This week we present a piece by Hamish Carlisle, analyst with the TAMIM Australian Equity Income IMA powered by Merlon Capital Partners, as they follow up a previous piece on the merits of value investing.

While the long term returns from “value investing” are strong and well documented, the approach has struggled over the past decade prompting many investors to question its merits.

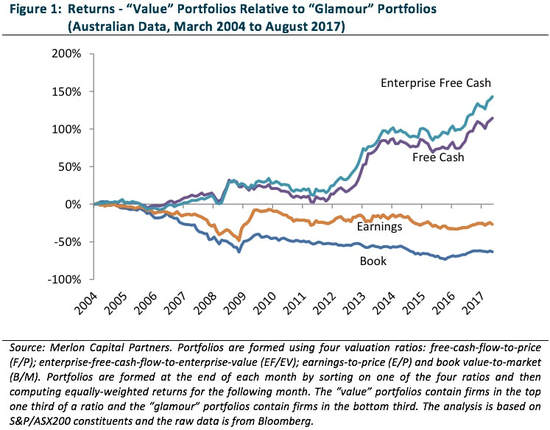

This paper represents the second of what will now be a three part series discussing value investing from an Australian perspective. In the first paper we concluded that value investing on the basis of free-cash-flow has performed well through a number of market cycles and has displayed low levels of volatility when compared to traditional classifications of value such as earnings, book value and dividends.

In this second paper, we begin to explore the question of why value strategies based on free-cash-flow outperform the broader market. Consistent with our philosophy, we present findings that show a linkage between value investing on the basis of free-cash-flow and earnings quality. We then go on to dismiss the notion that value investing is “riskier” than passive alternatives.

Why do stocks with high free-cash-flow yields tend to outperform?

The performance of value investing on the basis of free-cash-flow in an Australian context has been compelling and, in our view, represents a strong foundation for active stock selection. This key finding underpins TAMIM Australian Equity Income portfolio’s investment philosophy which is built around the notion that companies undervalued on the basis of free cash flow and franking will outperform over time.

A second key tenant of the TAMIM Australian Equity Income portfolio’s investment philosophy is that markets are mostly efficient. We don’t believe that value stocks outperform simply because they are “cheap” but rather because there are misperceptions in the market about their risk profiles and their growth outlooks.

We are focused on identifying and understanding potential misperceptions in the market. To be a good investment, market concerns need to be priced in or deemed invalid. We incorporate these aspects with a “conviction score” that feeds into our portfolio construction framework.

Value investing & earnings quality

The outperformance of stocks with high ratios of free-cash-flow to enterprise value could capture two sources of mispricing:

The well documented value premium; and/or

The accruals anomaly (See: “Do Stock Prices Fully Reflect Information in Accruals and Cash Flows about Future Earnings?”, R Sloan – The Accounting Review 1996), representing the degree to which accounting earnings are backed by cash flows

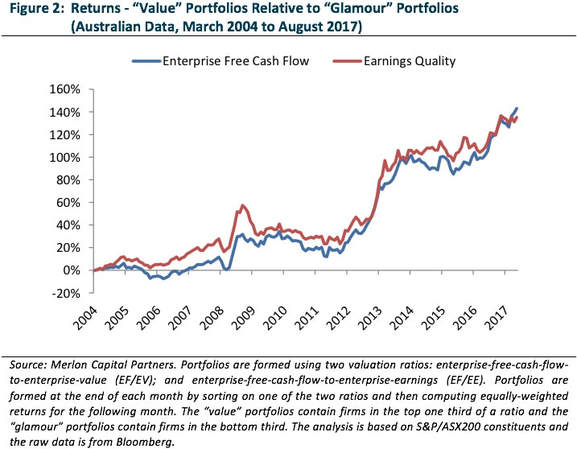

To further explore this question, we compared the returns from a strategy of investing in companies with good “earnings quality” – which we define as the ratio of enterprise-free-cash-flow to enterprise-accounting-profits – with the returns from the enterprise-free-cash-flow classification of value.

