This week we look to conclude the series with some insights into two more pharma companies that we believe could make for an interesting addition to investor portfolios. Both are potentially high growth and arguably further up the risk curve (if one is to define it by traditional valuation metrics).

Moderna (MRNA.NASDAQ)

This is one security that we’re quite sure most of you will have at the very least come across recently (i.e. their Covid-19 vaccine, Spikevax). Before delving further into the company however, it is probably good to start off by at least gaining a very basic understanding of the niche in which they operate; that is, in the development of RNA therapeutics.

As of today, the company’s only commercial product remains its Spikevax Covid-19 vaccine and the company has faced some governance issues, most recently in the form of board member Moncef Slaoui taking up a position as the head of Operation Warp Speed during the Trump administration and holding onto around US $10m in stock options at a time when the company received around US $483m in Federal Funding. Despite this, Moderna’s pipeline remains particularly interesting. I personally, became interested in the company in mid-2019 (so pre-Covid!) not due to its ability to tackle Covid but rather its pipeline of vaccines and treatments in relation to influenza, HIV and, more importantly, cancer (returning to one of our thematics). In particular, the company retains two potential vaccine candidates for cancer and is working in conjunction with AstraZeneca (AZN.NASDAQ) in cancer immunotherapy.

Author: Sid Ruttala

With that, lets get to the numbers (which are rather straightforward given that for now Moderna’s only commercial product remains Spikevax). Third quarter revenue of US $5bn, Net Income of US $3.3bn giving a fully diluted EPS of around US $7.70 per share. We expect the company to come up with full year vaccine sales of approximately US $21.5bn and $21bn in 2022 before tapering off. What will be interesting to watch here will be sequential revenues as the vaccinated population moves toward booster shots. On a related note, the CEO has recently suggested that existing vaccines may not be effective against the new Omicron variant of Covid-19, with the implication being that a new vaccine would have to be developed over the next six months (at the very earliest). This will certainly be the space to watch. However, what we would like to emphasize is that Covid-19 vaccines, while instrumental in propelling the company from an early stage biotech to a US $150bn company, are not the entirety of this company. The biggest change has first and foremost been the validation of its underlying mRNA technology platform and the ability to now use the cashflow generated to further speed up its work across other products and markets.

Covid-19 and associated vaccines will, we feel, be up for competition, not least from emerging markets and players. In other words, the initial windfall will not be sustainable. The more likely scenario is that revenues from this segment taper off into the low-single-digit billions annually, contingent on whether people continue to receive vaccinations over the long run (i.e. booster shots, new strains). We are also very likely to see increased competition and declines in pricing power as the sector and governments continue to adapt. So, why then do we feel that this may be a buy?

For one thing, the record-breaking speed of eleven months in which time the firm created and developed the two-dose vaccine, not only placing the company firmly in the limelight but also accelerating the development of clinical know-how and manufacturing capabilities that will pave the way for faster timelines in other products. Of these, the most significant progress to date has been concerning Human Metapneumovirus (Phase 1), Respiratory Syncytial Virus (successful Phase 1, moving to Phase 2 and 3), and HIV Vaccine (Phase 1). On the oncology front, the company continues to work with Merck (MRK.NYSE) and AstraZeneca in immunotherapy and groundbreaking personalised cancer vaccines (Phase 2, results pending in 2022).

From an investor perspective, the ability to have that number of potentially addressable markets while at the same time having exposure to growth via an existing product line is what makes Moderna a potentially lucrative investment. Typically, companies working on early stage and novel therapies do not have the ability to generate cashflows to fund R&D expenditures for consistent periods of time, especially should always inevitable unforeseen outcomes eventuate. That said, the investment is not for the feint of heart, the Covid-19 landscape continues to evolve and the company does face some uncertainty around its only commercial product line. But, with a PE of 21.61x, one wouldn’t be paying up egregiously for a potentially lucrative multi-decade investment.

Fate Therapeutics (FATE.NASDAQ)

Fate is a clinical-stage biopharmaceutical involved in cellular immunotherapies for cancer. Before proceeding further it maybe pertinent to understand a key characteristic that we look for, especially in earlier stage. That is, a niche with potential scalability. Moderna, for example, focuses on mRNA as its niche and that could be scaled up to work across multiple segments. Similarly, Fate focuses on something called iPSCs (induced Pluripotent Stem Cells). Briefly, let us first look at what iPSC technology is. It was pioneered by Shinya Yamanaka, for which he was awarded the Nobel Prize in Physiology or Medicine in 2012 alongside John Gurdon. He was able to show that the introduction of four specific genes, now known as the Yamanaka factors, could take a somatic (or undifferentiated stem cell) and turn it into pluripotent one, Pluripotent, as the name would suggest, is a cell that can differentiate into any of the three primary germ layers: endoderm (interior stomach lining, gastrointestinal, lungs), mesoderm (muscle, bone, blood, urogenital) and ectoderm (epidermal tissues and nervous system). Essentially, the discovery that mature cells can be converted to stem cells.

Think then about the potential for a company that could take a renewable pluripotent cell and then derive clonal populations? Currently the process for immunotherapy involves taking cells from specific donors with desired attributes, ex vivo modulation and then the creation of cell products for therapeutic functions. Fate seeks to circumvent then entire process and create 1) a renewable master cell line; 2) Cryopreservation which implies longer shelf-life and, most importantly for the profit motivated investor, 3) deliver it off the shelf. The potential for commercialisation and economies of scale could be substantial.

The global market size of lymphoma in Non-Hodgkin lymphoma alone could be around US $27bn. Which brings us to our first point for the not so patient investor. Although the initial results for their off-the-shelf treatment for lymphoma were below expectations, the fact that of eleven patients treated, six achieved remission seems to have been altogether missed by the market. In terms of what is in the pipeline for the future: unmet medical needs and potential off-the-shelf treatments for AML, myeloma and solid tumors. Of these, the solid tumors component seems to be the most promising with a Investigational New Drug (IND) application, for FT536, to be submitted before EOY in order to target multi-antigen targeting.

Looking at the numbers, though not particularly relevant given the early stage, revenue stands at US $11.1m. Importantly, the company has US $888m in cash and equivalents on the balance sheet (important as it indicates that a capital raise wont be necessary in the near term). Assuming operating expenses stay at current levels, $57.3m per quarter, this would imply that company has about four years worth of cash left. On the negative side, with a current market capitalisation of US $5.25bn, the market is certainly expecting a blockbuster in the near term. We would argue, rightly so.

Disclaimer: Both MRNA and FATE are owned by the author of this article.

This week we will be visiting a stock in our Global Mobility portfolio that is poised to benefit from the themes of electrification and autonomy. While these thematics are well known and are well covered, most investors look to only a few select stocks to benefit from the trends (i.e. Tesla or their favorite lithium stock). Our Global Mobility portfolio focuses on finding the companies that are forming the ecosystem around these core thematics, the companies that will benefit from these trends but are perhaps less known to the everyday investor.

