In investing, there are few enduring truths, but one towers above the rest: nobody knows the future. Whether facing the 2008 Global Financial Crisis, the COVID-19 pandemic, or today’s geopolitical upheavals and trade tensions, history repeatedly demonstrates that certainty is an illusion.

Drawing on insights from Howard Marks’ latest memo, “Nobody Knows (Yet Again),” we explore why embracing uncertainty, rather than fearing it, remains the most rational investment strategy. Investors searching for timeless lessons in navigating volatility, uncertainty, complexity, and ambiguity will find powerful guidance here.

The Nature of Uncertainty: Lessons from 2008 and 2020

In 2008, as financial institutions collapsed like dominoes, panic engulfed markets. Yet, even in the eye of the storm, Marks argued that predicting a full financial collapse was beyond anyone’s capabilities. He advised investors to move forward not with confidence, but with reasoned logic: most of the time, the world does not end.

Similarly, in 2020 during the COVID-19 pandemic, expert opinions were replaced by speculation. Without historical analogues or reliable data, investors had to make decisions based purely on imperfect information.

Key lesson: In moments of upheaval, acting without full certainty, while uncomfortable, is often necessary to achieve superior long-term returns.

Acting in the Face of Uncertainty: The Courage to Invest

One of Marks’ most profound insights is the recognition that “the refusal to act is itself a decision.” Investors cannot sit on the side-lines waiting for uncertainty to resolve. By the time clarity emerges, opportunities will have disappeared.

Buying into fear, when others are paralysed by it, historically offers outsized rewards. As Walter Deemer aptly titled his book, “When the Time Comes to Buy, You Won’t Want To.” Fear is often greatest precisely when prices offer the most attractive future returns.

Thus, embracing calculated risk-taking in uncertain times is not reckless; it is essential.

For more on how disciplined buying during periods of market fear can set the foundation for long-term success, see Investment Wisdom: Buying Well.

The Futility of Forecasting: Why Expert Predictions Often Fail

Marks emphasises that even seasoned economists, business leaders, and policymakers operate in an environment of complexity too vast for reliable forecasting. Models built on historical data fail when unprecedented events occur.

“Analysing the future” is, he argues, an oxymoron. The future is unwritten, shaped by millions of unpredictable human decisions. Those who demand certainty before acting are likely to be left behind.

Investor takeaway: humility and flexibility should replace false confidence.

Second-Order Effects: The Complicated Consequences of Policy Actions

Another major theme from “Nobody Knows (Yet Again)” is the importance of considering second and third-order consequences, especially around tariffs and trade wars.

While tariffs might aim to reshore manufacturing and reduce trade deficits, the unintended consequences are numerous:

Higher prices and rising inflation

Declining consumer purchasing power

Supply shortages and economic dislocation

Retaliation from trading partners

These ripple effects can cause far more harm than policymakers anticipate. Investors must consider not just the direct impacts of political or economic actions, but their cascading effects across industries and societies.

The Fragility of Globalisation: Risks to Peace and Prosperity

Globalisation has been a major driver of global peace and prosperity since World War II, raising living standards around the world. Marks cautions that protectionist policies could unravel decades of economic progress, weaken global alliances, and create new systemic risks.

If international trade and cooperation decline, investors should anticipate higher costs, lower growth, and greater geopolitical instability—a complex backdrop requiring selective, risk-aware investing.

Investing in uncertain times demands more than forecasting skills; it demands courage, humility, and discipline.

The greatest opportunities often arise when fear dominates markets. However, they require investors to move forward with rational analysis, not certainty. As Howard Marks reminds us, it is in the moments when “nobody knows” that the seeds of future outperformance are sown.

For Tamim investors, the focus remains on identifying resilient businesses, maintaining valuation discipline, and leaning into opportunities when risk premia are elevated.

Nobody knows what tomorrow holds but history has shown those who act thoughtfully during uncertainty are those who ultimately prevail.