We find that the returns from investing on the basis of earnings quality are remarkably similar and remarkably correlated to the returns from investing on the basis of value as measured by enterprise-free-cash-flow. This could be interpreted in a number of ways:

“Value” has been arbitraged away while the accruals anomaly has persisted; or

The value and accruals anomalies are one in the same (See, for example: “Value-glamour and accruals mispricing: One anomaly or two?”, H Desai, S Rajgopal, M Venkatachalam – The Accounting Review, 2004).

It is difficult to definitively answer this question but in our experience both explanations are valid in particular circumstances. With regard to earnings quality, management teams and boards are becoming ever increasingly creative about how they define profitability. Our favourite notorious measure is “pro-forma adjusted Earnings Before Interest, Taxes, Depreciation and Amortisation (EBITDA)”. This measure usually and conveniently ignores capital expenditure, working capital requirements, restructuring costs, discontinued operations and asset impairments to name a few. It is often used to justify expensive acquisitions and even more cynically, used as a basis for management remuneration.

The bottom line is management teams can define profitability however they choose but can’t as easily hide from the realities of the cash flow statement. Eventually these realities come home to roost and when this happens stocks with low earnings quality tend to underperform. So long as investors place weight on measures such as “pro-forma adjusted EBITDA”, we think the accruals anomaly is likely to persist.

At the same time, we think it would be irresponsible to “pay-any-price” for companies with high earnings quality (or indeed high quality businesses in general) and this style of investing is prone to many of the behavioural biases that support excess returns from value investing in the first place.

Are value strategies riskier than glamour strategies?

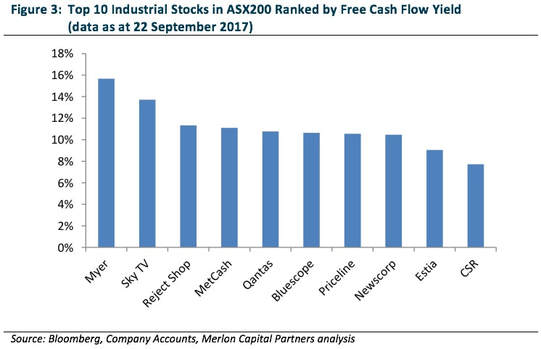

There are two schools of thought as to why value strategies have historically outperformed glamour or growth strategies. The first is value strategies are riskier than passive strategies. This is intuitively appealing when we consider the nature of value stocks. These companies are typically plagued with investor concerns, surrounded by popular pessimism and often have high levels of financial and operating leverage.

A brief look at the top 10 industrial stocks in the ASX200 ranked by free-cash-flow-yield highlights this point.

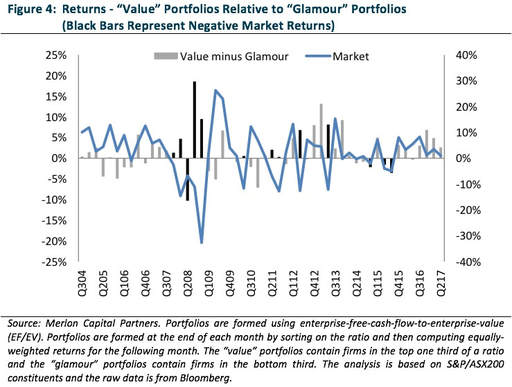

Different investors will perceive risk differently but for us the most crucial measure of risk is how particular portfolios perform in down markets. Figure 4 illustrates the performance of value strategies based on enterprise-free-cash-flow through a variety of market conditions. The point to note is that there is little difference in performance in up markets and down markets. If anything, the value portfolios perform better in more adverse market conditions.

Figures 3 and 4 highlight one of the challenges faced by many investors and their sponsors. The challenge is distinguishing between diversifiable risk (or company specific risk) and non-diversifiable risk (or systematic risk). By definition, company specific risk can be diversified away whereas systemic risk cannot. Myer – a department store – might appear to be a risky investment. However, investors should be only be concerned with how the stock performs within the context of a portfolio and how such a portfolio is likely to perform in a meaningfully down market.

