Australian small-cap shares aren’t normally household names and don’t get the same media attention as the big banks and miners that dominate the ASX 200.

However, keen investors can find opportunities in these smaller companies for better returns than blue-chip regulars like BHP (ASX: BHP) and Commonwealth Bank (ASX: CBA).

With reporting season in full swing, we take a look at two holdings from within our diversified TAMIM Fund: Small Cap Income that are maintaining positive guidance for the remainder of 2023.

Helloworld Travel Ltd (ASX: HLO)

Source: Helloworld.com

Helloworld Travel’s share price rebound accelerated this week. After falling in 2022, Helloworld stock has gained 74% since the start of 2023 while the All Ords has risen 6%.

Helloworld Travel is a leading Australian & New Zealand travel distribution company, comprising retail travel networks, corporate travel management services, destination management services (inbound), air ticket consolidation, wholesale travel services, and online operations.

The company released 1H23 results on Monday, detailing three times more transaction volume than the prior comparable period (pcp).

Here are the highlights from the company’s results:

$1.2 billion of total transaction volume (TTV) – up 209% on the pcp

$73 million total revenue from continuing operations – a 151% leap on pcp

$13 million of operating earnings (EBITDA) – rebound from a close to $8 million loss

Net profit after tax (NPAT) of $1.6 million – a flip from a $15.2 million loss from pcp

A strong balance sheet with $83.8 million of cash and no debt.

2 cent per share fully franked interim dividend declared

Travel is back

The entire travel sector has been riding a post-COVID boom, with demand and prices riding high. Visit any airport and you realise how much Australians want to travel, despite the impacts of interest rate rises and inflation.

The demand is surging across Helloworld Travel’s international operations too, with $178 million of TTV from New Zealanders – up 359% while Fijian operations also saw over 22 times more TTV last half.

The company said demand for the services of its network agents has continued to outstrip agent availability.

Helloworld chair Garry Hounsell commented on the results and outlook, writing:

“[TTV growth] reflects the strong demand from the travelling public, domestic and international borders returning to normal, Helloworld’s strong product offering, and the incredible efforts of our agency networks to service their customer base.

Booking volumes are expected to continue to increase as prices normalise and capacity returns with airlines and tour operators continuing to onboard further resources to meet demand.”

As a result of the strong first-half figures, Helloworld has upgraded its earnings (EBITDA) guidance to between $28 million and $32 million for the 2023 financial year.

PeopleIn (ASX: PPE)

Source: Peoplein.com

TAMIM fund manager Ron Shamgar currently thinks highly of PeopleIn because of Australia’s historically low unemployment rate, its reaffirmed FY23 earnings guidance, and relatively low valuation.

The company released 1H23 results on 17 February, highlight by record __ and a strong outlook.

Here are the key takeaways:

$597.3 million in revenue, up 89% on the pcp

$13.8 million of net income, a 223% jump from pcp

Profit margin up to 2.3%, bettering the pcp margin by a further 1%

Earnings per share (EPS) of $0.14, up from $0.045 in 1H22

PeopleIn is in the business of sourcing staff for its clientele, primarily temp staffing through the use of contractors. These include appointing supplementary nurses, labour hire, IT contractors and some niche areas including a focus on the PALM scheme and indigenous placement programs.

The company stands to benefit from positive operating conditions including, continued acute shortage of labour and strong market opportunity. PeopleIn’s share price fell just over 30% in 2022 and has seen choppy trading in 2023 despite the positive results and outlook.

This has led management to conduct a strategic review with the following rationale:

“The PeopleIN Board considers that the recent share price performance does not reflect the record financial results for FY22 or the fundamental strength of the business and has therefore decided to undertake a strategic review to evaluate options available to maximise shareholder value.”

“We are pleased to announce a record result, which was driven by strong organic growth across our core businesses and favourable industry tailwinds, including record low unemployment.

Based on the operating results for the first half and the mid-range forecast for economic conditions to continue, PeopleIN expects this strong momentum to continue into the second half of the financial year.”

