Following on from our previous discussion of income versus capital as a source of portfolio return Scott Maddock and the team at CBG, of the TAMIM Australian Equity Income IMA, look at Lendlease (LLC.ASX).

The Lendlease income opportunity Scott Maddock

LLC is a leading development, construction and investment management business, operating in 9 countries. We believe the company is positively leveraged to global economic activity. Operationally the company has been on a path of continuous improvement since their last major construction losses in 2004. Delivering a strong operational track record, generating 14% ROE. We expect LLC to have net cash within 18 months (5% gearing currently).

The current dividend does not seem high at first glance; however, LLC has a history of paying excess cash to shareholders – notably following the sale of a major Shopping Centre development for $1.3bn in the UK in 2014. We feel LLC will have the opportunity to deliver more cash to shareholders as current projects mature.

The Australian housing cycle is a fixation for most of us and we assume all our readers have a strong view regarding the near-term path of housing prices. We feel it’s clear that as housing construction activity peaks in Sydney and Melbourne this year, that housing prices will also peak. This process is assisted by controls on bank lending – both internal and those imposed by the bank regulator, APRA.

In this context, many would say LLC is a risky investment – and that’s true to an extent – contracting and construction businesses have inherent risks which we do consider. However, the housing cycle is less of a risk than you would think at first glance;

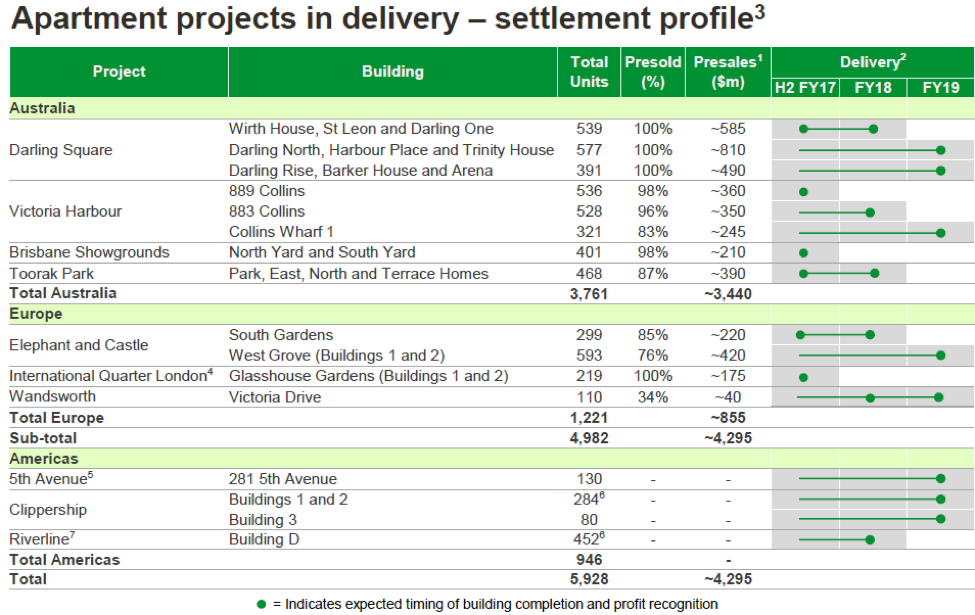

LLC’s exposure to Australian apartment earnings peaks this year at only 20% of group earnings.

Developments are 80-90% (and higher) pre-sold and most purchasers (especially from overseas) are holding a significant unrealised profit. This suggests there will be a low final payment default rate as buildings are completed.

Even during the GFC both LLC and Mirvac Group observed less than a 3% default rate, recently defaults are running at less than 1%.

Lend Lease’s apartment construction business includes projects in the UK and USA, further diversifying the sources of likely cash flow.

In summary, our investment thesis is that LLC has invested ahead of the economic cycle, has significant pre-sold revenue for work in progress, with buyers having paid 10% deposits and sitting on capital gains – therefore significant defaults or losses for LLC are unlikely. We expect that as most projects are finalized during the next twelve months (see table) we will see significant cash generated. Since LLC has relatively low levels of debt, cash should be available to increase dividends or potentially allow a capital return.

