Small Cap Reporting Season Preview – Part 1

Zenitas Healthcare (ZNT.ASX)

TAESC estimate: $6.75m

This recent interview with Justin Walters, ZNT CEO, provides an up-to-date summary of the ZNT strategy and opportunity.

As noted in this interview, ZNT has, as of late June, re-affirmed its previous EBITDA guidance and we would expect to see ZNT report in August an EBITDA profit in excess of $6.6m.

More importantly, the outlook for FY18 would appear positive, with 14 new clinics set to open early in FY18 which are expected to contribute to FY18 earnings, together with other organic growth initiatives that ZNT are pursuing. ZNT’s management are confident of capturing further market share, in a market that is growing at ~5% annually.

We see the current share price weakness as a reflection of the market’s impatience regarding delays in ZNT announcing an earnings accretive acquisition, rather than a sell down based on any fundamental aspect. That reaffirmation of guidance and positive industry and company outlook suggests that the thesis for investing in ZNT remains very much intact.

We have recently met with ZNT’s CEO and understand that a number of potential acquisitions are being progressed, and we are confident that these will add further scale to ZNT’s GP and homecare footprint* (ZNT already owns the largest network of allied healthcare/physiotherapy clinics in Australia). Irrespective of any acquisitions, the company continues to grow organically.

With a market cap at 30 June 2017 of $42m, cash of $9.7m (31 March 2017), undrawn debt funding for acquisitions of $10m and reaffirmed FY17 EBITDA of $6.6m, we continue to see ZNT as a highly compelling and undervalued investment, with material upside.

An increasing focus on 1) the benefits of community/home care as opposed to high cost hospital care, and 2) the potential for integrative health care to assist in the management of chronic disease will support the ongoing growth of ZNT.

*on 3 July 2017 ZNT announced an investment into an established homecare company with a large presence (800+ staff) across the east coast of Australia.

Fiducian Group (FID.ASX)

TAESC NPAT (underlying) estimate: $8.5m (22% EPS growth)

FID appears to be positioned well for a strong full year result:

- As at 30 April 2017, FID’s total funds under administration, advice and management (FUMAA) was $5.6b versus $4.7b at 30 June 2016 – an 18% increase over 10 months, with 2 of the strongest months of the financial year for inflows remaining.

- As at 31 May 2017, FID’s reported funds under management was $1.8b, up from $1.47b at 30 June 2016 (23% increase for year to date).

- In the second half of the financial year FID has acquired $52m in funds under advice through the acquisition of 2 financial planning networks.

FID’s operating model benefits from significant operating leverage, so these positive developments in relation to FID’s asset management base are supportive of strong earnings growth. In its half year result, FID noted the reduction of its Cost to Income ratio as a result of the scalability of operations. FID’s reported operating cash flows as at 31 March 2017 are strongly up on the same period for last year.

For the first half of FY17, FID delivered EPS growth of 22% with underlying NPAT of $4m. Based on a continuation of strong asset flows in the second half, FID is on track to deliver underlying NPAT for FY17 of approximately $8.5m (~22% increase).

Pioneer Credit (PNC.ASX)

TAESC estimate: $10.5m

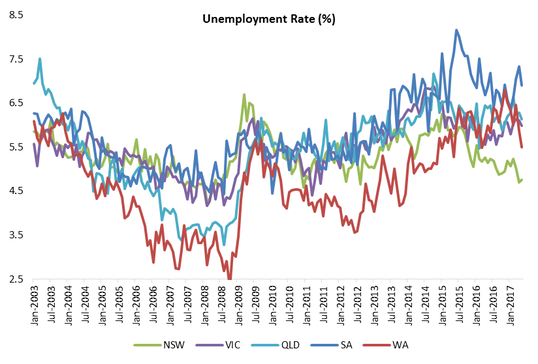

Since then, we understand that collections have remained steady and average payment terms are steady, underpinned by low unemployment rates across Australia and New Zealand.

Pioneer continues to build out its analytics focus, with a team of 12 now working on more sophisticated analysis, new business initiatives and predictive modelling.

PNC has also been busy recruiting staff for its anticipated growth, and while labor intensive, its success rate in recruiting staff has been improving. PNC’s staff retention is assisted by a strong culture installed by its impressive management team.

Due to the significant investment in training, it takes 5 months before new staff are profitable. All head count increases in back office, finance, risk, analytics, have been factored into Management’s forecasts.

We understand that Management remain comfortable with its disclosed forecasts. Despite a strong share price performance in recent months, PNC’s FY18 guidance of EPS of ~27 cents puts it on a multiple of under 9x, yielding 6% fully franked based on a 50% payout ratio. We believe this remains compelling for a business with a very strong management team, which is growing earnings at a double digit rate.