This week’s reading and viewing list covers Why International Investing Makes Sense for Long-Term Investors and eta CTO Andrew Bosworth on the Metaverse, VR/AR, AI, Billion-Dollar Expenditures, and Investment Timelines.

Based on our recent highlights, takeovers at the smaller end of the ASX tend to avoid lengthy, drawn-out scenarios due to the simplicity of business scale and fewer regulatory hurdles.

We’ve seen a number of examples within the TAMIM portfolios including Atturra’s takeover offer of Cirrus Networks and the PAR Technology Corporation (NYSE: PAR) 103% premium offer for Task Group Holdings (ASX: TSK). However, as the size and value of the deals increase, the intricacies and challenges multiply. Larger deals involve more stakeholders, higher scrutiny from regulatory bodies, and often, more significant strategic considerations.

This is evidenced in the recent developments surrounding Bapcor Ltd (ASX: BAP) a leading automotive parts retailer in Australia, which has recently rejected a substantial takeover offer.

The Offer

Prominent private equity firm Bain Capital had their $1.83 billion offer turned down by Bapcor.

The $5.40 per share, which represented a 24% premium over Bapcor’s closing price prior to the offer. In a brief statement, Bapcor’s board concluded that:

“The Bain Proposal does not represent fair value for Bapcor, is not in the best interests of Bapcor shareholders and therefore has rejected the Bain Proposal.”

The offer is perhaps seen as opportunistic given the company’s 12 month share price is down just under 19% even after the proposal, following three profit downgrades in the past year.

Bapcor’s board further justified the rejection by emphasising the company’s robust market position and growth prospects. Bapcor operates well-known brands such as Midas and Autobarn, and it has a significant presence in the Australian automotive parts market. The board believes that the company’s future earnings potential is far greater than what Bain Capital’s offer reflected.

Moreover, Bapcor’s strategic focus on expanding its market share and enhancing its operational efficiencies supports the board’s confidence in the company’s long-term growth.

The automotive spare parts industry is relatively resilient, driven by the ongoing need for vehicle maintenance and repair, which is less susceptible to economic downturns compared to new vehicle sales. Following the rejection, the company briefly traded lower before recovering.

Takeover Challenges

Larger takeovers, such as the one involving Bapcor, present a unique set of challenges and complexities compared to smaller deals. While many of these factors are also present in smaller acquisitions, the larger scale of big companies typically introduces more stakeholders and additional hurdles

As the size and value of the deal increase, the number of stakeholders involved also grows. This includes not only the shareholders and management teams of the companies involved but also regulatory bodies, financial advisors, and legal teams. One of the primary complexities is the heightened scrutiny from regulatory bodies. Regulatory authorities, such as the Australian Competition and Consumer Commission (ACCC), closely examine larger deals to ensure they do not create monopolies or reduce competition in the market. This can lead to extended review periods and the imposition of conditions that must be met for the deal to proceed.

Furthermore, larger deals often require larger-scale due diligence processes.

This involves an extensive examination of the target company’s financials, operations, legal standing, and strategic fit. The due diligence process can uncover potential risks and liabilities, which can complicate negotiations and affect the valuation of the target company.

Strategic considerations also play a significant role in larger takeovers.

Acquiring a large company often requires a clear and compelling strategic rationale, such as expanding market share, entering new markets, or achieving operational efficiencies. The acquiring company must demonstrate how the acquisition will create value for shareholders, which can involve complex financial modelling and projections. Additionally, larger takeovers can face resistance from various stakeholders.

Shareholders of the target company may believe the offer undervalues the company and push for a higher price. Employees and management teams may have concerns about job security and changes in corporate culture, leading to potential internal resistance.

These factors combined make larger takeovers a highly complex and challenging endeavour, requiring careful planning, negotiation, and execution.

Bapcor Leadership Changes & Outlook

Upon notification of the takeover bid rejection, Bapcor announced the appointment of Angus McKay as its new Executive Chairman and CEO.

McKay, the former CEO of 7-Eleven, brings extensive leadership experience and a track record of driving growth and operational excellence in retail businesses. His appointment is seen as a strategic move to strengthen Bapcor’s leadership team and support its growth ambitions. Shareholders will be hoping he will be the leader to turn the business around.

