10 Stocks that Benefit from Emerging Market Growth? Robert Swift – Head of Global Equity Strategies

After a few years of poor performance across emerging market equities, perhaps it is time for us to revisit the sector? Valuations look cheap relative to developed markets and with the exception of Brazil and South Africa, most economies have actually held up well. On a debt to GDP basis many emerging markets are actually in a healthier position than the developed ones. The continued higher population growth and the tendency for economic ‘catch up’ from a lower base, remain favourable trends for emerging markets, and all it may need for a rebound in asset prices is a catalyst?

To be sure, debt, currency fluctuations, and political risk are still present but most investment returns are seldom attractive without some degree of highly visible risk. It tends to “go with the territory” in looking for Value. However, rather than invest directly in stocks quoted on emerging market exchanges it has often been better to invest in companies listed on major developed exchanges but only where they derive meaningful revenues and profits, from emerging economies.

We have invested globally for many years and can identify companies which are capable of adapting products and business practices to local cultures and regulations. Such companies will tend to be long term successful in these markets. It has often been possible to capture emerging market growth, and participate in periods when emerging market stocks outperform, by investing in mature market stocks.

The benefits of investing in emerging economies this way are numerous.

Easier access – Some emerging markets prevent foreigners from investing without permission or a licence. This permission is typically reserved for institutional size investors. Smaller investors can access emerging markets through developed market stocks. This is especially true for technology stocks where Taiwan and Korea are hard to access directly.

Western governance is often more transparent – although not always perfect, standards tend to be fairer toward minority shareholders in developed stock markets

Liquidity – the bid offer price spread, commission rates and overall levels of price volatility tend to be lower in developed markets making it easier for investors to remain calm and objective, and invest more of their money in the company rather than pay to agents in transaction costs

When emerging markets perform better these companies tend to outperform developed market companies.

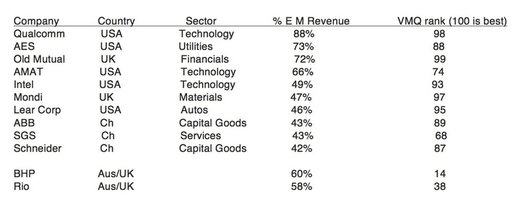

We have an extensive fundamental and accounting database which we use to assess the world’s major listed companies. We have recently done some work on ranking and identifying developed market companies with at least 40% of their revenue derived from emerging economies. The list of 10 of our favourites is below. By favourites we mean both >40% revenues from emerging economies AND attractively ranked on our quantitative stock VMQ model. We include both revenue % from emerging economies and our score in the table below. They are ranked in order of revenue from emerging economies.

We include BHP and Rio for information purposes. If you own these already note how much emerging market exposure you are getting. Why not look to diversify away from only mining and Australia?

Having a look at the worlds wealthiest individuals shows that over the last decade, we are seeing a much greater proportion of these individuals being born in emerging market countries. This shows us large masses of wealth are being created in areas that a lot of local investors just don’t have much exposure to. These are exciting times for emerging markets, where arguably most of the future wealth of the world will be created in decades to come- are you positioned to benefit from this explosion of development? Speak to TAMIM today about increasing your exposure to these exciting international developments that will likely underpin strong future investment returns for your portfolio in the years to come.

This week TAMIM launches theTAMIM Australian Equity Small Cap Individually Managed Account. This week we start the first in a 3 series set of articles highlighting the advantages of incorporating Small Company shares in your portfolio. The fund underlying the TAMIM Australian Small Cap portfolio has returned over 37% in the 12 months to 31 May 2016. If you would like to discuss this IMA with one of our directors please contact us at ima@tamim.com.au. This opportunity is strictly limited to $100m to protect the portfolio investment style and philosophy.

Low Liquidity – Friend or Foe?

Smaller companies generally trade with lower liquidity than larger companies reflecting their smaller market following and large founder stakes. Contrary to popular opinion we view lower liquidity as core to the smaller company investment opportunity since smaller companies only trade at low liquidity levels when they are under-researched and undiscovered, and their valuations generally reflect this. This creates significant opportunities for investors who are prepared to find the high quality smaller companies trading at a significant discount to intrinsic fair value.