Indeed, when we invest in businesses we place significant weight on understanding and quantifying downside valuation scenarios and their dependencies on uncontrollable external influences such as macroeconomic conditions. These are “systematic risks” that cannot be diversified away. This “margin-of-safety” concept is explicitly considered when we develop our “conviction scores” that combine with valuation to determine portfolio weights.

Concluding comments

The performance of value investing on the basis of free-cash-flow in an Australian context has been compelling and, in our view, represents a strong foundation for active stock selection. This key finding underpins Merlon’s investment philosophy which is built around the notion that companies undervalued on the basis of free-cash-flow and franking will outperform over time.

Any investment philosophy needs to be supported by an understanding of why a particular approach is likely to generate excess returns. In this paper we begin to explore this question. Consistent with our philosophy, we present findings that show a linkage between value investing on the basis of free-cash-flow and earnings quality. We then go on to dismiss the notion that value investing is “riskier” than passive alternatives.

In our third paper in this series to be released next quarter we will highlight a number of well documented behavioural biases that are empirically and anecdotally evident in the Australian market. We will also point to various elements of the TAMIM Australian Equity Income portfolio investment process, structure and culture that are aimed at minimising our exposure to these biases.

This week Robert Swift takes a look at the Chinese property market and the effect it will have on Australia and the World.

We have written on the China “marvel” before and continue to scratch our head on this enigma and the sustainability of it. You have to give them huge credit for what they have achieved – the greatest economic expansion in history improving the lives of so many people in a 30 year period.

I was back in Southern China again in early October on a client visit to Shenzhen – which has grown from a fishing port of 30,000 people in 1979 to over 11m people today! Shenzhen is the epitome of China’s success, otherwise known as the “silicon valley of China” it has some of the highest salaries and has now surpassed Beijing in terms of property prices.

Source: Thomson Reuters

Success and rapid growth rarely comes without its problems and its excesses. A lot of it has been built on debt – at the corporate (in particular), household and government levels. In a country that has not seen any significant downturn in the economy or property price levels, you can imagine that a feeling of infallibility and hubris is pretty strong. Trying to explain that property prices on a par with the best areas of London’s West End is rather extreme and worrying doesn’t get too many worrying at the dinner table – China’s different they say – and we’ve all heard that one before! It is clear that the Chinese government has let the residential property market get way out of control.

Of course, there have been strong fundamental drivers to the incredible rise in property prices. A close contact of ours with 30 years’ experience of investing and visiting the Asian region, Stewart Patterson has recently written a study of the Chinese residential property market.

In his report he identified three key growth drivers of residential property development in China

The increase in urban population;

The increase in living space per person and

The upgrading of sub-standard housing.

The result of these three drivers is that private urban residential property development in China has grown in nominal terms from USD300bn in 2008 to USD1.4tr now – a compound annual growth rate of 21%. Residential property sales in China are now larger than the GDP of Russia or Australia. The urban property stock in China has grown from 9.3bn sqm in 2000 to 29bn sqm at end 2016 – an annualized growth rate of 7.3%. While Chinese economic growth has accounted for more than half global growth since 2008, property (together with its multiplier impact) has been one of the key drivers of Chinese growth. If these three drivers of urban residential property demand are drying up, the global economy could well face a nasty deflationary shock. Although the Chinese government can always “manufacture” growth by increasing government borrowing, which is still relatively by world standards at around 46% of GDP, it may be difficult to contain the upheaval and the political fallout that may result in vast losses of wealth by Chinese households.

