This week’s TAMIM Reading List dives into industries, policies, and ideas undergoing transformation. GLP-1 drugs are challenging the life insurance industry’s traditional models, while off-premises dining has evolved from a temporary trend into an essential pillar for restaurants and consumers. We take a closer look at the origins of the Baby Boom and the powerful demographic and cultural forces it unleashed. On the geopolitical stage, we examine whether the U.S. is truly prepared for the next major conflict. Education and research also come into focus with a deep dive into the origins of the modern research university. Finally, clean energy advocates are racing to take advantage of tax credits before they disappear, underscoring the shifting dynamics of policy and innovation.

This week’s TAMIM Reading List explores the balance between chaos, memory, resilience, and reflection. We begin with lessons from the world’s oldest people and the molecular bond behind memories that last a lifetime. On the other side of the spectrum, a WhatsApp stock scam reveals how quickly trust can unravel, while flash flooding in New York and a tragic ferry accident in Bali remind us of nature’s force and fragility. We consider the quiet death of partying in America and what it says about changing social rhythms, while Mitchell Starc’s 100-Test milestone stands as a reminder that grit and longevity still matter. A list built on contrast, between risk and endurance, loss and legacy.

At TAMIM, we believe investing is as much about managing risk as it is about pursuing returns. In fact, one of the most critical frameworks in our investment process is a concept introduced nearly a century ago by Benjamin Graham and deeply embedded in the work of Seth Klarman: margin of safety.

In a world that often prioritises speed, speculation, and sentiment, Klarman’s Margin of Safety reminds us that true long-term outperformance is built on prudence, patience, and protection of capital.

This is not simply theory. It’s a blueprint for navigating both opportunity and uncertainty, especially relevant for Australian investors navigating today’s complex environment in equities, credit, and property.

The Core Principle: First, Do No Harm

Klarman’s fundamental belief is that successful investing starts with avoiding permanent loss. Returns matter, but only if you protect the capital base they are built on.

To illustrate this: an investor who compounds at 16% annually for 10 years will outperform someone who compounds at 20% for 9 years and then suffers a 15% loss in year 10. The compounding effect is powerful, but it is also fragile.

This is why TAMIM places such a strong emphasis on downside risk management. Before we assess upside, we consider what can go wrong and how we would be positioned if it does.

Investing vs Speculating: Know the Difference

Klarman distinguishes clearly between investing and speculation. Investors focus on cash flows, valuations, and business fundamentals. Speculators focus on price movements, narratives, and momentum.

The rise of retail trading, short-termism, and thematic ETFs has made speculation more accessible but also more dangerous. As Klarman puts it, many market participants are not buying assets because they are undervalued, but because they believe someone else will pay more for them later.

At TAMIM, we invest in businesses, not stories. We seek to understand what a company is worth, not what the market might temporarily believe.

Absolute Returns Over Relative Games

Another key theme in Margin of Safety is the importance of absolute performance. Many managers obsess over relative returns, “Did we beat the ASX200?”, even if their portfolio delivered a negative return.

We take a different view. The goal is not to beat a benchmark. The goal is to preserve and compound capital in real terms.

This philosophy requires discipline. There will be times when markets rally on speculative sentiment, and we may hold elevated cash positions or avoid popular sectors. But over a full cycle, this mindset protects capital and positions us for better long-term outcomes.

Cash is Not Failure Rather It’s Optionality

Klarman is unambiguous: when no attractive investments are available, the rational choice is to hold cash. Cash provides flexibility, liquidity, and the ability to act when mispricing occurs.

Buffett does the same. Holding cash is not a sign of indecision. It is a conscious choice to wait until the market offers a sufficient margin of safety. When opportunities do arise as they often do in moments of dislocation, cash is what allows an investor to act with confidence.

Beware of Accounting Shortcuts

One of the more technical but important observations in Klarman’s work is the caution against relying on accounting shortcuts like EBITDA as a measure of profitability.

Depreciation and amortisation are real economic costs, especially in capital-intensive businesses. Ignoring them can distort true cash flow and lead to overvaluation.

At TAMIM, we focus on free cash flow, return on invested capital, and underlying business quality, not just headline earnings or cosmetic multiples.

