Remember the Tech Media Telecom (TMT) bubble of the late 1990s? Australia didn’t participate because of an absence of such companies on the ASX, but elsewhere it produced a frenzy of deals and some ludicrous valuations which mostly came unstuck. Although it eventually got out of hand with crazy valuations, and a subsequent bursting of the bubble, there was clear logic to the excitement it generated. Much of the infrastructure we use today, and some of the companies we know today, were built and cut their teeth, during the TMT bubble and subsequent burst.

So you’ve sold Telstra… Now what? Robert Swift

Indeed, with the advances in smartphone technology and the growing importance of social media these forces have only strengthened. The younger generation especially expect to find TV, internet, video and social media all on a smartphone and delivered in one bundle or billable package. Latest evidence shows that the younger generation rarely watch a large TV in the home! Furthermore, further pressure has been put on incumbent telecom providers in most western markets, as regulators have forced them to share their infrastructure with other potential telecom providers.

Party like it’s 1999?

Due to this demand for bundling, and the downward pressure on margins imposed by the regulators, corporate deals have been on the rise – TV providers moving in to Telecoms (Sky providing internet, mobile and fixed line services) and Telecoms providers buying media companies (AT&T buying DirectTV and trying to buy Time Warner; Verizon buying AOL and, eventually, Yahoo). Just recently there was a bid for Scripps Interactive (owner of such awesome entertainment as The Food Network and Travel Channel) by Discovery Communications (Animal Planet). This brings a female and male content provider together in a cable TV package but it is not going to be enough to save the Cable TV business from the threat of a better internet and the 5G buildout by AT&T and Verizon and other Telecoms. In all probability, once this Scripps deal is consummated, it will make the enlarged group an even more attractive target for a Telecoms or Social Media giant company to acquire. Even a sector giant like Walt Disney with a market value of US$172bn cannot be immune given its relatively modest valuation these days trading on 16x earnings for next year. We note with interest that Disney have just told Netflix that they are no longer going to be an offering on the Netflix platform. It seems that content providers now have more choice as more platforms gear up, or it may be that Disney have just stated they are willing to talk strategically to all comers as an independent content company?

Deals cost

We also understand that Apple and Google are talking about an increase in price of $2bn for the iPhone to use Google’s app as the default for search. In 2014 Google paid Apple $US1bn for this! Some price increase! Verizon’s purchase of Yahoo may have been brilliant IF (and a big IF) they can reinvigorate that community to monetise it.

It’s not just party time in the USA. SKY in the UK, which owns satellite TV platforms in the UK and a number of other countries, and also moving in to mobile, fixed line and internet services, is currently in the middle of a takeover from Rupert Murdoch’s 21st Century which already owns just under 40% of SKY. Liberty Global (USA) continues to raise its stake in ITV (UK) and is widely seen as a prelude to a full bid. Altice, the large Dutch based telecoms operator, is rumoured to be looking to put a bid together for Charter Communications which is the 3rd biggest pay TV company (Spectrum) in the USA serving 25m customers.

Great content costs! Look how much Sky TV in the UK has to pay for premiership football rights – over £4bn for a three year deal! So, to pay for great content, you need scale and deep pockets! A large potential customer base with sufficient discretionary income is scale. You also need a strong balance sheet or high free cash flow to be able to finance such a deal and continued investment in the infrastructure.

It appears that there is more activity building in the TMT space. Given that investment bankers all talk the same concepts to the same companies it is likely these deals continue. This time the Telecoms companies seem to be on top of this and are aggressively playing in this space to become more vertically integrated. We believe these Telecoms have the distribution bandwidth, the customers from their telephony business (fixed line and mobile) and, are now hunting for content – think Optus buying the rights to live broadcast of the English Premier League football in Australia – to add more services to existing customers, more subscribers and, most importantly, the advertising $.

A second chance for Telecoms?

