In a recent episode of the All-In Podcast, Scott Bessent, the newly appointed U.S. Treasury Secretary under President Donald Trump, provided deep insights into the economic challenges facing the United States. The conversation, hosted by Chamath Palihapitiya, and David Friedberg, was expansive, covering topics from debt management to deregulation and the establishment of a sovereign wealth fund.

As the former Chief Investment Officer of Soros Fund Management and founder of the hedge fund Key Square Group, Bessent’s insights are grounded in decades of financial experience. His tenure as Treasury Secretary is likely to shape U.S. economic policy for years to come, with significant implications for global markets, including Australia. This analysis will break down the key points discussed during the podcast, examining their potential impacts and providing statistical context where applicable.

National Debt and Deficit Concerns

One of the central themes of the conversation was the alarming trajectory of the U.S. national debt and deficit. The U.S. budget deficit recently hit a record $840 billion over a four-month period, a figure reported by Bloomberg that highlights the unsustainable nature of current fiscal policy. Bessent drew comparisons to European economies that have been caught in cycles of stagnation due to excessive debt accumulation. His plan emphasises the need for targeted spending cuts, particularly within areas of wasteful government expenditure. According to the Congressional Budget Office (CBO), U.S. debt is projected to exceed 125% of GDP by 2030 if current trends continue.

Revitalising the American Dream

Bessent’s vision for economic policy includes restoring key aspects of the American Dream: home ownership, financial security, purposeful employment, and the ability to support a family without the need for multiple jobs. He emphasised that this vision requires addressing both inflation and wage stagnation. According to data from the U.S. Bureau of Labor Statistics, real wages have grown by only 0.7% annually over the last decade, failing to keep pace with rising costs of living. This dynamic has exacerbated income inequality, a problem Bessent aims to tackle through deregulation and enhanced productivity.

The ‘3-3-3’ Economic Strategy

Perhaps the most ambitious proposal laid out by Bessent was his ‘3-3-3’ economic strategy:

Achieving 3% real GDP growth.

Reducing the budget deficit to 3% of GDP by 2028.

Increasing U.S. energy production by 3 million barrels per day.

The implications of this policy are profound. A return to 3% GDP growth would significantly boost tax revenues and potentially ease the burden of debt repayment. However, reaching this target will require structural reforms that enhance productivity and incentivise private sector investment.

Addressing Government Spending

Bessent’s approach to fiscal discipline focuses on reducing government expenditure rather than increasing revenue. He argued that the U.S. faces a spending problem, not a revenue problem. This view is supported by recent data from the Tax Foundation, which shows that U.S. tax revenue as a percentage of GDP is already among the highest in the developed world. A focus on expenditure cuts, rather than tax increases, could mitigate the risk of dampening economic growth while still addressing fiscal imbalances.

Deregulation Initiatives

Bessent’s commitment to deregulation is aimed at fostering economic growth by reducing bureaucratic constraints on businesses. His focus includes sectors like financial services, healthcare, and energy. According to the American Action Forum, regulatory costs on the U.S. economy exceed $2 trillion annually. Rolling back inefficient regulations could boost productivity and enhance the competitiveness of American industries on a global scale.

Reordering International Trade and Revitalising Manufacturing

Bessent outlined a vision to restructure international trade, promoting domestic manufacturing through tariff incentives and supply chain resilience. This strategy aims to revitalise the U.S. middle class by bringing high-paying manufacturing jobs back to American soil.

Establishing a U.S. Sovereign Wealth Fund

The proposal to create a U.S. Sovereign Wealth Fund is one of the most radical ideas presented by Bessent. The aim is to better manage and grow national assets to generate higher returns and reduce reliance on debt. This approach mirrors the success of countries like Norway, whose Government Pension Fund Global has grown to over $1.4 trillion.

Balancing Energy Policies

Energy security was another priority discussed by Bessent. He highlighted the need for a balanced approach that includes both traditional fossil fuels and renewable energy sources. The goal is to reduce energy costs for consumers while ensuring the U.S. remains a global leader in energy production.