THE IMPACT OF LOW LIQUIDITY

Smaller companies are generally perceived to be higher risk investments than larger companies, largely due to the higher liquidity risk prevalent amongst smaller companies. These smaller companies often remain tightly held by a founding family and/or lack the institutional interest and ownership required to generate a sufficient level of stock liquidity. The market is generally biased against higher liquidity risk because no one wants to be stuck in a poor investment they can’t sell. However, as with most aspects of investing, we believe the reality is far from this simple. We view low liquidity as a double edged sword which can also create opportunity.

The market believes what the market believes. We have learnt to respect the market but at the same time understand that the market is not always right. Quite the contrary, the market can be incredibly inefficient, particularly at the smaller company end of the market where investors tend to be less informed. The effect of the market’s perception that higher liquidity risk makes smaller companies riskier than larger companies, is that many retail and institutional investors either stay away from illiquid stocks altogether, or are only happy to buy an illiquid stock at a much lower price than they would pay for an equivalent liquid stock. As a result, many smaller illiquid companies trade at much larger discounts to their intrinsic value to reflect this perceived risk. In many cases, the discount can be extreme.

“Lack of market liquidity can sometimes be of benefit to small-cap investors who already own shares. If large numbers of buyers suddenly seek to buy a less liquid stock, this can drive up the price further than in the case of a more liquid market.” – Investopedia.

We would go so far as to say that low liquidity is core to successful smaller companies investing. Our objective is to find undiscovered gems and to buy them when they are under-valued and illiquid, and before they are properly researched and understood by the market. Once they become liquid, these stocks will generally trade at significantly higher levels. The journey from illiquidity to liquidity is synonymous with the journey from undervalued to fair value and thus should be celebrated by experienced smaller companies investors.

EXAMPLE – FIDUCIAN GROUP LIMITED (ASX: FID)

Fiducian, a leading fund manager and financial planning operator, is one of our core holdings. We view the company as one of the highest quality micro caps on the ASX due to its excellent management team, clear growth strategy, strong competitive advantages and enviable track record of recent earnings growth. Fiducian’s earnings are expected to continue growing at double digit rates over the medium term and yet the stock is currently trading at only 11x FY16 underlying earnings and on a 5% fully franked dividend yield. This may seem strikingly cheap to large cap investors but this reflects the smaller company investment opportunity.

Recent trading in Fiducian provides an interesting insight into smaller company liquidity. As the chart below shows, the stock fell from $2.70 in January to $1.98 at the end of April. At $1.98, the stock was trading at only 9x FY16 earnings and on a fully franked yield of over 6% despite the company’s high quality business model, strong first half result and excellent growth prospects. While the volatile equity markets of early 2016 no doubt impacted sentiment towards Fiducian, the share price fall was accentuated by the stock’s low liquidity. If this was a large cap reporting excellent results it is very unlikely the stock would have fallen so dramatically.

In our minds this spelt opportunity so we bought more Fiducian stock into weakness at around the $2 mark. We viewed the selloff as a great opportunity to top up our shareholding in a high quality business on a very low valuation. Low liquidity once again presented a compelling opportunity which aligned with our disciplined value investing style and we were able to take advantage.

Conclusion

The reality is that liquidity risk can either play to your advantage or disadvantage as an investor. We believe many investors are missing a trick by viewing all smaller companies as riskier than larger companies. The fact that so many people view liquidity risk as a disadvantage provides an explanation as to why smaller companies often trade at such low valuations and therefore are attractive investment propositions.

In our opinion, the key to using liquidity risk to your advantage is to ensure you are investing in under-valued, high quality smaller companies where you have an information advantage. This is clearly easier to do in the smaller companies universe than amongst large caps where you may be competing with 20+ highly intelligent analysts who have followed the stocks for many years. When investing in smaller companies there may be no analysts at all following the stock so it is a far less competitive investment environment.

However, successful smaller company investing does require a disciplined filtering process since there are numerous listed smaller companies which will never reach profitability or a credible business model. We focus only on high quality companies which for us means having a diversified customer base, strong competitive advantages, a sensible growth strategy, a strong track record of earnings growth and good visibility around future earnings growth, and importantly, capable management who we are confident can execute on their growth initiatives. While illiquidity can offer great value buying opportunities, we do not want to be holding an illiquid company forever. Therefore, it is important that the investment has a clear pathway to growing earnings or growing its market capitalisation in order to attract a broader range of investor interest in the company. Fiducian is a great example of the type of company we will invest in, and one that we expect will attract greater broker and investor interest as it grows.