When we think back to what the incumbent telecom companies owned, what resources they had, and the strength of their balance sheets in 2000, it is extraordinary to think that they let the likes of Facebook, Google and Netflix in and to take from them so many potential subscribers and advertising $. These Telecoms had a vast customer database on which much detail was known, they had a comprehensive billing system that dealt with millions of customers, they had a network of engineers on the ground, and a high street presence through the mobile telephony shops, and they had the technical infrastructure to deliver a wide range of services. They also had great cashflow from their business and nicely mixed the need for dividends with acquisitions, debt repayments and capital expenditure. They still have these attributes and while they were asleep at the wheel they are not now and the competition with Google, Facebook and Netflix is hotting up. Given the discrepancy in P/E multiples between FANG stocks and Telecoms, we think that some telecom stocks especially in the USA are an attractive proposition right now. They have the bandwidth, the hardware, know the customers directly, and good technicians. They just perhaps need a new management culture to deal with this opportunity?

Meanwhile in Australia…

So where does Telstra the Australian incumbent fixed line and wireless company go? Can it join this revolution? Probably not without cutting its dividend (as it has done today!), or using leverage on its balance sheet, or, entering a JV. It actually has a big problem. Its dividend yield may be high which is attractive to investors, but as a result it has little money left over, or limited retained earnings, to expand organically. Also, its home market is small in comparison to say the USA or Europe and therefore it has fewer potential subscribers in which to spread the cost of expensively acquired content. Its home market is also fabulously competitive in both fixed line and mobile telephony so margins are under pressure and the new National Broadband Network (NBN), which is effectively Telstra’s own infrastructure is now open to all entrants. Telstra will have to compete with new comers on content and service but has no free cash flow after the dividend to pay for content or build a community to be monetised. Despite its attractive high dividend yield Telstra has significantly underperformed both the Australian stock market and its global telecom peers, as investors have recognised its limited scope to grow. Of course, it can continue to buy in rights to content but it is more of a price taker in such situations.

For a full delivery of a range of services you need the technical capability to deliver the media (which the Telecom companies have), the content itself (which the pure media companies like a Disney provides), and ideally then end distribution mechanism (a TV channel or these days just the internet will do). These developments look a lot like a move to vertical integration, which is a logical strategy given that ‘net neutrality’ laws may be revoked in the USA, allowing an internet service provider to narrow the range of services and content via its portal to only those subscribers it bills.

So, there is a lot of activity in this whole TMT space right now across the globe throwing up lots of potential investment opportunities. As more deals get done it will put more pressure on those who haven’t participated, who feel sub scale and vulnerable, and force them in to doing deals. Sadly, Telstra is being left behind and Australian investors need to be looking to their global equity portfolios for quality exposure to the TMT sector.

As mentioned last month, with reporting season in full swing, we will address the trading outlooks and our expectations around the upcoming results for some of our core holdings. Last month, we discussed Pioneer Credit, Fiducian and Zenitas, whilst this month we will focus on Apollo Tourism and Leisure, Elanor Investors and Konekt.

ATL is a leading integrated, global player in the RV (recreational vehicle market) – manufacturing, importing, retailing and renting RVs in Australia, NZ, United States and Canada.

The company was recently profiled in the Australian.

In early May, ATL provided a strong trading update, expecting FY17 NPAT to be between 5% and 10% above its forecasts. Management commented that forward rental bookings were ‘looking positive’ in all geographies, with bookings for the upcoming USA season tracking ahead of last year. In relation to ATL’s retail operations, Management noted that continued growth in new vehicle sales was expected in Australia and New Zealand, particularly for the Adria and Winnebago brands.

We believe beating the company’s prospectus forecasts will give the market increased confidence in the ATL strategy. Growth into FY18 for ATL will be supported by earnings contributions from its recently acquired Australian caravan and motorhome retail operations and its new wholly-owned Canadian RV subsidiary, CanaDream Corporation – one of the largest RV rental and sales companies in Canada. Both acquisitions are expected to be earnings accretive in FY18. Ongoing tourism growth from ATL’s key markets, particularly Europe, and increased RV fleet utilisation is expected to result in strong profit growth for ATL in FY18.

During FY18, to support its Australian retail RV footprint, management expects to relocate it Brisbane manufacturing facility to larger premises, resulting in an incremental ~$1m operating cost in FY18. This incremental cost will diminish in future years when the existing facility is fully exited. Notwithstanding this additional FY18 expense, ATL continues to trade on an undemanding multiple for a growing global company of ~12x FY18 earnings.

