Robert Swift takes a look at the sideshow that is North Korea. We do not believe that North Korea impacts global economic fundamentals and that any short term dips that it may create in markets are good opportunities for us to purchase assets we would like to hold over the long term.

North Korea – “Buy on the cannons; sell on the trumpets” Robert Swift

The saying was attributed to Nathan Rothschild from 1810 when Europe was plagued by periodic outbreaks of war which obviously needed financing, and which might end in change of government or, catastrophically, an invasion by foreign power and confiscation of assets. The anticipation of this turmoil led to falls in bond and equity prices which offered an opportunity to invest at cheaper prices. Fortunes are typically made by buying on dips when others panic.

Source: Wall Street Journal

With all eyes on North Korea and growing tension in the region is this such a time? Is the current selling, particularly in Asia, offering a chance to repeat Rothschild’s success?

It is hard to argue that equities are in ‘bargain basement’ territory – or at least that USA equities are. Over the last several years they have risen substantially and depending on the definition of the earnings number you use trade between 18 and 22 x next year’s earnings.

Source: Thomson Reuters Datastream

On the other hand earnings volatility has been reduced and is likely to remain low, and it is unlikely that 10 year Treasury Note yields, from which we can estimate the fair price of equities, will go much above 3%. (They are currently just over 2%) Both of these help underpin USA equities at current levels and make selling frenzies attractive entry points.

So while not bargain basement they aren’t a bubble either. Looking at the average PE is misleading anyway in such a diverse universe of stocks. It’s a bit like saying “if I put my head in the oven and my feet in the fridge, then on average I’m comfortable”. It’s nonsense. Focus on stocks and try to pick those whose prospects are strong but whose share prices have fallen to where PE multiples are reasonable.

How can we be so sanguine?

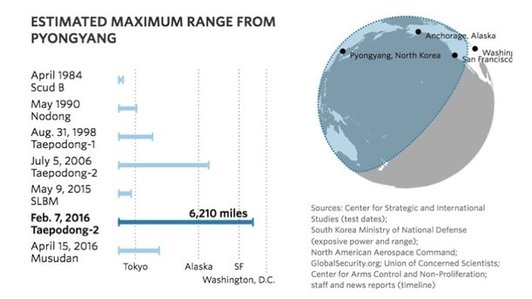

North Korea is a side show and has done this shakedown before. Once it gets paid out then tensions ease.

Trump might refuse to payout on such a shakedown, unlike past Presidents, and make bellicose gestures, but he has shown more restraint than expected.

This tension gives him a chance to backtrack on his ‘abandonment of the region’ which should do wonders for its long term prosperity and stability.

We can tell you from our connections in the USA that there is so much firepower trained on North Korea that it will be cinders in a second should it do something stupid. They aren’t stupid. Part of the opportunity to ramp up tension was created by the political corruption scandal currently engulfing the South and a perceived subsequent political vacuum. Clever stuff by the North in one respect?

A much more interesting line of conjecture is what should you do as investors if North Korea re-engages with the South as East and West Germany did in 1990. We won’t do that here but can suggest unification would cost South Korea a lot more than it cost West Germany. Japan would also need to reconsider its source of unofficial cheap labour.

In what should you invest?

Meanwhile back in the real world, certain USA financials we like have mostly reported good earnings and indicate stability ahead. JP Morgan beat (carefully massaged) expectations and with plenty of risk capital buffers is now starting to reduce risky loans.

Another financial stock we like, AFLAC, trades on a PE multiple of 11.5 and grows slowly but steadily in the USA and Japan by selling policies to supplement health and medical care and loss of income protection.

Part of our investment thesis for USA financials is that they are not the beasts of 2002 – 2008 and have much more control over what loans are being made, and are much more closely supervised. If anything, the problem is in hitting growth targets which was the root cause of the Wells Fargo accounts fabrication scandal? The next crisis won’t be caused by financial stocks.

Directly in the ‘firing line’ in Asia is another cheap financial stock Sumitomo Mitsui Financial Group which trades on a PE of just over 9x. It has fallen about 10% in the last month and represents an attractive entry point now. Those of you who have been to our seminars or read anything we publish will know that Japan is not the economic basket case that the conventional wisdom would have you believe. The economy won’t implode and there is lots of innovation.

