a relatively modest earnings multiple given the company’s growth trajectory. In our view, this leaves open the possibility of a competing proposal emerging in the coming months. A rival bidder offering between 70 and 75 cents per share would not be difficult to justify financially, particularly for a strategic buyer seeking to expand its presence in the Australian life insurance market.

Whether such a bid materialises remains uncertain. Corporate transactions are influenced by many factors beyond simple valuation metrics, including strategic fit, regulatory considerations, and shareholder dynamics.

The Crescent Factor

Another element that has historically influenced investor perception of ClearView is the presence of Crescent Capital as the majority shareholder. Large controlling shareholders can sometimes create an overhang for minority investors, particularly when the timing of potential exits is unclear.

By placing the company in play through the Zurich scheme proposal, Crescent has effectively removed that uncertainty. The market now has a clear timeline for a potential transaction and a defined valuation benchmark. For investors who have held the stock for several years, this represents an important development.

What Happens Next

Over the next few months, the market will watch closely to see whether any alternative proposals emerge. If a competing bidder appears, shareholders may ultimately receive a higher price for the business. If not, the Zurich scheme will likely proceed as planned. Either outcome provides clarity for investors.

If the scheme completes at the current price, it effectively sets the final valuation the market was willing to place on the business at this point in time. While that valuation may sit below embedded value estimates, it reflects the realities of market demand and corporate transaction dynamics.

If a higher offer does emerge, it will confirm that the underlying economics of the business are worth more than the current proposal suggests.

TAMIM Takeaway

ClearView’s first half FY26 results demonstrate a business that is performing strongly operationally. Sales momentum is accelerating, claims experience remains stable, and earnings are growing rapidly. The company’s embedded value also suggests that the long term economics of the business may be worth significantly more than the current takeover proposal.

Zurich’s offer at 65 cents per share provides a clear exit pathway for shareholders and establishes a baseline valuation for the company. However, the offer sits at a relatively modest earnings multiple and below the company’s embedded value range.

In our view, the coming months will determine whether another bidder emerges with a higher proposal. A competing offer in the range of 70 to 75 cents would not be difficult to justify based on the company’s financial performance and growth trajectory.

If no alternative proposal appears, the scheme will likely proceed and provide closure for investors who have followed the ClearView story for several years. Either way, this situation highlights an enduring truth in small cap investing. Value can remain hidden for long periods of time, but when it is finally recognised, it often happens quickly.

Disclaimer: ClearView Wealth (ASX: CVW) is held in TAMIM Portfolios as at date of article publication. Holdings can change substantially at any given time.

The geopolitical temperature in the Middle East is rising. The United States has increased its military posture in the region, naval assets are repositioning, and rhetoric between Washington and Tehran is intensifying. Whether conflict becomes kinetic or remains contained, markets are beginning to price risk. Investors do not need to predict war to prepare for it. They need to think clearly about probabilities, second order effects, and portfolio construction.

When geopolitical tension spikes, markets move first on fear, then on fundamentals. The opportunity lies in distinguishing between the two. Below are three key areas investors should be actively assessing in portfolios right now. In two of them, I see opportunity. In the third, I see risk that is still underappreciated.

1. Energy Security and Infrastructure: Follow the Physical Reality

If conflict escalates, the immediate market reaction will centre on oil. Iran sits astride the Strait of Hormuz, through which roughly 20 percent of global oil supply flows. Even a temporary disruption would have outsized price implications. But the more important issue is not a short term oil spike. It is the structural repricing of energy security.

Governments have spent the last three years focused on inflation, interest rates and energy transition. A Middle East conflict would remind the world that hydrocarbons still matter. Supply reliability matters. Infrastructure redundancy matters. For investors, this shifts the conversation from commodity speculation to infrastructure positioning.

Areas of opportunity include:

Midstream energy infrastructure

LNG export facilities

Strategic petroleum logistics

Pipeline operators

Defence-adjacent energy systems

These businesses are not simply oil price bets. They are toll roads on global energy flow.

We have already seen how energy shocks following the Ukraine conflict reshaped European energy policy. A Persian Gulf disruption would accelerate capital allocation into alternative supply chains, regional energy independence, and strategic storage capacity.