Powering the Global Shift to Renewables with Energy One

In Part 2 of our Small Cap Energy Transition Playbook, we continue identifying ASX-listed companies providing the critical infrastructure and technologies supporting the move to a net-zero economy. Following our focus on electrification and infrastructure in Part 1, we now turn to the brainpower behind energy trading: advanced software solutions.

One standout in this space is Energy One (ASX: EOL). This small-cap company is not only revolutionising energy trading but also positioning itself as a foundational pillar of the global renewable energy transition. With a unique integrated platform, significant European expansion, and a strong financial and operational track record, Energy One offers investors a compelling entry point into the evolution of energy markets.

Company Overview: Enabling the Future of Energy Trading

Founded 17 years ago, Energy One has evolved from a niche Australian software provider to a global leader in energy trading and risk management platforms. The company, led by CEO Shaun Ankers, has navigated the extreme volatility caused by global disruptions, notably the Russian invasion of Ukraine, and emerged stronger, solidifying its role as a mission-critical partner for energy market participants.

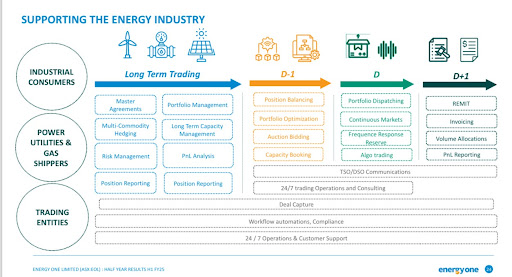

Energy One’s platform supports clients across Australia and Europe, delivering seamless integration across the entire energy trading lifecycle, from trade initiation to risk management, settlement, and regulatory reporting. This comprehensive capability increasingly differentiates it from competitors who specialise in narrower market segments.

Business Model: A Unique One-Stop-Shop Approach

Energy One’s integrated “one-stop-shop” software platform addresses the complexities of modern energy markets. Its end-to-end service model is particularly well-suited to the challenges posed by intermittent renewable energy sources, real-time pricing, and evolving regulatory frameworks.

By offering a full suite of energy trading solutions, Energy One enables utilities, energy retailers, and independent power producers to optimise trading, manage risks, automate settlements, and remain compliant. As energy markets grow more complex, the demand for holistic platforms like Energy One’s is set to expand significantly.

Source: Company

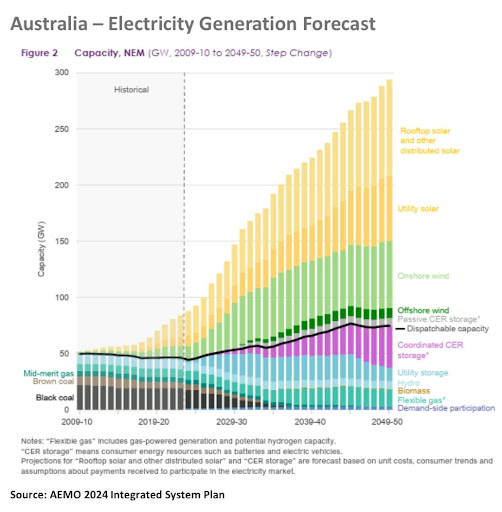

Market Dynamics: A Multi-Decade Tailwind

The energy transition is driving unparalleled growth opportunities. In Australia alone, over 300 new renewable energy assets are projected over the next five years, with wind generation expanding at 18% per annum and battery storage deployments growing at an astounding 40% annually.

Globally, particularly in Europe, the transition is even more profound. European energy markets are approximately 20 times the size of Australia’s, offering a substantial runway for growth.

As grids become more decentralised and complex, real-time trading, hedging, and settlement solutions become non-negotiable for financial stability. Energy One stands at the heart of this systemic transformation.