The TAMIM Takeaway

From an Australian perspective, Bessent’s policies are of significant interest. The deregulation of financial markets and emphasis on productivity growth could have positive implications for global capital flows, potentially benefitting Australian companies with exposure to the U.S. market. Moreover, the establishment of a U.S. Sovereign Wealth Fund could have far-reaching consequences for asset allocation and investment trends. As always, TAMIM remains focused on navigating these shifts with insight, foresight, and a steady hand.

Inflation. It’s a term thrown around by newsreaders and politicians, often with a tone of fear. But what does it really mean for Australians? More importantly, what’s happening right now in the United States, and how will that impact us here?

As Australians, we need to pay attention to what’s happening in the global powerhouse that is the US economy. And right now, something interesting is going on. Despite all the noise about rising prices, it appears that inflation is cooling down faster than most analysts predicted. Understanding why this is happening and what it could mean for Australia is crucial if you want to make smart investment decisions.

What is Inflation and Why Should Australians Care?

Inflation refers to the general increase in prices over time. It’s why a carton of milk costs more today than it did ten years ago. Moderate inflation is normal and even healthy for an economy. But when inflation surges too quickly, it can erode purchasing power, damage savings, and disrupt economic stability.

In Australia, inflation rose to a 32-year high of 7.8% in the December 2022 quarter before gradually falling to 5.2% by the September 2024 quarter (ABS). But the story doesn’t end here. Australia is heavily influenced by the economic conditions of major trading partners, particularly the United States. And right now, the US is dealing with some interesting developments that could spill over into our markets.

Why Inflation is Dropping in the US

While everyone has been expecting inflation to remain high, signs are emerging that it is cooling down. Here’s why:

Tariffs and Their Aftermath

The US implemented tariffs against major trading partners, including Canada, Mexico, and China. This led companies to stockpile goods before prices went up. But now that those stockpiles have dwindled, businesses are finding it harder to pass on the higher costs to customers. The result? Profit margins are shrinking, investment is slowing, and layoffs are increasing. This downward pressure on prices is what we call disinflation. Companies can’t charge as much as they want because consumers simply can’t afford it.

Falling Consumer Demand

Consumer spending, which makes up around 70% of the US economy, has been weakening. According to the US Federal Reserve’s Economic Data (FRED), real personal consumption expenditures grew just 1.4% year-over-year in the fourth quarter of 2024, down from 2.7% a year earlier. This decline in spending power is contributing to the slowdown in inflation.

Credit Squeeze

Banks are tightening their lending standards. According to the US Federal Reserve, mortgage applications have dropped by over 40% from their peak in 2022, and rejection rates for credit cards and auto loans are at their highest levels since 2013. If people can’t borrow, they can’t spend. And when people aren’t spending, prices tend to fall.

The Retirement Factor

As Baby Boomers retire, they naturally spend less. This is not just a US phenomenon; Australia will face similar dynamics as our own population ages. But in the US, with over 40% of the stock market and 25% of residential real estate owned by retirees (US Census Bureau), the pressure on asset prices is real.

Why This Matters for Australia

Australia’s economy is closely tied to the US through trade, investment, and financial markets. When inflation dynamics change in the US, there’s often a ripple effect here. Lower inflation in the US means the Federal Reserve could reduce interest rates sooner than anticipated. If that happens, there’s a strong chance the Reserve Bank of Australia (RBA) will follow suit.

Moreover, US financial markets are a major influence on global capital flows. If the Fed eases monetary policy, it could lead to a weaker US dollar, stronger Australian dollar, and better conditions for our exporters.

Is a Recession Coming?

Many signs suggest the US is either already in a recession or heading there. Companies are laying off workers faster than expected. Banks are making it harder for people to get loans. And more people are relying on credit cards just to make ends meet. According to the Cleveland Fed, CEOs now expect inflation to be around 3.2% over the next year — the lowest prediction since 2021.