With all analyst coverage signalling PeopleIn to be a buy to strong buy, a multiple of only nine times FY23’s estimated earnings and a potential grossed-up dividend yield of 7%, the market might be overlooking the upside potential of this small-cap company.

We continue sticking to the insurance thematic this week by looking at the other giant in the Australian market: IAG. We will continue using the same template as last week in assessing this business and its reports. The simple/straightforward equation: Profit = Earned Premium + Investment Income – Incurred Loss – Underwriting Expense.

Earned Premium

We’ve previously written about IAG and how it seems to have a parallel story to its competitor Suncorp. For one, this business also saw a transition in senior management with the retirement of its long-standing CEO Peter Hammer, who was replaced by the group’s CFO yet again. There is a common thread where margins are tight, CFOs tend to get preference. Nevertheless, let’s look at the results for the year, top-line growth again being our biggest issue previously.

On this front, the business has performed reasonably well, with gross written premium (GWP) for Home growing 13% while motor performed at a reasonable 8%. NZ added another 9% to growth on local currency terms. These numbers align with its counterpart Suncorp which saw higher numbers across motor and NZ. What was interesting for us was not this top-line number but how much of this accounted for premium increases vs. underlying customer growth. On this count, IAG does not compare particularly well with Suncorp, with the higher amount of its GWP growth driven primarily by rate inflation instead of member growth. However, the group has indicated quite ambitious targets for the coming year.

So on the first part of the equation, the business gets a manageable pass.

Investment Income

Again this is one aspect where the tailwind has been apparent for the business. The business now has an AUD $12 billion investment portfolio with a gain of AUD $80 million in technical reserves driven by higher yields and narrowing credit spreads. With the Fed and RBA likely to continue on their trajectory, we will probably see this increasingly grow. The yield on these funds is circa. 3.7%. Regarding shareholder funds, around 23% of the portfolio is weighted toward growth though there has been substantial derisking following exits from hedge funds.

On this front, as compared to Suncorp, the firm’s investment mix leaves much to be said, given that the total yield remains lower by 140 bps (though a like-for-like comparison is a little on the creative side, given the substantial differences in the underlying business). Again, assuming the status quo in central bank policy, we should continue to see the increase in yields.

We rate the company as a pass on the second part of the equation.

Incurred Loss

Just a refresher, the definition of incurred loss is the total benefits paid to policyholders during the current year plus changes to loss reserves from the previous year. Here it is perhaps appropriate to break this definition down into two components. The first is the benefits paid, which, more often than not, has a lot more to do with external events outside of the firm’s control and the loss of reserves (which indicates the extent or certainty to which the firm forecast future loss).

Like Suncorp, the business continues to battle the weather, with NZ floods taking away and putting pressure on margins. 1H ’23 perils have come in around AUD $70 million above estimate, and inflation is significantly impacting claims, especially in the motor segment. While IAG has a broader geographic segmentation than Suncorp, the La Nina weather cycle has still significantly impacted overall losses.

This brings us to the second part of the definition, which is the firm’s ability to adequately forecast and manage its risk profile (hence reserves). Despite the lack of geographic concentration in the same manner as Suncorp, the firm’s actuaries still have much to answer for, given the lacklustre performance in forecasting the increasing frequency of climate-induced perils. This is not the exception to the rule but rather becoming more habitual. On this front, the firm could certainly have done a better job.

We still give the firm a moderately good rating on the third part of the equation, not for any reason to do with its risk management practices but purely based on its greater geographic diversification. Also, its lack of legacy issues makes it a pure-play insurance provider (Suncorp has been operating the bank in addition).

Underwriting Expense

This brings us to the final part of the equation, and similar to Suncorp, with an Ex-CFO in charge, we should expect some reasonable performance. We were however disappointed that while expenses have declined by about 9.9%, additional outlays were required in what was categorised as the cost to transform expenditure, increasing 41.9%. For those unfamiliar, IAG has been (in)famous for legacy issues, including failed IT systems, provisions hits and charges. We would still have liked to see a greater decrease in the absolute number. We become rather cynical when businesses use words or synonyms like ‘transformation’, ‘strategic’ or words of that nature, especially when the business is being run by an accountant (i.e. new categories are not a particularly good look).