The opportunity is not in chasing the first oil spike. It is in owning the infrastructure that benefits from structural capital spending. Investors should be asking: which companies earn stable cash flows regardless of short term price volatility, but benefit from increased strategic importance?

That is where the asymmetric upside sits.

2. Defence and Strategic Technology: A Structural Re-rating

Every modern conflict reinforces the same lesson: warfare is becoming more technological, more digital, and more capital intensive. Defence budgets were already rising across the US, Europe, and Asia before this latest tension. A sustained Middle East conflict would likely accelerate procurement cycles. Opportunities here extend beyond traditional weapons manufacturers.

The modern defence ecosystem includes:

Cybersecurity platforms

Drone technology and counter-drone systems

Missile defence systems

Satellite and communications infrastructure

AI-enabled battlefield analytics

Investors often hesitate to allocate to defence due to ethical considerations or cyclicality concerns. But the geopolitical environment has shifted. Western governments are realigning industrial policy toward resilience and deterrence.

In previous cycles, defence stocks experienced short sharp rallies during conflict and then retraced. Today feels different. Supply chains are being rebuilt. Production capacity is expanding. Orders are multi-year. The key is selectivity.

Investors should avoid chasing companies trading purely on headline momentum. Instead, focus on businesses with long-term contracts, visible backlog, and technological differentiation. The structural trend is clear: national security is no longer optional expenditure. In an uncertain world, governments rarely cut defence budgets.

3. Rate-Sensitive Growth and Consumer Discretionary: The Area of Caution

Here is where I would exercise caution. A Middle East conflict is inflationary at the margin.

Higher oil prices feed into transport costs, food prices, manufacturing inputs, and ultimately consumer inflation. If inflation expectations reaccelerate, central banks may be forced to pause or even reverse easing trajectories. Markets currently expect a gradual normalisation of interest rates. A sustained energy shock complicates that narrative.

The asset class most vulnerable in that scenario is long-duration growth. High multiple technology stocks, consumer discretionary names reliant on strong sentiment, and businesses dependent on cheap capital can reprice quickly if bond yields move higher. We saw this dynamic in 2022 when rate volatility, not earnings collapse, drove valuation compression.

In a geopolitical shock, investors often underestimate the secondary impact on bond markets. The question to ask is simple: if oil remains 20 to 30 percent higher for six months, what happens to inflation expectations and the yield curve? If the answer implies higher real rates, then expensive growth assets deserve caution.

This does not mean abandoning technology or innovation. It means focusing on companies with real earnings, strong balance sheets, and pricing power rather than speculative future cash flows. Volatility does not destroy value. Leverage and overvaluation do.

The Portfolio Framework

In times of geopolitical tension, emotional reactions dominate headlines. But disciplined investors zoom out.

There are three guiding principles worth remembering:

Conflicts are inflationary before they are recessionary.

Governments respond with fiscal spending before austerity.

Markets overreact first, then recalibrate.

Portfolio construction should reflect these realities.

Investing through geopolitical uncertainty requires calm, not conviction theatre.

If the US and Iran move toward open conflict, markets will react sharply. Oil will spike. Defence stocks will rally. Bond markets will wobble. But the real money will not be made in the first week.

It will be made by owning structurally advantaged businesses that benefit from energy security, defence modernisation, and government capital allocation. And by avoiding overvalued assets vulnerable to renewed rate volatility.

We cannot control geopolitics. We can control portfolio positioning. In uncertain times, resilience becomes alpha. And portfolios built around cash flow, balance sheet strength, and strategic importance tend to outperform when headlines turn into history.

This week’s reading list brings together market dynamics, behavioural finance and the changing nature of work to highlight how investors and professionals are navigating a more complex environment. As recent market moves show, sentiment around themes like AI can shift quickly, reminding investors that narratives often move faster than fundamentals. At the macro level, the global outlook points to moderate growth alongside structural risks, where unexpected developments could reshape market direction. At the same time, renewed strength in emerging markets is challenging the narrow leadership that has defined recent years. Beyond markets, long-term financial outcomes continue to be driven less by short-term decisions and more by simple, consistent habits. The workplace itself is also evolving, with flexibility, productivity and changing career expectations reshaping how value is created. Together, these articles reinforce a common message: in a world defined by uncertainty and change, discipline, adaptability and long-term thinking matter more than ever.