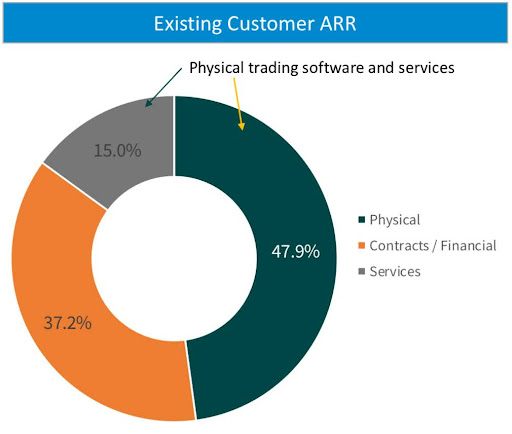

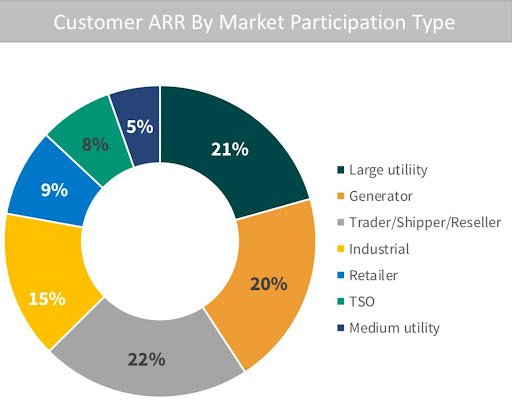

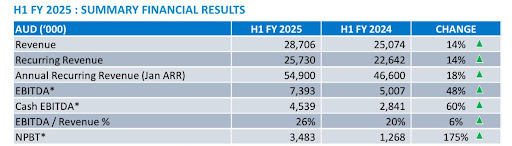

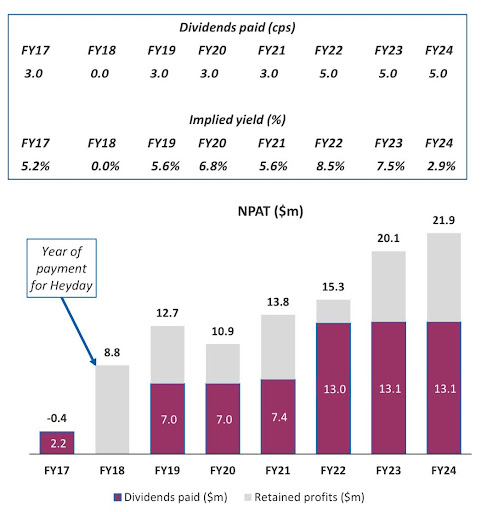

Financial Performance: A Record of Growth and Resilience

Energy One’s financial results for the first half of 2025 showcase robust operational strength:

Operational margins improved through strategic restructuring

Consistent 15-20% revenue growth targeted

The company maintains an impressive customer profile, with average contracts ranging from $150,000 to $200,000, and enterprise clients capable of generating up to $1 million in initial-year revenues. Importantly, the company’s European revenue share has grown from zero to 56% over recent years, significantly de-risking its revenue base and enhancing scalability.

Source: Company

Technological Innovation: Building the Energy Market of Tomorrow

Energy One is not resting on its laurels. The company is investing heavily in future-proofing its platform through:

Integration of Artificial Intelligence to enhance predictive analytics and automation

Development of automated trading platforms to streamline operations

Strengthening cybersecurity to protect critical infrastructure

Offering 24/7 operational support to cater to the needs of global energy traders

This commitment to innovation positions Energy One as more than a software provider, it is a strategic partner for energy market participants navigating the renewable revolution.

Growth Strategy: Focused and Disciplined Expansion

Energy One’s strategic growth pillars include:

Optimising pricing structures to enhance margins

Improving sales effectiveness and customer acquisition

Expanding market presence, particularly across European markets

Developing tailored solutions for emerging independent power producers and market entrants

With low current European penetration (~10%), the addressable market opportunity remains vast.

Future Outlook: Ambitious but Achievable Targets

Management has articulated clear and measurable goals:

Expand cash EBITDA margins from 16% to 30% by FY27

Maintain consistent organic revenue growth of 15-20%

Continue developing and deploying industry-leading technology

Capitalise on the accelerating global shift to renewable energy

If the company achieves these milestones, we assess an intrinsic valuation of over $20.00 per share is realistic.