We are confident that applying a disciplined value investing strategy to this select universe of smaller companies will lead to significant long term outperformance. We will continue to use smaller company illiquidity to our clients’ advantage.

We didn’t think that Brexit would win; but it did. This caused some immediate selling of risk assets and the European banking system was hit quite hard. The European financial system has become entwined but amazingly the agreements within the EU on services are not as advanced as on physical trade. Such uncertainty was behind the sell-off.

Brexit – What next for HSBC? Robert Swift – Head of Global Equity Strategies

We didn’t think that Brexit would win; but it did. This caused some immediate selling of risk assets and the European banking system was hit quite hard. The European financial system has become entwined but amazingly the agreements within the EU on services are not as advanced as on physical trade. Such uncertainty was behind the sell-off.

We wrote a piece before the referendum arguing that the UK portfolio of National Grid, Glaxo, and HSBC, was quite well hedged for either result -Remain or Leave. All 3 stocks have outperformed. What happens next for European financials is pretty simple to describe. Neither we, nor anybody else, knows what is going to happen. To an extent this uncertainty accurately describes all investment decisions – you can’t predict the future. All you can do is to analyse the strengths of each business franchise, assess fair values, and diversify the portfolio so that it isn’t hurt by one single event.

Currently there are some concerns that the “passporting” of financial services between the UK and the EU will cease and there will be a costly requirement to set up fully capitalised entities in each of the two areas. We think that a deal will be reached and “armageddon” avoided. Such a deal would see all financial stocks continue to recover.

What we liked, and still like, about HSBC was that its valuation and strategy make it very resilient to external shocks such as the Brexit vote. The odds of a good outcome are in our favour given the bank’s low valuation; departure from peripheral activities, and global franchise. The bank has already announced it may move staff to its Paris office to cope with any regulatory change and we do not see a funding problem for this bank relative to others. The Asian franchise is strong and it is quite likely that value of a strong franchise in a still fast growing Asian region, without the issues the EU and UK face, will be given a favourable reappraisal by the market.

These qualities make the bank both more profitable and provide the flexibility to deal with regulatory changes which is a possibility post Brexit. Since the 23rd June, the date of the referendum , the share price has held up quite well and is now at end June, back, in GBP, to where it was on the day of the referendum.

HSBC is on a P/E of 12; a dividend yield of 7.5% and a Price to Book ratio of 0.7. This compares with the best of Australian Banks, CBA on a P/E of 13; a price to book of 2 and a dividend yield of just over 6% assuming franking credits. If HSBC management can improve the return on their asset base and grow in Asia, then this stock has much further to go.

The fundamental justification for the deal appears reasonable for Microsoft shareholders, however Microsoft has a chequered history of business acquisitions and has paid a very high premium to gain exposure to a social networking channel, albeit one that is more relevant to Microsoft’s main product lineup.

On balance, it could work and there are several reasons I find in favour of the deal. The big problem is however that Microsoft (MSFT) has a poor record with paying too much for acquisitions and then not executing well on the strategy.

Quick summary of the deal:

Microsoft will buy Linkedin in an all-cash deal for USD 26B. Equivalent to $196 per share which is a 50% premium to where Linkedin was trading at prior to the announcement (around $132 per share). This ranks as one of the biggest tech transactions of all time.

The transaction is expected to dilute EPS by about 1% over the next 18 months.

LinkedIn will continue to operate as an independent business and its financials will be reported in Microsoft’s Productivity and Business Processes segment.

Opinion appears evenly divided about the deal. It has the potential to be transformative for Microsoft, but Microsoft has a poor track record with business acquisitions (Nokia, Skype, Yammer). Microsoft’s share price declined around 2.5% after the announcement of the deal.

Microsoft as an ‘old’ technology company has been in transition for a few years in an effort to remain relevant. Its revenues have stagnated for almost three years. It is strategically moving away from software and consumer products and is now primarily a business to business services company. Microsoft’s focus is developing new products and services for businesses and organisations. Microsoft is growing its cloud software division and expanding it into the professional social networking space with this deal. The cloud offerings, Office 365 subscriptions and big data technologies are pulling in more revenue and the profit margins remain high.

