This week’s TAMIM Reading List offers a deep dive into the forces shaping modern society and business. We explore the possibility of an “epic vibe shift” in America’s economic outlook and how Mr. Beast’s viral success holds lessons for the Gen Z workforce. From Cliff Asness navigating multiple quant crises at AQR to the looming subprime AI crisis, we examine key shifts in finance and technology. Learn about the iPhone 16’s innovations, surprising insights into inflation, and a breakdown of how shows like Hacks and The Bear are reshaping television. Each article connects to larger trends driving change in our world today.

As Artificial Intelligence (AI) reshapes industries globally, Australian companies like AI Media (ASX: AIM) are leveraging AI to transform their business models and drive growth. The Australian market is poised to benefit from AI’s projected $315 billion contribution to the economy by 2030, and local tech stocks are at the forefront of this revolution. In this two-part series, we highlight two ASX-listed companies that provide the best exposure to AI’s high-growth applications.

In Part 1, we covered Nuix (ASX: NXL), a leader in AI-driven data processing and investigation software. Nuix has shown significant growth through its proprietary Nuix Neo platform, which offers innovative solutions in legal, privacy, and forensic markets. Now, in Part 2, we explore AI Media (ASX: AIM), a company rapidly transitioning to an AI-powered technology business with global ambitions.

Part 2 – AI Media (AIM)

Company Overview and Business Model:

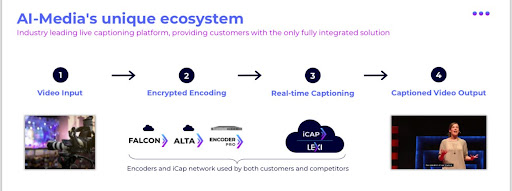

AI Media has been transforming its operations from a services-based business to a technology-focused company, centred around AI-powered language services. The company’s flagship product, Lexi, is an AI-powered captioning and transcription solution that integrates into customers’ workflows through AI Media’s EEG encoder devices and iCap network. This transition is key to their strategy of moving toward higher-margin, recurring technology revenue.

As highlighted by AI Media’s Chair in the 2024 Annual Report, the acquisition of New York-based EEG in 2021 played a critical role in the company’s evolution. This acquisition enabled AI Media to expand its suite of AI-driven technology solutions and diversify its customer base globally. In FY2024, approximately 50% of AI Media’s revenue came from technology sales, a significant increase from FY2022, when technology revenue accounted for just a portion of overall sales. The company achieved a compound annual growth rate (CAGR) of 35% in technology revenue from FY2022 to FY2024, significantly improving its gross profit margins from 55% to 64%.

AI Media’s Lexi 3.0, launched in May 2023, represents the latest in AI-powered live captioning solutions. Lexi 3.0 rivals human captions in accuracy but at a fraction of the cost. It delivers captions for a wide range of content, including live TV, sports, government proceedings, and more, through AI Media’s integrated encoder and iCap Cloud Network, providing a competitive moat for the company.

AI Media’s success is also reflected in its customer diversification. The company has grown its reach to include sports rights holders, local and federal governments, large enterprises, and universities. In FY2024, the company expanded its global presence by building its sales team and forming strategic distribution partnerships, leading to major contract wins and a robust sales pipeline for FY2025.

FY2024 Financial Results:

AI Media’s FY2024 results reflect its successful transition to a technology-driven business. The company reported $66.2 million in revenue, a 7% year-over-year increase, despite a gradual decline in low-margin services revenue. This decline was offset by a rapid rise in the high-margin technology segment, which boasts gross margins of 85%.

Overall, the company’s gross margins improved to 64%, driven by a 37% increase in technology revenue and a 39% increase in technology gross profit. AI Media remains cash flow positive with $11 million in cash on hand. Its $8 million R&D investment highlights the company’s commitment to innovation, though only $500,000 of this was capitalised, demonstrating conservative accounting practices.

Outlook for FY2025:

Looking ahead, AI Media aims to have 80% of its revenue come from technology by December 2025, up from the current 50% level. The company’s five-year targets are ambitious, with management aiming for $150 million in revenue and $60 million in EBITDA by focusing on geographic expansion, sector diversification, and new AI-powered product launches.