China has experienced a rapid urbanization of its population. Back in 2000 the urbanization ratio was just 36% rising to 50% in 2010 and 58% in 2016. The current pace of urbanisation, a net migration to urban areas of about 21m people per year ( out of a population of 1.36bn) is producing a rise in the urbanisation ratio of 1.5 percentage point per year. In 15 years time, on current trends, China’s urbanisation ratio will have converged on the USA, UK, France and a cluster of other OECD countries at around 78-83%. Whether it then trends higher towards Japan at 93% remains to be seen. From a housing demand perspective the key points are:

The net migration of 21m or so has been very stable over the past 20 years there is no structural growth in this number and it will fade with time as there is simply less scope for migration to the cities albeit the fade may be a decade away.

Housing demand from net urban migration as a percentage of total private housing sales is declining even if one assumes that a new migrant moves into an average sized space (which itself has been increasing). So for example: In 2000, the urban population increased by 21.6m people and the average living space per person was then 20.3 sqm. So new arrivals (either by birth or migration) required, assuming an average living space , 438m sqm. Yet in 2000, private residential urban property sales were just 151m sqm so new arrivals require 2.9x new private property sales (these exclude affordable housing and other forms of social housing). Last year the situation was dramatically different. New arrivals required (21.8m new arrivals * 36.6sqm / person) 800m sqm of property against sales of 1.35bn sqm or just 58% of the total.

The conclusion I think for this driver is that it will not drive growth in property sales anymore. It need not necessarily become a drag and produce a reduction in property sales any time soon but it is a ticking bomb in that 21m new arrivals to urban areas is not a sustainable number beyond 2030 and it may fade sooner than that.

The second driver of market growth has been the dramatic rise in the living space per person in Chinese urban areas. Back in 1985, China’s housing stock afforded just 10 sqm of living space per person in urban area. That number doubled over 15 years to 20.3 sqm in 2000. In 2016 a further 16.6 sqm per person had been added bringing the total living area per person to 36.6 sqm. The 2000 to 2016 Cagr in living space per person was 3.8%.

Clearly, 10 sqm per person was inadequate even for a country with a high population density but 36 sqm per head is a generous living space by international comparison even without adjusting for income per capita and population density. In Europe for example, the Baltic states, Poland and Czech range from 35-38 sqm per head but they have higher per capita GDP and low population densities. The UN sets a threshold of 20 sqm / capita as a benchmark for adequate housing as an economic development goal. In Japan, which is perhaps the best benchmark as to where china is heading, the ministry of land recommends a household of 2 people having 55 sqm (27.5 / head) in urban areas. A household of 3 is 23.3 meters / head.

By any standard it would appear that living space per head of urban population has ceased to be a necessary driver of growth in China’s housing stock and that in fact the urban housing stock, in aggregate has, if anything been over built in recent years.

At the end of 2016, China’s urban housing stock was 29bn sqm according to the NBS that was an increase of 25% or 5.7bn sqm over the level in 2012. So a minimum of 20% of China’s housing stock is less than 4 years old. 65% of China’s end 2016 housing stock of 29bn sqm did not exist in 2000 (when the stock was 9bn sqm) so it must be less than 16 years old. In addition, housing that was demolished and replaced between 2000 and 2016 is also less than 16 years old. Whichever way one slices the numbers (one needs demolition numbers to complete the model) it is hard to avoid the conclusion that the median age of urban housing in China is no more than 10 years. When Japan’s housing bubble burst in 1989, the average age of a housing unit was 12 years and the stock has now aged to an average age of 22 years. Housing starts, even now, 28 years after the bubble economy burst are just 50% of the peak. In the US the median age of a house is 37 years (with a range by state of 55 years in New York to 23 years in Arizona). New buildings in the US now are built with a recommended life expectancy of 75 years (implying a replacement rate of just 1.5% of the stock per year). The aging process of China’s housing stock will likely result in meaningfully lower investment.

The fundamental factors therefore clearly point to a potential ending of the property boom in China, which has been a big driver in the overall economic growth rate. But what about the speculative element of property demand? It is difficult to gauge the size of speculative demand from the paucity of statistics coming out of China but from my anecdotal evidence it appears significant. It would appear that a significant number of apartments lay empty and are simply held for capital appreciation purposes. It appears that a small but significant percentage of the business/professional classes engage in property speculation – and on paper at least, have made many millions of RMB this way. Many of these properties have been bought with mortgages. So you have potentially very “weak holders” of property here if they start to run in to cash flow problems if there business isn’t doing so well or if they start to think that property prices may start to decline or are indeed declining. So you have a potential recipe for a very volatile situation.

