In a market environment where capital is scarce and investors are hunting for profitable, cash-generative growth stories, EROAD Limited (ASX/NZX: ERD) has emerged from the shadows. The company’s FY25 results mark a turning point, not just for its financials, but for its narrative. After a challenging few years marked by legacy tech upgrades and tight macro headwinds, EROAD is finally demonstrating the operational leverage and strategic clarity needed to attract serious investor attention.

This is not a speculative bet on hype or disruption. EROAD offers a more grounded story, one of discipline, execution, and re-rating potential.

Why EROAD, Why Now?

EROAD is a fleet management and telematics technology company operating in New Zealand, Australia, and North America. Its software and hardware solutions help large vehicle fleets optimise operations, manage compliance, and enhance safety. In short, it is digitising transport logistics, one of the more stubbornly analogue parts of the economy.

What makes it interesting now? Put simply: it’s finally firing on all cylinders.

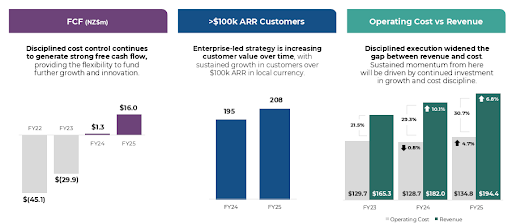

Revenue up 6.8% to $194.4m

Annualised Recurring Revenue (ARR) up 6.1% to $175.1m

Normalised Free Cash Flow surged to $23.6m (vs $1.3m last year)

Positive NPAT of $1.4m (vs -$0.8m)

EBIT jumped to $5.9m (normalised to $9.9m)

Source: EROAD FY25 Results

From top-line growth to bottom-line profitability, the company has turned a corner. And unlike many tech names, it’s doing so with a clear focus on capital discipline.

Cash Is King Again

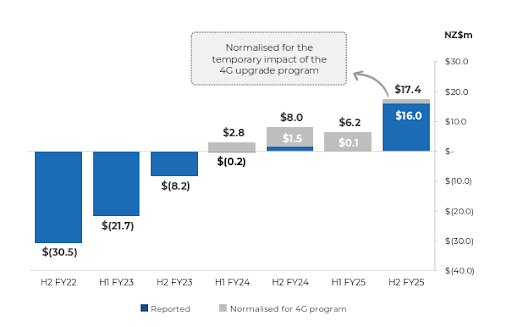

Perhaps the most important takeaway from the FY25 result is this: EROAD is now generating real, repeatable free cash flow. Gross FCF improved tenfold year-on-year, and once adjusted for the 4G/5G hardware upgrade cycle (known internally as Project Sunrise), the business is delivering an 8-10% FCF yield.

Source: EROAD FY25 Results

This puts the EROAD in rare company for a small-cap technology stock: profitable, growing, and cash-generative.

Moreover, capital expenditure, once a source of concern, is no longer a drag. FY25 capex fell to $13.4m (from $32.2m), with a sustainable range of $14 to 18m flagged going forward. This drop is attributed to more efficient hardware, better billing cycles, and a growing mix of software-based upsells.

In a post-ZIRP world where investors care deeply about capital allocation, EROAD is finally speaking the right language.

Strategy and Execution in Sync

Beyond the numbers, it’s clear that management has found its rhythm.

High asset retention across all regions: 92.5% group-wide.

Enterprise segment now 54% of ARR with a 7% YoY increase in enterprise customers.

ARR tailwinds include: a $1.1m cross-regional expansion from a major NZ client into Australia, $7.2m in NZ upsells, and $4.9m in new US enterprise deals.

This speaks to a very sticky product, once a large fleet adopts EROAD, they tend to stick around and expand.

The dual-CEO structure (with Mark Heine and David Kenneson sharing the reins) seems to be working well, with regional focus delivering operational granularity while aligning to a common strategy. Their investor communication is confident, transparent, and focused on long-term outcomes, not quarterly theatrics.

Source: EROAD FY25 Results

North America: The Next Frontier

While New Zealand remains EROAD’s heartland and Australia continues to scale, North America is where the asymmetric upside lies. The US is the world’s largest market for commercial vehicles, and the adoption curve for telematics is still maturing.

The company’s commentary around deal pipeline strength in the US suggests that more contract wins could act as a catalyst in FY26. With more enterprise clients shifting to bundled software and compliance offerings, EROAD’s value proposition is rising.