Author: Adam Wolf

Aptiv (APTV.NYSE)

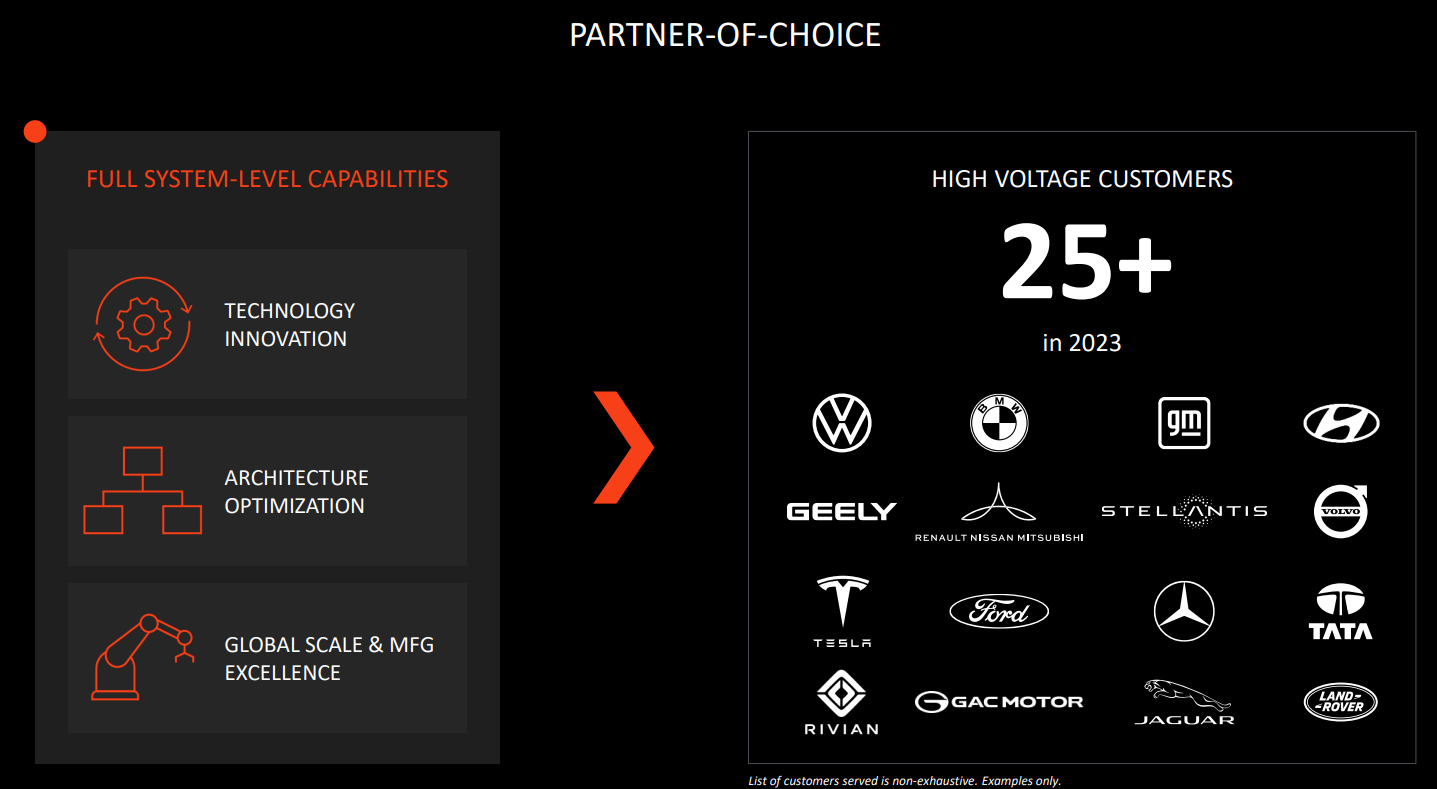

Aptiv manufactures, and sells vehicle components internationally. The company provides electrical and electronic tech products as well as safety technology solutions to the automotive and commercial vehicle markets through two main segments, the first being signal and power solutions and the second being advanced safety and user experience. Key positioning in high demand and rapidly growing industries such as autonomous driving, E-mobility, and smart vehicle architecture are likely to set Aptiv up well for the foreseeable future. Their signal and power solutions are aiming to capitalise on the need for high voltage subparts for electric vehicles.