Now is not the time to reduce equity risk. If you are heavily invested in Australian equities then try to become more diversified. Be wary of the financial sector here which although not badly managed represents a single exposure to residential real estate. More legislation is likely which will reduce the potential for growth of that loan book and then where is the growth going to come from? Not overseas where NAB and ANZ have conspicuously failed and are now withdrawing, nor from investment banking. It won’t take much of a PE derating to make the franked dividends look a forlorn reason to own so much of the Australian financial sector.

This week Guy Carson takes a look at the Australian banking sector, how it generates profit, how this has operated historically and what the outlook is going forward. Guy argues that the tailwinds aiding bank profitability over the last 25 years may be coming to an end.

Australian Banks: The death of a 25 year bull market

Guy Carson

In the early days of May, ANZ, Westpac and NAB will all report their first half results. Short-termism will grip the market and the focus will be on whether earnings from the October to March period are above or below expectations. This will undoubtedly swing share prices a few percent in the appropriate direction and as a result lead to under or out performance for fund managers relative to the Australian index. Now if I was a betting man, I would probably say the odds are in favour of a “beat”. This is based on the evidence from CBA’s recent result that showed an easing of credit conditions in the corporate sector combined with the APRA data showing the banks continue to grow their investor mortgage book (at least until last month). However, when investing it is the not the last six months that will determine your success or failure. It is important to take a longer term view of the companies and the economic drivers that will drive the performance over coming years.

In order to understand this, we have a look at two areas:

A bottom up analysis of how the banks have performed over the last 25 years.

A top down analysis of what the drivers have been that have led to that performance and how likely they are to continue.

Bottom up analysis – How the banks have performed

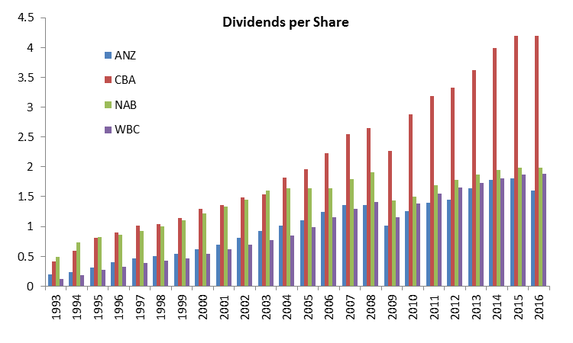

The banks are mainstays in most Australian equity investor’s portfolios and with good reason. They have been remarkable investments. Commonwealth Bank listed in 1991 at $5.40 per share. The price currently sits at around $85 and the company has paid plenty of dividends along the way. Dividends for the Big Four banks are a major attraction and have grown fairly consistently over recent history with one minor hiccup in 2009.

Source: Company filings, Thomson Reuters

By any measure an investment in CBA has been incredibly successful. To understand why it has been it’s worth stepping back and looking at how a bank makes money. This can be broadly defined as follows:

Raise capital to support business.

Borrow funds (liabilities) typically at a ratio of up to 20 times capital.

Lend borrowed funds to borrowers (assets).

The interest earned less interest paid creates the interest margin (net interest).

Charge fees (non-interest income).

Non-interest costs divided by net interest plus non-interest income is the cost to income ratio.

Provisions for potential and possible problem loans are charged against the profit.

Profit after provisions divided by capital gives return on equity.

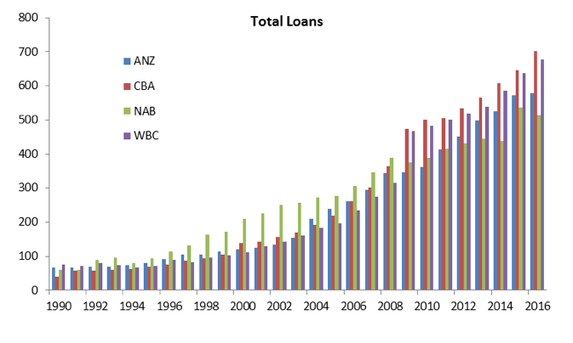

Any objective analysis of the above for the Big Four banks over recent history suggests they have done a good job. Starting with point number 3 above, all of the Big Four have used their balance sheet to good effect and grown their loan book significantly. The below chart looks at total loans (chart is in billions).