Bapcor has not been without its leadership controversies in recent times. McKay will be the company’s 4th CEO appointment following on from the Interim CEO Mark Bernhard. Bernhard took up the role temporarily after Paul Dumbrell made the call a day prior to starting the CEO position that it was no longer for him. Bernhard will return to a non-executive director role. Prior to Mr Bernhard, Noel Meehan, was in the role for two years following Darryl Abotomey, who left Bapcor in late 2021 after a falling out with the board and chairwoman Margie Haseltine.

Bapcor’s financial performance has faced challenges recently, particularly in its retail division.

The company has recently confirmed its Pro-Forma net profit to be between $93 million to $97 million for the 2024 financial year. The decline in profit is attributed to impairment charges in the retail segment, which have been influenced by a slowdown in discretionary spending due to cost-of-living pressures.

Despite these short-term challenges, the underlying dynamics in the automotive spare parts market remain positive. Bapcor’s trade and specialist wholesale businesses, which account for about 80% of its earnings, continue to perform well. These segments are driven by nondiscretionary spending on vehicle maintenance, which is less affected by economic fluctuations.

The TAMIM Takeaway

Bapcor’s rejection of Bain Capital’s takeover offer is another example of the intricate challenges associated with larger deals.

Larger takeovers bring a multitude of unique complexities. In this case, Bapcor’s decision reflects the board’s belief in the company’s long-term growth potential, even amid recent profit downgrades and share price declines.

Shareholders will be hoping the new appointment of Angus McKay as CEO will solidify Bapcor’s leadership and navigate the challenging market currently testing the automotive spare parts industry’s resilience.

With June 30 now in the rear vision window, we suspect your attention has turned to digging up old receipts and preparing your tax returns. For the global fund, the date represents an important milestone to review our performance for the financial year; what went right, what didn’t go to plan and where we can improve in the months and years ahead.

Below we profile three top performers for the financial year end. If you would like to read more about our investment views on KLA and Emcor, please review our February and October monthly fund reports.

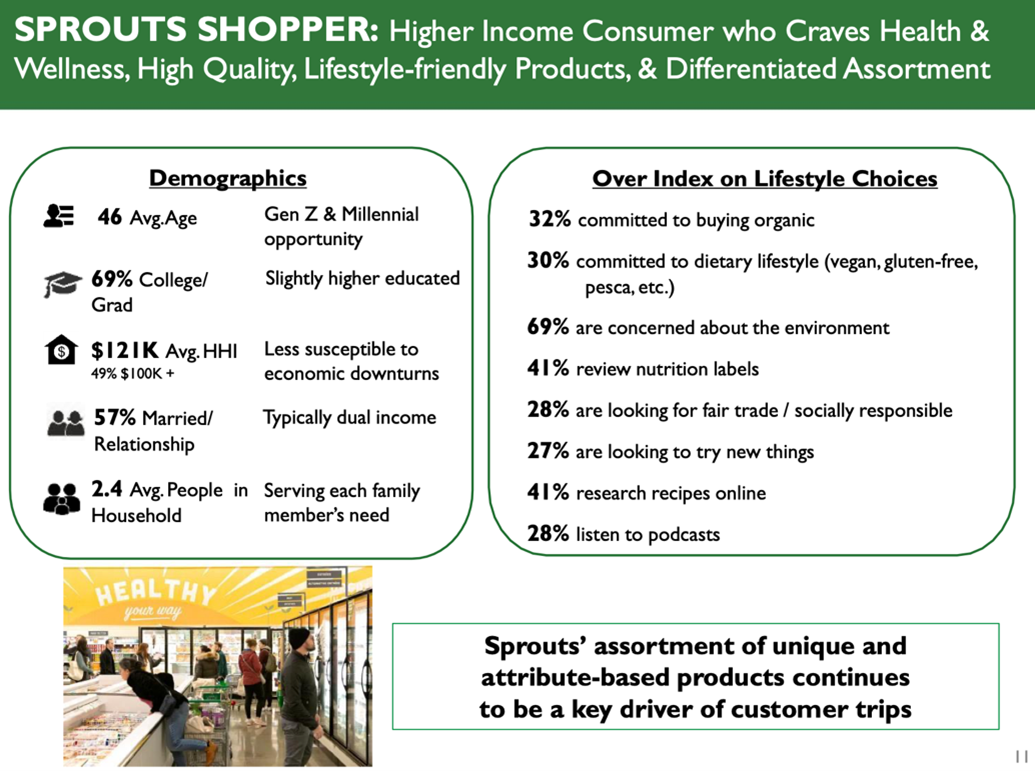

Sprouts Farmers Market Inc (NASDAQ.SFM)

Sprouts Supermarkets is an American fresh-food supermarket retailer. The company offers a wide selection of fresh, organic, vegan, dairy-free, gluten-free and whole foods rarely available at mainstream supermarkets.