Konekt provides workplace health solutions, helping organisations prevent workplace injuries and minimise the impact of workplace injury costs by assisting injured employees return to work. KKT is an Australian market leader (~11-12% market share) in a very fragmented market.

In May, Konekt confirmed its revenue guidance in the range of $51.0 to $53.5m and EBITDA margin in the range of 10.5% to 11.5% (of revenue).

In H117 KKT recorded revenue of $26.3m at 11.3% margin and noted it was well positioned going into 2HFY17 with some good momentum across the business. We would expect a result at the top end of guidance which implies earnings per share of c. 5 cents. This places KKT on a price/earnings multiple of c. ~11x FY17 earnings.

We do not think that is demanding pricing for a market leading national business, very well led by Damian Banks, and with a strong track record of very high earnings growth (EPS was just 1.4 cents in FY14). The business has the potential to take further market share in a fragmented market and/or expand its range of service offerings to become a diversified corporate health provider. To drive organic growth, KKT continues to open new offices (to add to its existing network of 40+ services) and to offer to existing clients a wider range of services (ie workplace mental health).

Notwithstanding a significant CAPEX program undertaken for FY17 (approximately $1.8m), KKT’s free cash flow and acquisition funding facility of up to $10m positions it nicely to take part in industry consolidation and provides further potential upside to organic growth. Given the sector consolidation, KKT also may be seen as an attractive takeover target itself at some stage.

Elanors Investors (ENN.ASX)

ENN guidance: not provided

TAESC estimate of core earnings: $12.3m

(FY16 Earnings: $11.6m)

Property and hotel fund manager and investment company, Elanor Investors, is a portfolio holding where we are expecting a small increase in earnings for the year, but a weaker earnings per share result relative to the prior year due to share issues during the year. While ordinarily this would be concerning, for the reasons set out below, we believe ENN now represents compelling value for investors.

After a strong first half where ENN delivered a record result on the back of significant performance and acquisitions fee, ENN’s second half will be softer with reduced contributions from performance and acquisition fees.

However, based on a market update in June, as a result of recent valuation uplifts to its hotel and tourism assets and the mark to market of a development asset, ENN’s underlying net asset value is now approximately $2.00 per share, almost equal to its current share price.

What this means is that the market is essentially valuing ENN based only on the value of its hard assets (its hotels and property investments and some minor non-core assets) and is attributing almost no value for ENN’s actual ‘operating business’ – its highly regarded fund management operations.

This fund management business currently has $700m funds under management, and generated segment EBITDA of $8m in FY16 and $7.8m in H117 (driven by $5m in performance and acquisition fees), and has significant leverage to ongoing FUM growth and significant potential performance fees. ENN management are optimistic about converting their strong pipeline of new fund initiatives which should support growth into FY18 after a relatively quiet last 6 months in terms of FUM initiatives and divestments.

As value investors, we believe that this represents a compelling value opportunity, and we like the ability to buy a share of a high quality funds management business with a top class management team for next to nothing. Catalysts to potentially unlock this value include the sale of non-core assets, new fund initiatives and asset realisation / generation of performance fees.

Note: All three stocks mentioned here are currently held in the TAMIM Australian Equity Small Cap IMA portfolio.

Australia has a love affair with property, however you can’t go a week without seeing a newspaper headline proclaiming the next property crash. The low level of global and local interest rates over the last 9 years has caused property prices to go up significantly due to low financing rates and investors searching for an investment vehicle to provide them with a better yield then they are able to receive from the banks. The apparent benefits of property are good long term return potential.

Generally property is an asset class with lower levels of volatility and when added to an existing portfolio of shares and bonds it is an excellent diversifier of overall portfolio risk. Headlines, as always, are dangerous as they are designed to sell newspapers and don’t provide the full picture. With property (as with equities) there are a large number of factors to consider. This includes the ever important location, location, location as well as the yield on the property. You also need to consider which sector of the property market you are looking at, is it residential housing? Commercial buildings? Industrial factory space? Or retail shopping centres to name a few. At TAMIM we are constantly researching investment markets for opportunities to deliver returns to clients and over the next few months we will be sharing our thoughts on investing into the various property sectors starting with retail.