Source: Lend Lease company filings

Source: Lend Lease company filings

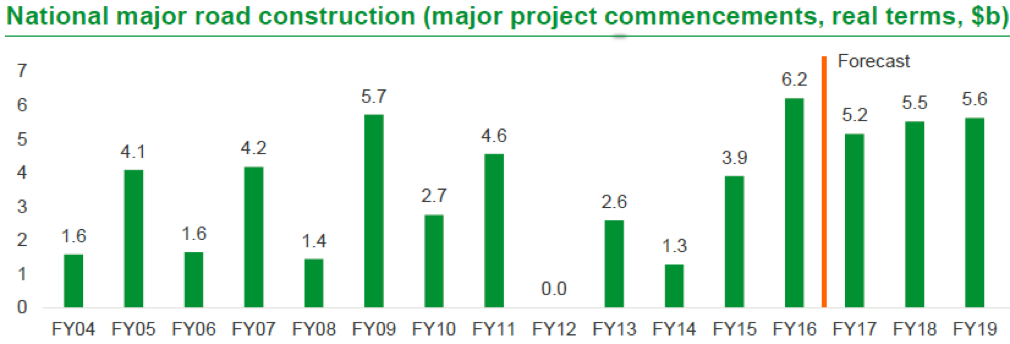

Just as importantly LLC earnings will benefit from growth in construction activity in Australia – particularly in road-building and related infrastructure. The company has also been increasing capital employed offshore. Capital allocated internationally is expected to increase from 23% of total to 30-50% as LLC apply their expertise in Urban Renewal projects around the world.

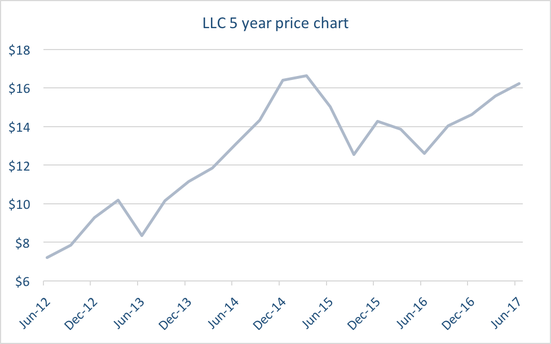

We believe valuation remains attractive vs. history and global peers, on a 12x forward PE vs 17x for similar global listed construction companies. LLC is likely to deliver more cash to shareholders along with a positive share price return.

This week Guy Carson provides a mid-year-update to his 2017 Outlook for the Australian economy. Have things been playing out as expected in the two-speed economy or is there more yet to come?

Mid-year Australian Update – Have we turned the corner? Guy Carson

At the start of the year, in our 2017 Outlook, we wrote about our concerns over the two speed nature of the Australian economy. Our fears seem to be largely playing out through the first quarter as GDP came in at a very soft +0.3% q/q and +1.7% y/y. However, as the year has progressed a few things have surprised us, primarily the strength of the Australian job market and as a result the recent rebound in consumer activity. The strength of the Western Australian job market in particular has been a significant surprise. Given this new information at hand, it seems worthwhile to revisit our views.

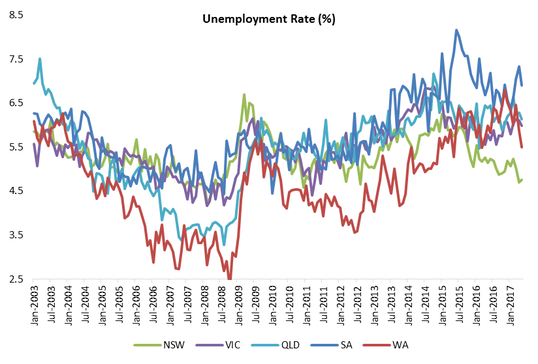

The change of course for the Australian economy seems to have started around March when the employment data took a significant turn for the better. Over the three months starting March we saw employment gains of 60k, 46k and 42k. For a steady unemployment rate a figure of around 15k is needed to keep pace with population growth. As a result the unemployment rate has fallen from 5.9% to 5.5%. The biggest improver somewhat surprisingly has been Western Australia where the unemployment rate has fallen from 6.5% to 5.5%. The other main improver is New South Wales which continues to have the lowest unemployment in the country.