A key part of the company’s strategy is growing its iCap network and introducing new AI products such as audio description and voice services. AI Media is also considering strategic acquisitions to accelerate growth, replicating its successful U.S. acquisition of EEG in other regions.

TAMIM Takeaway:

AI Media represents one of the most promising AI-focused companies on the ASX. With a strong foothold in global markets, AI Media’s business transformation, bolstered by its flagship Lexi platform, positions it well for long-term growth. The company boasts strong revenue and profit growth, a cash-rich balance sheet, and a highly committed leadership team. The Founder and Managing Director, holding a 16% stake, has continued to purchase shares, signalling confidence in AI Media’s future. Tony Abrahams is the kind of high energy and passionate founder we like to back here at TAMIM.

With technology revenue growing at 35% annually, we value the stock at around 90 cents in the medium term. As AI Media continues its rapid transition, the market is likely to price it according to its trajectory towards its five-year goal of $150 million in revenue and $60 million in EBITDA. At that point, a valuation of $5.00+ is achievable, making AI Media a potential ten-bagger over the next few years.

Taking time to revisit the basics periodically is a practice we’ve always advocated for. When you’re living and breathing the markets day in and day out, it’s easy to lose sight of fundamental principles—sometimes you can’t see the forest for the trees. The beauty of the basics is that they often remain consistent over long periods, even while the world around them changes. Today, we want to take a moment to reflect on what we’d tell our 21-year-old selves about finances and achieving financial independence, focusing on several time-tested principles.

These concepts are not just independent rules but interconnected ideas that influence each other. The markets are complex, and while no principle can be applied in isolation, the basics are your building blocks. Once mastered, they can be expanded upon and made more intricate as your understanding deepens.

Principle 1: High Return = High Risk

At its core, the market is a function of risk, although recent years of unconventional monetary policy may have blurred this fact. Understanding risk and return is essential for any investor. The strongest portfolios are those that maximise expected returns while minimising risk. To illustrate, imagine two investments, A and B, with identical expected returns. The key to choosing between them lies in determining which carries the lower risk. But here’s the tricky part: investment is as much an art as it is a science, meaning that sometimes your decision will hinge on both quantitative analysis and your belief in the investment.

Risk is often manifested as volatility, and as investors, we must learn to live with it. Market fluctuations can be harsh—Charlie Munger famously noted that a 50% drawdown is the “price of admission.” But it’s important to keep perspective. Aside from rare events like the Great Depression, the markets have historically been generous over the long term. Volatility is best viewed through the lens of time. If your investment horizon is measured in decades rather than years, volatility becomes less concerning. The longer you stay invested, the more you can tolerate short-term fluctuations. This brings us to a critical mantra: time in the market beats timing the market.

Principle 2: The Rule of 72 and the Power of Compounding

It is rumoured that Albert Einstein called compound interest the “eighth wonder of the world,” and nowhere is this more evident than in the Rule of 72. This rule helps investors estimate how long it will take for their money to double based on a given rate of return. For example, with an annualised return of 7.2%, your money will double in ten years. It sounds simple, but understanding compounding through this lens encourages discipline and patience. There’s no need to rush—time does much of the heavy lifting for you.

Consider an example: $100,000 invested at 7.2% annually grows to $1.6 million over 40 years, without any additional contributions. Now imagine adding regular investments into the mix. The results become even more powerful. This strategy, known as dollar-cost averaging, not only helps you build wealth but also mitigates sequencing risk—the risk of poor returns during specific periods of time. Regular contributions, especially in volatile markets, help smooth out returns and reduce the emotional decision-making that often plagues investors during market swings.

For those with a higher risk appetite, consider a rules-based system. When the market experiences a drawdown, buy more shares incrementally. Conversely, reduce your purchases as markets rise. This approach aligns your investments with market sentiment, ensuring your strategy adjusts based on the level of fear or greed in the market.

Principle 3: Don’t Borrow What You Can’t Repay

Leverage can be one of the most powerful tools in investing, amplifying both returns and losses. Used correctly, debt can be productive—leveraging property investments or making strategic stock purchases can be wise moves. But debt for debt’s sake is dangerous. Always plan for worst-case scenarios. For instance, if you’re investing in property, ask yourself: what would happen if your rental income was halved or interest rates doubled? Prepare for the worst, even if the capital seems freely available.