There are a lot of significant factors that impact the performance of a shopping centre be it regional or metropolitan.

Anchor tenant:

One thing that is noticeable is that the performance of the anchor tenant be it a supermarket or discount department store has a very strong bearing on the overall returns of a shopping centre. The anchor tenant can, amongst other things, be impacted greatly by opening hours, the range of goods on offer, the price point, and the ratio of car parking. This, logically, can impact the performance of the adjoining specialty stores. If customers visit the centre for their staples then the surrounding stores will, in turn, benefit from increased foot traffic.

Catchment Areas:

As can be expected, the retail sector will always face cyclical and structural economic issues. Several cyclical issues are beginning to move in the sectors favour. With strong growth in four or five sectors and dwindling numbers in four or five other sectors, employment is a cyclical issue significantly impacting the performance of any given shopping centre. The jobs gained and lost are not necessarily in the same locations. It follows that certain catchment areas are doing better than others.

The catchment area for the shopping centre impacts the performance of the centre. Accessibility (i.e. the surrounding road system and the actual points of access to the centre) is a factor while location in relation to competing centres is also important when projecting performance. As you can imagine, the size and demographic (age etc.) of the population as well as the potential for its growth in the long term can have a material and critical impact on performance. In today’s world, with greater fluidity of the global population and increased levels of immigration, ethnic factors are increasingly playing a role in determining the performance of shopping centres too.

Demographics:

Continuing this discussion around employment and catchment areas, the size and shape of the workforce has a weighty influence on retail property. Wages dictate spending and jobs roughly delineate catchment areas. Australia is one of a small number of countries that have enlarged their workforce over the last ten years. The Australian workforce continues to grow in size while unemployment creeps lower. This has occurred in part because growth in wages has been borderline stagnant allowing for the hiring of more workers than may otherwise have been the case. Inflation in asset prices has boosted household wealth despite household income growth being restrained. Growth in household disposable income remains below average despite positive contributions to household spending capacity coming in the form of increasingly low interest rates, depressed petrol prices and increased comfort regarding job security.

Spending patterns:

It appears that changes in consumer spending patterns in the last decade have had a negative effect on apparel, department store, and discretionary retailing turnover in general. This has affected tenants in many regional and some sub-regional centres. Many sub-regional shopping centres have been immune from this though. The turnover statistics from ABS in the table below show robust growth over the long term in many of the significant retail categories found in your average shopping centre. Supermarkets have been seeing solid turnover growth as have the liquor stores that come under their stable. Discount department stores dealing in discount clothing, electronics, and household goods including furniture have also been experiencing decent turnover growth. Specialty shops associated with shopping centres such as bakeries, chemists, newsagencies, take away food stores, and other local service providers such as dry cleaners may be in the tenancy mix too.

Source: Savills

The Amazon factor:

In addition to these broader issues, there is the imminent arrival of Amazon on our shores to consider when looking at retail property. There is no doubt that Amazon arriving here will have a significant impact on retail. Having said that, there will be a grace period of sorts before the impact is truly seen. Amazon will need to set up the infrastructure they need to properly compete with shopping centres and follow that by winning over the trust of the Australian public before taking significant market share. In looking at the entry of Amazon to the Australian market one must also consider that regional and sub-regional shopping centres will unlikely be affected anywhere near as quickly or as much as those located in the major cities as Amazon will look to establish itself and win over major population centres like Sydney and Melbourne ahead of places like Newcastle or Ballarat. To this point, Amazon recently confirmed it will open a 24,000 sq metre warehouse in Melbourne’s Dandenong South.

The Trend for 2017:

Smaller stores are in; larger stores are out.

Changing consumer preferences will push more and more “big box” retailers to focus their attentions on smaller-format stores. Less is more in 2017 when it comes to store size. Retail giants such as Target, Best Buy, and Ikea are already adjusting to this trend by increasingly spending on smaller-format stores instead of their traditional borderline-warehouses. The importance of convenience and accessibility in todays world of instant gratification is key to understanding why shoppers are moving away from larger stores. People just don’t want to waste their valuable time roving the never-ending aisles of huge stores these days. They want things to be made easy for them with smaller stores offering specialised selections. Additionally, smaller stores cost less to establish and run. They also take up less space in urban environments which allows retailers to capitalise on the potential of more densely populated areas.