Source: ABS

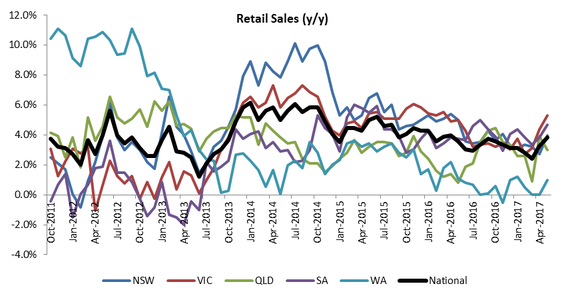

With lower unemployment, we have started to see an improvement in retail sales over the last two months. After a steady decline since 2014, national retail sales have rebounded significantly in the last two months up 1.6%. Western Australian continues to lag the other states but there is some sign of life.

Source: ABS

These are positive turnarounds, more people with jobs leads to increased consumer spending and increased economic activity. Whilst GDP is a near impossible number to predict, we can say the foundations are there for a rebound in the June quarter. Hence the question we get is have we turned the corner? Are we out of the woods yet again?

At this point, we are not confident that these positive signs will be maintained. Yes, near term economic signals are positive but for us three key structural challenges remain. These challenges are:

Record low wage growth.

Record high household debt.

An unprecedented building boom that appears to be softening.

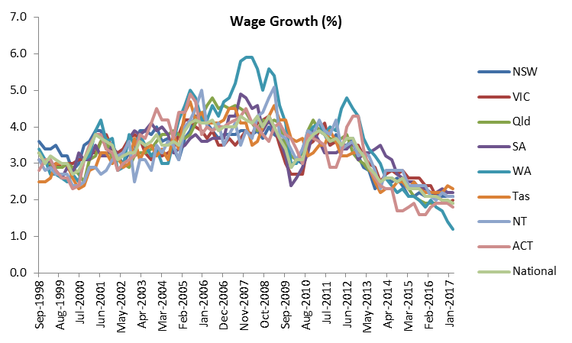

Despite the strength in the labour market over the last three months, we are yet to see signs of wage pressures. In fact wage growth has declined steadily in Australia since 2012 and is currently running at its lowest level on record at 1.9% year on year. During this period we did see a significant decline in unemployment in 2015 but even this did little to stop the wage trend. The current bounce in the employment numbers would therefore, in our opinion, need to last significantly longer to have an impact.

