This week’s TAMIM Reading List dives into a fascinating array of topics. Discover how aging unfolds in dramatic waves during our 40s and 60s, and explore the pivotal role of the mortgage market in monetary policy. We take a journey to the origins of life with plankton and learn about the longest nerve in the body and its crucial role in connecting the mind and body. For a lighter note, find out the best way to load a dishwasher, read about an unusual encounter with a stranger, and reflect on life’s milestones as one writer turns 60. Each article offers fresh perspectives and intriguing insights.

As the reporting season draws to a close, it’s understandable if you’re holding your breath as some companies delay releasing potentially lacklustre results.’

While not every report can be a winner, we believe the last few weeks had two further standout performers in ClearView Wealth (ASX: CVW) and Austco Healthcare Limited (ASX: AHC). Both companies continue to see the benefits of strategic focus while growing organically.

Let’s take a deeper look at both earnings results below.

ClearView Wealth’s Success Driven by Strategic Precision

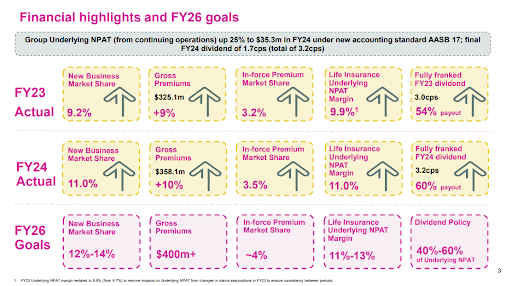

ClearView Wealth (ASX: CVW) has delivered strong performance for FY24, reinforcing its strong market position in the Australian life insurance sector.

The company’s strategic shift towards focusing solely on its core life insurance business has continued to yield positive results. This year, the company’s underlying net profit after tax (NPAT) rose by 25% to $35.3 million.

ClearView’s new business market share increased to 11%, up from 9% in the previous year, indicating an expanding presence in the market. Gross premiums rose by 10% to $358.1 million, driven by strong customer acquisition and retention efforts. Life insurance underlying NPAT improved by 23% to $39.5 million, reflecting effective management and favourable market conditions.

Underscoring the success of ClearView’s strategies in attracting new customers, new business growth expanded by 34% to $33.7 million, up from $25.2 million in FY23.

In line with its strong financial performance, ClearView declared an interim dividend of 1.5 cents per share in March 2024 and a final dividend of 1.7 cents per share in September 2024, bringing the total FY24 dividend to 3.2 cents per share. ClearView’s net assets stand at $353.2 million, with an embedded value of $591.1 million (including franking credits), equivalent to 91.4 cents per share.

Strategic Focus and Business Simplification

ClearView has maintained a clear strategic focus on its life insurance business, simplifying its operations to become a dedicated life insurer.

A cornerstone of this strategy is ClearView’s technology transformation, aimed at providing greater flexibility and enabling customised solutions tailored to the evolving needs of customers and distribution partners.

Leveraging its expanding distribution network and enhanced data insights, ClearView aims to make life insurance more accessible and improve customer experiences. This strategic direction is supported by the company’s exit from wealth management and the sale of its advice business to Centerpoint Alliance (CAF). This divestiture enables ClearView to concentrate fully on life insurance, driving growth in its most profitable segments. We estimate the wealth division exit to complete in March 2025.

Outlook

Looking forward, ClearView remains optimistic about sustaining its growth trajectory, targeting an FY26 underlying margin of 11-13%. This expected margin expansion will be driven by scale efficiencies, increased underwriting risk exposure, and cost savings from the company’s technology initiatives. This will also yield higher dividend payments.

The company’s key strategic priorities include continued business simplification and significant technology investments. The planned migration of existing portfolios onto a new functional platform is set to deliver substantial scale and efficiency benefits starting in the first half of FY26.

ClearView appears well-positioned to seize future market opportunities, and we anticipate the stock will re-rate to its fair value of 90+ cents as it proves these targets during FY26 (next 12-15 months).

Austco Healthcare: Record-Breaking Results Fueled by Strategic Acquisitions

Austco Healthcare Limited (ASX: AHC) delivered an outstanding performance in FY24, marked by record-breaking revenue and profit figures.

The company reported a 39% increase in revenue, reaching $58.2 million, and an impressive 213% growth in net profit after tax (NPAT) to $7.1 million. Growth in unfilled contracted orders continued with $50.3 million (as of 15 August 2024) representing confirmed contracted orders from customers that have not yet been fulfilled and, as such, no revenue recognised.