Source: Company

Investment Relevance: Why Energy One Stands Out

Energy One (ASX: EOL) ticks all the fundamental boxes sought by discerning investors:

Founder-led leadership with strong alignment to shareholders

Profitable and growing with high recurring revenue visibility

Robust balance sheet and scalable business model

Positioned at the nexus of the global energy transition

In a sector characterised by disruption and rapid change, Energy One offers a rare combination of technological edge, operational excellence, and strong secular tailwinds.

TAMIM Takeaway

Energy One exemplifies the type of high-quality small-cap business investors should seek when targeting exposure to the global energy transition. It is profitable, founder-led, growing its market share, innovating continuously, and addressing a critical need in the energy trading ecosystem.

For investors seeking technology-enabled leverage to renewable energy trends—without taking on the high risks associated with pre-revenue green tech startups—Energy One is a compelling proposition.

As a strategic enabler of the new energy economy, Energy One deserves close attention.

This week’s TAMIM Reading List explores the forces shaping how we think, invest, and imagine the future. From the challenge of discerning truth in a digital age to the deeper structural shifts in manufacturing and financial markets, we see a world in flux where certainty is elusive and complexity is rising. We reflect on the vulnerability of a generation to misinformation, the tools we can wield against it, and the surprising persistence of casino-like behaviour in capital markets. Meanwhile, discoveries across the cosmos from hidden hydrogen gas to the search for alien artifacts, remind us that exploration and understanding often advance through uncertainty. Even at home, the rapid reinvention of nations signals how quickly paradigms can shift. It’s a reading list for those seeking perspective amid the noise.

This week’s TAMIM Reading List captures a world quietly shifting beneath our feet. In the U.S., the heartland’s economic recovery offers cautious optimism, while Europe begins to redefine its place on the world stage. AI looms large from Nvidia’s pivotal role in global power dynamics to undercover bots infiltrating protests. We reflect on the legacy of leadership through the lens of President Biden’s cognitive fitness and explore how perception shapes reality. There’s also fresh evidence suggesting life beyond Earth and surprising lessons from slot machines and doctor visits. A collection of stories about what’s shaping and shaking our sense of control.

Investing in Australia’s Energy Infrastructure Backbone

In this three-part series, we outline the Tamim investment framework for identifying ASX-listed companies that provide the critical infrastructure, software, and services enabling the global energy transition. This thematic investment approach focuses on businesses that support the structural shift from fossil fuels to renewable energy sources, energy storage, and grid modernisation.

Part 1 highlights Southern Cross Electrical Engineering Ltd (ASX: SXE), a leading player in Australia’s energy and infrastructure sectors. As the world mobilises capital towards net-zero emissions targets, SXE stands out as a profitable, well-capitalised business poised to benefit from Australia’s growing infrastructure and electrification spend.

Business Overview: A Strategic Operator in Energy and Infrastructure

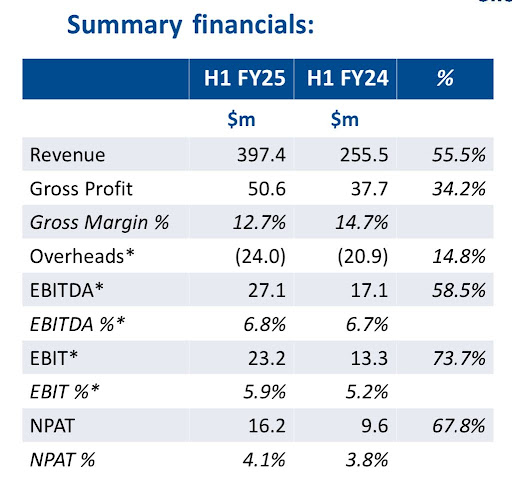

Southern Cross Electrical (SXE) has delivered record financial results, validating its position as a key contractor in the infrastructure and energy transition markets. The company’s first-half FY25 performance demonstrated exceptional operating momentum:

Revenue grew by 55.5% to $397.4 million

EBITDA increased by 58.5% to $27.1 million

Net profit rose by 67.8% to $16.2 million

Sources: Company

Infrastructure remains the company’s core revenue driver, accounting for 63.3% of total revenue. Key projects include the Collier Battery Energy Storage System, significant works at Western Sydney Airport, and the Shellharbour Hospital development—the largest healthcare project in SXE’s history.