Source: Company filings, Thomson Reuters

The four banks as a whole have grown their loan books from $242bn in 1990 to almost $2.5tn today. That is a 10 fold increase with CBA leading the way going from last to first.

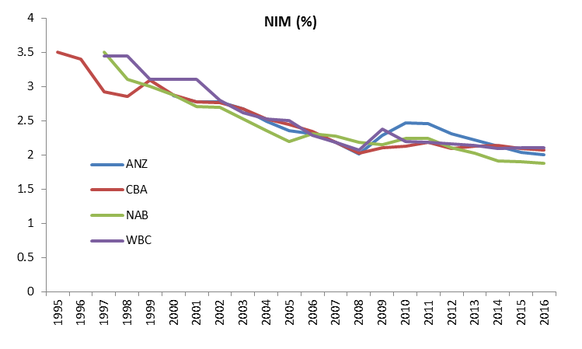

So they have had no problems growing their book. Moving onto point 4 and the Net Interest Margin (NIM) which has gone the other way.

Source: Company filings, Thomson Reuters

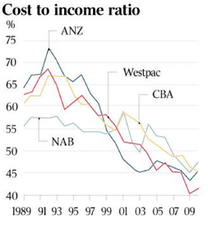

Net Interest Margins have fallen from around 3.5% in the mid-1990s to 2% today. Now there are a lot of explanations for why this has happened but one of the key ones in our opinion is technology. Technology has brought down the cost to income ratio for banks by allowing them to work more efficiently with less staff concentration. The below chart shows this with cost to income ratios dropping from above 60% in the early 1990s to around 40% today.

Source: The Australian, CLSA

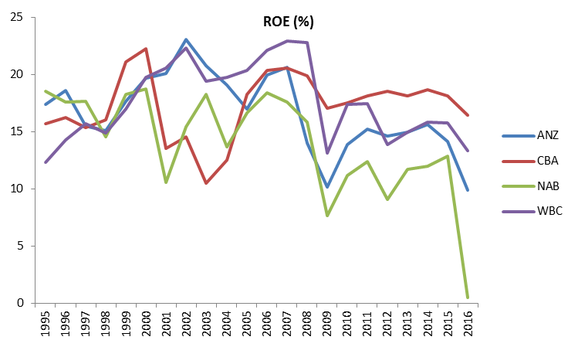

The lower cost to income ratios have allowed the banks to reduce their NIM and maintain profitability. Return on Equity (ROE) for the last 20 years has been consistently in the mid to high teens. You would be hard pressed to find this consistency in any other banking system around the world.

Source: Thomson Reuters

All in all, this track record is impressive and as a result the shares have been great investments. Although one aspect of the above chart does give some slight concern for the future and this is the dip in the ROEs over the last year driven by regulatory changes. We’ll cover this in the next section.

Top Down analysis – What has driven this performance and will it continue?

From the above analysis, one might come to the conclusion that Australian has a strong banking system that has been well run in recent history. However it is important to realise that banks are highly leveraged cyclical companies, when the economic tailwinds are behind them it is easy to look good. When things turn, the real test will begin. This is a point that many Australian fund managers seem to have forgotten in recent times due to the long term success of the domestic banks.

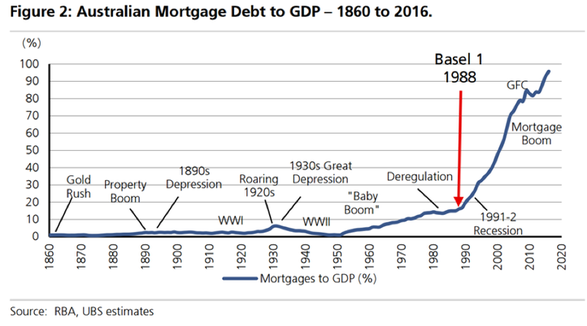

In order to understand why the banks have been so successful in recent times it’s important to examine the economic drivers behind the performance. This begins with a trip back to the 1980’s which saw a significant amount of deregulation for banks and the beginning of the Basel capital requirements. This decade saw the beginning of a debt supercycle globally which imploded in many developed countries in 2007. Prior to 1980, the global standard for banks was a leverage ratio of 7x, this has changed dramatically since. Just prior to the Global Financial Crisis, leverage in the European Banking system stood at 40x, in the US it stood around 30x and in Australia it stood at over 20x. Australia joined the rest of the world in “gearing up”.