For equity investors, leverage can be especially risky. Your ability to withstand margin calls often depends more on your emotional stability than on the actual numbers. If your first experience with leverage was positive, it might encourage risky behaviour. But if it was negative, you might become overly cautious, even when it’s not warranted. The lesson here is to only use leverage for a small portion of your portfolio and never borrow more than you can afford to lose. Plan as though your borrowed capital could go to zero, and invest accordingly.

Principle 4: Quit Procrastinating

Procrastination is one of the most common pitfalls for investors. With so much information available, it’s easy to fall into the trap of over analysing and delaying decisions. However, the markets will never offer perfect clarity. At some point, you must develop a view, take action, and be prepared to adapt if conditions change.

Waiting for the perfect moment can be just as harmful as making a rash decision. The overload of information—often conflicting—can lead to analysis paralysis. For instance, if you wanted to research every detail about a stock like Apple (NASDAQ: AAPL) before buying, you might never actually make the purchase. The sheer volume of available information makes this an impossible task. Don’t let perfection be the enemy of progress. Set your goals, understand your parameters, and, as Nike says, “just do it.”

Remember, even doing nothing is a decision. If you decide not to act, make sure it’s based on logic, not fear. And always challenge yourself: if you’re not investing, ask why. Pretend you’re explaining your reasoning to a room full of financial experts who will question every assumption you make. If you can’t justify your inaction, it’s time to reconsider.

Principle 5: Diversification is Vital

Diversification is one of the most powerful tools for managing both short-term volatility and long-term market risk. While full-time investors may afford a more concentrated portfolio, most people should diversify to spread their risk. Even the best companies can fail, as demonstrated by the likes of Kodak, which once dominated its industry but has since faded into obscurity.

The challenge with diversification is finding the right balance. As you add more investments, the marginal benefit decreases while costs increase. A portfolio of 15 to 30 investments or strategies is generally optimal, and older investors may prefer the higher end of that range. Diversification allows you to reduce the risk of any single investment having an outsized impact on your overall portfolio, ensuring that your long-term goals remain intact.

Principle 6: Ask Questions

Asking questions is fundamental, not just in investing, but in life. It’s how we learn and grow. Every time you consider a new investment, ask “why” until you’ve thoroughly explored every assumption. This relentless curiosity will make you a better investor.

And don’t be afraid to ask tough questions of your financial advisors or portfolio managers. After all, you’re the one with skin in the game. At AGMs, remind management that they are simply custodians of your capital. You’re the owner, and it’s your right to demand accountability.

Principle 7: Keep an Emergency Cash Fund

Australia is a fortunate country, but it also has one of the highest household debt levels in the developed world. Given today’s interest rate environment in Australia, leveraging debt might seem less appealing than it once was. However, with inflation still a concern, having an emergency fund is more crucial than ever for weathering unexpected financial storms.

As a rule of thumb, younger individuals should keep at least three months’ worth of living expenses in an emergency fund. This cash cushion ensures you’re not forced to sell investments at an inopportune time to cover unexpected costs.

Principle 8: Track Megatrends and Themes When Investing Long Term

This principle ties back to diversification. While you must remain diversified, it’s also important to stay nimble and adjust as new trends emerge. Megatrends, such as demographic shifts, artificial intelligence, and growing income inequality, will have profound effects on markets for decades to come.

For example, slower economic growth in Western countries and changing demographics will impact industries like healthcare and pensions. Meanwhile, advancements in artificial intelligence will disrupt sectors ranging from transportation to retail. However, picking winners in these trends is challenging. Instead of betting on a single company, look for those that provide key components to multiple players within an industry.

The key takeaway: understand how megatrends affect your portfolio and be prepared to adjust your investments accordingly.

Principle 9: Minimise Taxes

Finally, minimising taxes is an obvious but often overlooked principle. The less you pay in taxes, the more wealth you accumulate over time. In Australia, this can be as simple as placing capital growth assets within the superannuation environment or utilising franking credits.