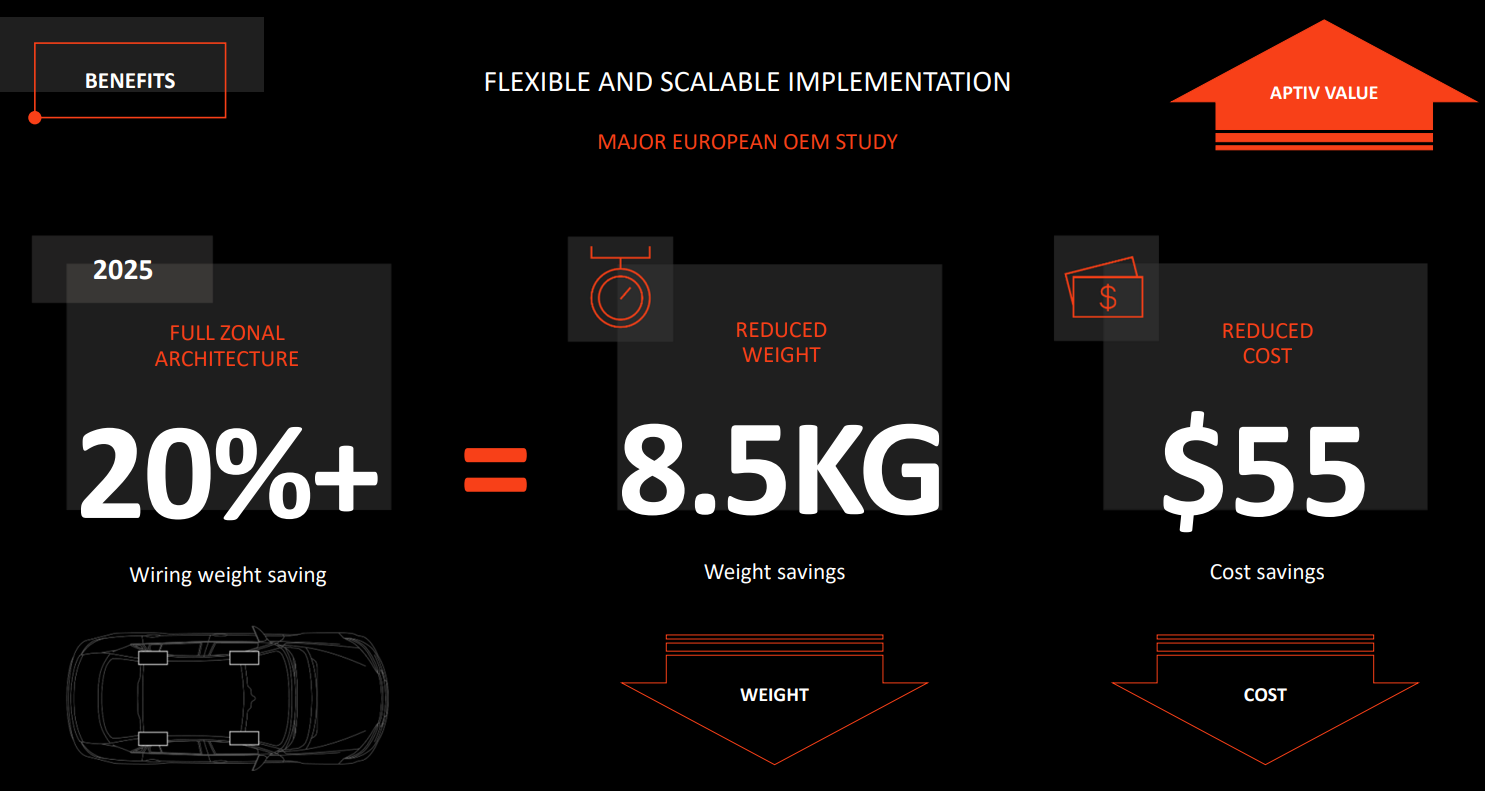

Aptiv solutions optimise electric vehicle architecture, making intelligent design trade-offs that reduce cost, weight and mass. This allows for faster democratization of technologies that reduce CO2 emissions and reduce traffic accidents and fatalities.

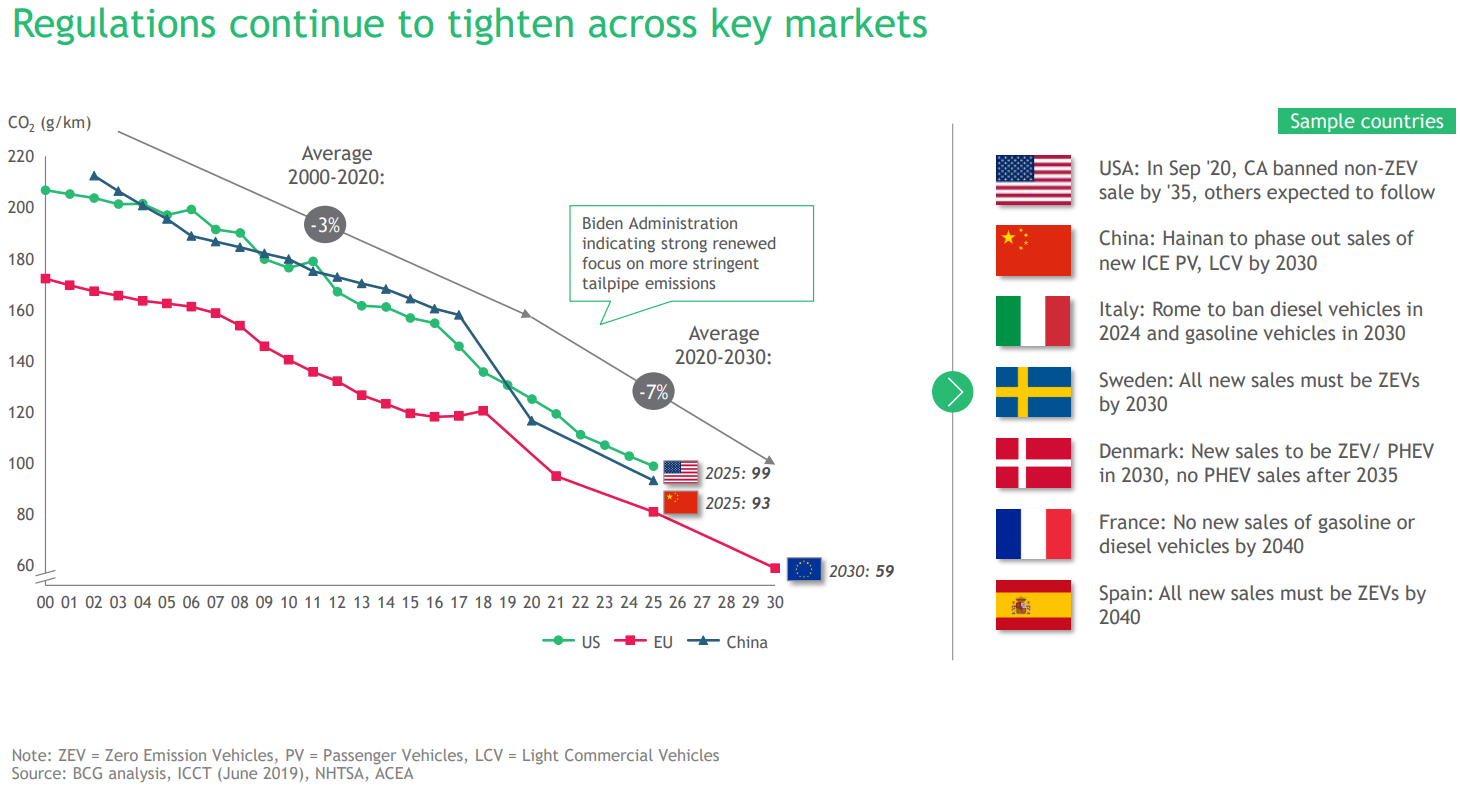

Government mandates are accelerating electric vehicle demand

We are seeing countries around the world, especially in Europe, begin to tighten various mandates on carbon emissions. Many are trying to do so before 2030. This is a huge backdrop for electric vehicles and other carbon friendly thematics such as uranium, carbon credits, hydrogen, solar/wind energy and the like. While they aren’t manufacturing electric vehicles themselves, Aptiv’s solutions are critical for the viability of electric vehicles, Aptiv are integral in reducing carbon emissions but they aren’t getting the same credit for it, especially compared to their customers.

Source: APTV company filings

High voltage

Electric vehicles are being adopted rapidly worldwide but it is still in its infancy and there are still some pressing inefficiencies that need to be addressed. Unlike an internal combustible engine (ICE), an electric vehicle needs to be charged which can be time consuming depending on which charger you are using. On top of this, they are somewhat limited in their range, a real issue until appropriate charging infrastructure is rolled out or ranges improve. Consumers are demanding faster charging cycles, which means higher voltages and currents. Higher voltages and current brings greater reliability and performance requirements, which increase vehicle range as well.