The original Basel accord in 1988 looked at minimum capital levels and the risk weightings of different types of loans. For residential mortgages, risk weights were set at 50%, hence banks had to carry half as much equity against them and could in effect leverage their balance sheet twice as much. This helped kickstart a boom in Australia.

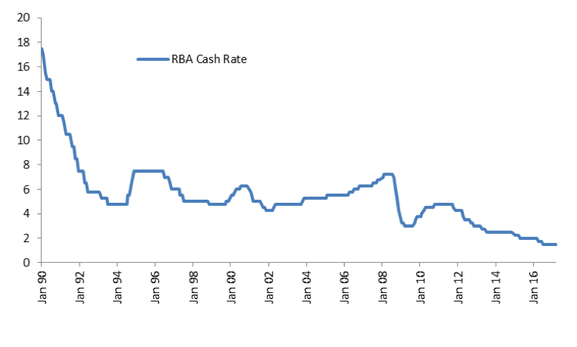

Adding to this was a falling interest rate environment. Interest rates over the last 27 years have gone from 17.5% to 1.5%. Amazingly over that period, Australia has barely been through a tightening cycle.

Source: RBA

Basel 2 in 2007 has added a further tailwind with the banks effectively allowed to set their risk weights through their internal risk models. The banks moved to a 17% risk weighting for residential mortgages. Given an 8% minimum tier one capital ratio from APRA, this allowed banks to leverage their equity 83x. A 17% risk weight means they only have to hold 17% of the 8% minimum capital requirement. In other words for $1 of equity, a bank could lend out a staggering $83 in residential mortgages.

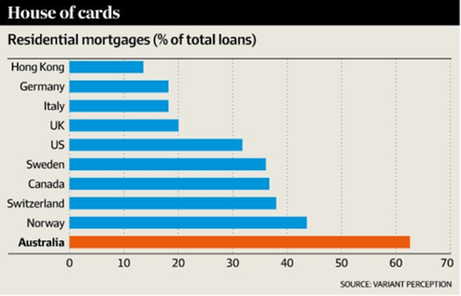

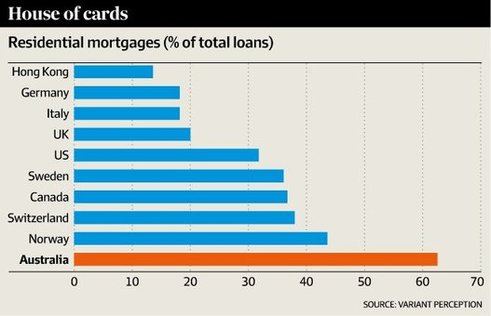

The impact of lower interest rates and favourable risk weightings has meant that our banks have in effect become rather large building societies. Australian banks have a disproportionate amount in residential mortgages when compared with international peers.

Source: AFR, Variant Perception

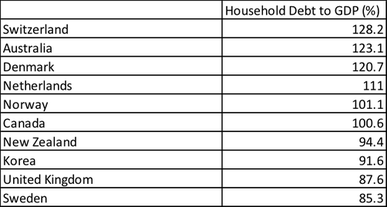

In becoming building societies the banks have driven household debt up. Australia now sits in 2nd place globally with regards to household debt to GDP.