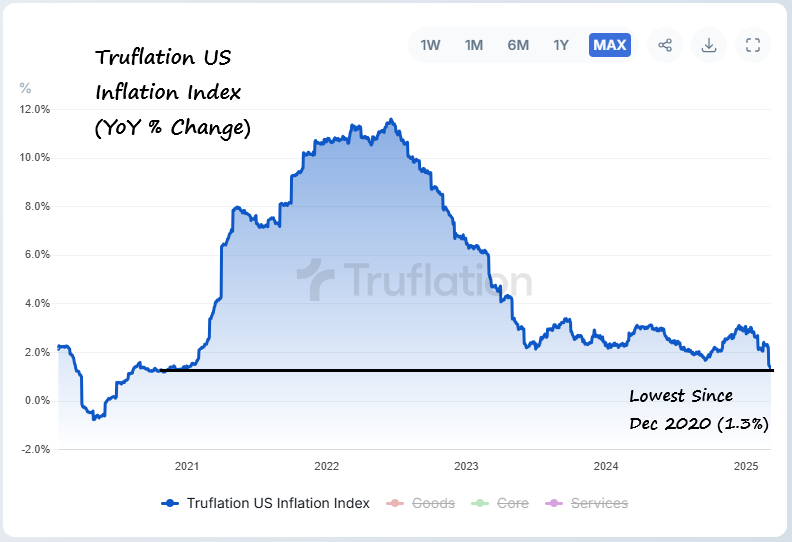

Meanwhile, according to Truflation, a real-time data source that tracks over 18 million data points, inflation could drop to as low as 1.5% within the next few months. If this is accurate, the US Federal Reserve may be far behind the curve in its planning.

What Could Happen Next?

If the US continues on this path, we’re likely to see:

Interest rate cuts sooner than the market expects.

Shifts in global capital flows as investors chase yield in different regions.

A stronger Australian dollar if the US dollar weakens, which could impact our exports.

Improved conditions for growth stocks as falling interest rates make borrowing cheaper.

The TAMIM Takeaway

At TAMIM, we keep a close eye on the global economy, particularly the US, because its moves have direct implications for Australia. The signs are clear: Inflation in the US is cooling, and if the Federal Reserve fails to adjust its policies quickly enough, there could be significant opportunities for astute investors.

Whether it’s identifying undervalued assets, positioning for interest rate cuts, or taking advantage of a stronger Australian dollar, now is the time to prepare. The market often punishes those who react too late. At TAMIM, we believe in being proactive. And right now, the proactive approach means understanding how these global trends will impact your investments.

Want to know how to best position your portfolio for what’s to come? Contact us at TAMIM to discuss your investment strategy today.

This week’s TAMIM Reading List spans finance, technology, and human resilience. As markets shift, we explore perspectives on downturns, why no one should root for a recession, and the growing global pivot away from U.S. investments. Meanwhile, AI’s boom is reshaping power grids, and China is embracing DeepSeek’s potential. We remember the legacy of Daniel Kahneman, dissect Boeing’s worst years, and uncover the hidden insights galaxies hold beyond the cosmic microwave background. Plus, relive the greatest sports moments of the past 25 years, follow the takedown of a crime ring targeting pro athletes, and learn the simple secret to better gut health.

The February reporting season presented one of the most dynamic market environments in recent memory. Earnings results triggered sharp movements, with investors swiftly adjusting their positions based on performance. This created significant shifts in valuations, with certain stocks experiencing price swings of -20% or more in response to earnings surprises.

Portfolio Positioning & Strategic Adjustments

For sophisticated investors, navigating this environment requires a proactive and disciplined approach. Identifying companies with strong fundamentals while managing risk exposure is critical in volatile conditions. Where businesses show genuine structural weaknesses, it is prudent to reassess positions and reallocate capital strategically. At the same time, market overreactions can present opportunities to build on high-conviction holdings at more attractive valuations.

A well-structured portfolio should emphasise quality, resilience, and long-term growth potential. Investors who maintain discipline, refine their asset allocation, and capitalise on market dislocations will likely be well-positioned for the months ahead. Some of the key themes and opportunities in focus are discussed in this report, with further insights to follow.