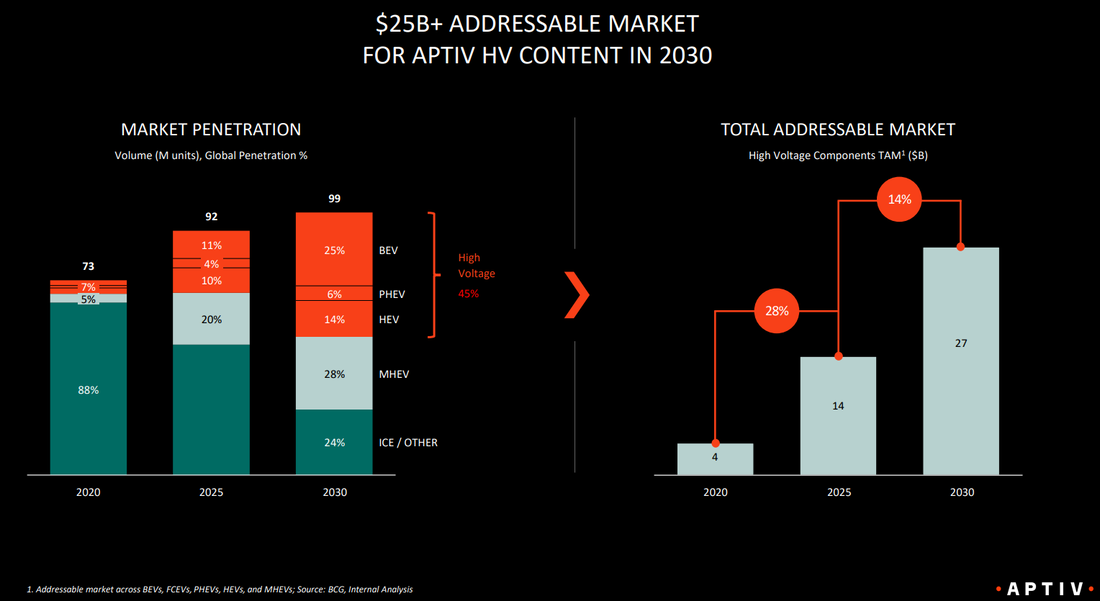

Increasing the voltage level from 400V to 800V represents the most efficient way to optimize performance. By doubling the voltage, considerably more power can be transmitted in the same time with the same current, which can lead to up to half of the charging time compared to a 400V system. When scaling up the electrical vehicles to 800V, the requirements of all sub-components change. All parts in the e-drive motor´s construction must be adapted and entire mechanical sub-systems need to be electrified, creating a huge opportunity for companies that produce these subparts to capitalise on. Aptiv estimate that the requirement for high voltage equipment in an electric car is 1.5-2.0x higher than a traditional ICE car. Aptiv have positioned themselves to be a key player in the electrification ecosystem and will benefit from the increased demand for high voltage subparts. Aptiv currently provide high voltage cabling, high voltage connectors, internal battery connections, charging cable sets and inlets, power distribution boxes and battery disconnect units.

Source: APTV company filings

Architecture optimisation

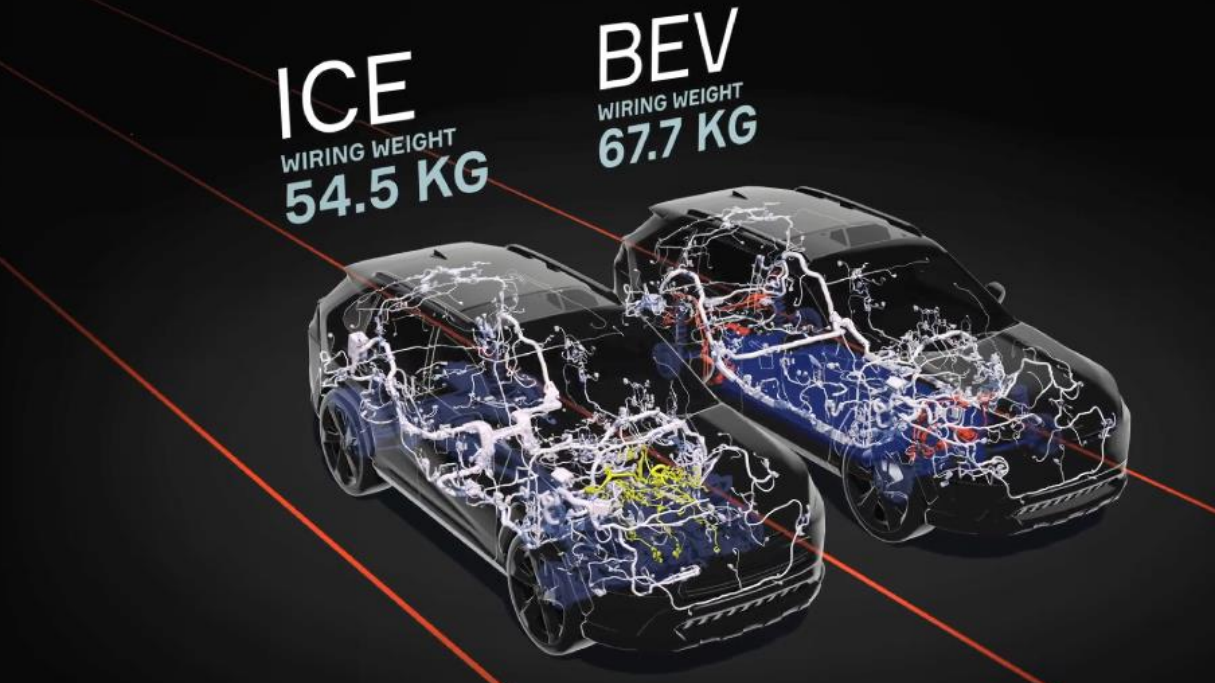

Electric vehicles require a lot more wiring and denser materials compared to an ICE. this increases the weight of the vehicle and is one of the reasons electric vehicles are more expensive. As mentioned, government mandates are currently fueling the rise in electric vehicle adoption but, in order for them to be rolled out at a mass scale, the price needs to come down.

Source: APTV company filings

Using AI and data models, Aptiv provide architecture optimisation solutions that help manufacturers save costs, reduce weight and minimise errors. Aptiv provide software solutions that break the vehicle down into zones which allows the manufacturers to break apart the vehicles physical complexity into more manageable zones and further drive up the integration of ECUs (electronic controller unit – a small device that controls the electrical systems in the vehicle), reducing the weight and lowering the total system costs in the vehicle.

Source: APTV company filings

Hyundai Partnership

Aptiv has formed a partnership with Hyundai Motor (005380.KRX), a joint venture (they have both dedicated $2bn to this JV) whose objective is to develop a robot taxi platform. The first model should be ready before year end with a new version in 2022. Hyundai Motor Group and Aptiv will each have a fifty percent ownership stake in the JV, valued at a total of US $4bn. Aptiv will contribute its autonomous driving technology, intellectual property, and approximately 700 employees focused on the development of scalable autonomous driving solutions. Hailing a ride from your smartphone is no longer new. Google’s (GOOGL.NASDAQ, owned) Waymo have been operating a fully driverless service in Phoenix for a while now. The JV’s goal is to make riding in an electric/hybrid vehicle driven by a computer system commercially viable in Las Vegas. For once, what happens in Vegas doesn’t need to stay in Vegas.

Connectivity

The technology content of vehicles has continued to rise as a result of infotainment systems, greater safety, and convenience. In order for autonomous vehicles to be fully operational, the vast majority of roadside infrastructure will also need to be connected. This involves traffic lights, sensors, cameras, road maintenance etc all communicating with each other. This will enable cars to safely travel at higher speeds, preemptively reduce their speed when necessary as well as aid in the efficient flow of traffic, preventing traffic jams. Autonomous vehicles may be widespread before this point but this will be required to maximise their benefits and efficiency. As a result of the increased amount of data, there is an increasing demand for solutions that enhance connectivity. Aptiv are developing vehicle to vehicle (V2V) and Vehicle to infrastructure (V2I) communication technologies which enable vehicles to detect and signal danger, reducing collisions and improving safety. Aptiv’s solutions will maintain connectivity to an increasing number of devices both inside and out of vehicles utilising connectivity solutions such as over the air (OTA) technology that enables vehicles to receive software updates remotely and collect market relevant data from other connected vehicles.