Importantly, the Constellation Software overhang has now been removed. Their 10% holding (once tied to a $1.30 takeover bid in 2023) has exited the register. This clears the deck for a potential re-rating as ERD proves itself as a standalone, self-sustaining business.

Looking Ahead: FY26 and Beyond

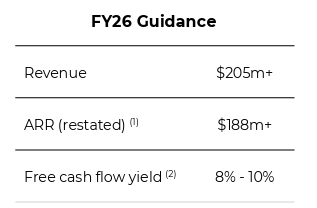

Management has provided FY26 guidance that’s both credible and compelling:

Revenue of at least $205m

ARR of $188m+ (7.5% YoY growth)

Normalised FCF yield of 8–10%

Medium-term ARR CAGR of 11–13%

Source: EROAD FY25 Results

Project Sunrise is scheduled for completion by December 2025, which will mark the final capex outlay tied to legacy tech. Post-2025, the business becomes even more software-centric, margin-accretive, and scalable.

Add to this the upcoming Investor Day, which is expected to include roadmap visibility and long-term product strategy, and the setup for FY26 looks well-calibrated.

Market Mispricing?

Despite all this progress, EROAD still flies under the radar. The stock trades well below historical highs, and the institutional register remains relatively thin. As more investors re-focus on profitable growth in underappreciated small caps, EROAD could be a beneficiary of a valuation catch-up.

The company fits Tamim’s Australia All Cap company checklist:

High insider ownership

Growing free cash flow

Low investor expectations (relative to execution strength)

Exposure to mission-critical B2B infrastructure (not hype-driven consumer tech)

And with macro drivers like supply chain digitisation, fuel cost optimisation, and ESG compliance gaining momentum, the tailwinds are tangible.

TAMIM Takeaway: Backing Execution in a Re-Rating Opportunity

EROAD’s FY25 result is more than just a strong set of numbers, it’s a signal that the business has entered a new phase. With strong free cash flow, a sticky enterprise customer base, a leaner capex profile, and growing international traction, this is a company no longer in ‘hope’ mode.

It’s executing.

The departure of Constellation Software removes a structural overhang, while new product enhancements and market expansion provide optionality.

For investors who value cash flow, recurring revenue, and credible growth in real-world infrastructure software, EROAD is one to watch.

We continue to believe that the best opportunities lie where operational execution meets investor neglect. EROAD might just be one of them.

Disclaimer: EROAD Limited (ASX/NZX: ERD) is held in TAMIM Portfolios as at date of article publication. Holdings can change substantially at any given time.

When the Australian Treasurer takes to the National Press Club with a prepared script and a confident tone, investors would be wise to listen. Especially when that Treasurer is Jim Chalmers, a policymaker who, love him or not, has proven to be more than a caretaker of Treasury. He’s actively reshaping the role of government in Australia’s economic future.

After delivering two consecutive budget surpluses and navigating the country through a tricky period of post-COVID inflation and geopolitical flux, Chalmers now has the political capital, economic momentum, and likely tenure (another three years) to implement what he calls “capitalism with a public purpose.” That’s not just soundbite rhetoric. It’s a signal. And for investors, it’s a roadmap.

So what does this mean for Australian investors in property, equities, and credit over the next cycle?

Let’s unpack the key themes and how to think about positioning capital in this evolving landscape.

Property: The Era of Policy-Driven Undersupply

From Crisis to Controlled Crisis?

Chalmers’ address highlighted an uncomfortable reality: despite the rate hike cycle (which is now over), housing remains unaffordable, and the solution is not more demand-side stimulus but structurally increased supply. The budget’s $6.2 billion National Housing Accord and extended Commonwealth Rent Assistance are commendable, but they won’t fix housing overnight.

Meanwhile, migration remains high, planning remains sluggish, and developers are still facing tight lending conditions and high construction costs. The result? Undersupply in key markets like Sydney, Melbourne, and Brisbane will persist, pushing rents higher and squeezing yields upward.

Investment Insight

For investors, the playbook is not to speculate on rapid capital growth. It’s about yield, scarcity, and regeneration. High-quality residential REITs, build-to-rent infrastructure, and suburban land banking in growth corridors are increasingly attractive. Look to companies involved in modular construction and property tech, particularly those that help scale housing efficiently.

Commercial real estate, especially office, still faces headwinds but to us that remains the stand out opportunity. Industrial and logistics property remains a secular winner (but still expensive), particularly in the context of “A Future Made in Australia” reshoring.