Source: ABS

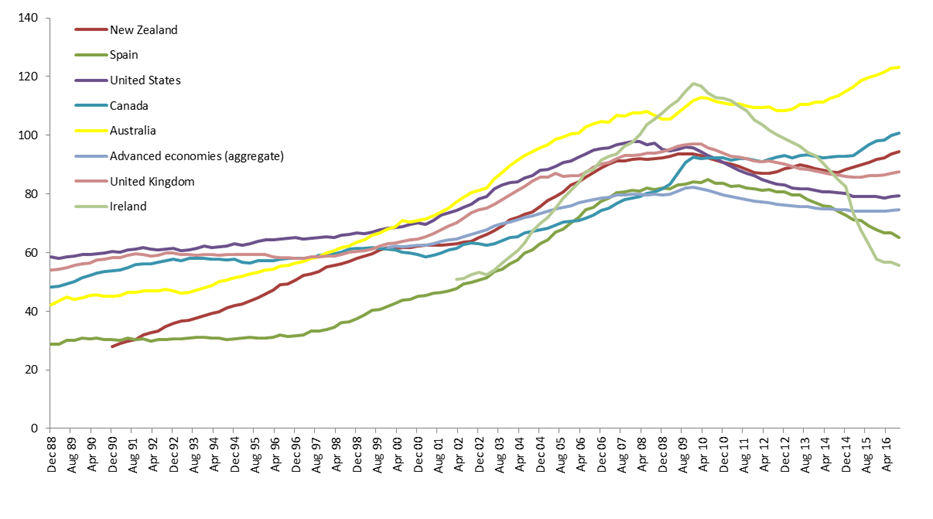

Low wage growth is a major problem. This is particularly true when combined with record household debt. Recently the cost of that debt has started to rise. Due to the intervention of regulators, the banks have announced significant interest rate hikes for interest only loans (due to come into effect this month). The intention of these hikes is to get property investors to switch from interest only to principal and interest. The net effect will be slightly increased total payments. A small increase on a large amount can have a big impact and, as we have written about previously, Australian household debt to GDP levels are currently the second highest in the world (according to the Bank of International Settlements) and above the peak that the likes of Ireland and Spain saw before the GFC.

Source: Bank of International Settlements

A majority of this debt sits against residential property which has been a key driver of the Australian economy in recent years. In response to the end of the mining construction boom, the RBA began to cut interest rates in 2011. All up they have cut rates from 4.75% to 1.50% and have seen off a recession we most likely would have had otherwise.

The interest rate cuts have enabled households to borrow more. In turn this has led to house price increases and higher house prices have led to greater incentive to build. The residential construction industry has as a result boomed, primarily across the East Coast and primarily in apartments. The RBA has effectively replaced a mining boom with a property boom.

There is a considerable amount of research around about the impact of residential construction booms. The Bank of International Settlements has warned against cutting interest rates to boost asset prices and the consequences that it can have. Regular readers of ours will also know about Edward E. Leamer’s paper “Housing IS the business cycle” where he paints residential construction as the major cause of economic recessions. One of the key points that Leamer makes is that “house prices are very inflexible downward, and when demand softens as it has in 2005 and 2006 [in the US], we get very little price adjustment but a huge volume drop. For GDP and for employment, it’s the volume that matters.“ So whilst most of the commentary and focus remains on Sydney and Melbourne house prices, we would suggest that people need to be more focused on the volume and here we are starting to see potential signs of a decline in construction activity.

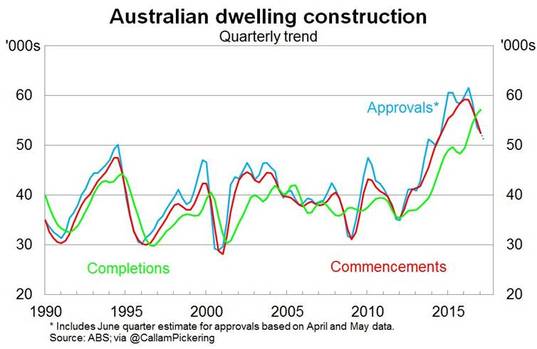

The chart below looks at residential building approvals, commencements and completions on a national level. From this data we can see that building approvals act as an excellent indicator of building activity and they are showing signs of rolling over. If we were to see a continued decline in approvals from here we will start to get very nervous. Typically commencements follow approvals closely and completions tend to peak 6-9 months thereafter.

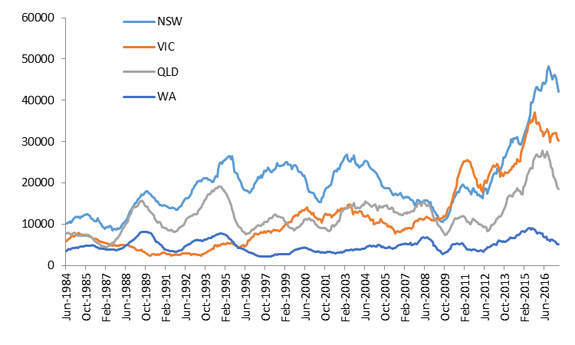

Whilst the decline is a on a national level, there are certain areas that are leading the fall. The below chart looks at apartment approvals on a rolling annual basis. There are two interesting things to note. Firstly all of the four states that experienced booms are off their peaks, and secondly there is real pain set to come for apartment developers in Queensland.

Source: ABS

With the residential construction boom potentially coming to an end, there will be a growth hole to fill. The RBA cut interest rates by 3.25% to fill the hole from the mining boom, but now with interest rates at 1.5% they have significantly less fire power. Which begs the question of how the RBA would deal with a prolonged slowdown?