These results display Austco’s successful execution of its growth strategy, which combines organic expansion with strategic acquisitions.

A significant portion of the revenue growth was driven by the acquisitions of Teknocorp and Amentco, which contributed $6.5 million and $2.7 million, respectively. Organic growth also played a crucial role, particularly in the North American and Asian markets. The gross margin for FY24 was AUD 30.7 million, an increase of 37% from the previous year, although the gross margin percentage slightly declined due to the integration of the lower-margin acquired businesses. The company anticipates that as integration progresses, margins will improve in the medium term.

Strategic Initiatives and Market Tailwinds

Austco’s strategic focus on expanding its software and subscription-based revenue streams was evident, with Software and SMA revenues growing by 9% to $9.3 million.

This growth represents a key opportunity for Austco to further integrate and expand these revenue streams within the newly acquired businesses. The company also made significant strides in reducing its cost base, with overhead expenses increasing only slightly relative to revenue growth. This cost discipline, combined with strong operating leverage, enabled Austco to more than double its operating earnings, which exceeded the top end of the company’s guidance.

Outlook

Austco’s outlook for FY25 appears promising, bolstered by its record-high unfilled contracted orders.

The company plans to continue leveraging its recent acquisitions to drive further revenue growth, particularly in the high-growth markets of North America and Asia. Austco’s strategic roadmap includes launching innovative products, forming strategic partnerships, and exploring potential mergers and acquisitions, all of which are expected to strengthen its market position and contribute to long-term profitability.

Overall, Austco Healthcare’s record-breaking performance in FY24 reflects its strong operational execution and strategic focus, positioning the company for continued success in the healthcare technology space.

The TAMIM Takeaway

Both ClearView Wealth and Austco Healthcare are examples of the type of innovative, growth-oriented companies that align with TAMIM’s investment strategy.

These businesses strike a balance between organic growth, business simplification and strategic acquisitions, delivering impressive financial performance despite their competitive markets. These companies are not just responding to market demands but proactively transforming the way they operate.

As they continue to leverage their unique strengths, both ClearView and Austco are well-positioned to deliver long-term value and attractive returns for patient investors.

Disclaimer: Austco Healthcare Limited (ASX: AHC) and ClearView Wealth (ASX: CVW) are held in TAMIM Portfolios as at date of article publication. Holdings can change substantially at any given time.

Market sentiment is a powerful force that often drives fluctuations in stock prices and market volatility, sometimes overshadowing the actual business fundamentals.While sentiment can be a useful gauge of market mood, relying on it to make investment decisions introduces significant risks. As Benjamin Graham wisely observed, “The investor’s chief problem—and even his worst enemy—is likely to be himself.” This underscores the peril of sentiment-driven investing, where emotions and herd behaviour can lead to decisions that stray far from a company’s true value.To avoid these pitfalls, investors should consider second-level thinking—a concept championed by Howard Marks, co-founder of Oaktree Capital Management. While first-level thinkers react impulsively to immediate events, second-level thinkers dig deeper to assess the broader implications of those reactions. In a market where sentiment can easily cloud judgement, this level of thinking becomes indispensable. Investors must scrutinise whether the prevailing market enthusiasm or fear is justified—whether soaring stock prices, driven by multiple expansion, genuinely reflect a company’s future potential, or if they have become overinflated, making the risk unattractive. Conversely, they should evaluate whether negative sentiment, triggered by macroeconomic events or a single company’s earnings announcement, has been exaggerated, leading to unjustified price declines.By mastering this understanding of market behaviour, investors can position themselves to have the market serve them, rather than being misled by its emotional swings.