On the insurance trading ratio (standing at 10.7%), the business also fails in comparison to Suncorp, though again, it may not be fair given its quota-sharing agreement with Berkshire, to whom it will give away the lion’s share. That is, the firm effectively gives away close to AUD $3 Billion of its AUD $3.5 Billion in premium income for a 32.5% quota share. This does significantly derisks the firm as a tradeoff.

Still, overall, we give the business a fail.

Overall Outlook & Growth

The business stands to benefit from the broader tailwinds associated with a rising interest rate environment and premium escalation. That said, we think the business could do a lot better when it comes to a like-for-like comparison with its competitor Suncorp. As a pure-play insurer that had significantly derisked (especially in quota sharing), one could understand why it may have struggled. We don’t recognise preventable issues such as prudent allocation of reserves, a more conservative allocation of its investment portfolio and, quite simply put, a basic understanding of modern IT systems.

Would we still buy it?

From a pure valuation perspective, we still think it’s a reasonable allocation especially given that the insurance market remains a duopoly and the fact that it has a good geographic diversification. An average business at a great price is the best way to put it. We see the possibility of a price target or significant upside of 20% from where it is trading today ($5.80).

Disclaimer: ASX.IAG is currently held in TAMIM portfolios.

Global equity markets began the year with a wave of optimism. The MSCI World Index added 7.1% during the month, while the S&P/500 added 6.3%. Inflation appears to be abating, allowing central banks to taper interest rate hikes soon. China’s emergence from a three-year global hiatus is positive for global growth, particularly with Europe and the United States potentially heading into some level of downturn.

Today, we will be sharing three companies from the TAMIM Global High Conviction Fund. All three are profitable, trading at compelling valuations and are focused on returning profits to shareholders. As always, keep in mind the companies form part of a broader portfolio and are not recommendations.

1. eBay Inc (NASDAQ.EBAY)

Global e-commerce platform eBay connects sellers of new and used goods with buyers. Like most retailers, eBay benefitted from the pandemic as shoppers were forced online and households built up excess savings. The share price retreated significantly in 2022 as this unwound. However, the underlying business has proven far more resilient. Revenue is expected to fall marginally, while eBay has improved its take rate and bought back shares.

eBay’s growth strategy centres on “enthusiastic buyers”. This cohort of customers shops frequently, has high order value, and spends 30 days a year on the site. The website has become a destination for high-quality second-hand goods, including refurbished electronics, trading cards, sneakers and motor vehicle parts. eBay has also enhanced its platform through authenticity guarantees and certifications of purchase. Other positive moves include digital wallets and a focus on advertising revenue.

eBay’s share price gained 19 per cent over January. Still, the company is priced for demand to fall significantly, trading on a price-to-earnings multiple of 12 based on non-GAAP earnings. The business also trades on a dividend yield of 1.8 per cent, with a 20 per cent payout ratio implying plenty of headroom to increase this over time.

2. General Dynamics Corporation (NYSE.GD))

General Dynamics is a global aerospace and defence company based in the United States. The business offers a range of products and services for marine systems, land combat vehicles, weapon systems and munitions, technology and business aviation.

During the month, General Dynamics reported fourth-quarter and full-year earnings. Earnings in 2022 were USD $3.4 billion, up 4.1% from the prior year, on a healthy operating margin of 10.7%. What impressed us was the cash performance of the business. Cash from operations represented 135% of earnings, indicating that accounting profits turn into real cash for shareholders. This allowed the business to reduce debt by USD $1 billion, invest USD $1.1 billion in capital expenditure, and return USD $2.6 billion to investors via dividends and share repurchases.

Management noted a strong order book, with a backlog of USD $91.1 billion. This is the largest in company history and represents more than two years of revenue. At the midpoint of guidance, it expects earnings per share to increase by 3.6% in 2023.

We expect demand for General Dynamics products to be robust going forward, with nations prioritising defence capabilities in light of Russia’s invasion of Ukraine. NATO’s intention for 2% of GDP to represent the floor of defence spending, with some countries pushing for higher, is a clear example of this. The recent AUKUS deal between Australia, the United Kingdom and the United States is another positive tailwind. Trading on a price-to-earnings multiple of 19 and a dividend yield of 2.2%, we believe this is an attractive valuation for a company with strong cash and shareholder returns.