The counter argument to our assessment of the residential boom is that due to record immigration levels, current building levels are rational and must be maintained. We take a slightly different view and would suggest that immigration may have a component that is pro-cyclical, i.e. people will move to where there is work. On that basis, it’s the building work drawing people here and not the people moving here that is forcing the building work. On this point we would highlight that Iceland, Ireland and Spain all had record immigration in 2007 and we probably don’t need to remind people what happened in 2008. For Australia, whilst immigration has remained high over the last decade or so, there are three clear surges. These surges occur with both stages of the mining boom (pre GFC and post) as well as the recent residential construction boom.

In summary, the last few months has seen renewed energy from the Australian consumer and that could provide some short term relief to sectors such as retail and financials. However, when we invest we take a longer term view and believe the risks to the downside outweigh the upside for these sectors. As a result, we continue to focus our efforts on finding companies with structural tailwinds, global earnings and strong value propositions. These companies should be able to grow and prosper despite an uncertain domestic economic environment.

Robert Swift provides an update on his stance on asset allocation having just ticked over into the new financial year.

An update from our asset allocation models.

One of the most important decisions is how to allocate your money across different asset classes – property, bonds, equities, or cash. This is because a combination of these assets will be less volatile than simply holding equities, and the returns, although lower, will be safer and reduce the chances of a nasty surprise to your pension pot.

Summer in the Northern hemisphere often brings with it dull markets – the “sell in May and go away” expression is routinely trotted out for a good reason! Fewer investors at work, fewer company announcements and a long break for politicians, makes for a lack of news flow.

In the absence of news, markets tend to drift lower. Will it be the same this year?

We first wrote on asset allocation four months ago and thought it was time to revisit the landscape using our asset allocation models.

Our conclusions then were: Equities – overweight especially Value Bonds – underweight especially net debtor countries such as Australia, Turkey, Spain Property – residential is overpriced and liable to be taxed by governments keen to spend more of your money. Be careful of yield hunting.

How did we do?

We did ok and you would have made money following the recommendation.

Most European equity markets have drifted a little over the last month, after a strong few months, but the US has continued upwards, as has Japan and a number of Emerging markets like China. We have held a strong Value bias in equities for a few months now and have been wrong in this regard.

Growth styles, and the ‘sexy six’ have performed exceptionally well. We aren’t changing our view on this and still recommend a Value tilt in an overweight equities position.

Our Tactical Asset Allocation model continues to like equities overall, and still prefers them to Bonds.

Other asset classes to consider currently are:

Overweight Equities

Prefer Value style, with dividends and high free cashflow yield

Prefer Financials, Cheap Tech, Telecoms

Underweight Advanced Economy Government bonds.

Equal weight Emerging Market bonds (China, Asian & Middle East issuers) but avoid South Africa & Brazil

Underweight commodities especially oil

Underweight residential property (including Australian banks). Prefer industrial and retail in Asia

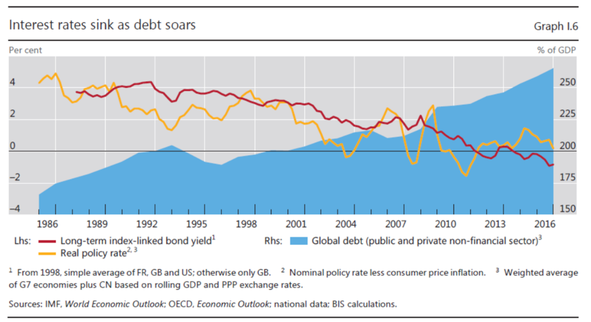

Given the inexorable rise in debt (see the chart above) over the last decade, and the decline in interest payable on it, as a consequence of central bank intervention in fixed income markets, the question you have to ask yourself with bonds is: – “Why should I lend money to governments at 2-3% when there is so much debt already outstanding?”

We wouldn’t! We might at 6%.

