In a market environment where capital is scarce and investors are hunting for profitable, cash-generative growth stories, EROAD Limited (ASX/NZX: ERD) has emerged from the shadows. The company’s FY25 results mark a turning point, not just for its financials, but for its narrative. After a challenging few years marked by legacy tech upgrades and tight macro headwinds, EROAD is finally demonstrating the operational leverage and strategic clarity needed to attract serious investor attention.

This is not a speculative bet on hype or disruption. EROAD offers a more grounded story, one of discipline, execution, and re-rating potential.

Why EROAD, Why Now?

EROAD is a fleet management and telematics technology company operating in New Zealand, Australia, and North America. Its software and hardware solutions help large vehicle fleets optimise operations, manage compliance, and enhance safety. In short, it is digitising transport logistics, one of the more stubbornly analogue parts of the economy.

What makes it interesting now? Put simply: it’s finally firing on all cylinders.

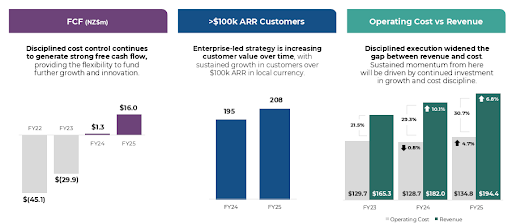

- Revenue up 6.8% to $194.4m

- Annualised Recurring Revenue (ARR) up 6.1% to $175.1m

- Normalised Free Cash Flow surged to $23.6m (vs $1.3m last year)

- Positive NPAT of $1.4m (vs -$0.8m)

- EBIT jumped to $5.9m (normalised to $9.9m)

Source: EROAD FY25 Results

From top-line growth to bottom-line profitability, the company has turned a corner. And unlike many tech names, it’s doing so with a clear focus on capital discipline.

Cash Is King Again

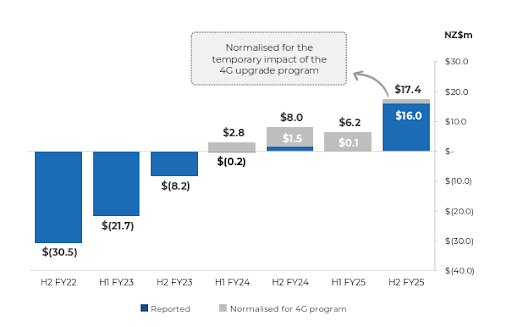

Perhaps the most important takeaway from the FY25 result is this: EROAD is now generating real, repeatable free cash flow. Gross FCF improved tenfold year-on-year, and once adjusted for the 4G/5G hardware upgrade cycle (known internally as Project Sunrise), the business is delivering an 8-10% FCF yield.

Source: EROAD FY25 Results

This puts the EROAD in rare company for a small-cap technology stock: profitable, growing, and cash-generative.

Moreover, capital expenditure, once a source of concern, is no longer a drag. FY25 capex fell to $13.4m (from $32.2m), with a sustainable range of $14 to 18m flagged going forward. This drop is attributed to more efficient hardware, better billing cycles, and a growing mix of software-based upsells.

In a post-ZIRP world where investors care deeply about capital allocation, EROAD is finally speaking the right language.

Strategy and Execution in Sync

Beyond the numbers, it’s clear that management has found its rhythm.

- High asset retention across all regions: 92.5% group-wide.

- Enterprise segment now 54% of ARR with a 7% YoY increase in enterprise customers.

- ARR tailwinds include: a $1.1m cross-regional expansion from a major NZ client into Australia, $7.2m in NZ upsells, and $4.9m in new US enterprise deals.

This speaks to a very sticky product, once a large fleet adopts EROAD, they tend to stick around and expand.

The dual-CEO structure (with Mark Heine and David Kenneson sharing the reins) seems to be working well, with regional focus delivering operational granularity while aligning to a common strategy. Their investor communication is confident, transparent, and focused on long-term outcomes, not quarterly theatrics.

Source: EROAD FY25 Results

North America: The Next Frontier

While New Zealand remains EROAD’s heartland and Australia continues to scale, North America is where the asymmetric upside lies. The US is the world’s largest market for commercial vehicles, and the adoption curve for telematics is still maturing.

The company’s commentary around deal pipeline strength in the US suggests that more contract wins could act as a catalyst in FY26. With more enterprise clients shifting to bundled software and compliance offerings, EROAD’s value proposition is rising.

Importantly, the Constellation Software overhang has now been removed. Their 10% holding (once tied to a $1.30 takeover bid in 2023) has exited the register. This clears the deck for a potential re-rating as ERD proves itself as a standalone, self-sustaining business.

Looking Ahead: FY26 and Beyond

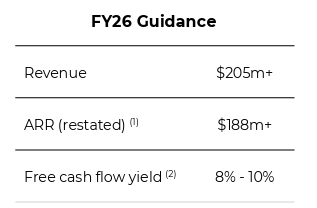

Management has provided FY26 guidance that’s both credible and compelling:

- Revenue of at least $205m

- ARR of $188m+ (7.5% YoY growth)

- Normalised FCF yield of 8–10%

- Medium-term ARR CAGR of 11–13%

Source: EROAD FY25 Results

Source: EROAD FY25 Results

Project Sunrise is scheduled for completion by December 2025, which will mark the final capex outlay tied to legacy tech. Post-2025, the business becomes even more software-centric, margin-accretive, and scalable.

Add to this the upcoming Investor Day, which is expected to include roadmap visibility and long-term product strategy, and the setup for FY26 looks well-calibrated.

Market Mispricing?

Despite all this progress, EROAD still flies under the radar. The stock trades well below historical highs, and the institutional register remains relatively thin. As more investors re-focus on profitable growth in underappreciated small caps, EROAD could be a beneficiary of a valuation catch-up.

The company fits Tamim’s Australia All Cap company checklist:

- High insider ownership

- Growing free cash flow

- Low investor expectations (relative to execution strength)

- Exposure to mission-critical B2B infrastructure (not hype-driven consumer tech)

And with macro drivers like supply chain digitisation, fuel cost optimisation, and ESG compliance gaining momentum, the tailwinds are tangible.

TAMIM Takeaway: Backing Execution in a Re-Rating Opportunity

EROAD’s FY25 result is more than just a strong set of numbers, it’s a signal that the business has entered a new phase. With strong free cash flow, a sticky enterprise customer base, a leaner capex profile, and growing international traction, this is a company no longer in ‘hope’ mode.

It’s executing.

The departure of Constellation Software removes a structural overhang, while new product enhancements and market expansion provide optionality.

For investors who value cash flow, recurring revenue, and credible growth in real-world infrastructure software, EROAD is one to watch.

We continue to believe that the best opportunities lie where operational execution meets investor neglect. EROAD might just be one of them.

______________________________________________________________________________________________

Disclaimer: EROAD Limited (ASX/NZX: ERD) is held in TAMIM Portfolios as at date of article publication. Holdings can change substantially at any given time.