Source: Bank of International Settlements

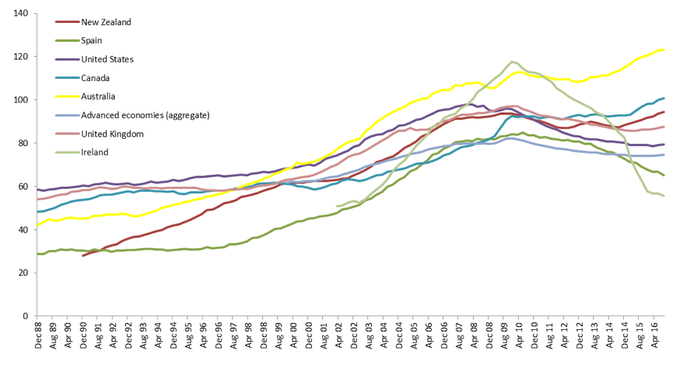

Comparing our journey to some other significant countries, you can see one major difference. In the period post 2007, all of these other nations have been through “deleveraging cycles” and household debt at some point has fallen (with the exception of Canada, an economy similar to Australia with a large exposure to the resource sector and commodity markets). Australian households never deleveraged and have in fact taken on more debt. Household debt has risen from 40% of GDP back in 1990 to 123% today.

Source: Bank of International Settlements

The problem for banks now is that the two key drivers that lead to this growth in the mortgage book and household debt are either exhausted or reversing.

Interest rates are sufficiently close to zero that further scope for lending growth from rate cuts is limited. It also suggests that the capacity of households to take on more debt is limited. Hence for the banks it will be a struggle to grow their loan books.

After a long period of supportive regulatory changes, the tailwinds have reversed. APRA moved back in 2015 to shift the risk weighting associated with residential mortgages from 17% to 25%. This means that the banks have to hold more equity against their current loan books (they can now only leverage their equity a meagre 50x as opposed to 83x). The impact of this was that slight drop in ROE seen above. APRA now has indicated there are further changes to risk weightings coming and these set to be announced “around the middle of the year”.

Conclusions:

Investing is all about probabilities. The value of a share is the sum of its future cashflows. The future however is unknown. Therefore, when establishing what a company is worth or how much certain shares will return we need to look at a range of circumstances to understand the potential upside and downside scenarios.

For the banks, we know that loan growth going forward will be constrained. The best scenario is a likely flat lining of the household debt to GDP ratio over the coming years. In that instance, earnings will grow at roughly the level of nominal GDP which has averaged 3.3% over the last 5 years. Add to that a dividend yield of around 5% and some franking and you get a return of around 10%, a perfectly reasonable outcome for a low interest rate environment. The problem is this is the best expected outcome (outside of a surge in GDP growth that seems unlikely), and it doesn’t even include the likelihood of higher capital requirements from APRA.

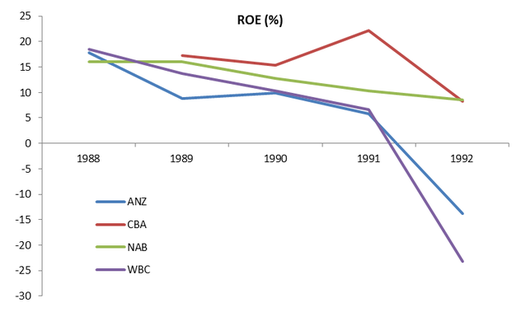

What about the other side of the equation? Well, high household debt doesn’t cause a problem on its own but it does make our economy and our banks vulnerable to a shock. The last time we had a shock two of the Big Four recorded significant losses. In fact, Westpac managed to destroy 23% of their equity in one year. A loss that large will lead to a significant rerating in the Price to Book multiple meaning the loss for shareholders would be considerably more than the 23%.

Source: Company filings, Thomson Reuters

So what could lead to a potential shock? There are three potential catalysts:

Higher Interest Rates. There is a very low probability of interest rate rises anytime soon and in our opinion there is a very low probability of any meaningful tightening cycle in Australia over the next decade. The RBA is effectively hamstrung by the high level of household debt, a problem which they have largely brought on themselves. Although we have to note, a consequence of the stricter capital limits and the rising rates of the US Federal Reserve has led to “out of cycle” rate hikes from Australian banks.

Higher unemployment. Recent job numbers have shown a deterioration in the employment picture most notably in Queensland and Western Australia (something we wrote about in our 2017 Outlook). We do expect this to cause some problems for the banks over the coming 12-18 months.

Low wage growth. Low wage growth makes it more difficult to service debt and currently wage growth in this country is at a record low.

Ultimately, when we assess the outlook for banks we arrive at a conclusion that asymmetric risks exist with limited upside but significant downside. When we look for companies to invest in we want the opposite, limited downside with large potential upside. As a result we continue to avoid the banks, believing that the 25 year bull market has come to an end. The only question that remains for us is whether this bull market ends with a bang or a whimper.