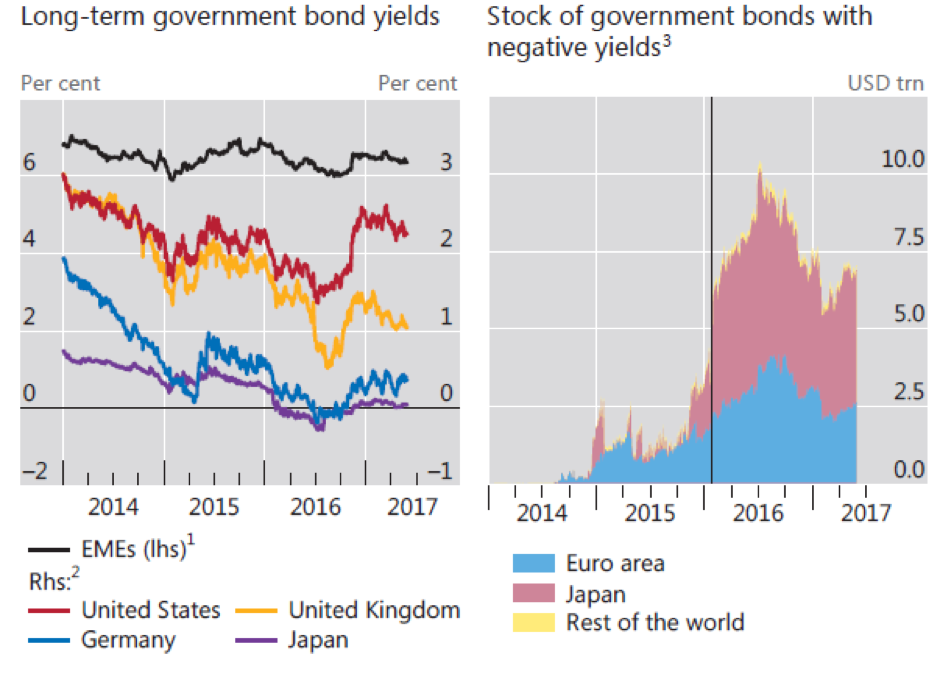

Looking at the charts below it appears to us that the only value in bond markets is to be found in certain emerging market bonds. These are bonds issued by net creditor emerging market countries and they still offer returns of 5-6% (LH Scale on left chart) which is a reasonable return. Avoid bonds with negative yields and those issued by governments which are heavily indebted already. (Right Hand chart)

Central bankers and politicians are the greatest larcenists of all time and will use inflation to erode your purchasing power. The chart above tracks cumulative inflation over the last 100+ years. Most has occurred since the rapid issuance of government debt for ‘welfare states’ and the constant temptation to monetise this and reduce the liabilities aka your savings!

Inflation hurts bonds more than equities where companies can, usually, pass on cost price increases and whose asset values rise in line with inflation.

Near term risks and what to watch

Purchasing Managers Indices – widely followed data as an indication of near term economic activity – have recently showed slowing activity. If this continues over the Summer this may see medium and long term interest rates move down and bond prices move up.

After a good first half of the year we may well see some pause or setback in equities, but they continue to be the preferred major asset class for now, given that we are currently in a broad synchronised global upswing in global economic activity.

Within equities, across the regions we continue to prefer Europe which is exhibiting its best growth since the financial crisis in 2008. Emerging markets are also now looking attractive both in terms of valuation and price action. The USA is the market where we continue to struggle to find value in stocks. The rally there has been very narrow there in the top hot tech stocks – Apple, Facebook, Google, Amazon – when you strip those out – the US market advance has not been widespread.

From the chart above you can see that Value stock returns have fallen relative to Growth stocks.

Value stocks have been disappointing for sure this year but we continue to believe that the focus on just a few big stocks in major indices has been excessive. Meanwhile some very good companies such as Daimler, Glaxo SmithKline, China Mobile, Legal & General, JP Morgan, Itochu are on modest PE ratings and with dividend yields in excess of 4%, will find favour.

The market may be a voting machine in the short run, but it’s a weighing machine in the long run. Now is the time to favour companies paying sustainable dividends, with asset backing. Now is the time to ensure your portfolio is set to take advantage of these coming market changes!

Robert Swift talks about how the TAMIM Global Equity High Conviction IMA is positioned heading into the Brexit vote and in particular reviews our 3 London listed investments.