The Double-Edged Sword: When Sentiment Becomes the Market Driver

Multiple expansion is often a sign of sentiment-driven investing. As an example, where a company’s price-to-earnings (P/E) ratio increases not due to improved fundamentals but because investors are willing to pay more for each dollar of earnings. This can lead to inflated share prices that are not a true reflection of the company’s actual performance. Nvidia (NASDAQ: NVDA), a leader in the semiconductor industry, serves as a textbook example. Although Nvidia’s fundamentals are robust, its share price has surged largely due to multiple expansion fueled by investor enthusiasm for its pivotal role in emerging technologies such as artificial intelligence and gaming. However, this sentiment-fueled rise has pushed Nvidia’s valuation to potentially unsustainable levels, posing a risk to investors buying at these elevated prices. Conversely, negative sentiment can lead to undervaluation, where a company’s share price is unfairly depressed due to broader market fears. This scenario often unfolds during market downturns, where panic selling drives prices down across the board, regardless of a company’s fundamental strength.. The Oracle of Omaha, Warren Buffett, has long advocated for buying during such periods of irrational pessimism, famously stating, “Be fearful when others are greedy, and greedy when others are fearful.” Historically, there have been numerous instances where strong companies were unduly punished by negative sentiment, creating buying opportunities for contrarian investors. For example, during the initial stages of the Covid-19 pandemic many high-quality companies were sold off in the panic. When there was so much unknown investors were quick to take money off the table, only for share prices to recover and thrive in the subsequent years.

The Perils of Timing the Market Based on Sentiment Alone

One of the most perilous aspects of sentiment-driven investing is the temptation to time the market based on fleeting emotions. As discussed earlier, positive sentiment can lead to FOMO where investors chase after hot companies or sectors, often buying in at peak prices. Though this strategy might deliver short-term gains, it carries substantial risks. The upside of each investment becomes more and more limited as multiples expand. As market sentiment shifts, these potentially overvalued shares can experience sharp declines, leaving investors with substantial losses. The long-term impact of an investment decision peak sentiment (and multiples become detached from reality in either direction) could be devastating for both your portfolio and your investing mindset. Investors who succumb to FOMO can find themselves in a position where they must sell low during market corrections, locking in losses and potentially derailing their financial goals. In contrast, a contrarian approach to investing—buying when others are selling and selling when others are buying—has proven successful over time. This strategy is based on the understanding that markets often overreact to both good and bad news. By going against the crowd, contrarian investors can potentially capitalise on the market’s misjudgments. Studies indicate that companies bought during periods of low sentiment and market downturns tend to outperform in the long run. Similarly, selling during periods of high sentiment can help investors avoid the pitfalls of market bubbles. It’s easier said than done. When markets turn it often goes against everything your mind is telling you to buy into a declining market. Investing is difficult, and timing the market is even more challenging.

Lessons from History: The Impact of Sentiment on Investment Outcomes

History is replete with examples of how sentiment can push markets to extremes.The tech bubble of the early 2000s is a classic case where investor enthusiasm for internet companies pushed valuations to unsustainable levels. Companies like Pets.com, theGlobe.com and eToys saw extreme price movements, often being valued based on page views and projected revenue rather than actual revenue and profitability. Despite the initial hype, these companies struggled to generate sustainable income and eventually collapsed.As the bubble burst, trillions of dollars in market value was wiped out.The lesson is clear: while sentiment can be an investor’s ally, it can also become a trap, especially for those who fall into the cycle of buying high and selling low. For second-level thinkers, the focus should be on discerning what is truly driving market or individual stock prices. Is sentiment working in your favour, pushing your investments higher, or is it presenting an opportunity where prices have become disconnected from long-term business fundamentals?By grounding decisions in thoughtful analysis and questioning whether an investment is rooted in solid fundamentals or merely riding a wave of excitement, investors can cultivate a mindset that remains steady amidst market noise. Achieving long-term outperformance often requires a different approach from the majority. By thinking and behaving differently from the crowd, investors can leverage sentiment to their advantage, rather than being led astray by it.

The TAMIM Takeaway

In a sentiment-driven market, it’s easy to be swept up by the excitement of soaring prices or the panic of sudden downturns.So, how do you successfully navigate these emotional tides?The most successful investors are those who rise above the noise, employing second-level thinking to evaluate the true value of their investments, regardless of the market’s current mood. As Howard Marks wisely pointed out, “You can’t predict. You can prepare.”By maintaining a focus on long-term fundamentals and resisting the temptation to follow the crowd, investors can skillfully navigate the complexities of sentiment-driven markets and position themselves for sustained success.In the end, the key to thriving in today’s investment landscape isn’t about riding the wave of sentiment, but about accurately valuing the future and making informed, thoughtful decisions.

Governments serve as the driving force, utilising three key aspects as pillars of power with leadership in these pillars defining the winners of the new global order. What are the pillars of power and why are they the focus sectors for our Global Tech and Innovation Fund.

Disc: All investing entails risk – please read disclaimer on our website for more details – www.tamim.com.au.