Robert Swift presents 4 short videos on the impact of the withdrawal from Zero Interest Rate Policies on financial stocks, infrastructure, geographic segments and asset allocation. As global central backs commence the process of normalising rates we will see the investment landscape change, Robert provides his thoughts on how best to navigate global investment markets.

This week Guy Carson, manager of the TAMIM Australian Equity All Cap Value IMA, takes a look at the recent RBA decision to yet again leave rates as they are. Have they made the right call? Should they have made a change?

The RBA’s Conundrum Guy Carson

Earlier this week the RBA remained on hold for the 7th consecutive month. However, when we look at economists’ forecasts for the remainder of the year there is significant divergence. Some believe that the economy needs further stimulus whilst others believe we are through the worst and will eventually follow the US Federal Reserve in raising rates. The interesting thing is that both cases have some merit when looking at the overall data and it’s only when we delve down to a state level that we can really understand why.

Firstly, let’s examine the rational for a rate cut. The RBA has a dual mandate to maintain full employment and the stability of the currency. The stability of the currency is seen as achieving an inflation target of 2-3%. As can be seen from the chart below, the Consumer Price Index fell below this targeted band in June 2015 and has remained there ever since.

Source: ABS

So currently the RBA is not achieving its price stability target. What about full employment? After seeing the unemployment rate improve from 2015 through to mid last year, we are now starting to see job growth slow. In fact the unemployment rate since the last RBA cut in August last year has gone from 5.7% to 5.9%, which isn’t exactly what they would have wanted. In addition the underlying quality of the jobs created in recent times has been poor with a large shift towards part-time employment meaning that underemployment has risen as well:

Source: ABS

Adding to this weak employment picture, wage growth is at record lows and this indicates that plenty of “slack” remains in the labour force. The Wage Price Index (WPI) is currently running at 1.9% year on year and has fallen steadily since 2012:

Source: ABS

It’s not until you look under the headline unemployment rate that you will notice some significant divergence in trends between states:

Source: ABS

If we look at the period of improvement in the unemployment rate from 2015 through to mid last year, it was largely driven by New South Wales and Victoria (as well as South Australia improving from a very high level). New South Wales currently has the lowest unemployment rate in the country at 5.2% which is near recent lows. Victoria has seen its unemployment rate tick up slightly to 6.1% but this is slightly misleading given the state has been the primary driver of job growth in the last year. The below chart looks at net jobs growth in each state over the last year and Victoria has represented a staggering 98% of the Australian total. The unemployment rate in the state has been impacted by high migration and it should be no surprise that people are moving to Melbourne given it’s the only place with jobs growth. Immigration tends to be pro-cyclical, i.e. people will move to where the jobs are.

Source: RBA

On the other end of the spectrum, a few of the states are struggling. In terms of job growth, Queensland has gone backwards by 38.6k in the last 12 months. Western Australia, whilst having stabilised in recent months has seen a worrying longer term trend in unemployment from a low of 3.5% in 2012 to 6.0% currently.

There are two major reasons for the divergence between states and that has been the end of the mining construction boom and the transition to the residential construction boom (we wrote about this extensively in our 2017 Outlook). Essentially in an attempt to see off a recession in the face of a significant fall in mining investment, the RBA has cut interest rates from 4.75% to 1.50%. This has led to is an unprecedented construction boom in housing, particularly along the East Coast and most notably in apartments.

The chart below looks at building approvals for apartments across New South Wales, Victoria, Queensland and WA (data is rolling annual). This is a leading indicator of construction activity and we can see all four states have recently reached all-time highs.

Source: ABS

Western Australia saw building approvals peak in June 2015 and hence is dealing with the end of a residential construction boom now as well as the ongoing falls in mining investment. The major concern now is Queensland where the annual number has rolled over, and on the volatile monthly basis it looks disastrous, as can be seen in the chart here:

Source: ABS

This is a significant headwind that the Queensland economy faces over the next 12-18 months. It is likely going to put further pressure on the current employment situation. So you could argue that Queensland is in need of further stimulus.