Source: Sprouts May 2024 Investor Deck

We first wrote about Sprouts in September 2023, highlighting that we believed the market had underappreciated the store rollout trajectory and the stickiness of its customer base. Since then, the company has continued to beat internal and analyst expectations regarding the pace of new stores, revenue and earnings. Despite the weakening economy, customers have continued to frequent Sprouts with same-store sales increasing by 4% and total sales rising by 9%.

The superior value proposition (Sprouts is regularly cited as being cheaper than close competitor Whole Foods) has shielded the business – and its consumers, from economic headwinds. The health-conscious shopper is also likely to be of middle or high-socioeconomic demographic and therefore relatively less immune to cost of living pressures. The average Sprouts shopper is 46 years old, has an income of US$121,000 per year and is likely to be college-educated.

Sprouts is a classic case of a market caught up in short-term macro headwinds rather than seeing the long-term fundamental growth story. The 122% increase in the share price means the earnings ratio now reflects a growth company rather than a nascent, low-margin retailer. While we would not expect the same share price gains to be repeated, the company remains well-positioned to capitalise on a growing and profitable grocery niche.

CNOOC Ltd (HK.0883)

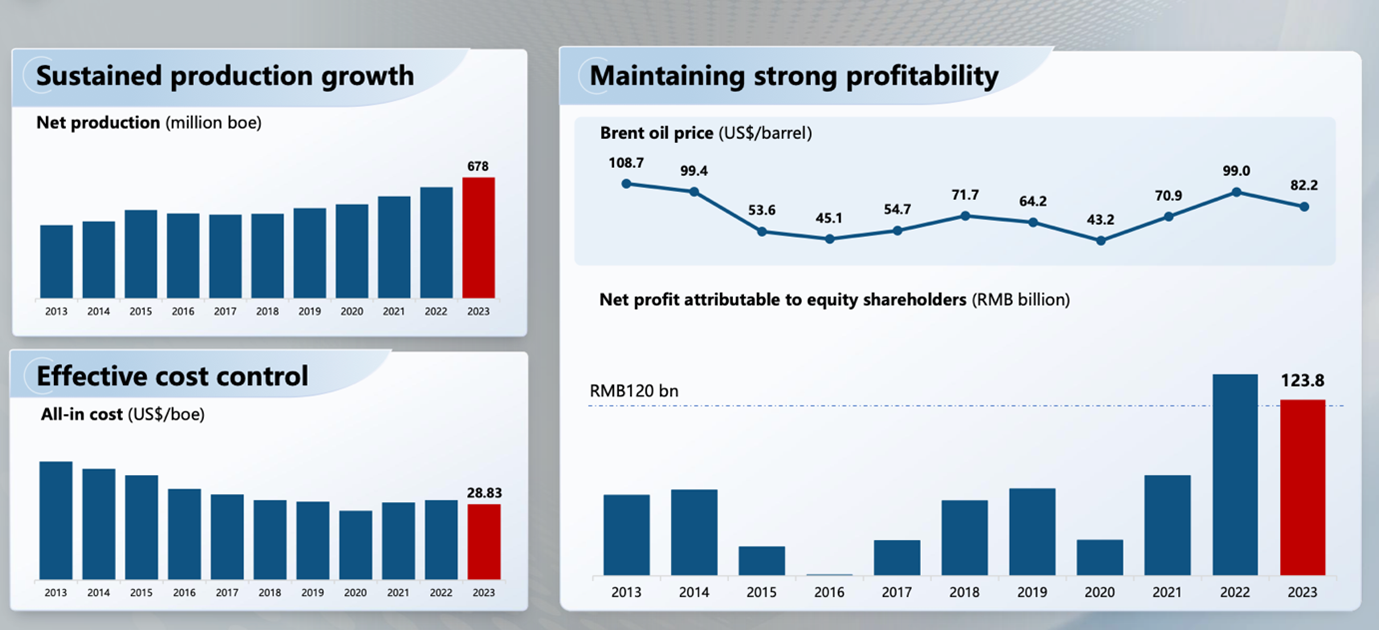

China National Offshore Oil Corporation (CNOOC) is one of the world’s largest oil and gas companies. The business derives around 70% of its production from China with the remainder sourced from assets in the Americas, Asia and Africa. CNOOC’s assets are competitive on the cost curve with an average cost of ~US$28/BOE (barrel of oil equivalent) compared to a current oil price of ~US$78.