Investment Thesis

The past year has been a tough one for Aptiv. Widespread chip shortages and fractured supply chains are having a huge impact on electric vehicle production in general. The decline in EV production has definitely slowed down Aptiv’s growth but the thesis for broader increased EV production remains strong and, once these shortages normalise, Aptiv should have a huge pipeline of sales ahead of them. Interestingly, Aptiv tick every box in terms of the pillars we are looking at in our Global Mobility portfolio (electrification, autonomy and connectivity/sharing). Aptiv present as an opportunity to gain exposure to all three thematics in this $10tn mobility revolution and yet they aren’t one of the names you think of when talking about electric or autonomous vehicles. The management team are well aligned with shareholders and have done an exceptional job at creating shareholder value.

Source: APTV company filings

The valuation of 19x EV/EBITDA next twelve months (NTM) seems more than reasonable to us considering how big this company can truly be once the autonomous and electric vehicle industries advance from infancy. We expect EBITDA to be around $2.7bn in FY22 which would be a rise of over 30%, considering how EV production has been declining in the past year this is still a good result.

Source: APTV company filings

Electric and autonomous vehicles still have a long way to go to reach full functionality and efficiency in order to replace ICEs (and drivers themselves). Aptiv’s solutions are helping electric vehicles become more affordable and more convenient to use. Aptiv has already established a dominant position in the high voltage subpart market and, if they can capture the customers they are targeting by 2023 (most of whom are already customers), they will have a big chunk of that particular $25bn addressable market.

Aptiv have a strong position in the ecosystem enabling the electric/autonomous vehicle industry and we can see them being a market leader in their segments. In doing this they will be an integral piece of the $10tn revolution we are looking to exploit. All being equal, in a more mature industry this could mean a much larger market cap for Aptiv (currently $43bn).

Disclaimer: APTV is currently held as a long position in TAMIM’s Global Mobility portfolio. The TAMIM Global Mobility strategy seeks to to capitalise on the ongoing $7 trillion autonomous and electric vehicle revolution.

This week we continue on to the final in the pharma series by looking at specific companies that we feel are worth at least a review by investors. As elucidated last time, the categories that offer the most lucrative long-term opportunities are Oncology, Diabetes and Cardiovascular. It is with this in mind that we look at prominent or interesting players, they are DexCom, Bristol-Meyers Squibb, Moderna and Fate Therepeutics. The last two we shall leave for next week given the complexity of the issues on hand and the nuance required in explanation.

DexCom (DXCM.NASDAQ)

Author: Sid Ruttala

To sum up DexCom, the company is in the business of glucose monitoring for diabetes. A certainly lucrative market that places it front and centre in a tremendous growth category. For those that read last week, this is potentially the biggest growth category in both emerging and developed markets. So, what is the problem that the company seeks to solve?

At the risk of sounding overly simplistic, one of the biggest issues for diabetics is the ability to consistently monitor glucose levels. Traditional processes included metering (i.e. many may be familiar with strip metering), a rather ineffective process that relies on individuals to constantly stop and use test kits (using needles to prick). DexCom’s CGM (Continuous Glucose Monitoring) system is a small wearable device that sends continuous readings to a user’s smartphone.

This may be one way for investors to gain access to a growing and lucrative healthcare market while having the same advantageous characteristics of technology companies (i.e. sticky revenues). The business relies on every consumer that signs up buying higher-margin consumables for years to come, much the same way as Apple creates an ecosystem for its own products. The flipside however is that sensor technology, although the company is a first entrant and has rapidly updated its tech, faces increased competition and is not protected in the same way as Neuren, for example, with its own pharmaceuticals. What is also important to note is that DexCom’s product is consumable and has to be replaced within a period of 10 days. After this users would be required to buy again at a cost of US $349 per box (three units per box). Here we have to remember how heavily subsidised the consumers are in this space). In a way, this is effectively recurring revenue in.

So, why does this make sense?

Aside from its revenue model, DexCom continues to grow at an exponential pace. Seemingly unaffected by the ebbs and flows of Covid-19, quarterly revenues growing 30% Y-o-Y and the firm maintaining its market leadership in both accuracy and usability despite competition from industry giants such as Abbott’s (ABT.NYSE) FreeStyle Libre, which we might add is more competitively priced, and Medtronic (MDT.NYSE). On the latter, Medtronic’s own insulin pump offers an integrated CGM in conjunction with its insulin delivery. However, the fact that the company continues to retain customers and increase market share is rather telling. Moreover, its collaboration model with companies such as Tandem (for insulin release) makes it more flexible than those with a more diverse revenue model, such as Medtronic.Getting to the numbers; revenues up 30%, US revenue continues to grow at 20% while it has recently expanded into further growth markets where sustained increases of 35% are on the table. We project this to continue to grow at 35% this calendar year (above managements own guidance of 15-20%). More attractively, Gross Margins continue to run at circa. 69%. Assuming this to be correct and using a 5-year forecast period, revenue should grow from circa. US $1.9bn currently to $8.5bn. DexCom’s continued expansion into the G7 nations and smaller European countries bodes well for the future.

Red Flags & Risks: The biggest risk remains its current valuation at a P/E of 109. Nevertheless, for the growth investor the important metric to consider is potentially the Price to Sales which remains 19.46 (still a premia especially when compared to traditional competitors like Abbott or Medtronic).

Price Target over a 5-year period: US $1,500 per share (currently trading at ~$600). Assuming discount rate of 3%.

Bristol Myers Squibb (BMY.NYSE)

From a high growth, high P/E company we move onto one of the largest pharmas on the planet. Many may already be aware of the Bristol Myers Squibb (or BMS), given the company’s more than 100-year history. The good, including Presidents Clinton’s accolades and culmination in the award of the National Medal for Technology, to the not so good in the early 2000s where it was accused of maintaining a monopoly of its cancer drug Taxol (Paclitaxel), a vital prescription in the treatment of a number of cancers, from breast to cervical. It has also been an unfortunate addition to many investors’ portfolios in recent years.

So, why now?

In answering that question, let us begin with why investors have seemingly discounted the business. As is perhaps rather evident from the mention of monopoly in Taxol, BMS plays across all the segments that we feel rather bullish on, most importantly oncology and cardiovascular. What investors have seemingly focused on (and discounted) to date has been the loss of major patents across its major portfolios over the next decade, including its blockbuster oncology treatments Revlimid, Sprycel, Pomalyst and the all important immunology play Orencia. These four make up 50% of all sales. The market also continues to be rather unimpressed with its largest acquisition to date, Celgene, at a rather hefty price tag of US $74bn (to put that in context, current market cap is circa. US $128bn). We, however, see this as a crucial piece in further expanding BMS’ oncology footprint, Celgene focusing and well entrenched in blood cancer. A more recent acquisition is Medarax, for another US $2.4bn, which again cements its footprint in cancer immunotherapy (for which it remains a first-mover).