Equities: Government as Catalyst, Not Competitor

Strategic Sectors Are the New Growth Stocks

One of the clearest signals from Chalmers is that the government will not stand on the sidelines. Whether it’s clean energy, critical minerals, defence tech, or advanced manufacturing, Canberra is stepping in, not to nationalise, but to catalyse.

The “Future Made in Australia” Act is designed to de-risk private investment in national-interest sectors. For equity investors, this is a green light: companies aligned with national policy will likely benefit from favourable capital treatment, faster approvals, and co-investment opportunities.

Think:

Critical minerals: ASX-listed producers with downstream ambitions.

Renewables infrastructure: Particularly firms with grid, battery, or hydrogen exposure.

Advanced industrials and defence contractors: Particularly those aligned with reshoring, digital sovereignty, or regional security.

Investment Insight

In this environment, equity selection becomes as much about macro understanding as micro valuation. Companies that can tell the right “nation-building” story to policymakers and capital markets alike will trade at a premium.

The key here is to filter between companies that are policy-aligned but also commercially viable. Don’t chase hype, follow balance sheet strength, cash flow quality, and institutional backing.

Credit: Stronger for Longer, but Differently Positioned

From Rate Risk to Credit Risk

With inflation moving back within the RBA’s target band and two budget surpluses under Labor, we are now entering a new phase for the bond and credit markets. Yields will stay structurally higher than the zero-rate era—but the acute rate volatility is likely behind us.

In this setting, credit becomes increasingly attractive. While Labor and Chalmers are not known for fiscal prudence, budget surpluses and sector-targeted investment has helped contain bond market concerns about sovereign risk. At the same time, banks are being more selective, creating gaps for non-bank and private credit to flourish.

Investment Insight

Investors should look beyond term deposits and into credit investments that target infrastructure, housing, or business lending with tight covenants and strong origination networks. The risk is real, but so is the reward, particularly as spreads remain wide relative to historic norms.

Australian investors who previously shunned credit due to perceived risk should revisit the asset class. In a world of modest growth and steady rates, credit earns its place in multi-asset portfolios again.

Chalmers’ Strategic Capitalism: What It Means for Investors

Jim Chalmers made it clear: the next three years of economic policy will be activist, not reactive. This is not deregulated, hands-off capitalism. It’s targeted, coordinated, and deliberately aligned with structural megatrends, from energy transition to industrial reshoring.

But here’s the rub: investors who understand the direction of travel (and front-run it) will do well. Those who resist, or cling to the playbooks of the past, may be left behind.

TAMIM Takeaway: A Policy-Driven Cycle Demands a Policy-Aware Portfolio

In an age of “capitalism with a public purpose,” you can’t afford to ignore what Treasury is doing especially when Treasury is flush with cash, has political stability, and a mandate to drive national transformation.

At TAMIM, we believe the right positioning now is clear:

Invest in property segments aligned with long-term demographic and policy tailwinds.

Seek equities with exposure to public-private megaprojects and strategic national interest.

Diversify into credit alongside your equity and property investments as the income-generating workhorse in your portfolio for the next cycle.

With Chalmers at the helm, the map is clear, even if the terrain remains unpredictable.

This week’s TAMIM Reading List explores the curious logic of modern life—where $900 ideas become billion-dollar brands, YouTubers outshine media empires, and the military turns to microwave weapons to fight future wars. We unpack the investor behaviour gap, explore Switzerland’s deep-rooted obsession with bunkers, and consider whether your morning coffee is doing more for your health than you think. Stunning images of the Milky Way offer a final reminder that, amid the noise, there’s still space for perspective. A collection of sharp, surprising reads that reveal the habits, risks, and obsessions shaping our world.

Introduction: Investing at the Intersection of Intelligence and Infrastructure

At TAMIM, we spend a lot of time thinking about where the world is headed and how capital should follow. When a CEO like Sundar Pichai speaks, we listen. Not for the headlines, but for the signals buried beneath the surface. In a wide-ranging interview with Lex Fridman, Sundar, the CEO of Google and Alphabet, offered a glimpse into the tectonic shifts underway in artificial intelligence (AI), digital infrastructure, and the way we interact with information.

In our view, the key takeaways are not just relevant to Silicon Valley engineers, they’re essential for long-term investors. Especially those looking to position themselves for a decade where data is the new oil and infrastructure is no longer just roads and rail but chips, code, and computational horsepower.