Sources: Company

Capitalising on Data Centre Expansion

One of the company’s most compelling growth vectors is its rapid expansion into data centres, driven by the proliferation of cloud computing and artificial intelligence workloads.

SXE has increased its data centre revenue from approximately $20 million annually (FY19–FY23) to $50 million in FY24, with a projected rise to $120 million in FY25. The company is currently tendering for more than $500 million in future data centre projects.

Electrification and Energy Transition Exposure

SXE is directly aligned with Australia’s decarbonisation and infrastructure modernisation agenda. The company provides:

Engineering services for solar and wind farms

Battery storage installations

Electrical upgrades for industrial customers

Modernisation of grid and electrical infrastructure

This makes SXE a direct beneficiary of the electrification megatrend underpinning the global push towards net-zero emissions. Unlike many companies in the space, SXE is already generating strong earnings, has no debt, and pays a fully franked dividend.

Balance Sheet Strength and Strategic M&A

SXE’s robust financial position underpins its capacity for future growth:

$114.8 million in cash

No debt

Record $670 million order book

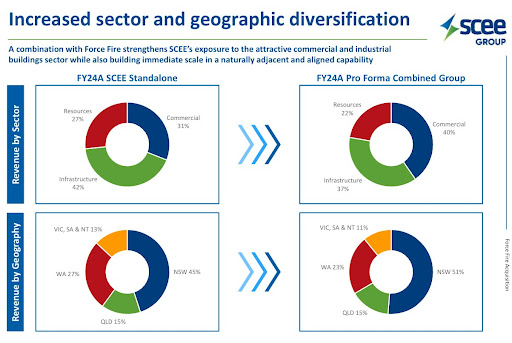

The company recently acquired Force Fire Holdings, a NSW and QLD-based fire safety services provider. The transaction was funded entirely from existing cash reserves:

Initial consideration: $36.3 million; total up to $53.5 million with performance-based earnouts

EBIT contribution forecast: $10 million in FY26

EPS accretive from day one

The acquisition provides strategic synergies by expanding SXE’s capabilities and footprint while increasing exposure to recurring revenue through maintenance contracts.

Valuation and Market Opportunity

SXE currently trades at:

~10x forward PE

A fully franked dividend yield of 5%

Source: Company

Comparable infrastructure and services companies on the ASX typically trade at mid-teens earnings multiples. Given SXE’s growth profile, strong cash position, and strategic alignment with key infrastructure trends, a market re-rating is possible.

We assess the company’s intrinsic value to be in excess of $2.00 per share, supported by earnings momentum and the scalability of recent acquisitions.

Investment Relevance

The structural transition in energy systems globally and in Australia necessitates significant capital deployment. Investors seeking exposure to this trend should look beyond pure-play renewables or speculative technologies and consider enabling businesses such as SXE.

Southern Cross Electrical offers:

Tangible exposure to data centre growth, renewable energy buildout, and electrification

A well-diversified client base and project pipeline

A disciplined M&A strategy funded by internal resources

Operational and financial resilience

SXE is not reliant on regulatory subsidies or unproven technologies. Instead, it generates consistent, growing profits from real-world projects.

Tamim Takeaway

Southern Cross Electrical is a compelling example of a high-quality, small-cap company delivering on Australia’s energy transition objectives. The company offers investors:

Leverage to infrastructure and decarbonisation trends

Strong financial discipline and capital allocation

A well-supported dividend yield with upside from valuation normalisation

For investors seeking reliable exposure to Australia’s net-zero infrastructure buildout, SXE deserves serious consideration as a core small-cap holding.

Stay tuned for Part 2 of The Small Cap Energy Transition Playbook, where we examine a software-driven billing and customer engagement company facilitating the shift to distributed energy systems and smart metering.

Disclaimer:Southern Cross Electrical Engineering Ltd (ASX: SXE) is held in TAMIM Portfolios as at date of article publication. Holdings can change substantially at any given time.