Market Correction: A Natural Part of the Cycle

Since mid-February, both Australian and U.S. markets have undergone a healthy reset, experiencing a -10% drawdown. This adjustment has been driven by a combination of policy shifts under the new Trump administration and broader economic recalibrations.

History has shown that such periods of adjustment are common and often necessary for long-term market strength. Notably, the recent drawdown from the February 19th highs represents the fastest -10% correction since the COVID recovery in 2020. Understanding these cycles provides important context for long-term decision-making.

The Trump 2.0 Administration: A Structural Shift

The current administration is implementing key structural changes aimed at strengthening the U.S. economy. The focus is on balancing government spending while fostering private sector growth through pro-business policies, tariff realignments, and strategic incentives.

A pivotal figure in this approach is Scott Bessent, the newly appointed Secretary of the Treasury. With a distinguished career in financial markets, his expertise in economic strategy and capital allocation is expected to drive meaningful, long-term improvements. By streamlining regulations and encouraging domestic investment, these initiatives set the stage for a more efficient and resilient economic environment.

Additionally, with true inflation tracking below 1.5% (according to Truflation), the Federal Reserve is expected to adjust interest rates more quickly than current market projections suggest. As the economy stabilises post-adjustment, a supportive rate environment combined with policy-driven expansion could provide a robust foundation for market performance in the coming years.

(Source: truflation.com)

Market Trends & Historical Context

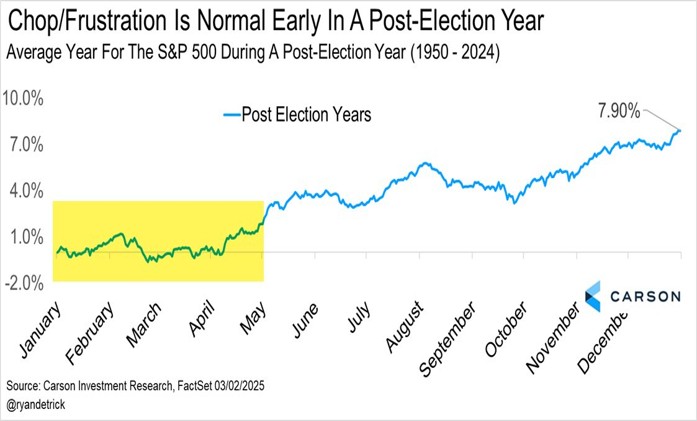

Short-term volatility is a natural feature of evolving markets, particularly in the first year of a new U.S. presidency. Historically, policy transitions introduce uncertainty in the first half of the year before stabilising as frameworks become clearer.

1. First-Year Presidential Cycle: Historically, the first year of a presidential term sees early volatility, followed by greater market clarity as policies take effect. We are seeing this pattern play out now.