This brings us to our first point, we feel that the business has made rather astute acquisitions that should cement BMS’ leadership positions in oncology, despite the market seemingly unimpressed with the positions. Moreover, BMS also has a partnership with Pfizer (another favourite we previously wrote on) in the cardiovascular category. Aside from this point, the market continues to be seemingly unaware or at the very least discounting several new drugs in the pipeline that we believe should make up for the gradual decline in other categories as patents expire. This includes things like Zeposia (used to treat relapsing forms of multiple sclerosis) and Breyanzi (CAR-T cancer drugs i.e. immunotherapy). These drugs bring us to the second point, the business seems to be focused on higher margin/lower volume products, which we continue to love.

For those more interested in the upside, the business continues to focus on late-stage pipeline to do with cardiovascular and cancer drugs to replace and effectively be upgrades on the expiring patents. This suggests to us that the market may have this business wrong in its assumptions. We forecast that the potential earnings of new releases and upside of late-stage pipeline should more than compensate for the expected decline in earnings as a result of patent expiration.

Red Flags & Risks: As a rule of thumb, we prefer organic growth to M&A and BMS has accumulated total debt of approximately US $51.67bn (though it has been seeking to pay it down). This requires management to be almost perfect in implementation and commercialisation of its late stage pipeline for our own undervalue thesis to play out.

Price Target over a 5-year period: US $95 per share, assuming sales continue to hold up with the addition of new drugs. We expect Reblozyl and mavacamten to support an additional US $3.8bn in annual sales at peak.

This week we will be writing about one of our core holdings, one that the market hasn’t been very optimistic about. In doing this we will look at why we think the market has this one wrong. Sometimes the best opportunities come from running toward the fire and figuring out if the situation is quite as bad as everyone thinks. Often in investing, if you find yourself on the same side as the majority that’s when you should be asking yourself all the questions.

EML Payments (EML.ASX)

Authors: Ron Shamgar

Author: Ron Shamgar

The fire: EML Payments has been heavily oversold because of a dispute with the Central Bank of Ireland that could impact their European operations.

EML Payments Limited (formerly EMerchants) are the provider of payment solutions, offering payment technology for payouts, gifts, incentives and rewards, and supplier payments. EML issues mobile, virtual and physical card solutions to a number of corporate brands around the world and manages more than 3500 programs across 26 countries in North America, Europe and Australia.

Source: EML company filings

Central Bank of Ireland Correspondence

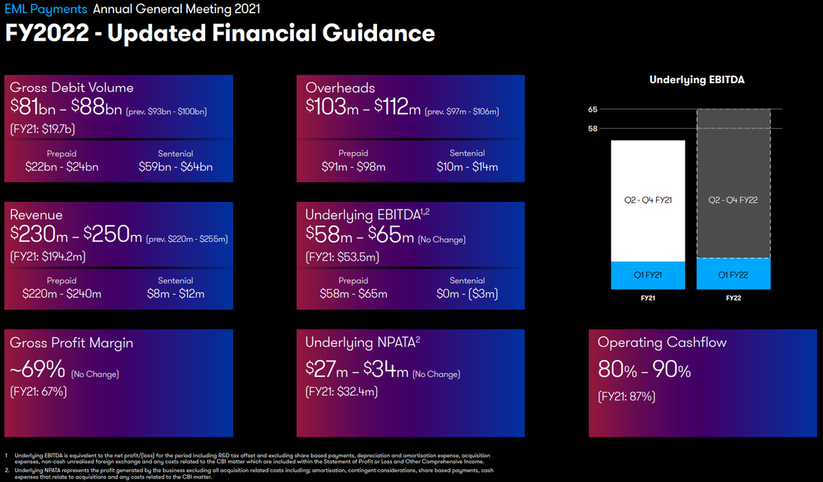

In March 2020 EML completed the acquisition of Prepaid Financial Services (Ireland) Limited (PFS), a multi award winning European provider of white label payments and banking-as-a-service technology which gave them a presence in Ireland. In May this year EML announced that there had been correspondence with the regulator in Ireland, the Central Bank of Ireland (CBI). The Central Bank of Ireland deems all e-money institutions to be high risk, and they require firms in such sectors to have very strong AML/CTF frameworks in place to mitigate that inherent risk consistent with their expectations. The Boards of PCSIL (the Irish regulated entity) and EML have endorsed a Remediation Plan that has been in progress for some months. EML is hoping to resolve the regulatory issues at the end of this year. The silver lining to this situation is that under the acquisition terms EML will save $110m (AUD) contingent on PFS achieving agreed rebased annual EBITDA targets for the three financial years ending 30 June 2021 to 2023, reflecting growth of approx. 20% CAGR.

EML has completed 45% of Level 1 tasks as at the end of October and we are expecting another update before the half year results. So far, the CBI has found zero breaches of AML or CTF. Our view is that the CBI is reluctant to regulate a high growth fintech like EML and is making life difficult in the hopes that EML moves on to another regulator in Europe.

While this undoubtedly has a material impact on the business, we saw the share price fall 50%, from $5.76 to today’s price of ~$2.75. This fall wiped $1bn worth of market cap off EML; we think this is too much. EML’s management team has proven that they are good at managing issues over the years as they have done with both Covid-19 and Brexit. We are extremely confident that not only will the CBI issue get resolved but that EML will transition away from the CBI and into another regulated jurisdiction like Spain or France (where they already operate). We estimate a 4-6 month time frame. Their recent AGM update tell us a different story than the one painted by the market.

AGM Update

Last week, at their AGM, EML provided an operational update for Q122. EML were able to affirm guidance for FY22, the market was clearly expecting that this would not be the case. The company noted that in Q122 it signed 23 contracts and launched 64 programs, ending the quarter with 114 programs in implementation globally (including 36 on hold due to the CBI issue). The business has still been able to grow and maintain guidance despite the issues with the CBI.

For example, management has replaced high volume-low margin programs with the CBI in order to make room for the 36 on hold high margins programs. This should be approved shortly. They also announced a new deal with Banco Sabadell, one of the largest banks in Spain, operating in twenty countries including the United Kingdom and Mexico. We expect to see more deals like this in Europe which should more than compensate for the delayed CBI contracts. Given the huge pipeline and growth in the business, the CBI issue is now potentially a significant upside scenario if successfully resolved.

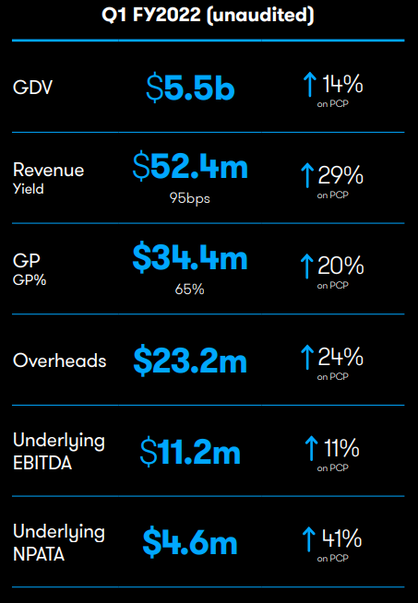

EML reported gross debit volume (GDV) growth of 14% Y-o-Y in Q122, with increases across all three divisions. An increase in the group yield (Q122: 95bp, Q121: 84bp) resulted in Y-o-Y revenue growth of 29%. Their EBITDA guidance for FY22 (including acquisition costs and costs related to CBI) is $42.2m, $10m or 30% above FY21.