This article unpacks the major themes from Sundar’s conversation and frames them through a Tamim lens: What does this mean for investors? Where are the durable cash flows and competitive advantages being built? And how do we separate noise from signal in a hype-driven market?

AI Is Foundational, But Needs Infrastructure to Scale

Sundar Pichai makes a clear comparison between AI and other transformative technologies like electricity or fire. These aren’t just enhancements to productivity; they’re general-purpose technologies that reshape every industry they touch. But here’s the catch: AI cannot scale in isolation. It needs infrastructure, and lots of it.

From data centres and optical fibre networks to cloud platforms and custom semiconductors like Google’s TPU, the investment required to power generative AI is enormous. This aligns directly with what we’ve been arguing: global listed infrastructure is no longer just a defensive play; it’s a lever for digital and economic transformation.

Investors should pay attention to the businesses enabling AI behind the scenes: data centre REITs, utility-scale power providers, semiconductor foundries, and specialist contractors laying the physical and digital pipes.

Regulation Is Coming and That’s a Feature, Not a Bug

One of Sundar’s strongest points was the need for global AI regulation. He draws comparisons with nuclear energy and aviation safety. The lesson? AI is too powerful to be left unchecked.

This regulatory shift is already taking shape, from the EU’s AI Act to U.S. executive orders. For investors, this may feel like a threat to innovation. But at Tamim, we see it differently: regulation adds clarity, and clarity reduces risk. Companies that build AI responsibly, with robust governance and transparency, will attract capital and clients. Those that don’t, won’t.

This reinforces our emphasis on governance (the G in our Global equity ASG process) and our preference for companies that aren’t just fast but resilient, regulated, and trusted by governments and institutions.

Search, Advertising, and the Repricing of Intangibles

AI is transforming how we access information. Google’s Search Generative Experience (SGE) blends AI summaries with traditional links. It’s more helpful to users, but potentially disruptive to Google’s ad-driven business model.

This highlights a broader investment theme: the repricing of intangible assets. As AI reconfigures value chains, companies must adapt how they monetise attention, trust, and data. Investors should prepare for margin compression in legacy models, but also seek exposure to firms inventing new economic moats.

We see opportunity in platform businesses that control scarce digital real estate from cybersecurity APIs to cloud-native developer tools. The infrastructure of the digital world is being repriced.

Multi-Modality and the Era of Intelligent Systems

Pichai speaks at length about Gemini (Google’s generative AI suite), which integrates images, text, code, audio, and video. This reflects the next phase of AI: systems that are not just smart in a narrow domain but fluent across modes.

For investors, this underscores the increasing need for compute power, bandwidth, and intelligent orchestration. It also speaks to the rise of converged infrastructure, where cloud, edge, and on-prem systems are optimised in real time.

This is not science fiction. It’s already reshaping supply chains, industrial automation, and enterprise IT. We believe infrastructure businesses that understand AI workloads and deliver low-latency, high-availability environments will be the next secular winners.

Talent, Trust, and Technological Diplomacy

Sundar’s personal story is also telling. From his upbringing in Chennai to the helm of Alphabet, he reflects a global mindset that views technology as a force for upward mobility. Importantly, he emphasises that AI progress will require trust, cross-border cooperation, and a global pool of talent.

This is critical. Just as the energy transition has highlighted the geopolitical dimensions of rare earths and battery minerals, the AI revolution is reshaping talent pipelines and alliances. Countries and companies that attract and retain world-class technical talent will dominate.

For investors, this argues for backing global champions with decentralised R&D, strong academic partnerships, and reputations for openness and integrity. These are not intangible values. They are competitive advantages in the new AI-industrial economy.

What This Means for the TAMIM Process

At Tamim, we approach the market with a multi-dimensional process. Our Global equity PAR model (Premium, Action, Resilience) screens for valuation, catalysts, and quality. But it’s our ASG overlay, assessing Accounting, Strategy, and Governance, that tests for durability.

Sundar Pichai’s insights reinforce our conviction in this process. In a world where the pace of change is accelerating, resilience matters more than ever. Companies with fortress balance sheets, clear strategic vision, and ethical capital allocation will thrive. Those relying on hype, leverage, or opacity will falter.

That’s why the Global High Conviction (GHC) portfolio contains infrastructure names like Quanta Services, Engie, and A2A. These companies are not only beneficiaries of capital flows into grid modernisation and mixed-source energy but are also building the backbone for AI-powered economies.