So why should we care about residential property prices in China? Well, the residential sector has clearly been a key driver of growth in China – even if it is with borrowed money! Higher prices drive more construction and more demand for raw materials like copper, steel etc and a whole lot of other inputs – some of which come from overseas. So a potential blow up in the Chinese residential market will have a significant impact on the world economy. There will be secondary effects too. The Chinese middle classes will pull in their expenditure on overseas trips, luxury items, etc.

The conclusion seems to be that while urbanisation will likely continue and hence the urban population will grow at about 3% to 2.5% year on year or 20-22m new additions per year, the current housing stock is large enough for the existing urban population and is incredibly new on average. The key demand drivers for housing development have peaked at best or are exhausted at worst. A major engine of both Chinese economic growth and global reflation is potentially running on empty. As development becomes less necessary, it will become even more speculative, cyclical and that coupled with its increasing debt-dependency (albeit still low by international standards) in our view makes it more prone to a sudden down turn.

This week Guy Carson takes a look at REITs and their potential role as the source of crisis in the Australian economy.

A version of this article was published in The Australian on 21 October 2017.

Back in 2007, the wheels began to fall off the global equity market rally. The key driver was a tightening within credit markets globally to the point where some companies were completely frozen out and couldn’t refinance their debt. The REIT sector was the epicentre of the crisis in Australia and the poster child for problems was Centro Property Group.

Centro operated as a funds management company with ownership stakes across the underlying investment funds. These funds then undertook developments, and deployed capital. After an initial equity raising, the funds would use debt to complete developments whilst booking revaluation gains. The head company, Centro would use debt to fund their equity stakes in new funds and increase their gearing there as well, effectively creating gearing on gearing. As a result the financial statements were opaque and the company hid negative cashflow and rising debt levels behind asset revaluations. This behaviour was prevalent across the industry and other players such as Goodman Group, Charter Hall and GPT were all forced into deeply discounted equity raisings just to survive.

When you look back at history and examine businesses that have failed, they all have one thing in common. High debt levels combined with insufficient or negative cashflow. Typically these companies will rely on capital markets to fund their operations and when those capital markets close, the music stops. This happened in 2007 for the REIT sector and the poor capital management was exposed.

Understandably, with interest rates starting to rise globally, investors are now starting to get nervous and many worry about a repeat of 2007 and 2008. However, when we look across the sector we do see vastly improved capital management in recent years than we did during the previous bull market. The funds management model has evolved and companies such as Charter Hall and Goodman Group have become more efficient at using other people’s capital and taking less development risk on their own balance sheet. The potential problem for them comes if that capital pipeline dries up and rising rates could potentially do that. If demand for property funds fall then earnings could falter. As a result we don’t think it’s necessarily a good time to buy REITS but given their vastly improved capital structures we don’t believe solvency is an issue like last time.

Elsewhere in the sector, some companies do have elevated gearing levels and will feel some pain such as Cromwell (who has recently been downgraded by Moody’s), although again we are not overly concerned around solvency. In fact, of all the major REITs we would consider Westfield as the one most reliant on capital markets and hence most at risk. Since spinning out Scentre back in 2014, the company has been in development mode and as a result has had negative free cash flow, rallying instead on capital markets to finance its growth. With a $9bn development pipeline left to complete this need for funds will continue for a number of years yet, whilst at the same time valuations of Retail property assets are coming under pressure globally.

Given we don’t expect REITs to be the epicentre of the next crisis; it’s worth looking at what sectors might be. The obvious answer would be the financial sector and obviously the banks are under scrutiny from investors but the rise of the small cap finance sector warrants some watching with a large amount of junior companies operating in niche sectors. Another popular sector amongst investors that stands out due to complex financial reporting is the Aged Care sector.