Source: CNOOC 2023 Annual Results

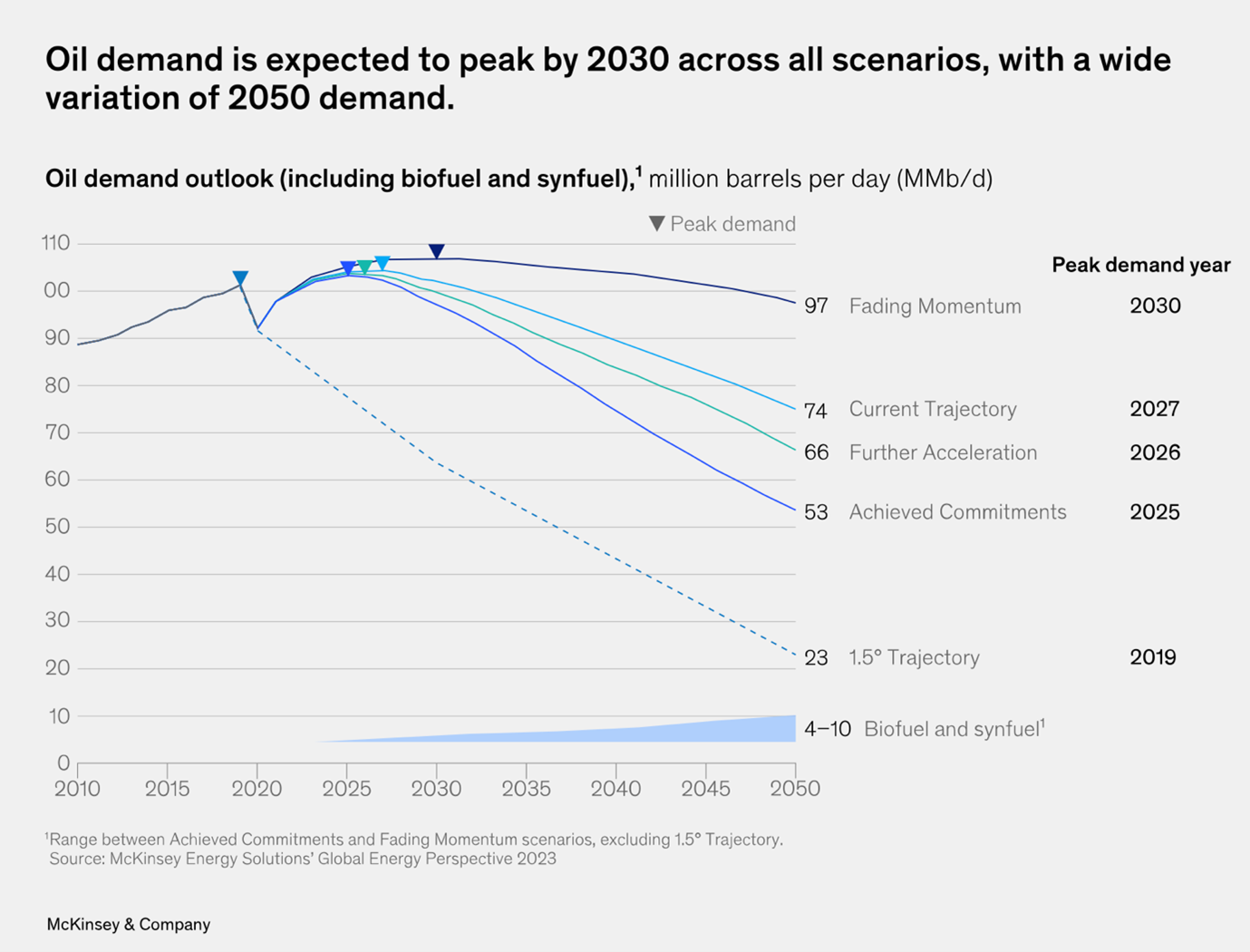

It’s well established that in the next five years, we will reach peak oil demand as electric vehicle adoption accelerates. However, the steepness of the decline is still uncertain, and given the lack of substitutes for fueling trucks, planes, and ships in addition to producing plastics, there is a fair chance that oil demand will remain resilient until commercial alternatives are developed and widely available. Moreover, new supply is becoming increasingly difficult to first gain approval, and then scale to be competitive, particularly in developed nations. This bodes well for CNOOC as a low-cost producer with a growing production profile. Management expects net production to reach 810-830 million BOE by 2026, up from 678 million in 2023.

Source: McKinsey

Traditional energy companies have faced significant valuation headwinds in recent years as the rise of sustainable (or ESG) prevented pension managers and institutions from deploying capital into the sector. Chinese companies such as CNOOC have also battled concerns over the domestic economy and ownership structures. While these headwinds remain to varying degrees, the underlying business performance of CNOOC has grabbed the market’s attention.

The company has diligently expanded production and reserves while also retaining tight control. Since 2018, earnings have increased 134% despite gyrations in the underlying oil price. There’s also been a broader trend in the energy market to “get big or get out”, with larger rivals taking over smaller peers to amalgamate resources and cash flows.

Recent transactions include Woodside’s US$19.6 billion purchase of BHP’s gas and oil assets and Chevron’s US$53 billion agreement to buy Hess. This has given the market a yardstick to value other public energy companies leading to multiple rerating. Even after the CNOOC share price has doubled, the business trades on a dividend yield above 5% and a mid-high single-digit earnings multiple.