From a business development perspective, EML ended the financial year with 313 deals in their pipeline which we believe represent potential GDV in Years 3-4 post-launch of approximately $10.5bn. Their historical win rate for new business is approximately 40%. Using their historical GPR yield, this would generate an incremental $40-50m in revenue in 3-4 years.

Source: EML company filings

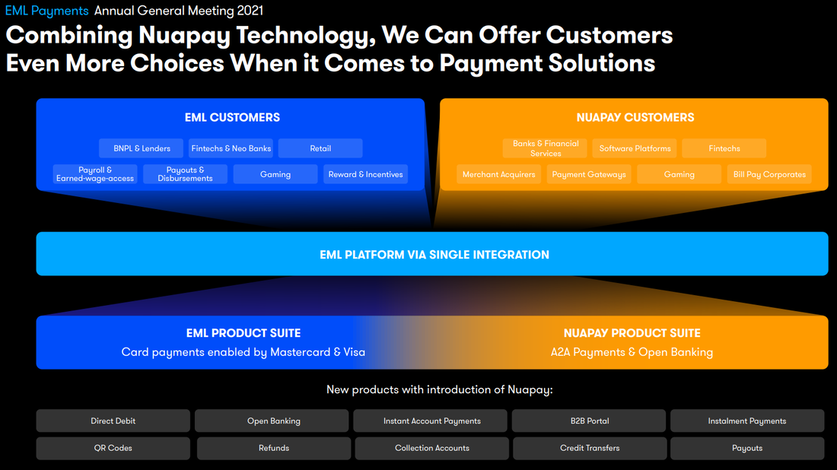

Sentential Acquisition

EML recently acquired Sentenial. Sentenial own Nuapay, a market leading open banking platform processing Account-2-Account payments. This broadens EML’s payment offerings to include alternate (non-card, non-scheme) payment products on their platform to address customer demand, complementing card scheme based payments. Sentenial is currently connected to 1,750 banks across Europe and growing. Open banking is not well understood by Australian investors, but it is the future of payments and it will bypass the rails of Visa and Mastercard. This is why both giants are scrambling to acquire any open banking data provider at ridiculous valuations.

Source: EML company filings

Nuapay is capitalising on the Open Banking functionality for pulling funds direct from their customer bank accounts. They can use Open Banking to identify, upfront, if the customer is a legitimate customer or represents a higher credit risk. Additionally, they can factor that into their own unit economics. For example, one use case is a lender, using Open Banking data, can determine how much it wants to loan to a customer and having EML provision that loan instantly through a digital wallet on their phone. Open banking is expected to grow at a CAGRs in the range of 10-50% a year.

Rising Interest Rates

EML currently have around €2bn from cash received from stored value account holders. Whilst this comes with a corresponding liability, the cash is invested in high quality bonds and all the interest earned from this cash goes straight to the bottom line. For those that are predicting inflation and a rise in rates, EML should be a beneficiary. For example, for every 1% rise in interest rates we estimate that it will add €20m to EML’s bottom line.

Outlook

EML’s recent update was far more positive than the market was pricing in, yet the share price has only gone down. EML is now trading at lower multiple to its peers and sitting on half the market cap it was before the CBI issues, even though their FY22 guidance has been reaffirmed which should see a 30% increase in EBITDA. Their pipeline is huge at $10.5bn and their recent acquisition of Sentenial and their contract with Banco Sabadell gives them a huge presence in Europe. Heading out of lockdown and into Christmas they should also see an increase in their gifts and incentives segment. As a result of the huge sell down, any downside in resolving the CBI issues has more than been accounted for. At this point, there isn’t much risk if these issues can’t be resolved and any positive news out of the CBI is all upside. EML is sitting on an EV of around $900m, we think EML will do at least $80m of EBITDA in FY23 which will put them at a forward EV/EBITDA of around 11.5x. It may take time but the market will get it right. Our valuation is $4.50

UPDATE SINCE TIME OF WRITING:

Today, 25 November 2021, EML updated the market on the CBI issue. The CBI will permit PCSIL to sign new customers and launch new programs while staying within the material growth restrictions. PCSIL is confident that it can meet these obligations. Broad based reductions in limit controls on programs will not be imposed.

As mentioned throughout this article, this was a unique situation where the downside was fully priced in at this point. The announcement today should see these issues appearing in the rear view mirror.

This week we continue to look at the global pharmaceutical industry. More specifically, this week we will be looking to identify some of the trends and segments which may produce some more lucrative opportunities.

Author: Sid Ruttala

Before we begin, a quick recap of the main points from last week:

Over the past few decades the industry has been characterised by exponential declines in overall IRRs for new products;

The above scenario can be attributed mainly to increased regulatory and compliance requirements which have incentivised massive consolidation in the space along with greater focus on maximizing the potential monetisation of existing patents;

This is despite the fact that in nominal terms global biopharmaceutical R&D expenditures continue to be an outlier in comparison to even the defence and software sectors. This can mainly be attributed to significant cost increases as opposed to real growth though.

Finally, this has also created certain unique characteristics such as public, private and academia collaborations (most recently seen in the development of the Covid Vaccines) as well as success stories such as India which has become the powerhouse when it comes to manufacturing capacity and generics.

At this point, many may be arriving at the conclusion that this seems to be an argument against investing into pharma. So, why then do we feel that this is one sector that may have legs? We shall begin by returning to our base case scenario around inflation and rationalise why pharma, and biotech in particular, makes sense.

Think for a moment about a company that is undertaking R&D. Given what we just mentioned around associated costs, it is likely that a significant proportion of their financing comes via the issuance of debt (rarely is it the case that, outside of the majors, biotech companies in their infancy have positive cash flows). Similar to our thesis around listed property, issuing debt, especially longer duration and locking in rates, is effectively a transfer of wealth away from debt holders to equity holders. Moreover, once a firm passes from the R&D stage to actual commercialisation (assuming that it doesn’t make itself a takeover target, consolidation is a hallmark of modern pharma), this effectively creates a double tailwind for equities investors.

Let’s also consider the actual attributes of intellectual property in this particular instance. IP protections effectively ensure that no one else can compete against a particular product line for a given period. In real terms this means it is behaving the same way and has the same scarcity value attributes of precious metals. In effect, if inflation is rising then a seller (of IP) just adapts the asking price and valuation in a much more fluid manner than would otherwise be the case.

Last but not least, the attribute that is most prominent and which most people may be aware of is the inelasticity of demand. That is the change in quantity demanded in relation to the price. In the absence of regulatory intervention and assuming patent protection (which is effectively the highest barrier to entry imaginable), healthcare expenditure is potentially the best inflation hedge possible. In fact, one favourite piece of research is one conducted by Mark Hulbert which showcases that healthcare beats any other industry, including the gold miners or bullion which most people are familiar with. The logic is rather intuitive. With the exception of elective procedures, consumers don’t have the opportunity to turn down medical care because of price increases. The most infamous recent example of this being Martin Shkreli (currently in prison for securities fraud), hiking the price of a life saving AIDS drug from $13.50 to $750 in 2015. Consider the nominal increase in medical care expenditure since 1948, the multiple increase over the period is 40x while the increase in official CPI over the same period is 12x.