“Retailtainment”, as may be evident from the name, is the combination of retail and entertainment. The concept is a concerted effort by retailers to offer shoppers a fun or unique experience that incorporates lifestyle elements into their stores. Things like boutique coffee offerings or reality experiences that are more likely to engage retailers and keep them coming back for the shopping experience. For an international example one can look at Fortnum and Masons, a department store in Piccadilly in London. The 3rd floor has been transformed from menswear (which is offered in overabundance in other local outlets) to a cocktail bar.

The opportunity:

The structural issues facing retail property can be formidable but certainly not insurmountable. TAMIM anticipates that the retail sector will evolve to take advantage of these structural issues rather than be over-whelmed by them. An ageing population will not stop creating challenges for the retail space as they compete for the all-important spending of retirees. Retirees can usually be expected to show preference for services over goods and will not necessarily continue to dwell in their traditional catchment areas. Online shopping has already had a great impact on retailing for certain categories of goods and, with the imminent arrival of Amazon, it will no doubt continue to present challenges for the sector. Retail has already been forced to begin adapting without the world’s biggest player arriving and will continue to do so. Certain areas, notably regional and sub-regional centres, will likely hold out longer and more effectively than their metropolitan counterparts.

Every six months in Australia, reporting season comes around. It’s an important time for investors as it gives us a chance to see in detail how companies are travelling and, in some cases, what their outlook is for the year ahead. As a result, February and August become important times for shaping portfolios and generating investment ideas. Whilst every result will be scrutinised, we believe this reporting season there are a number of major questions outstanding for which we will receive further clarification.

Reporting Season: The unanswered questions Guy Carson

1) Will Telstra cut its dividend?

Back in February, we wrote that “we expect that Telstra will be forced to cut their dividend sooner rather than later.” That was on the basis that Telstra was paying out more in dividends than it was earning as can be seen below.

Source: Thomson Reuters, company filings

From the above we can see that historically Telstra has paid out close to, if not all of their earnings in dividends. However, going forward we believe this needs to change. The Telstra of today is a very different company to ten years ago. What was once a national monopoly now faces competition on all fronts. As a result, the company will need to invest in their networks and in other growth initiatives to stay ahead of the pack. Previously, due to their natural advantages the company could pay out earnings and then use to capital markets to facilitate investment. With the increase of competition and the potential decline in margins and market share ahead, we believe this capital allocation strategy needs to be revised. As a result, we expect Telstra to cut their dividend. Whether it happens at this result or they provide guidance for next year, we believe we should get some clarity at this result.

2) Will the end of the residential construction boom factor into the guidance for residential REITs?

The leading indicators for the residential construction industry are pointing down. Building approvals have peaked, commencements have followed and completions typically follow 6-9 months after.

In an economic sense, this has been one of the major drivers of the Australian transition from the mining boom in recent years. With the RBA cutting interest rates from 4.75% to 1.5%, they have sparked the biggest building boom in Australian history. With the downturn upon us the only question that remains is whether we have a hard or soft landing. How the major developers react will be interesting.

The building boom has been kind to some of the major listed players in recent years. Mirvac, for example, has seen residential earnings grow by 51% last year and potentially by another 45% this year.

Source: Company filings

The focus though will quickly turn to next year and the expected amount of settlements as well as the level of presales. If volumes start to decline, earnings will follow.

3) Which companies are shaping up to be the major beneficiaries of an East Coast infrastructure boom?

With the residential construction boom potentially coming to an end, one of the most compelling stories from a top down perspective is the coming infrastructure boom set to take place predominately on the East Coast. The chart below looks at the major construction projects across Australia and their planned timing.

Source: CImic Company filings, Macromonitors

The vast majority of projects are taking place in New South Wales (Bruce Highway, NorthConnex, WestConnex, Western Sydney Roads, Sydney Metro, Sydney Light Rail) and Victoria (West Gate Tunnel, City Link – Tulla Widening, Melbourne Metro Rail, Regional Rail Revival). Both state governments have seen significant cashflows from stamp duty in recent years and are now in the process of spending the proceeds. The focus is very much on roads, which seems a little short-sighted particularly in Sydney where there is a definite need for a legitimate metro/rail system.

