A Forgotten Small Cap, Poised for Re-Rating

In the underfollowed world of ASX small caps, it’s rare to find a stock that combines deeply discounted valuation, tangible earnings visibility, and the potential for outsized upside. Pioneer Credit (ASX: PNC) is one such opportunity. Operating in the personal debt recovery space, this niche player is quietly rebuilding momentum, buoyed by strong sector tailwinds and a disciplined operational reset.

At TAMIM, we’ve long emphasised the value of small cap value stocks that combine real cash flow with misunderstood narratives. Pioneer Credit (ASX: PNC) fits squarely into this camp. With its stock trading well below its liquidation value and clear earnings growth on the horizon, it may be one of the more compelling ASX turnaround opportunities in 2025.

The Business Model: Focused and Understood

Pioneer Credit is a pure-play retail debt recovery business. Its model is simple: purchase portfolios of delinquent consumer debt (PDPs) at a discount and then collect repayments over time. Unlike some debt recovery stocks on the ASX that dabble in origination or lending, PNC stays firmly within its lane, collection.

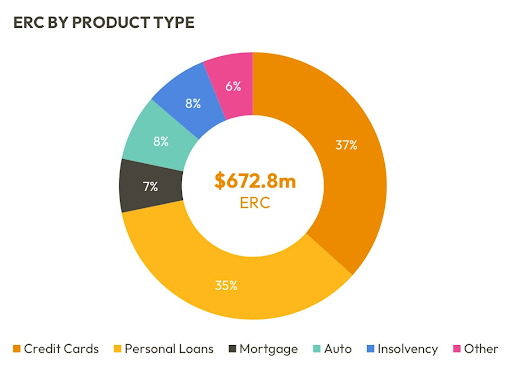

It has a customer base of over 750,000 people, with 220,000 active accounts. Approximately half of the debt it manages comes from Australia’s major banks, and the other half from non-bank lenders, providing a diversified stream of accounts.

Since listing in 2014, Pioneer has delivered consistent net IRRs above 15% on its portfolios, suggesting a solid return framework, especially in an asset-light, cash-generating model.

Valuation Gap: A Deep Discount to Fundamentals

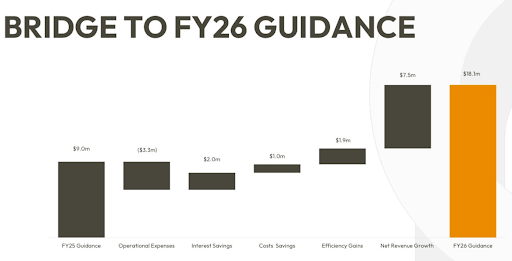

Despite its underlying profitability, Pioneer Credit trades on just 8.5x forecast FY25 earnings and 4x FY26 earnings, assuming the company achieves management guidance of $18 million NPAT by FY26. This implies a sub-$75 million market capitalisation for a business that could feasibly generate more than that in net present value over just a few years.

Perhaps more compelling, management has flagged that the company’s liquidation value sits between $200 million and $330 million. This disconnect, where Pioneer trades closer to its debt recovery value than its going concern value, creates a compelling investment case for patient holders of small cap value stocks in 2025.

The Turnaround Story: From Crisis to Clarity

Pioneer’s journey hasn’t been smooth. In 2019, corporate governance issues and a funding covenant breach led to a trading halt and a dramatic collapse in market value. The stock plummeted, and by April 2020, PNC was trading at just $0.10 per share.

Since then, the business has stabilised. Debt has been refinanced, most recently in July 2024, reducing interest costs by $8 million annually, and operational discipline has returned. Portfolio acquisitions are now selectively focused, and the business is on a clearer path to profitability.

The result is a company with lower financial risk and stronger operational footing. For investors focused on ASX turnaround opportunities, the transformation at PNC should not be overlooked.

Tailwinds in the Sector: Supply and Rationalisation

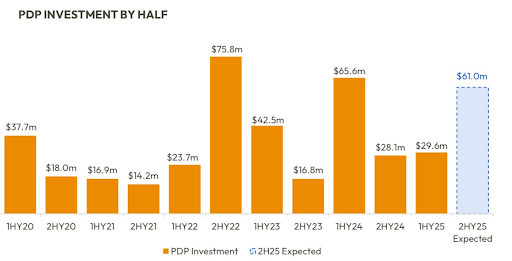

Debt recovery stocks on the ASX benefit from cyclical and structural dynamics. The supply of purchased debt portfolios (PDPs) is rising, $325 million in FY24 and expected to grow to $400 million in FY25. Banks and non-bank lenders alike are offloading bad debts at scale, seeking balance sheet relief.

At the same time, the industry is consolidating. With fewer active players and increased focus on return discipline, competition for PDPs is becoming more rational. This trend supports improved IRRs for those with proven collection infrastructure, like Pioneer Credit.

Litigation Optionality: A Material Catalyst

One potential near-term catalyst lies in PNC’s $32 million legal claim against PwC, stemming from legacy audit failures. The claim is set for resolution in Q1 FY26. If successful, it could unlock significant shareholder value, either via special dividends, debt reduction, or accelerated reinvestment in new PDPs.

This litigation represents real optionality, not often found in companies at this valuation level. It adds further upside to an already asymmetric risk-reward profile.

Management’s Long-Term Ambition

The leadership team at Pioneer Credit has outlined a bold target: growing NPAT to $50 million and achieving a $1 billion market cap in the next few years. While ambitious, the framework is grounded in tangible steps:

- Scaling the PDP book via disciplined acquisitions (guidance: $90m in FY25);

- Leveraging existing infrastructure to expand margins;

- Monetising the broader customer database beyond collections.

This aspiration aligns with the criteria for small cap value stocks in 2025 that offer a genuine pathway to scale and sustained returns.

Risks: Pricing Reflects Known Challenges

Of course, no investment comes without risk. Pioneer carries debt, $290 million as of the latest update, and requires careful capital management. Regulatory risk is ever-present in the collections space. Execution of the FY25–26 turnaround hinges on sustained PDP purchasing discipline and portfolio performance.

Yet, at a $76 million market cap, these risks appear not only understood but heavily priced in. For investors seeking undervalued opportunities with high upside, Pioneer remains one of the more contrarian ASX turnaround opportunities available.

Tamim Takeaway: Real Cash Flow, Misunderstood Risk, Uncommon Value

Pioneer Credit (ASX: PNC) is the type of stock that rarely makes headlines, but quietly rewards patient investors. It combines a simple business model, a recovering balance sheet, strong insider alignment, and multiple paths to value creation.

Whether you’re seeking exposure to debt recovery stocks on the ASX, looking to add small cap value stocks in 2025, or searching for ASX turnaround opportunities, PNC demands closer inspection.

Actionable Insights for Investors:

- Track August 2025 results to confirm earnings momentum.

- Watch for developments in litigation that may unlock material capital.

- Reassess valuation relative to earnings and liquidation benchmarks.

- Position sizing is key, this is a high beta, high reward opportunity.

At Tamim, we continue to find opportunity in unloved, mispriced companies that quietly compound capital. Pioneer Credit (ASX: PNC) fits that thesis, with an added layer of litigation optionality and operating leverage. It may be time for investors to give this hidden gem another look.

Disclaimer: Pioneer Credit (ASX: PNC) is held in TAMIM Portfolios as at date of article publication. Holdings can change substantially at any given time. Source: Company ASX material, discussions with management, Tenva Capital Research