TAMIM Takeaway: The Intelligence Infrastructure Decade

As AI moves from lab demos to production deployment, the infrastructure underpinning it becomes the strategic asset of the 21st century. Sundar Pichai’s vision of integrated, multi-modal, safe AI systems is only possible with enormous investment in computation, connectivity, and capability.

For investors, the next decade is not just about betting on model-makers. It’s about backing the builders, the companies laying the foundations for AI to thrive safely and scalably.

And that’s why next week, Tamim will be officially launching the Global Listed Infrastructure Fund. Managed by Robert Swift and Charles Wannan, the fund will give investors access to the real assets powering the intelligence revolution.

As the world rushes headlong into the age of artificial intelligence, electrification, and digital dependency, much of the investor focus remains fixed on the front-end winners: AI models, chip designers, and consumer-facing tech. But behind every leap in productivity and every transition to cleaner, smarter systems lies a quieter revolution, the global rebuild of our physical and digital infrastructure.

At TAMIM, we believe this shift presents an extraordinary long-term opportunity. While the headlines celebrate ChatGPT or the latest Nvidia chip, it is companies like Sterling Infrastructure, Arrow Electronics, and Kajima Corporation that are laying the foundations of the intelligent economy. These businesses may not shout for attention, but they are quietly enabling the 21st century.

Intelligence Infrastructure: The New Growth Engine

It’s tempting to think of AI as a purely software phenomenon. But as Jensen Huang, the CEO of Nvidia, has noted, AI is a full-stack transformation. Data centres, networks, electric grids, semiconductors, and logistics chains, they’re all part of the ecosystem.

This is where Sterling Infrastructure, Arrow Electronics, and Kajima excel. They represent the brains, brawn, and bandwidth required to operationalise the AI revolution:

Sterling is constructing the physical pads for hyperscale data centres and next-gen manufacturing facilities.

Arrow designs and delivers the complex electronics, components, and computing infrastructure to power edge and cloud environments.

Kajima builds and maintains the physical environments, hospitals, campuses, earthquake-resistant infrastructure, in which these technologies live.

In short, these companies make AI and the digital economy possible in the real world.

Sterling Infrastructure: The Smart Shovel in America’s Rebuild

Sterling Infrastructure (NASDAQ: STRL) is a US-based engineering and construction group with its boots firmly planted in America’s re-industrialisation and digital infrastructure renaissance. Operating across E-infrastructure, transportation, and building solutions, Sterling is benefitting directly from three unstoppable forces: federal infrastructure stimulus, a manufacturing revival, and the exponential growth in data centre demand.

Its E-Infrastructure segment, which focuses on site development for AI-enabled data centres, warehouses, and manufacturing, has seen explosive growth. With shares up over 85% in the last three months, this isn’t just a cyclical bounce, it’s structural.

Meanwhile, Sterling’s transportation unit addresses the crumbling US infrastructure highlighted in the American Society of Civil Engineers’ 2025 report card, reinforcing the tailwinds behind highways, bridges, and ports. Its building solutions division focuses on the high-growth Sun Belt regions, targeting residential concrete and plumbing in booming states like Texas.

Are there risks? Certainly. The company is reliant on a handful of clients, particularly in its AI-focused pipeline and Department of Transportation contracts. But with strong revenue visibility and a scalable model, Sterling represents a quintessential Tamim holding: real growth, strong fundamentals, and misunderstood potential.

Arrow Electronics: The Invisible Hand of Industrial Technology

Arrow Electronics (NYSE: ARW) is the unsung architect behind much of the world’s industrial and commercial electronics. With a global footprint and a client base that includes the biggest names in computing, telecommunications, automotive, and industrial automation, Arrow is the ultimate picks-and-shovels provider to the digital economy.

Its edge? Arrow doesn’t just supply components, it delivers integrated solutions, from supply chain design to data analytics, hardware, and systems integration. For companies facing tariff uncertainty or volatile global supply chains, Arrow offers a lifeline: reliable delivery, visibility, and antifragility.

In today’s era of fragmented geopolitics and volatile logistics, this makes Arrow a vital strategic partner to global enterprises. It is no surprise, then, that revenue revisions have been trending positively. Investors are beginning to realise that Arrow is not just a distributor, but a system-level enabler of digital transformation.

While not flashy, its stability and relevance in a changing world give it a valuable role in a diversified global portfolio. Think of Arrow as the backbone of modern electronics, invisible to most consumers, but indispensable to every manufacturer.