There will be some significant winners from this increase in infrastructure work, the question investors have to ask is who they will be and is it already in the price. Obvious beneficiaries such as Cimic have seen their prices run hard but there is one value opportunity that we have initiated a position in recently, which is Veris.

Veris is a Western Australian based surveying company that has expanded into the East Coast via acquisition. The surveying market is highly fragmented and as the first mover with a roll up strategy, Veris has a good opportunity to grow strongly over the coming years.

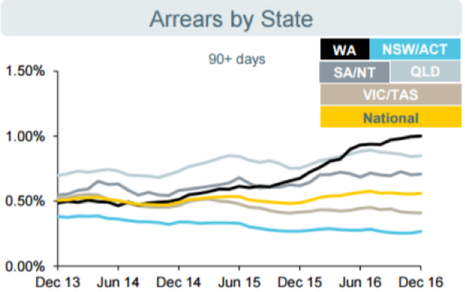

4) Will WA arrears start to hit the profit line of the banks?

The only one of the big four with a June balance date is Commonwealth Bank. Whilst the other three have quarterly updates around the same time, the focus will be very much on the details of the CBA result. To that end, one area of risk we have identified in recent times is the rising arrears within the Western Australian property book. The rise in arrears started in 2015 (coinciding with the peak in the residential construction market in WA) and has continued steadily in recent periods.

Source: Company filings

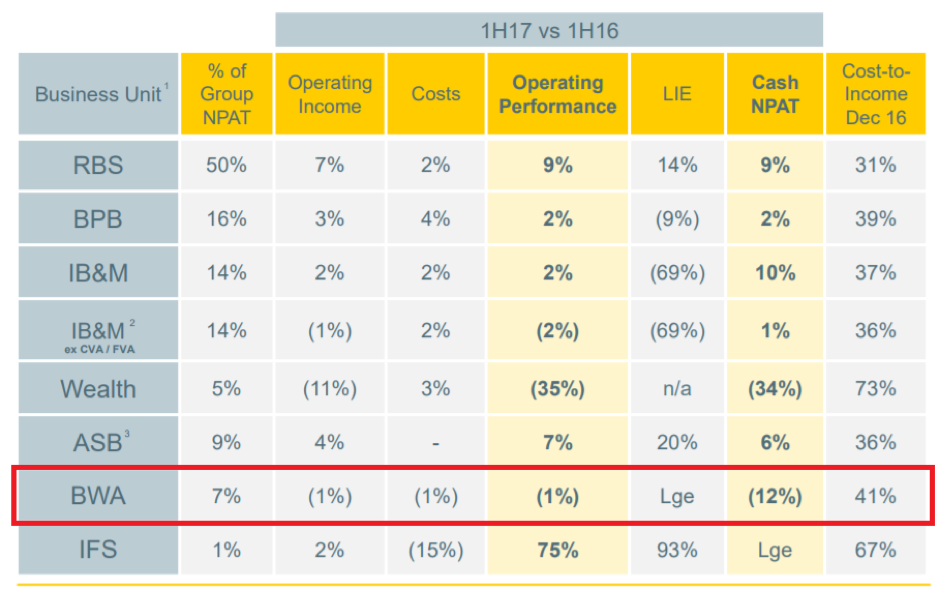

If arrears persist, they move to stressed and eventually become impaired. A large increase in impairment expense as well as a stagnating top line saw Bankwest’s cash NPAT fall by 12% in the first half of the financial year. High volume growth within the Retail Bank saved them as they grow their asset book by 8% in total over the half. The question is will slowing volume start to reveal some cracks.

Source: Company filings

The volume growth from the first half will continue to benefit earnings in this half but we’d expect the rate of operating income growth to slow in coming halves.

Ultimately, these are some of the issues will dictate the direction of the Australian Equity market over the next six months. Of course, there will be other stories that will catch us by surprise and the ongoing movements of commodity prices and the level of the currency will have an impact. Portfolio management is a 365 days a year job and we need to absorb and process information at all times, it’s just in the next month we will see a large amount hit us at once.