As we mentioned above, the characteristics that lead to business failure are debt levels that are too high and insufficient cashflow. In the Aged Care sector we worry that the companies are potentially understating the amount of debt they have and overstating their cashflows. This phenomenon comes about through what is referred to as Refundable Accommodation Deposits (RADs). The RADs are a lump sum payment paid upfront for entry into an Aged Care facility. They can be used for multiple purposes and sit on the balance sheet as a liability but not as pure debt. As a result they can be used as a third source of funding (alongside equity and debt) and can effectively be used to increase a company’s return on equity. The current listed players (Estia Health, Japara Healthcare and Regis Healthcare) have historically used these funds plus debt to make acquisitions, adding more RADs and hence more funding to the balance sheet. In addition some of the listed players include the change in RADs in operating cashflow, which potentially overstates the cash they are earning.

If we take Estia for example, we find their current debt level is $121m against $1,798m of total assets. At first glance it appears there is nothing to be worried about (a gearing ratio of 6.7%), however we delve a little deeper we discover some cracks. Of the $1,798m of assets we find $1,036m are intangible, predominantly goodwill from acquisitions. In addition the RADs on the balance sheet are $730m; hence if we were to include these as debt (they do have to be repaid and the holder does receive government mandated interest) the company has negative Net Tangible Assets.

The problem for these companies comes about if the proportion of residents who pay via RADs starts to fall. If this proportion does fall, these companies will experience potentially negative cashflow in what is effectively a forced reduction in debt. A large reversal in resident behaviour would cause tremendous financial strain. The three major players are all recent listings that came to market riding changes in legislation (the Living Longer Living Better reforms) and a thematic that investors were exciting by (an aging population). However, at the heart of these companies are low returning assets juiced up by financial engineering and subject to regulatory scrutiny. We don’t believe the sector has been fully tested as yet and we worry about what happens when it is.

This week the TAMIM Small Cap team take a look at the embedded value within their portfolio.

Summary:

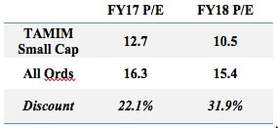

As the portfolio underlying the TAMIM Australian Equity Small Cap IMA approaches its 3 year anniversary we believe the embedded value opportunity within the portfolio is as compelling as when the portfolio was launched. The strategy is invested in high quality smaller companies which are trading well below our view of fair value. The portfolio is currently trading at a 32% FY18 P/E discount versus the All Ords despite the fact that expected FY18 earnings growth is expected to be almost four times greater.

What is embedded value?

Embedded value is generally defined as being the underlying value of an asset based upon:

Earnings – The underlying value of the asset is generally calculated as the net present value of expected future cash flows.

Assets – The underlying value of the asset is generally calculated as the realiseable value of the assets, or the price they could be sold at on the market.

In the TAMIM Small Cap strategy, we are looking for high quality smaller companies in which embedded value is far in excess of the current market cap.

The TAMIM Small Cap portfolio embedded value opportunity in numbers:

The TAMIM Australian Equity Small Cap IMA portfolio currently owns 17 high conviction stocks which we believe are the “best of the best” high quality smaller company opportunities listed on the ASX. At present, the vast majority of these positions are earnings based positions – i.e. stocks in which we believe the discounted value of these companies’ future cash-flows is far in excess of their current market caps.

At a portfolio level the most effective way to present the earnings based embedded value opportunity is to show the underlying portfolio’s weighted average P/E valuation versus the weighted average for the All Ords, and then to compare the weighted average expected earnings growth for FY18 with the All Ords.

TAMIM Australian Equity Small Cap underlying portfolio weighted average P/E vs the All Ords (assuming portfolio is fully invested as cash has no P/E):

The TAMIM Australian Equity Small Cap portfolio is trading at a significant valuation discount versus the broader market.