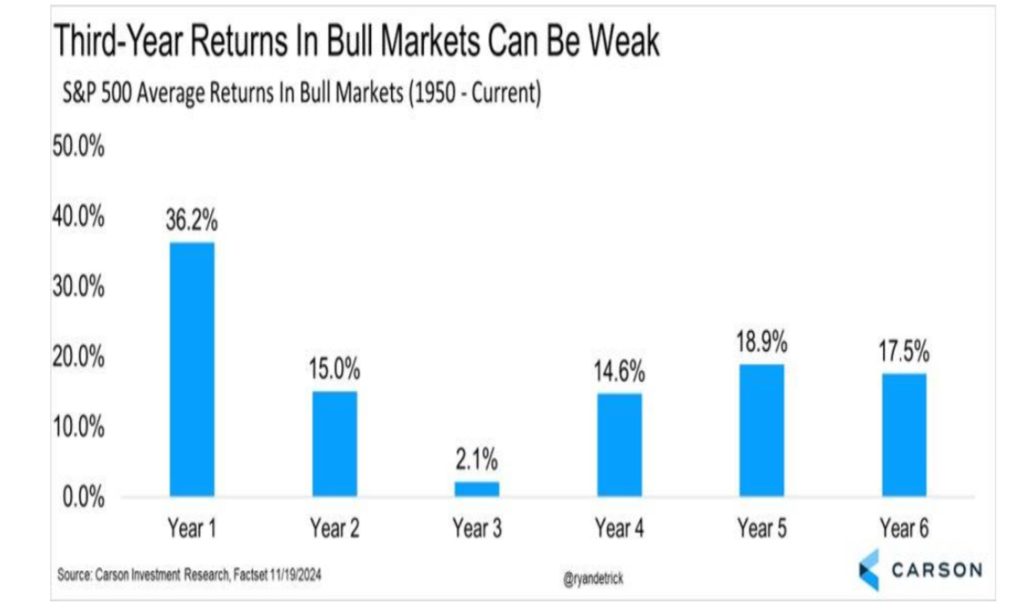

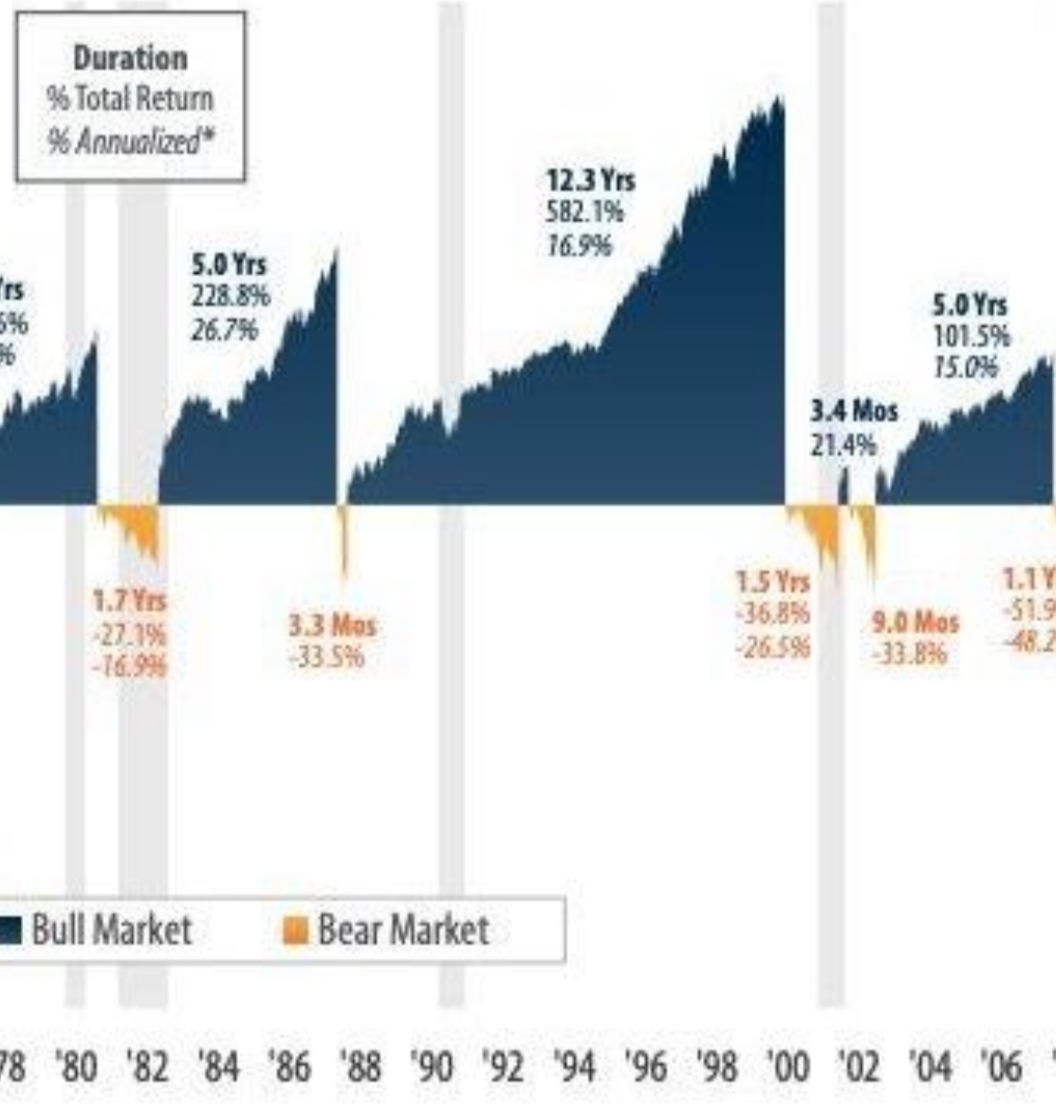

2. Bull Market Trends: We are currently in the third year of this bull market cycle. Historically, the third year tends to be a period of consolidation before the stronger performance typically seen in years 4-6 of an extended market cycle.