Moving across to Western Australia and whilst the employment situation has improved slightly in recent months, unemployment still remains elevated and households are struggling. We have talked previously about how mortgage arrears for the banks in WA on a 90 day basis have moved up significantly over the last 12 months (again, see our 2017 Outlook). We can now see, via Moody’s, that 30 day arrears are shooting higher for the entire country. This is being driven by the 2013 vintage of loans which is not overly surprising given it corresponds with the mining investment peak of 2012. This vintage is the purple line in the chart below.

Further evidence of household stress can be seen in the Retail Sales data where WA has seen very little growth since the beginning of 2016. Quite clearly WA households could use a further interest rate cut.

Source: ABS

Overall, there are arguments for both directions in rates. WA and Queensland are both in need of stimulus; an interest cut rate can easily be justified in both states. Meanwhile, the unemployment rate in New South Wales is sitting near decade lows at 5.1% and Victoria is recording strong jobs growth. Both of these states are in the midst of a record residential construction boom and have large infrastructure projects in progress or due to start. One could argue that interest rate rises would be more appropriate for these states.

The conundrum the RBA faces is that interest rates are a blunt tool. To provide stimulus to WA and Queensland, they need to provide stimulus to the rest of the country, there isn’t a way of differentiating.

Thankfully there is a solution but unfortunately it relies on a functional political system. Too often in recent years, central banks have been the only port of call for stimulus globally. Monetary stimulus (interest rate cuts and quantitative easing) has been the dominant force whilst fiscal stimulus (government spending) has been non-existent. On a global basis, there is hope that this might change, a big part of the Trump rally is based upon expectations of increased infrastructure spend in the US (whether Trump lives up to these expectations is another story altogether). Unfortunately in Australia, we have a government fixated on reducing its deficit and focused on the corporate tax rates. These tax cuts are more likely to just flow through to corporate profits and are unlikely to lead to the job gains and wage increases that the government is trumpeting.

Looking at the above state of play, we believe targeted fiscal stimulus in the form of infrastructure spending into Western Australia and Queensland would be the best option for the Australian economy. This would take pressure off the RBA, improve job prospects in those areas and potentially slow interstate migration to Victoria and New South Wales. The current government should be considering some sort of action, after all the WA voters recently showed their thinking on the matter by overwhelmingly going against the incumbent Liberal government. This (in addition with the rise of One Nation in Queensland) is a function of an unpleasant economic reality. It is similar to the trends seen globally which have seen the UK leave the EU, Donald Trump’s rise to power in the US and the popularity of Marine Le Pen in France. If things don’t improve, people will vote for change.

Robert Swift and Roger McIntosh compare local and international banks. Does it make sense to own the behemoths that dominate the Australian market? Are you unknowingly doubling down on exposure to the Australian property market?

Australian vs. Global banks – Which should I own? Robert Swift & Roger McIntosh

For Australian investors, the banking sector, particularly the four major banks, form a significant part of their investment strategy and exposure to Australian economic activity. However, only investing in Australian banks even with the franked dividend income, is definitely a suboptimal approach to investing.

Let’s compare Australian banks with global competitors in terms of valuation, capital sufficiency, and business positioning or resilience.

Australian banks have high dividend yields and low variability of EPS growth compared to global competitors. This would usually make them attractive. Although we like dividends as proof of cash flow, it appears to us that Australian banks are overdistributing earnings as dividends, and not sufficiently acknowledging the risk in their loan books. In other words, their EPS resilience is somewhat masked by ‘highly managed’ bad debt recognition.

In terms of capital sufficiency, the Australian banks are average. It appears to be a form of financial arbitrage to us that the Australian banks pay out franked dividends and then raise capital in the markets to meet regulatory capital ratios. If management wanted to avoid this ‘distribute capital and then raise capital’ merry go round they would cut the ordinary dividends and wouldn’t need to raise capital since the capital buffers would be built by retained earnings. However, there would be an outcry from investors desperate for dividend income. When companies are hooked on dividend amounts which they shouldn’t be paying, it strikes us as risky.

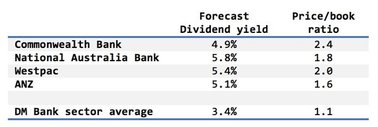

Price/book ratios may be a better guide to valuation given the latitude which all banks have in their EPS reports? In the table below we show the Australian banks look expensive on this measure compared to other developed market banks.