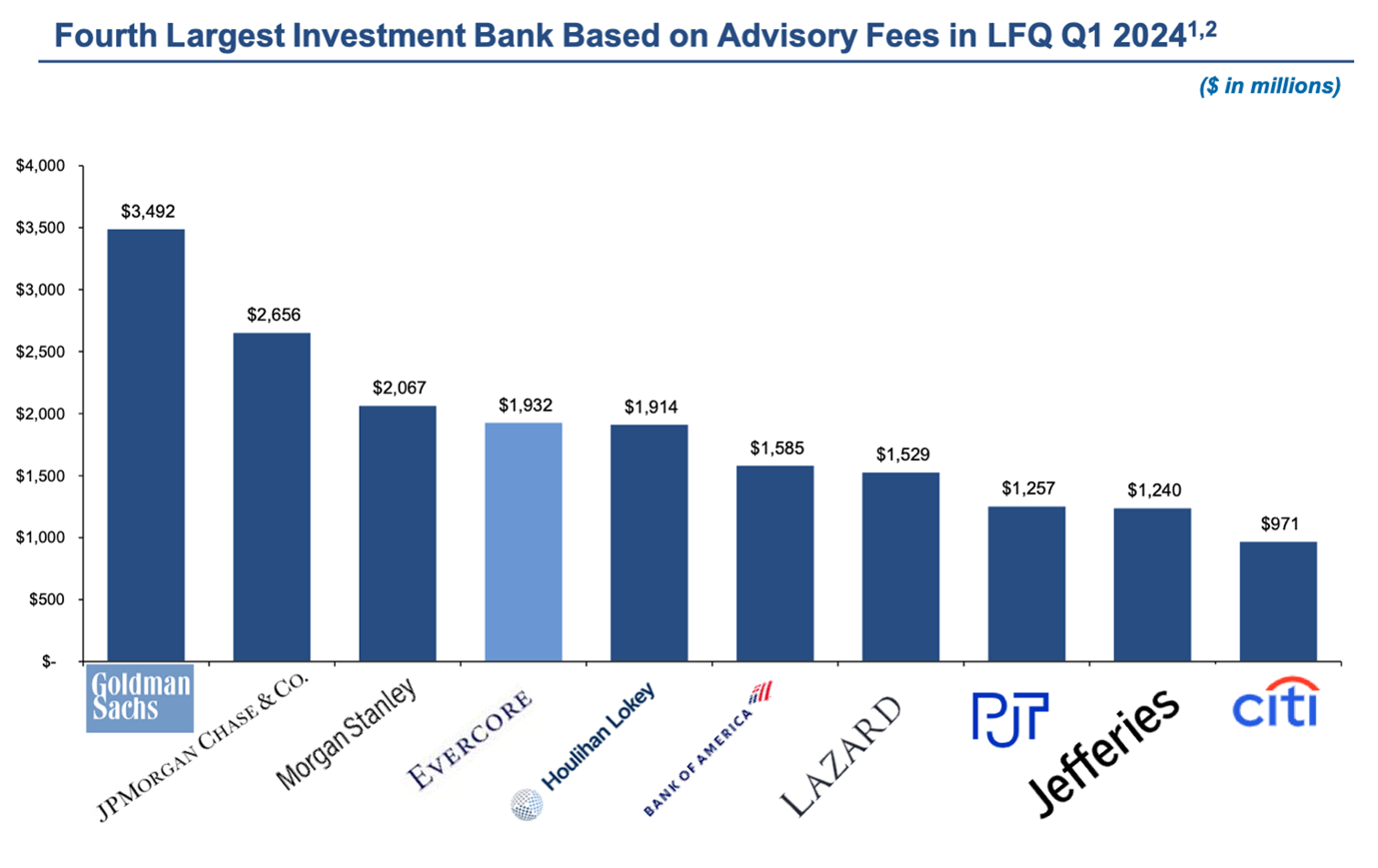

Evercore Inc (NYSE.EVR)

Evercore is the world’s largest independent investment bank. Unlike competitors who typically offer a universal banking platform that includes trading, lending and investing, Evercore focuses purely on advising organisations. This positions the company and its employees as trusted partners without the potential conflicts of interest that arise with larger peers. As a result, the business is frequently appointed to the largest corporate transactions including the spinoff of GE’s energy division Vernova and Global Infrastructure Partners sale to Blackrock.

Source: Evercore Q1 Results

Despite its size today, Evercore never intended to become a global company. It was founded three decades ago with the humble ambition of creating a small but high-quality advisory shop without the rough-and-tumble culture of Wall Street. The firm was deliberately not named after its founders, nor did they reserve any special ownership or legal structure. A uniform and transparent compensation system remunerated the whole firm rather than each department or business unit paying themselves from their respective P&L.

This instilled a culture of collaboration and comradery rather than an “eat what you kill” mindset. The unique culture has enabled Evercore to attract and retain high-quality talent that drives organic within the business. The company has 142 senior managing directors with a median productivity of US$18 million per year.

The 77% increase in Evercore’s share price over the past twelve months is primarily a result of the market recognising the company’s sizable growth runway. While investment banking remains a cyclical industry leveraged to corporate activity, Evercore has built earnings redundancy by expanding its advisory coverage across new sectors and geographies.