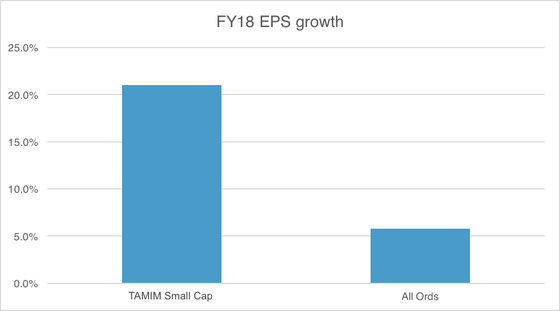

TAMIM Australian Equity Small Cap underlying portfolio weighted average expected FY18 earnings growth vs the All Ords (assuming portfolio is fully invested as cash has no EPS):

The TAMIM Australian Equity Small Cap portfolio’s expected earnings growth is 3.6x that of the broader market.

It is the combination of the above table and chart which shows the TAMIM Australian Equity Small Cap portfolio’s embedded value opportunity: i.e. The portfolio is trading at a 32% valuation discount versus the broader market and yet earnings growth is expected to be almost four times the market average. In our experience, this is an usual combination within the investment company universe, and highlights the size of the strategy’s opportunity looking forward.

How will the embedded value opportunity be realised for investors?

Earnings positions: Typically for earnings based positions the value opportunity will be realised through earnings reports which highlight cash flow growth rates above market expectations, and thus lead to an increase in market expectations regarding future cash flow growth rates.

Example: Zentias (ASX:ZNT) is a typical TAMIM Small Cap portfolio earnings based position in that it ticks all our boxes for a high quality company, is trading at a significant sector discount, and its expected catalysts are earnings upgrades driven organically and through acquisitions. We believe the stock is trading significantly below its embedded value at present.

ZNT has been covered in a recent research article (again here).

Asset positions: Asset based catalysts tend to be less predictable than for earnings positions as they are often driven by one significant catalyst as opposed to regular quarterly earnings reports. The key major catalysts we generally expect for asset based positions include: asset sales, asset purchases, and growing sum of the parts visibility based on improved market communication/disclosure.

Example: Elanor Investors (ASX:ENN) offers a compelling asset valuation opportunity at present in our opinion as the stock is currently trading roughly in line with its current net asset value which implies its highly profitable fund management business is trading at a significant discount to fair value. This is a typical example of the sum of the parts becoming increasingly visible in an asset based position over time.

A generally long term perspective: We believe we have a significant advantage over shorter term focused investors/traders over the long term. By “not caring” about the short term market noise we find that we are well positioned for the value creation in our stocks as and when it arrives. This long term perspective will be absolutely key in realising the embedded value within the TAMIM Small Cap potfolio.

Conclusion:

Buying stakes in ASX listed companies in which embedded value is far in excess of the current market value is what we are focused upon day in, day out. We believe this underlying value will be realised through catalysts such as earnings upgrades, as well as our old friend, time.

This week Robert Swift and Roger McIntosh, of the TAMIM Global Equity High Conviction IMA, take a look at the tricky subject of creative accounting and how it must be factored into your stock analysis.

Quantitative stock selection models such as our VMQ assessment, provide a sound and proven framework for identifying attractive and unattractive stocks.

However, quantitative signals that are based on financial statement information can fail to spot creative accounting techniques which may fool the signal and give false comfort. Consequently, we perform complementary ‘fundamental’ research based on Accounting, Strategic and Governance perspectives.

These are as equally important as our quantitative signals. Although we dislike the term, some people call it a ‘quantamental’ approach to stock analysis and selection. It’s actually quite hard to use both sets of signals since most portfolio managers believe these two kinds assessment models are from competing philosophies. We believe they are complementary philosophies and wouldn’t invest without analysing both.

One currently overlooked aspect of company profitability and its sustainability, is that of corporate taxation. Many companies know that EPS are the driving force behind share price growth and will consequently do all they can to boost that number. This can be done by creative accounting including tax avoidance, and simply by underinvesting in the business by reducing capital expenditure and thus depreciation charges.