Can we immunize the portfolio from Brexit or Bremain risk? Robert Swift – Head of Global Equity Strategies

Much has been written on the referendum on June 23rd when eligible UK citizens will be able to vote on whether to remain in, or begin to negotiate an exit from, the EU. You’ll be glad to know we won’t be making arguments for either choice in this article, and that this article will be brief.

It is a fascinating, and unprecedented, spectacle not least because the protagonists on either side transcend their traditional divisions. There has been much nonsense spouted, but by the Remain side in particular, and it is perhaps some of their insulting and patronising drivel that has caused the outcome to become closer than initially thought? We don’t trust polls but the bookies, who tend to be better predictors, have certainly shortened the odds on a Brexit. Consequently, if markets are sort of efficient, the closeness of the vote predicted by the bookies, should be discounted in the equity markets? Theoretically what only remains as a risk is if the vote is a resounding victory for one side or the other?

We’re not so sure and a narrow victory either way as well a resounding victory either way needs to be considered. While the numbers don’t warrant a big reaction (Total value of ALL trade and services between the UK and the EU accounts for around 1% of global GDP. Nobody for one minute is suggesting this will disappear overnight) there may well be one since markets love to overreact. Since we can’t predict what will happen we need to try and reduce portfolio exposure to a deleterious outcome. We think we can do this without going to cash by selling all UK exposure.

Here is what we have done. We own 3 UK stocks of which only one may be exposed to a shock in the UK economy and changes in interest rates and legislation. Two of the companies we own are multinational businesses, Glaxo, and HSBC which happen to have their main listing in the UK. They could just as easily be listed in New York, Shanghai, or indeed Frankfurt. If Sterling falls on a vote to Brexit they should benefit. Their US$ earnings are substantial so they are also a hedge against Euro risk. On a decision to Remain, they are quite likely to be favoured if investors wish to take on equity risk in a relief rally. Given the UK’s very large twin deficits we don’t think a vote for Remain causes a permanent and painful increase in the value of Sterling. Any such relief rally in Sterling is likely to be short lived.

The ‘pure’ UK company is National Grid which owns regulated electric and gas transmission assets. It also owns assets in the USA which actually comprise about 1/3rd of its asset base but it is overwhelmingly considered a UK company and its shareholders are predominantly UK based.

We find the company attractive because it has a stable and strategically important business, and has a high and growing dividend yield. This is a much better investment option than a UK bond or gilt at current interest rates. National Grid is unlikely to be affected by a close vote or an overwhelming vote either way. The UK is running seriously close to full utilisation in energy; NG is investing, and is being encouraged to invest by the regulator. The dividend yield will become really attractive if the Bank of England has to cut interest rates on a Brexit vote, to boost the economy. On the other hand if there is capital flight and an increase in interest rates to protect the pound Sterling, funding for capex is more likely to be directed TO this company than removed given the UK’s imminent energy shortages.

We believe these kinds of companies are attractive regardless of the outcome on June 23rd. We will be watching and relaxed doing so!

Robert Swift weighs in on the active vs. passive management debate and questions the risk levels in so-called passive strategies.

How much risk is there in my passive strategy? Robert Swift

Investment strategies, where investors simply invest in a fund that tracks a standard index like the S&P/ASX 200, have become increasingly popular both with institutions and private investors.

The reasons are clear – they are cheaper than most active strategies, people feel they know what they are buying and often the relevant target strategy can be hard for active managers to beat.

Not all is what it seems. This article will seek to demystify some of the hype surrounding these “passive” strategies and to highlight that while they are “passive”, it does not mean that they are without risk of disappointment.

It is important to first understand that they are typically based on the market value of companies. The largest companies in the index are the largest ones in the portfolio. This means you can end up investing proportionately more in the largest market capitalisation and most expensive companies and can potentially also have larger exposure to industries that than is reflected in the real economy. Reduced to its simplest a market capitalisation strategy simply keeps investing in the biggest companies regardless of their valuation. At some point this valuation may become too stretched and therefore dangerous to keep investing. A passive strategy will not care about the valuation of the largest companies but merely keep investing any subscriptions. Consequently, they may be anything but “calm and safe” as the word passive may imply?