Linkedin is similar to Microsoft in that consumers are familiar with the flagship application, but Linkedin’s growth is also based on business to business services. In 2015 Linkedin earned 80% of its revenue from business clients, the majority coming from the growing Talent Solutions segment. Linkedin can benefit from Microsoft’s programming and product development strengths while Microsoft will gain Linkedin’s relationships with a growing list of companies and professionals across the globe. Microsoft CEO Satya Nadella was keen to stress the combined company’s addressable market will increase over 50% following the acquisition. A LinkedIn application integrated into the Microsoft range of products has the potential to improve efficiency, particularly for human resource and CRM functions.

Linkedin’s NOPAT (net operating profit after tax) has declined over the last two years and was -$58M for 2015. Working on Microsoft’s WACC (weighted average cost of capital) of around 8%, the NOPAT of Linkedin needs to increase to around $2.1B to at least not destroy value for Microsoft shareholders. This is a big task to achieve. The fundamental justification for the deal appears reasonable for Microsoft shareholders, however Microsoft has a chequered history of business acquisitions and has paid a very high premium to gain exposure to a social networking channel, albeit one that is more relevant to Microsoft’s main product lineup.

This recent technology transaction highlights the fact that this is not a set and forget market. You constantly need to be reviewing your portfolio and, much like we do in our portfolio committee, constantly re-evaluate your investment thesis for holding a particular position. At the same time, you should be reviewing the various asset classes and investment styles of your investments. We know that asset allocation decisions are equally as important as stock picking decisions.

Can we immunize the portfolio from Brexit or Bremain risk?

Robert Swift – Head of Global Equity Strategies

Much has been written on the referendum on June 23rd when eligible UK citizens will be able to vote on whether to remain in, or begin to negotiate an exit from, the EU. You’ll be glad to know we won’t be making arguments for either choice in this article, and that this article will be brief.

It is a fascinating, and unprecedented, spectacle not least because the protagonists on either side transcend their traditional divisions. There has been much nonsense spouted, but by the Remain side in particular, and it is perhaps some of their insulting and patronising drivel that has caused the outcome to become closer than initially thought? We don’t trust polls but the bookies, who tend to be better predictors, have certainly shortened the odds on a Brexit. Consequently, if markets are sort of efficient, the closeness of the vote predicted by the bookies, should be discounted in the equity markets? Theoretically what only remains as a risk is if the vote is a resounding victory for one side or the other?

We’re not so sure and a narrow victory either way as well a resounding victory either way needs to be considered. While the numbers don’t warrant a big reaction (Total value of ALL trade and services between the UK and the EU accounts for around 1% of global GDP. Nobody for one minute is suggesting this will disappear overnight) there may well be one since markets love to overreact. Since we can’t predict what will happen we need to try and reduce portfolio exposure to a deleterious outcome. We think we can do this without going to cash by selling all UK exposure.

Here is what we have done. We own 3 UK stocks of which only one may be exposed to a shock in the UK economy and changes in interest rates and legislation. Two of the companies we own are multinational businesses, Glaxo, and HSBC which happen to have their main listing in the UK. They could just as easily be listed in New York, Shanghai, or indeed Frankfurt. If Sterling falls on a vote to Brexit they should benefit. Their US$ earnings are substantial so they are also a hedge against Euro risk. On a decision to Remain, they are quite likely to be favoured if investors wish to take on equity risk in a relief rally. Given the UK’s very large twin deficits we don’t think a vote for Remain causes a permanent and painful increase in the value of Sterling. Any such relief rally in Sterling is likely to be short lived.

The ‘pure’ UK company is National Grid which owns regulated electric and gas transmission assets. It also owns assets in the USA which actually comprise about 1/3rd of its asset base but it is overwhelmingly considered a UK company and its shareholders are predominantly UK based.

We find the company attractive because it has a stable and strategically important business, and has a high and growing dividend yield. This is a much better investment option than a UK bond or gilt at current interest rates. National Grid is unlikely to be affected by a close vote or an overwhelming vote either way. The UK is running seriously close to full utilisation in energy; NG is investing, and is being encouraged to invest by the regulator. The dividend yield will become really attractive if the Bank of England has to cut interest rates on a Brexit vote, to boost the economy. On the other hand if there is capital flight and an increase in interest rates to protect the pound Sterling, funding for capex is more likely to be directed TO this company than removed given the UK’s imminent energy shortages.

We believe these kinds of companies are attractive regardless of the outcome on June 23rd. We will be watching and relaxed doing so!