Valuation: Three Practical Tools

Klarman outlines three main valuation methods that remain essential today:

Net Present Value (NPV): Used when future cash flows are reasonably predictable.

Liquidation Value: A conservative assessment based on tangible assets, useful in distressed or asset-heavy companies.

Market Comparables: Useful for understanding how peers are valued, though to be used cautiously.

We use all three, depending on the business in question, and always with a focus on conservatism. Forecasting is inherently uncertain which is why we prefer to anchor our assessments in reality, not optimism.

Quality Over Quantity: Concentrated Portfolios

Klarman advocates for focus. You do not need 50 or 100 positions to be diversified. Twenty to thirty well-understood investments diversified across sectors, geographies, and risk factors can be sufficient.

At TAMIM, we construct concentrated portfolios by design. We believe true conviction comes from deep understanding. Over-diversification, in contrast, can dilute returns and hinder active management.

Market Inefficiencies Are Real

While markets are often efficient, they are not always so. Klarman identifies several areas where disciplined investors can find mispricing:

Forced selling (e.g. spinoffs, index exclusions)

Illiquidity or low coverage (e.g. small caps)

Temporary disruptions (e.g. macro shocks or earnings misses)

Distressed assets (e.g. corporate restructurings or bankruptcies)

These are often areas where short-term investors, index funds, or institutional mandates cannot or will not participate. That creates opportunities for long-term investors with patient capital.

Portfolio Management: A Disciplined Framework

Klarman’s approach to buying and selling is methodical:

Buy when the margin of safety is wide, not based on forecast optimism.

Sell when the valuation converges with intrinsic value or the investment thesis changes.

Hold cash when valuations are stretched or opportunities are limited.

At TAMIM, we follow a similar discipline. Every holding is reviewed continuously, not just on performance, but on the validity of the thesis and valuation. And we are comfortable holding elevated levels of cash or reducing position sizes when required.

Investor Psychology: The Hardest Part

Much of what Klarman outlines requires not just analysis, but temperament. The ability to be patient, to resist herd behaviour, and to act decisively when markets are panicked.

This is where many investors struggle, not because they lack information, but because they are not emotionally prepared for volatility.

Our role at TAMIM is not only to construct portfolios, but to remain clear-headed and calm when others are not. Margin of safety is a mindset as much as a metric.

TAMIM Takeaway

Seth Klarman’s Margin of Safety is not a trendy framework. It is a timeless one.

In a world where short-termism dominates and risk is often mispriced, the principles of capital preservation, valuation discipline, and thoughtful portfolio construction remain as relevant as ever.

At TAMIM, we adhere to these principles, not because they are fashionable, but because they work. Through every investment cycle, our goal is the same: to protect capital first, and grow it responsibly over time.

If you’d like to learn more about how we apply these principles across equities, credit, and property or how they inform our current asset allocation, we’re always happy to engage.

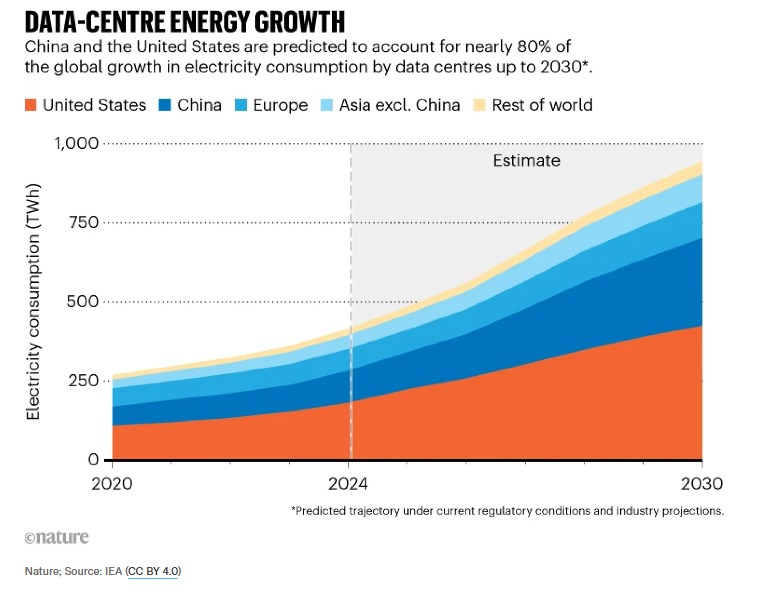

Let’s start with a bold premise: if we’re serious about building the infrastructure of the future, one that can support the exponential demands of AI, digital transformation, and decarbonisation, then we need to stop tiptoeing around nuclear energy. The power needs of the next generation are staggering, and nowhere is this more evident than in the United States, where data centre energy consumption is projected to quadruple by 2030.