If a company has been systematically underpaying tax then it is quite likely, now more than ever, that its day of reckoning will come. We have been working with a forensic accounting service, Bucephalus Research in Hong Kong, to identify companies which are creatively avoiding tax (and performing other accounting shenanigans) and are concerned where this tax avoidance alone makes their shares look cheap. We believe in an era of greater scrutiny and cooperation on corporate behaviour, this is a risk to share prices which is underestimated. Our portfolios, we believe, have very limited exposure to companies with earnings boosted by this creative accounting.

Where we do have exposure, such as Gilead, we try to ensure that we understand why.

Tax is incurred and payable as part of a company’s regular business and can provide a good indication of the real level of cash earnings behind profits. Since cash pays the bills, cash earnings do matter. For most companies, their tax expense is close to their notional and national tax rate, but disparities do exist. This is typically due to the nature of cashflow within different industries. Tax expensed is not the same as tax paid. While there can be many reasons, these differences are typically short term and wash out quite quickly – this is normal and doesn’t bother us.

For some companies however, even when adjustments are made to take these additional factors into account, discrepancies persist. These are the companies where investors should question why and how the company is more able to book non-taxable profits. Are other matters being hidden? Is the circumstance sustainable? The OECD, a body which seeks greater global cooperation and conformity, has established a Base Erosion and Profit Shifting (BEPS) programme in 2016. This was established in the wake of different profit shifting scandals, and aims to prevent jurisdiction shopping where companies move to declare profits in places of more favourable tax rates. The BEPS framework will make it harder for companies to maintain this situation and ultimately will lead to higher tax costs for certain businesses and industries.

Tax is important for different reasons. Higher tax paid on profits reduces shareholder access to this via dividends. We are seeing some moves across different countries to reduce company tax rates to retain and grow business activity. Companies, particularly international entities, in different industries and regions can relocated cashflow to legitimately pay a different effective tax rate.

Analysis of tax paid can also identify anomalies in financial statement information such as whether a company is applying creative accounting techniques to elements that form the input to quantitative valuation signals. It can identify whether a company is utilising debt manipulation techniques to provide a set of accounts that meet credit requirements and investor expectations, but glosses over reality.

Robert Medd from Bucephalus recently identified Amazon as a company suspiciously paying little tax. This is in line with a recent article we wrote where we argued that this was just as anti-social as a company which was involved in high carbon emissions, and armaments manufacture. Yet this aspect of company behaviour is, not yet, remarked upon. So, the ESG advocate, who argues for shutting coal mines is quite happy to do so having bought their corporate wardrobe on line via Amazon! We have had a few provocative and animated discussions on this one.

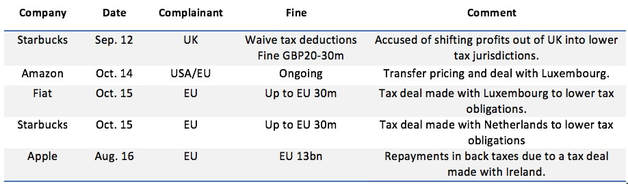

We recreate here Robert’s recent work on the USA companies most likely to be at risk of being “called to account”.

Recent tax penalties:

Source: Bucephalus Research Partnership

Companies that may be most affected by BEPS – NB Gilead!

Source: Bucephalus Research Partnership

Certain companies and industries have greater ability to move cashflow to minimise the impact of tax on ongoing cashflow. The monitoring and enhancement of fundamental characteristics and oversight through company knowledge can help to ensure the strategy avoid investment based on aggressive or even misleading information

What this all means is that any investment process should maintain a robust fundamental oversight on all information that is available. This ensures that any stock is verified as truly attractive with all risks identified. As we state in our presentations – It’s Valuation Momentum Quality (VMQ) + Accounting Strategic Governance (ASG). Sources: ‘Tax matters: Creative accounting and tax laundering’, Robert Medd, Bucephalus Research Partnership, September 2017