However, tax considerations should never drive your investment decisions. Don’t hold onto an investment just to avoid paying capital gains tax. If a better opportunity arises, it’s worth paying the tax.

The TAMIM Takeaway

At TAMIM, we understand that investing is both a journey and an ongoing learning process. The principles we’ve revisited here—balancing risk and return, leveraging the power of compounding, maintaining diversification, and staying disciplined—are the foundational elements for long-term financial independence. Whether you’re an experienced investor or just starting, these concepts remain as relevant today as they were decades ago.

In particular, the importance of staying proactive cannot be overstated. Making consistent, thoughtful decisions and adapting to evolving market conditions is key to success. While the markets can be complex, staying focused on these tried-and-true basics will help you navigate uncertainty and take advantage of opportunities.

This week’s TAMIM Reading List offers a range of thought-provoking topics. Explore why Elon Musk’s dream of colonising Mars may never come to fruition and question whether professional forecasters are too confident in their predictions. We also dive into the plastics industry’s manipulation of recycling definitions and examine the stunning economics behind OnlyFans. Learn how Europe is embracing train travel for sustainability, revisit predictions from 1974, and discover why health experts are rethinking whole milk and cheese. Each article provides a fresh perspective on the intersection of technology, society, and sustainability.

Artificial Intelligence (AI) is no longer just a futuristic concept; it is reshaping industries across the globe, creating massive opportunities for businesses that can harness its potential. From automating complex processes to driving new innovations in data analysis and decision-making, AI’s rapid adoption is set to drive significant growth in the global economy. According to research by PwC, AI is expected to contribute up to $15.7 trillion to the global economy by 2030, with Australia standing to gain $315 billion in additional economic value over the next decade.

In Australia, AI is becoming increasingly integral across sectors such as healthcare, financial services, legal services, and logistics. Companies that leverage AI to enhance efficiency and deliver intelligent solutions are positioning themselves to benefit from this explosive growth. The ASX is home to several businesses that are at the forefront of AI-driven innovation, providing investors with a compelling opportunity to tap into this trend.

In this two-part series, we explore two Australian companies that offer the best exposure to the rapidly growing applications of Artificial Intelligence (AI). These companies not only operate in high-growth sectors but also showcase strong profitability, scale, and have strong net cash balance sheets. With management teams heavily aligned with shareholder interests, these businesses are positioned to deliver long-term value. We believe their current share prices represent an attractive entry point for investors.

Part 1 – Nuix (ASX: NXL)

Company Overview and Business Model:

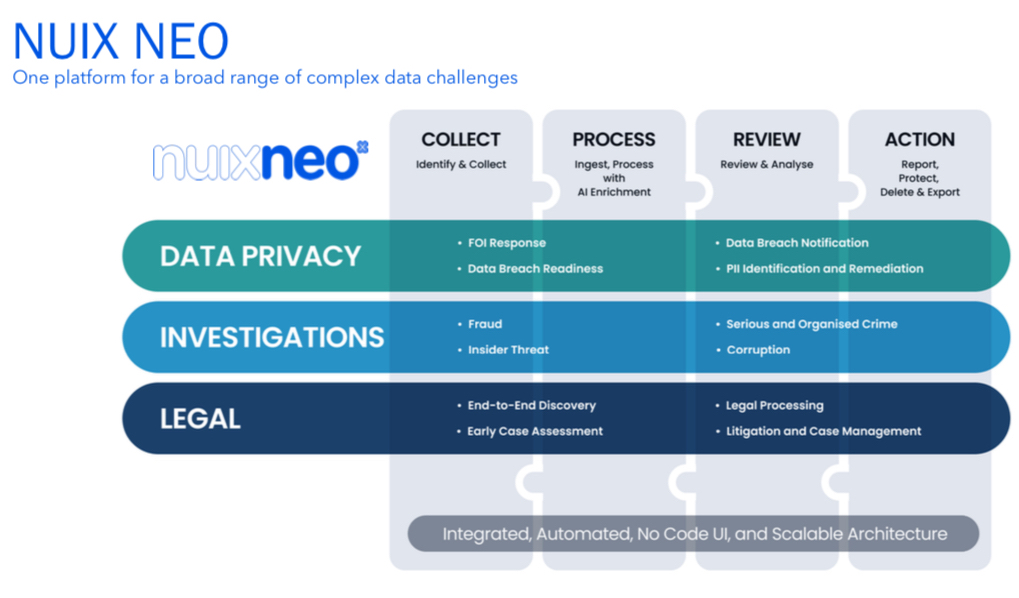

Nuix is an Australian-based software company that specialises in delivering intelligence solutions globally. Its core product, the Nuix Neo platform, provides cutting-edge tools in data privacy, forensic investigations, and legal case processing. Nuix’s data processing engine, enhanced by proprietary AI, is at the heart of its solutions, enabling the company to simplify complex data challenges for its customers.

The company’s acquisition of Rampiva last year significantly enhanced its automation capabilities, enabling clients to achieve higher operational efficiency. While Nuix’s products can be intricate, they address real-world problems for a wide range of industries, particularly in legal and investigative fields. Nuix products can be complex and difficult to understand but the following graphic does a good job of highlighting the 3 key products:

Operating in a global market, Nuix generates 85% of its annual contract value (ACV) from clients outside Australia. With a portfolio of 1,000 high-quality customers, including those in law enforcement, government agencies, and large enterprises, Nuix has a strong market presence. Over 75% of its clients have been with the company for more than five years, illustrating the strength of its offerings and long-term relationships.

FY2024 Financial Results:

Nuix’s financial results for FY2024 exceeded expectations across the board. The company achieved a 14% increase in ACV, reaching $211.5 million, with 95% of this revenue coming from recurring subscriptions—a key metric in evaluating software companies. This success was largely driven by the Nuix Neo platform, which contributed to nearly half of the ACV growth.

Nuix also outpaced its revenue growth target, delivering a 20.9% increase to $220.6 million, well above the 10% constant currency growth goal. Its net dollar retention rate—a crucial measure of customer retention and upselling—rose to an impressive 112.9%.

Profitability was another highlight, with underlying EBITDA growing 38.7% to $64.4 million, and statutory EBITDA climbing 60.2% to $55.9 million. Strong operational leverage resulted in positive cash flow generation, a notable turnaround from the previous year, with $24.7 million in underlying cash flow and $11.9 million in total cash flow.

Outlook for FY2025:

Nuix has set ambitious targets for the upcoming financial year, aiming for 15% ACV growth while continuing to grow revenues faster than operating costs. A portion of this growth will be driven by increased R&D investments, with a focus on further enhancing the Nuix Neo platform and expanding its core solutions to appeal to a broader customer base.

The company also has a $30 million debt facility in place to explore M&A or partnership opportunities, which could further accelerate its growth strategy. With a strong cash position and improving profitability, Nuix is well-equipped to pursue these initiatives.

TAMIM Takeaway:

Nuix’s transformation, exemplified by its FY2024 performance, highlights the potential of its AI-driven solutions and the strength of its global customer base. The company’s focus on operational efficiency and continued innovation positions it to capitalise on the massive opportunities in the AI space.

Looking ahead, Nuix Neo AI capabilities have the potential to drive revenue growth by 2 to 3 times over the next 5 to 10 years, coupled with expanding profit margins. With double-digit revenue growth and high EBITDA margins, Nuix is on track to become a Rule of 40+ software company—a key indicator of both growth and profitability. Global peers in this category typically trade at 7-10x sales, and we believe Nuix’s valuation could reach $10.00+ per share in the next 2-3 years.

AI Media has been transforming its operations from a services-based business to a technology-focused company, centred around AI-powered language services. The company’s flagship product, Lexi, is an AI-powered captioning and transcription solution that integrates into customers’ workflows through AI Media’s EEG encoder devices and iCap network. This transition is key to their strategy of moving toward higher-margin, recurring technology revenue.

AI Media has been transforming its operations from a services-based business to a technology-focused company, centred around AI-powered language services. The company’s flagship product, Lexi, is an AI-powered captioning and transcription solution that integrates into customers’ workflows through AI Media’s EEG encoder devices and iCap network. This transition is key to their strategy of moving toward higher-margin, recurring technology revenue.