At Tamim, we’re constantly scanning for mispriced assets, misunderstood value, and global disconnects that others overlook. Right now, one of the most glaring opportunities lies in Japan, specifically, its fleet of dormant nuclear power plants, sitting ready to supply massive baseload energy to an AI-hungry world.

Let’s unpack why.

AI’s Insatiable Appetite for Power

In the US Data Centre Energy Consumption chart, we see the trajectory of energy use by American data centres. From 147 TWh in 2023 to a forecasted 606 TWh by 2030, data centres will represent nearly 12% of total US power demand. That’s not incremental growth, that’s a structural reordering of the energy grid, driven by artificial intelligence, machine learning, cloud computing, and high-density enterprise storage. The biggest tech names: Meta, Amazon, Microsoft, Nvidia are all pushing the limits of data processing. The AI boom isn’t a cycle. It’s an epoch.

Meta recently tried to develop a 4GW power source for its data centres, only to be stopped by environmental objections involving bees.

With the U.S. facing both environmental and bureaucratic barriers, it’s time to look east.

Japan: A Sleeping Giant in the Nuclear World

The 2011 Fukushima disaster understandably pushed Japan to idle most of its nuclear reactors. But time, technology, and regulatory progress have shifted the picture dramatically. More importantly, the market has yet to catch up with this change in sentiment and potential.

Take Hokkaido Electric Power (TSE: 9509), for example. It owns the Tomari Nuclear Power Plant, a three-reactor PWR facility that’s been offline since 2011. The plant ran at near 100% capacity when operational and remains structurally sound and technically ready. It’s located in southwest Hokkaido – a cold, isolated area perfect for large-scale data centre co-location.

Why isn’t it online now? Bureaucracy. Specifically, a lack of staff at the Nuclear Regulation Authority to answer final technical questions. Not technical problems. Not infrastructure issues. Just a slow process.

Meanwhile, the Tomari plant’s 4GW capacity is sitting idle, nearly the same amount Meta was trying to build from scratch in the U.S. And unlike renewables, nuclear provides the consistent baseload power that data centres require 24/7. Japan’s existing infrastructure could be rebooted faster and more economically than new builds elsewhere.

Cement, Renewables, and Cost Illusions

Let’s address the elephant in the room: the debate between nuclear and renewables. Much of the opposition to nuclear power is not grounded in science, but in ideology.

Take wind turbines, for example. Anchoring just one turbine requires between 1,000 and 2,000 tonnes of cement. Cement production emits sulphur dioxide, nitrogen oxides, and carbon monoxide, pollutants that rarely make it into the glossy charts presented by renewable lobbyists. And then there’s the intermittency problem: wind and solar are variable; nuclear is not.

The bottom line? Nuclear energy, particularly from already-built plants, remains the most carbon-efficient and scalable solution for industrial power demand. And right now, Japan is sitting on a stockpile of it.

Valuation Disconnect: Hokkaido, Kansai, Shikoku

Let’s look at the numbers. Hokkaido Electric Power is trading on a P/E of 3.6x, a P/B of 0.45x, and an EV/EBITDA of just 11.5x. Compare that with the stretched valuations in global equities. As an infrastructure play with a nuclear asset that could be back online within 12–18 months, it’s one of the most asymmetric investment opportunities in global markets.

It’s not just Hokkaido. Kansai Electric (TSE: 9503) and Shikoku Electric (TSE: 9507) are also on the runway for nuclear restarts. Both have already received NRA clearance to resume operations.

Yet, these utilities still trade well below their long-term highs. The market continues to treat these companies like they’re operating in 2012, not 2025.

But the macro backdrop has shifted.