Over the past decade, revenue has increased 12% annually. Moreover, the business has an exceptional track record of rewarding shareholders, returning US$2.6 billion to equity holders since 2018 and increasing the dividend each year since 2008.

This week’s reading and viewing list covers Investing In The Era of Climate Change w/ Bruce Usher, AI Commoditization and Capital Dynamicsand The Transition to a Higher Cost of Capital.

The COVID-19 era witnessed unprecedented growth in technology stocks, fueled by government stimulus packages and historically low interest rates.

This perfect storm of economic conditions created a fertile ground for a risk off attitude with tech companies a significant beneficiary, many seeing their valuations soar to dizzying heights. However, as central banks began to tighten monetary policy and raise interest rates to combat inflation, numerous tech darlings experienced sharp corrections, leaving investors questioning the sustainability of their growth narratives and valuations.

Following a difficult period, a select few companies have managed to regain their footing and approach their previous share price heights. One such standout is Life360 (ASX: 360), a family-focused social networking and location-sharing platform. Unlike many of its peers that have struggled to recover, Life360 has managed to not only return to those heights but exceed, attracting renewed investor interest.

The company’s ability to navigate the challenging post-stimulus environment and deliver value in an era of higher interest rates sets it apart in the tech sector.

About the Company

Life360 offers a comprehensive family-oriented platform designed to keep loved ones connected and safe.