But what if we’re wrong about inflation? A rather valid and pertinent question to ask. Even here, we feel that recent events have presented a turning point for the industry overall. Covid has shone the limelight on just how global and interconnected supply chains have become. Take the policy response in India which, as previously alluded to, manufactures approximately 50% of the global vaccine supply. The bipolar response of the central government which, much like the Trump administration Stateside, continued to hold election campaigns and enabled religious festivals (after taking a stellar initial response). The flip side of this scenario was that the second wave of the virus effectively crippled that nation’s ability to export its vaccine supply (which many emerging markets were relying on). The point here? We will likely see increased government support to subsidise and reshore certain manufacturing capacity. A certain tailwind, especially for the consolidated top end (including Pfizer which we spoke of last week).

Sticking with the topic of viruses and vaccines, resistance to second and third-line antibiotics is expected to be around 70% higher in 2030 (compared to 2005 in OECD countries). This, combined with a lack of new drugs and patents, will create a catalyst for the sector going forward. In essence, Antimicrobial resistance (AMR) will, even on conservative modelling, result in the death of approximately 10m people p.a. globally if current approval trends and increases in resistance exceed approvals. This creates another tailwind, not only in increasing regulatory efficiency for, if Covid has proven anything, it can be rather more efficient and timely in the presence of emergencies. Using current trends, even with AMRs, we are headed towards one.

Moving away from vaccines, some interesting and lucrative trends that are likely to play an increasingly prominent role are diabetes, oncology (cancer) and cardiovascular/respiratory, all of which we feel will continue to grow at exponential rates globally. On the first front, the changing eating patterns in emerging markets, incorporating more processed food and foods higher in sugar and salt, ensure that we should see a double digit growth when it comes to the diabetes segment. India, for example, is expected to roughly double its diabetic population between 2017 and 2025, from approximately 72m cases to 134m. According to the International Diabetes Foundation in 2019, “approximately 463 million adults (20-79 years) were living with diabetes; by 2045 this will rise to 700 million.” In an amusing yet somewhat twisted example of capitalism, “Nestlé would sell a problem with one hand and a remedy with the other”. With, amongst other things, their Nestlé Institute of Health Sciences, they are both enabling and profiting from the problem but also looking to enter the market for the treatment.

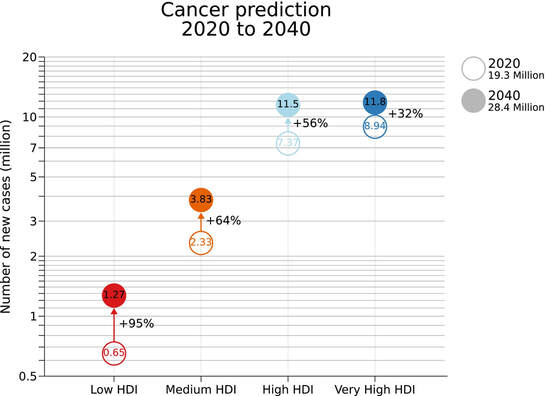

Oncology, given the nature of the issue, is potentially the highest margin segment; global revenue for the oncologics segment stands at an astonishing US $99.5bn.

“Worldwide, cancer incidence rate has increased to make it the second leading cause of death after cardiovascular disease. Environmental factors, such as tobacco smoking, urbanization and its associated pollution and changing diet patterns together with increased wealth associated with better medical services and extended postreproductive life span, have been considered responsible for this phenomenon.”

”Overall, the authors predict cancer incidence rates/risk to stabilize for the majority of the population; however, they expect the number of cancer cases to increase by >20%.”

Cardiovascular/Respiratory is one segment that should also continue given obesity rates across the West and smoking habits in emerging markets. The flip side of big tobacco being squeezed out of developed markets has been an increased focus on poorer countries. In fact, over 80% of the global smoking population comes from Lower to Middle Income Countries (LMIC). On a side note, the readership may be interested to read about British American Tobacco’s (BATS.LON) rather interesting legal approach to Kenya and Uganda when those nations undertook efforts to decrease smoking. On this third front, a more nuanced approach has to be taken given that the vast majority of the growth in respiratory conditions are likely to come from emerging markets like South East Asia. The pricing power and companies to benefit will be substantially different. Here it may be more effective to look towards generics manufacturers or third party manufacturers.

So, let’s sum up some key attributes that investors should look for given what we have covered so far:

Look for companies with significant patent protections and ones that operate in markets that have less regulatory intervention when it comes to pricing. In markets such as Australia or the EU, an interesting angle may be to find companies with organ drug designations. These patents protect companies that go after rare diseases and give longer term protection. One company owned personally is Neuren Pharmaceuticals (NEU.ASX) which has an interesting pipeline targeting Rett Syndrome and Fragile X, both rare but significantly debilitating conditions for adolescents. If the company does succeed in trials, it will have 7 years of exclusivity in the US, for example, in the distribution and marketing of these drugs.

Look at the duration and nature of the debt on the balance sheet in conjunction with the nature of the eventual revenues. Moderna (MRNA.NASDAQ, owned), for example, continues to hold US $603m, a figure substantially higher than its counterparts in biotech. But, assuming it continues to hold its revenue run rate, this should not be an issue. Though the same cannot be said for its valuation at US $93.4bn, which seemingly prices it for perfection. Despite this, I continue to hold personally given their exposure to MrNA therapeutics in the Oncology and Cardiovascular categories.

Stick to the more lucrative categories of Oncology, Diabetes and Cardiovascular. These categories are not only relevant due to the number of people they impact but because of the nature of the markets they are prevalent in which remain lucrative. So, while viruses such as HIV may still have a massive impact on emerging economies and vast swathes of the global population, especially Africa, the ability to price is quite limited. Put another way, cancer’s continued prevalence in developed markets makes it a margins game whereas diabetes and cardiovascular is both margins and growth. That is, greater pricing power combined with volume growth in markets such as India and South East Asia. Some personal favourites: Fate Therapeutics (FATE.NASDAQ, owned) for oncology, DexCom (DXCM.NASDAQ, owned) for diabetes, Bristol-Myers Squibb (BMY.NYSE) for cardiovascular.

Outside of the three aforementioned categories, there is also much to be said for generics manufacturers who are able to get licensing agreements and scale across emerging markets. Here we are looking at not particularly high margins but great growth potential. Some firms that remain interesting are Sun Pharma (SUNPHARMA.NSE, owned), Lupin Pharmaceuticals (LUPIN.NSE, owned), Biocon (BIOCON.NSE, owned) and Cipla (CIPLA.NSE, owned). All of these working across the lucrative categories but playing the lower cost and poorer markets.

Next week we take a more in-depth dive into a number of the aforementioned companies including Moderna, Fate Therapeutics, DexCom and Bristol-Myers Squibb. Following which we shall conclude with a few of the generics manufacturers.

Disclaimer: Author holds a position in a number of the companies mentioned in this article, all have been disclosed.