Macro Themes Colliding in 2025

Several powerful currents are now converging:

AI growth is structurally increasing power demand; especially for constant, uninterrupted supply.

The US and Europe are struggling to build new baseload power plants, due to cost, environmental regulation, and political inertia.

Japan’s fiscal and energy policy has pivoted toward reindustrialisation and economic security. Nuclear reactivation fits squarely within that mandate.

Valuations remain deeply discounted, reflecting a regulatory status quo that’s already shifting.

In short, this is a rare case where energy policy, AI infrastructure, and contrarian value investing collide.

Why We Like It at TAMIM

At TAMIM, we look for investments where the downside is well protected and the upside is driven by mispriced probabilities. Hokkaido, Kansai, and Shikoku all qualify.

These are not “hope and hype” stories. These are tangible assets with decades of operational history, efficient legacy infrastructure, and balance sheets that have weathered over a decade of idleness. The regulatory dominoes are falling into place and the AI data centre boom is creating a once-in-a-generation tailwind.

The TAMIM Takeaway

In a world where markets are obsessed with the next chip design or data analytics platform, we believe the real infrastructure play lies in powering that future.

Japan’s nuclear utilities are underappreciated, undervalued, and sitting on gigawatts of capacity that offer investors a unique opportunity to align with one of the most urgent megatrends of the decade: the energy demands of AI.

We expect these companies to re-rate significantly as restarts proceed and the global hunt for stable power intensifies.

Disclaimer: Hokkaido Electric Power (TSE: 9509) and Shikoku Electric (TSE: 9507) are held in TAMIM Portfolios as at date of article publication. Holdings can change substantially at any given time.

Domino’s Pizza Enterprises (ASX: DMP) has long been a household name in Australia and beyond. From its humble beginnings to becoming a dominant player across the Asia-Pacific and European markets, Domino’s built its brand on one simple idea: deliver great pizza fast. But in recent years, this once-reliable recipe has started to crack.

Sales stagnated, franchisee profitability melted away, and new competition from delivery aggregators left the company looking more like a tired takeaway than a growth engine. For long-term investors, Domino’s became a frustrating experience, a great brand held back by execution missteps and an overly ambitious expansion strategy.

Yet, what we are seeing today is a compelling narrative of change. A pivot. And, quite possibly, a very rewarding turnaround.

This view was reinforced in the most recent investor update call on Thursday, July 3, 2025, led by Executive Chairman Jack Cowin, following the unexpected resignation of CEO Mark van Dyck after just seven months in the role. The Zoom-based meeting offered candid insight into Domino’s refreshed mindset, one focused on execution, franchisee profitability, and a return to operational excellence.

A Decade of Momentum, Then a Sudden Pause

Between 2010 and 2020, Domino’s was a market darling. Under long-time CEO Don Meij, the company executed a tech-driven growth strategy, investing heavily in logistics, ordering platforms, and store expansion. Earnings grew, margins expanded, and the stock price skyrocketed.

But no growth story lasts forever.

Post-COVID, Domino’s ran into a perfect storm:

Overexpansion in weaker international markets

Margin pressure from rising labour and food input costs

Increased competition from Uber Eats, DoorDash, and Deliveroo

Frustration from franchisees who saw profitability fall sharply

Same-store sales growth stalled, and the operational leverage Domino’s once touted began working in reverse. Investors started losing faith. And yet, through the noise, the underlying brand strength remained.

The “Pizza Reset” Begins

Now, Domino’s is undergoing a significant operational and strategic overhaul. Led by Executive Chairman Jack Cowin, the founder who turned a $400,000 investment into a global pizza empire, the company is slicing out inefficiencies and turning up the heat on performance.

Let’s break down the key ingredients of Domino’s comeback recipe.

1. Leaner, Smarter Operations

Domino’s is targeting corporate cost reductions, particularly in its tech and administrative divisions. While the company has always presented itself as a tech-enabled retailer, it became apparent that not all technology was delivering ROI. Systems that over-promised and under-delivered are being replaced or eliminated.

This isn’t just about saving dollars, it’s about re-focusing on simplicity. The company is reverting to its core strengths: fast, reliable pizza delivery, and supporting its franchisees to grow.