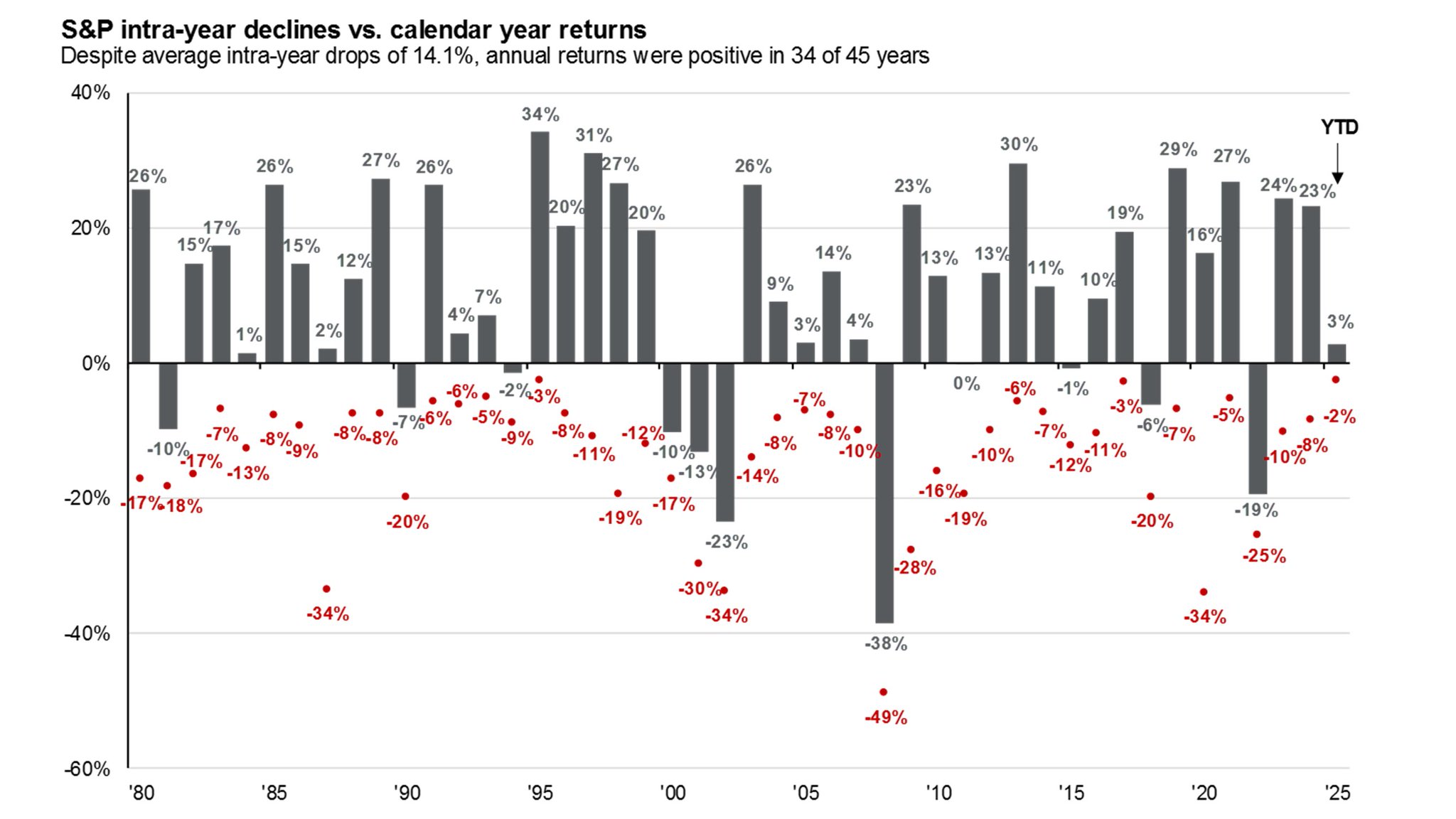

3. Intra-Year Corrections: Market cycles regularly include multiple intra-year pullbacks. These drawdowns, often averaging around -14%, have historically been part of broader growth cycles.

(Source: @Mike.Zuccardi)

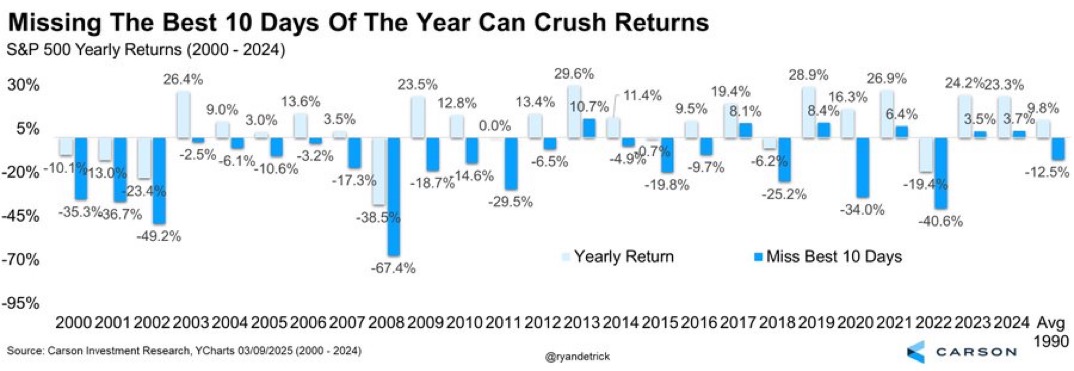

4. Long-Term Market Participation: Market history illustrates that sustained participation is key to capturing growth. Missing even a handful of the best-performing days each year has historically had a significant impact on long-term returns.

The TAMIM Takeaway: Looking Ahead with Confidence

Periods of recalibration often provide valuable insights into market direction and structural shifts. With a balanced economic strategy, a measured interest rate outlook, and long-term growth drivers in place, we see the current environment as part of a broader trend of innovation-led expansion.

As we move forward, the interplay between fiscal policies, technological advancements, and shifting economic frameworks is expected to create a dynamic environment for strategic positioning. This cycle closely resembles the early 1990s, which preceded a decade-long period of economic and market growth, offering strong potential for disciplined investors.

The world is shifting under our feet. Global markets are being reshaped by technological advancements, economic realignments, and geopolitical shifts that demand a new approach to investing.

As investors, it is no longer enough to simply track historical trends or rely on the same old blue-chip strategies, we must look forward. The key to success in 2025 and beyond is identifying long-term structural trends and positioning accordingly.

In my latest investment presentation, I outlined a global roadmap for navigating this new environment. The short version? The world is changing, and investors must adapt.

The Global Economic Pivot: A Market in Flux

I often say that “the world is being turned upside down,” and I mean it. This is not hyperbole, it’s a reflection of fundamental changes in how economies function, how industries operate, and where capital flows.

While equities remain the preferred asset class, the real challenge is knowing which ones to own. Investors need to go beyond the headlines and dig deeper into valuation, resilience, and sectoral positioning.

The U.S. Market: The Mega-Cap Illusion

Many investors remain captivated by a handful of mega-cap technology stocks in the United States. These companies dominant as they may be now trade at valuations that are, frankly, difficult to justify.

The top seven mega-caps in the U.S. market now account for an outsized share of market capitalisation, creating a distorted investment landscape.