The actual volatility, or the price swings, of an index fund may be very high especially if it has high weightings in just a few stocks. For instance, at 31/5/2017 the 20 largest companies in the ASX300 represents 54% of the index market capitalisation. If the largest companies share common business models and an event occurs, then the share prices of all will move together. We highlighted recently the similarity of the Australian banks and how their share prices moved together more than any other bank sector.

Passive or “index” funds have also been shown to underperform certain investment styles like Value or Growth or “Quality”– where an active fund may focus on lowly valued companies or high growth companies. Investment managers have attempted to replicate exposure to these investment styles through what are commonly known as “Smart Beta” funds. These are becoming increasingly sourced through Exchange Traded Funds (ETFs).

While they appear to be better than simple market capitalisation weighted index approaches, they also contain risks of which investors should be aware. To keep costs down and to pass the test of being an ETF the “investment rules” that define these style portfolios are often very crude and simplistic. Using low Price to Book value ratios to select the preferred stocks in the ETF, for example, will give a Value tilt but the tilt will come without any regard to the risk of the aggregate positions. The crucial difference between an index or “smart Beta” passive approach and a portfolio is that the portfolio should be designed to maximise return while managing the risk. The standard “smart Beta” indices do not manage the risk of the $ invested but only select stocks in weights which reflect their style exposure. “Smart Beta” makes dumb portfolios.

We can explain this with an analogy. We use the analogy of shopping for food in a supermarket. Let’s say that you have to shop for food to prepare dinner. You know what dinner should look like – a sensible mix of the food groups. This sensible mix we can call a portfolio. It is optimal like a portfolio in that it will meet a number of criteria not just meet a certain tilt to price. A “smart Beta” approach to shopping for dinner would be to look for the ingredients on the basis of price. A certain $ budget would be allocated and the shopping basket (or stocks) would be selected only on the basis of price to weight of tin or price to quantity of food. You would get some ingredients that are specifically suitable for your dinner menu, but it would not be exactly what you want. A portfolio management approach would use price as an input BUT ALSO try to optimise the ratio between price paid and the amount of the specific food item to make up the dinner ingredients. The portfolio management shopper would perhaps pay up for an ingredient that was essential to diversify the other items on the menu? The portfolio management shopper should look to get a more appropriate mix of the ingredients in the basket and care about price AND relative weights to make dinner.

Like so many things in life, there is always a risk when things get too popular and so much money pours into particular strategies. Those stocks that are in indices, be they simple market cap weight indices or a crude Value or Growth fund can get pushed up too far due to the sheer weight of money going in to them, whilst those stocks lowly considered or outside these indexes or style benchmarks can become neglected and potentially undervalued. These neglected stocks may potentially be more attractive investments going forward as is the case now – we believe.

For example, in the USA this year there has been a big focus on Growth / Momentum stocks which has meant most of the market rise can be accounted for by the movement of just a few stocks – Facebook, Amazon, Apple, Alphabet (formerly known as Google) and Netflix. The last time we saw this kind of rise was in 1999 in the USA Tech bubble.

Many of these Smart Beta strategies are currently perceived to be the new “holy grail” of investment management. The limitations of these investment approaches may only become truly apparent after the event. We have only to think back to the Tech boom bubble in the late 1990s and the ultimate bust of so many dot com companies in the fall out of 2000-2 to see the dangers of fashions in investing.

So, the advice is to look behind the shiny wrappers and bold claims and try to see how intelligently these strategies have been put together. What empirical evidence there is to support these approaches, and whether these trends are likely to continue?

Importantly, it is important to understand how the strategies operate and not get caught up in purely mechanical and computer driven investment approaches just because their current performance is good. Recognise that all investment decisions involve judgement and experienced people are required to manage a portfolio, not just a set of rules.

We like to use two famous quotations when we describe our process which seeks to use quantitative or computer driven models but only with a human being in charge.

“Not everything that can be counted counts; and not everything that counts can be counted”

“I would rather be approximately right than precisely wrong”