Kajima Corporation: Building for a Resilient Future

Kajima Corporation (TSE: 1812), one of Japan’s oldest and most respected construction and civil engineering firms, is more than just a traditional builder. It is an operator, innovator, and problem solver with global reach. From coastal defences and earthquake-proof buildings to green energy systems and data centres, Kajima operates at the nexus of sustainability, resilience, and renewal.

Its position in the Tamim Global High Conviction portfolio reflects a dual thesis: first, that Japan is on the verge of a structural inflationary shift; and second, that global demand for resilient infrastructure will continue to rise.

Kajima’s presence in Asia, the Pacific, and the US allows it to benefit from multiple stimulus programs and private sector CapEx booms. Its diversified business model includes real estate, environmental services, and specialised construction for logistics, hotels, and public health infrastructure.

In a world increasingly shaped by climate volatility, supply chain fragmentation, and energy transformation, Kajima offers strategic exposure to the kinds of projects that are not optional, but essential.

A Hedge Against Volatility, a Bet on Productivity

Investors face a paradox: extreme technological acceleration on one side, and extreme geopolitical and economic volatility on the other. The result? An investment environment where conviction is difficult and panic is easy.

The businesses profiled here are not reactive trades, they are proactive allocations to long-term themes:

Productivity gains from digital transformation and automation

Resilient, smart infrastructure that bridges the physical and digital worlds

A rebalanced energy policy that complements renewables with reliable baseload power and grid resilience

In short, this is where macro meets micro: structural tailwinds manifesting in tangible earnings.

The Capital Expenditure Supercycle Is Here

After decades of underinvestment in infrastructure, the world is waking up to the urgent need for renewal and expansion. The CapEx supercycle is not just about potholes and power plants. It’s about preparing for a digitised, decentralised, and decarbonised economy.

Sterling Infrastructure is building the roads, bridges, and pads that undergird AI data centres and solar farms.

Arrow Electronics provides the brains and logistics to keep industry running, no matter the macro conditions.

Kajima Corporation is modernising cities and regions to withstand floods, earthquakes, and demographic shifts.

Together, they form a quiet but critical axis of long-duration infrastructure investing.

TAMIM Takeaway: Investing in What the Future Requires

At TAMIM, we aim to be ahead of the narrative and inside the theme. Sterling, Arrow, and Kajima may not command attention like Nvidia or Tesla, but they enable the world those companies are building.

Our process, grounded in data, refined by fundamental due diligence, and structured through disciplined risk management, has led us to invest in these three names. They are the embodiment of our investment philosophy: own what matters before the crowd realises it does.

And this is just the beginning.

Next week, we’ll be unveiling our new TAMIM Global Infrastructure Fund, built to take advantage of these secular trends and allow our investors to participate in the roll-out of the intelligent economy. Sign up for the webinar here.

Disclaimer: Sterling Infrastructure (NASDAQ: STRL), Arrow Electronics (NYSE: ARW) and Kajima Corporation (TSE: 1812) are held in TAMIM Portfolios as at date of article publication. Holdings can change substantially at any given time.

Source: EROAD FY25 Results

Source: EROAD FY25 Results

Sterling Infrastructure (NASDAQ: STRL) is a US-based engineering and construction group with its boots firmly planted in America’s re-industrialisation and digital infrastructure renaissance. Operating across E-infrastructure, transportation, and building solutions, Sterling is benefitting directly from three unstoppable forces: federal infrastructure stimulus, a manufacturing revival, and the exponential growth in data centre demand.

Sterling Infrastructure (NASDAQ: STRL) is a US-based engineering and construction group with its boots firmly planted in America’s re-industrialisation and digital infrastructure renaissance. Operating across E-infrastructure, transportation, and building solutions, Sterling is benefitting directly from three unstoppable forces: federal infrastructure stimulus, a manufacturing revival, and the exponential growth in data centre demand. Kajima Corporation (TSE: 1812), one of Japan’s oldest and most respected construction and civil engineering firms, is more than just a traditional builder. It is an operator, innovator, and problem solver with global reach. From coastal defences and earthquake-proof buildings to green energy systems and data centres, Kajima operates at the nexus of sustainability, resilience, and renewal.

Kajima Corporation (TSE: 1812), one of Japan’s oldest and most respected construction and civil engineering firms, is more than just a traditional builder. It is an operator, innovator, and problem solver with global reach. From coastal defences and earthquake-proof buildings to green energy systems and data centres, Kajima operates at the nexus of sustainability, resilience, and renewal.