These stocks trade at 30 times earnings, compared to just 16 times earnings for small and mid-cap companies.

I see much better value in smaller-cap stocks. The S&P 600 Index of smaller companies provides a more reasonable entry point, with businesses that have adapted to economic pressures and are better positioned for resilience.

Reindustrialisation: America’s Next Big Investment Theme

One of the biggest themes for the decade ahead is reindustrialisation, the process of bringing manufacturing and supply chains back to American shores.

This is not just political rhetoric; it is an economic reality.

Infrastructure investment is essential. The American Society of Civil Engineers has given U.S. infrastructure a failing grade – this must change

Manufacturing is being reshaped, and companies involved in industrial automation, logistics, and materials science stand to benefit

Supply chain resilience is now a corporate priority, creating new demand for domestic production capabilities.

This movement presents a once-in-a-generation investment opportunity, particularly in sectors that support domestic production and industrial transformation.

The AI and Energy Nexus: The Next Critical Shift

Much has been written about AI’s potential, but one overlooked consequence is its massive energy consumption.

Artificial intelligence models require enormous processing power, which in turn demands significantly more electricity.

Energy grids will need upgrading, and those who control energy infrastructure stand to gain.

Where are the opportunities?

Power generation companies that can meet surging electricity demand

Grid infrastructure providers upgrading systems for efficiency

Nuclear energy resurgence, as plants extend their lifespans to accommodate AI-driven power need

Renewable energy and traditional energy sources integrating to support a sustainable future

This isn’t speculation – it’s a necessity. Data centers, cloud computing, and AI workloads will drive the next wave of energy investment.

Japan: The Overlooked Gem in Global Markets

One of the most underappreciated investment stories today is Japan.

Japanese companies have historically underperformed due to poor corporate governance.

But now, things are changing companies are becoming more shareholder-friendly, boosting dividends and share buybacks.

At the same time, Japan is home to some of the world’s most technologically advanced companies.

For investors willing to look beyond the usual suspects, Japan presents a compelling valuation opportunity.

The China Factor: Mutual Dependency, Not Decoupling

While many analysts continue to discuss “decoupling” from China, the reality is far more complex.

China remains deeply entrenched in global supply chains.

The U.S. and China are economically interdependent, whether policymakers admit it or not.

Instead of a total separation, I expect a future of “mutually agreed dependency.” While political rhetoric may suggest otherwise, the economic reality means trade will continue just under different terms.

Europe: Defense and Infrastructure in Focus

Europe often flies under the radar, but investment opportunities exist, particularly in:

Defense spending, as nations reassess military budgets in response to geopolitical tensions.

Infrastructure investment, as European governments allocate funds to modernisation.

While growth in Europe remains sluggish, targeted investments in these sectors could yield strong returns.

Investment Playbook for 2025

Given this backdrop, where should investors focus?

Look beyond mega-cap tech stocks. The best opportunities are in smaller, more reasonably valued companies.

Reindustrialisation is real. Companies involved in infrastructure, manufacturing, and logistics will benefit.

Energy is undergoing a transformation. AI-driven demand will push investment into power grids and energy production.

Japan is an underappreciated market. Improving governance and attractive valuations make it worth considering.

China remains an economic force. The West may reduce reliance, but full decoupling is unrealistic.

The Tamim Takeaway

The investment landscape in 2025 is undergoing a profound transformation, and investors who fail to adapt will find themselves on the wrong side of history.

U.S. markets remain strong, but investors should seek value beyond the overvalued mega-caps.

AI’s rise will drive unprecedented energy demand, making power infrastructure a key investment theme.

Japan is one of the most attractive, yet ignored, opportunities in global markets.

China remains deeply interconnected with global markets, making a full economic break unlikely.

Europe’s defense and infrastructure investments will provide new openings for investors.

As we move through 2025, the best investors will be those who embrace change, seek value in underappreciated markets, and stay ahead of long-term structural shifts.

At TAMIM, we remain committed to spotting these emerging trends early and investing with conviction.

The world is changing – make sure your portfolio is changing with it.