This week Robert Swift takes a look at the currency debate that has been raging recently. Robert takes a look at what has happened so far and how he expects equities to react accordingly. Is it time to increase or decrease your weighting towards international investments?

Investing internationally can expose you to currency risk. If the AUD$ falls against other currencies then you benefit to the extent that the value of your investment rises when translated back into AUD$. On the other hand if the AUD$ rises then the value of your investment is reduced by the extent of the decrease in the foreign currency. It is important to note that you haven’t lost money if you do not sell the position. It is only a “loss’ or ‘gain’ on the basis of adjusting prices to current market values.

Currencies fluctuate and in the short run can do so for random and illogical reasons. In the long run (5 years +) they tend to follow a more logical path which is determined by relative competitiveness in traded goods. Countries with more debt, more inflation, and less capital investment tend to have currencies which structurally decline in value.

The AUD$ has recently risen by about 5% against the US$ and the global equity portfolio has about 50% of its assets in US$ denominated stocks. This has reduced the value of the portfolio.

We consider below the reason for the increase and, more importantly, if it will it continue. Are we going to see a repeat of the commodity boom from China which drove the AUD$ over parity, and at the time caused all sorts of currency experts to predict that the AUD$ would remain there! As we said – currencies fluctuate in the short run and are notoriously hard to predict.

While equity prices could be said to behave in a predictably irrational fashion, currencies tend to behave in an unpredictability irrational fashion.

So what happened and why do we think this is nothing to worry about? You shouldn’t sell international equities nor be afraid of owning many foreign currencies.

The RBA’s Deputy Governor successfully (sort of) arrested the Australian dollar’s ascent last Friday, but while it has at least stopped rising for now, its recent surge has not been reversed as it laps at 80 US cents and 5.4 Chinese renminbi (yuan).

The US$ was faltering after a strong run as part of the ‘Trump trade’. Political gridlock in Washington (aka chaos) has removed some of the lure of the US$ and the big increase in infrastructure debt issuance at higher interest rates, now looks less likely.

The Federal Reserve is once again signalling a slow exit from zero interest rate policy and only gradual increases in interest rates. The Federal Reserve, like all central banks, is keen to keep hinting to the market what they will do and is consequently causing the volatility.

As economic news varies between a faltering USA economy and a strengthening USA economy, the US$ rises and falls with expectations of interest rate changes. In the Northern Hemisphere Summer, USA economic activity tends to be softer. Although seasonal adjustments are made in the measurement of these statistics, they are imprecise.

The RBA Board meeting minutes released recently indicated the Board viewed the neutral cash rate as around 3½% compared to a current rate of 1.5%. This was (incorrectly) taken as a hint that rates would shortly be on their way there.

The iron pre price in US$ has bounced which helps the AUD$.

Why do we think this is a temporary surge and one should remain invested in unhedged international equities?

The last thing the RBA wants is a rising AUD$. it continues to acknowledge that …“An appreciating exchange rate would complicate” the transition of the national economy away from its earlier heavy reliance on the construction of big-ticket resource projects.

USA inflation, or many components of the index, remains well-contained, and so the RBA’s capacity to switch back to a tightening bias, much less actually raise the cash rate, is limited by the extent to which they want Australian interest rates to be a lot higher than USA interest rates. We show the spread in the chart below. We are at an extreme now and a wider spread is not helpful to a smooth economic transition.

Source: Bankwest

Export item prices other than iron ore are still subdued. Note also that Chinese GDP composition will be different in the next 15 years from the last 15 years. In the last 15 years there was a lot of construction and basic infrastructure. As the economy matures there will be more services and less physical construction. To view Chinese GDP as being a predictor of commodity demand may no longer be quite as easy and analysts will have to be cognisant of this changing shift rather than simply measure the rate of Chinese GDP.

Most importantly the AUD$ is not a cheap currency. The OECD calculation of the PPP fair value of the A$, an anchor price around which news flow drives it up and down, is about $0.71. We attach that chart below.

Source: Thomson Reuters

Consequently the AUD$ at a little above fair value is not likely to rise much more. With the Australian dollar at levels above 80c, one should be investing more into international equities to attain better portfolio diversification and to gain exposure to sectors and themes not present in Australia.