Source: Thomson Reuters

Australian banks tend to copy and follow each other’s business strategies and this is clearly shown in the very high correlation of the bank’s total returns with each, not offering investors a reasonable level of asset diversification. They rushed into expensive wealth management platforms and ‘fund management’ (multi-manager offerings) and all now appear to be exiting simultaneously? They all rushed into mortgage lending in NSW, Victoria and Queensland and are now being told by APRA, their regulator, to ‘cool it’. Further, to increased limits around mortgage lending, the regulator has now indicated they are reviewing further changes to the risk weightings the banks use (for details on this, please see The Lazy Dog blog post). None have cracked Asia; none have cracked investment banking as have the USA majors.

You can see the result of this ‘tack and cover’ strategy in the table below. This compares the price behaviour of the Australian banks to each other where a figure near 1 means they are al the same and a figure of -1 means they are all different.

Correlation figures of 0.8 or higher show very close similarity in asset returns. Investing in Australian banks is essentially investing in one big bank. This is not ideal for your portfolio.

Correlation of monthly total returns for 5 years ending 31/3/2017

Source: Thomson Reuters

Investing in non-Australian banks, particularly those with broad, global operations, offers a much broader and diverse source of business activity and economic exposure which in turn provides broader net cashflow and alternative revenue sources. The analysis suggests that the market is aware that the largest source of revenue for Australian banks arises from net interest income, primarily domestic loans and credit to personal and business customers. They are all the same and their fortunes will wax and wane together. No diversification here at all. Own the Australian banks and you own their residential property exposure and your own home as well. Potentially a large part of your wealth and income is focused on one asset class – Australian residential property.

Source: AFR

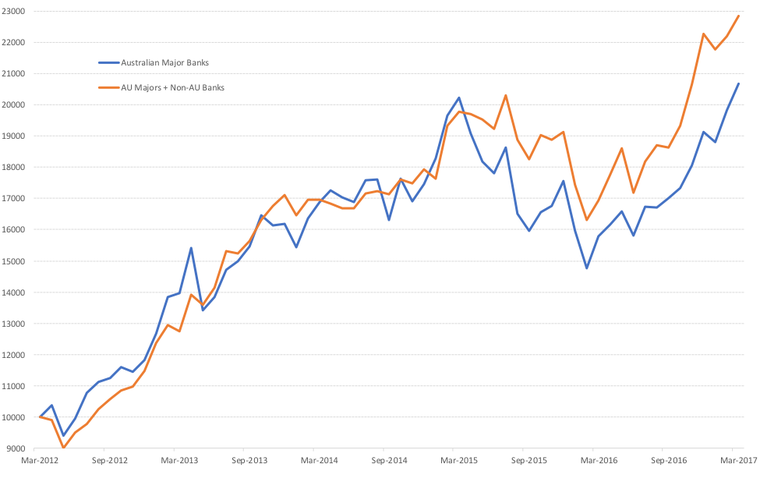

Benefits of diversifying are clearly demonstrated in an analysis of the differences in return and risk outcomes of a strategy that holds equal exposure to the four major Australian banks and an equal-weighted portfolio of the four majors and the banks held in our High Conviction Strategy. Currently, these are JPMorgan Chase (US), Sumitomo Mitsui Financial Group (JP), BNP Paribas (FR) and Bank of Montreal (CA). These banks provide a great combination of exposure to global banking and to different types of regional economic activity. They are far more diversified with their loan books.

AUD annualised gross total return and volatility for periods ending 31/3/2017

Source: Thomson Reuters

There is definitely a benefit in terms of higher returns and reduced variability of returns by adding exposure to non-Australian banks. This can also be seen in the growth in $10,000 invested in each strategy over the last 5 years.

Australian banks are not badly managed. They are not bad businesses. They pay seemingly attractive dividends. They are however very similar to each other and are currently over exposed to Australian residential loan risk. They are possibly paying out too much in equity dividends. A small increase in loan loss provisioning could wipe out in share price terms, the extra tax credits from their dividends. Consequently, there are meaningful benefits by investing outside Australia and its banks.