2. Rebuilding Franchisee Trust and Profitability

Perhaps the most important strategic initiative is rebuilding the relationship with franchisees. Many stores have struggled to remain profitable, with average store earnings hovering around $95,000 per annum, hardly compelling for a small business owner bearing significant risk.

Domino’s now has a stated target of increasing this to $130,000 per store. That’s not just a feel-good number. It signals a shift from top-line obsession to bottom-line delivery. Key initiatives include:

Menu simplification to reduce labour costs

More targeted marketing campaigns

Smarter store placement and closure of underperforming units

Cost-effective use of promotions and discounts

Franchisee profitability is the bedrock of Domino’s success. More money in the pockets of operators translates to better service, more consistent branding, and ultimately, sustainable growth.

3. CEO Transition: Fresh Thinking, New Era

The sudden departure of CEO Mark van Dyck, after just seven months, might have shocked the market. But the July 3 update made clear: this is not a crisis. It is an opportunity to reset the leadership tone. Jack Cowin has stepped in to steer the ship while the board seeks a new CEO, someone focused not on global dominance, but on operational excellence and franchisee support.

This change matters. A fresh CEO can re-energise the company culture, bring new ideas, and re-establish confidence in execution. With Cowin still deeply involved, the balance between entrepreneurial vision and disciplined management may finally be achieved.

Financials: Signs of Stabilisation

Despite the doom and gloom of recent years, Domino’s is not a broken company. It still generates over $100 million in after-tax profit and maintains a robust balance sheet. There’s no need for capital raisings, and no looming debt crisis.

What we are witnessing is a business that overshot on ambition but retains brand equity, infrastructure, and customer trust.

Importantly, Domino’s has signalled a return to modest, consistent same-store sales growth. A 3% same-store sales figure may sound pedestrian, but with improved margins and disciplined cost control, this could drive double-digit earnings growth in coming years.

Competitive Landscape: The Delivery Duopoly Dilemma

No modern discussion of Domino’s is complete without acknowledging the rise of delivery aggregators. Uber Eats and DoorDash have changed how customers access food. The convenience of multi-brand menus and app-driven promotions is formidable.

Yet, this isn’t a death sentence for Domino’s. In fact, it may become a strength.

Domino’s is one of the few brands that controls its own delivery logistics at scale. This means:

Lower delivery fees

Full control over customer experience

Better data on ordering habits

No revenue-sharing with third parties

With aggregators increasingly squeezing restaurants with commissions and advertising fees, Domino’s stands out as a vertically integrated model. In a world of rising costs, owning the delivery process is a differentiator.

The Macro Backdrop: In Pizza We Trust

In times of uncertainty, consumers often turn to comfort, affordability, and familiarity. Fast food, particularly pizza, has long been a defensive consumer staple. Whether interest rates are high or economic confidence is low, families still crave a Friday night pizza.

That macro trend supports the Domino’s thesis. Moreover, rising wages and improving employment metrics should aid the very franchisees who power the company’s store network.

Risks and Hurdles to Watch

No investment is without risk. For Domino’s, key issues include:

Execution: Can new leadership deliver on profitability targets?

Competition: Will aggregators continue eating into market share?

Wage inflation: Labour remains a major cost centre

Market saturation: Are there still growth opportunities in mature regions?

However, these risks are now better acknowledged, and the company is actively addressing them, making it a more investable proposition today than it was 12 months ago.

The TAMIM Takeaway: A Slice of the Right Strategy

At TAMIM, we like companies that are misunderstood, undervalued, and fixing their flaws. While we don’t currently own the stock, Domino’s could fit this mold going forward. The story is no longer about pizza delivery, it’s about operational reinvention, franchisee empowerment, and strategic humility.

If Domino’s executes, this could be one of the more compelling medium-term turnarounds on the ASX.

The brand remains strong

The balance sheet is solid

The strategy is refocused and realistic

The leadership refresh is well-timed

In other words: Domino’s is still cooking. Just at a slightly lower temperature, with a sharper recipe. Dominos remains on our watchlist with us looking for clear signs of execution.

Disclaimer: Companies and stocks mentioned in this article are not held in TAMIM Portfolios as at the date of publication. Holdings may change substantially at any time.