The company’s flagship mobile application and Tile tracking devices form the core of its product ecosystem, providing users with a suite of features including real-time location sharing, safe driver reports, and crash detection with emergency dispatch capabilities. With a global reach extending to over 150 countries and approximately 66 million Monthly Active Users (MAU’s), Life360 has established itself as a leader in the family safety and connectivity space. The company’s mission to deliver peace of mind resonates with families of all types, addressing the universal need for security and connection in an increasingly digital world.

Life360’s recent expansion includes the acquisition of Tile, enhancing its ability to track not just people but also pets and valuable belongings. The move has broadened the company’s service offerings and strengthened its market position. As Life360 continues to innovate and grow, it has taken steps to increase its presence in the U.S. market, including a recent initial public offering aimed at boosting capitalisation and financial flexibility

The company’s Nasdaq initial public offering marks a significant milestone. The offer consisted of 5,750,000 shares of common stock priced at $27.00 per share, with 3.7 million shares being offered by Life360 and a further 2.05 million from existing investors. The company raised approximately $100 million from the sale of its shares, which will be used to bolster its financial position and fund general corporate purposes including working capital. Trading on the Nasdaq under the ticker symbol (NASDAQ: LIF) commenced on June 6, 2024.

The US is viewed by management as a natural progression in the company’s expansion, potentially opening doors to a broader investor base and increased market visibility.

How They’ve Turned it Around

Life360 has seen its share price more than double in the last 12 months.

The catalyst for the incredible growth has been driven by the company’s strategic pivot towards monetising its valuable user base through advertising. After experiencing volatility in 2022, with shares falling to $2.50 in June amid a broader tech sell-off, the company has rebounded strongly. The new advertising offering leverages Life360’s unique position in the family-tracking app market, tapping into a high-value demographic that is particularly attractive to advertisers. The company’s extensive first-party location data provides a rare and valuable asset for contextually relevant advertising.

The announcement sparked market enthusiasm and led to an impressive 38% increase on the day.

While initial revenue from this new offering in Q1 2024 was minimal, Life360 anticipates significant growth in the second half of 2024 and substantial scaling in the coming years. The company has completed development work for programmatic ads and expects to be set up for direct sales at scale.

The move positions Life360 to potentially transform its business model, creating a major new source of revenue while maintaining a privacy-first approach that complements the user experience.

Recent Results

In a Q1 update to the market, Life360 showcased impressive financial and operational performance.

Total revenue increased by 15% year-over-year to $78.2 million, driven by a 19% rise in subscription revenue, which reached $61.6 million. Core subscription revenue, excluding non-core hardware-related subscriptions, saw a 23% increase to $57.0 million. The company achieved a record net addition of 96,000 Paying Circles, a 21% year-over-year growth, bringing the total to 1.9 million. Paying Circles represent groups of users subscribing to Life360’s premium services. MAUs also grew significantly, with 4.9 million new users added, a 31% year-over-year increase, totaling approximately 66.4 million globally.

Life360 reported its sixth consecutive quarter of positive adjusted operating earnings at $4.3 million, a substantial improvement from $0.5 million in Q1 2023, and narrowed its operating earnings loss to $4.1 million from $12.6 million the previous year.

Annualised Monthly Revenue (AMR) reached $284.7 million, up 19% year-over-year. Additionally, the company generated positive operating cash flow of $10.7 million, an improvement of $19.9 million from Q1 2023.

The TAMIM Takeaway

Life360 has progressively moved through the broad peaks and troughs of technology share price movements of the 2020 to 2022 period. The company is showing impressive growth in its key operations measurements, as well as improving financial performance, hence it has gained prominence in the past 12 months.

Life306’s innovative approach to monetisation, particularly through its new advertising offering, has positioned it for continued future growth. With impressive Q1 2024 results and significant user base expansion, Life360 is capitalising on its unique market position in the family-focused technology sector. The company’s streak of positive adjusted operating earnings and improved cash flow underscore its operational efficiency. As Life360 begins to leverage its valuable first-party data and expand its advertising capabilities, it is poised for further financial growth and market penetration. The recent Nasdaq listing opens new avenues for investment, reinforcing Life360’s status as a compelling opportunity in the technology sector.

With a clear strategy and strong execution, Life360 is well-positioned to continue expanding its user base, collecting valuable data and providing value to its customers. In turn, with both operational and financial metrics showing positive progress, this technology company should continue to be on investor’s radar.