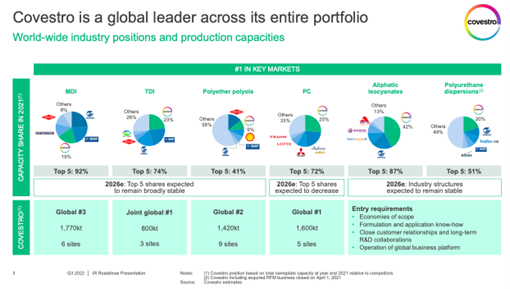

3. Covestro AG (ETR.1COV)

Covestro is a German producer of polyurethane and polycarbonate-based raw materials. More simply, Covestro produces precursors for plastics, foams, adhesives, coatings and films to support end markets, including automobiles, furniture, constriction, electronics, cosmetics and healthcare. Shares in Covestro were sold off last year as the business faced the prospect of high energy prices, limited supplies of inputs, economic and political instability, and ongoing inflation. In January, the company provided a preliminary update on its full-year results. It missed analysts’ expectations regarding accounting earnings, but we were pleased with revenue and free cash flow results, which are more representative of the underlying business.

Covestro commands leading market share positions in several material markets, including MDI, TDI, polyether polyols and polycarbonate. It achieves this by spending upwards of EUR 900 million on research and development each year. Barriers to entry are high, with new competition deterred by the significant upfront capital cost and required operational know-how.

Covestro is forward-facing, creating new products which are lighter, more durable and better for the environment than incumbent offerings. For example, it has developed new insulation materials to improve the shelf life of food. It’s also exposed to future industries such as electric cars, which require 2-5x more polycarbonates than conventional vehicles. The company is committed to becoming climate neutral by 2035 regarding its scope 1 and 2 emissions. With a share buyback program currently underway and an aim to double sales by 2025, we believe the future is bright for this essential materials company.

With the RBA lifting rates another 25 bps this week, we look to a business that has steadily benefitted from the current rate environment. Suncorp. A company that seems to be in the midst of a long-awaited turnaround.

Before we proceed further, let’s set the context. Insurance is a straightforward equation that can be summed up as follows: Profit = Earned Premium + Investment Income – Incurred Loss – Underwriting Expense. It is with this in mind that we assess how Suncorp has fared.

Earned Premium

The insurance industry in Australia is a somewhat competitive environment, it has also seen heavy consolidation over the last few years. When we last wrote on Suncorp in 2021, top-line growth was our biggest issue. With changes to senior management, including the promotion of the CFO to the top job, concern remained around the new strategy going forward. On this front, Suncorp has performed relatively well. GWP (Gross Written Premiums) are on a significant double-digit growth trajectory. Specifically, home insurance was up 12.1% and 11.7% in Motor, while NZ increased another 12.2%.

This shows us that the business is on firm footing and momentum-wise. At the same time, we do see this slowing down given base effects, primarily since much of the growth was driven by solid premium increases (i.e. a particularly trying time in relation to natural hazards), while Motor also reflects elevated underlying claims inflation and higher sums insured. On the latter point, assuming our base case is that inflation starts to come down, we should also see a flow-on impact on premiums.

Nevertheless, the overall result has shown that management’s strategy seems to be working.

So on the first part of our equation, Suncorp gets a pass. We now move on to the second part of the equation; investment income.

Investment Income

This is perhaps the most apparent tailwind that most might think of when it comes to rising rates and the impact on an insurance business. Despite the volatility in investment markets through the course of the year, the firm’s prudent allocation, especially in relation to ILB (Inflation Linked Bonds) and investment grade, has meant that:

1) It has provided an offset to claims of inflation

2) Increased the average yield on insurance funds to above 5%.

Assuming that we continue to see a hawkish tilt to central bank policy, the increase in yields should, in our view, continue to more than offset mark-to-market losses on risk-free bonds (i.e. treasuries) and breakevens.

The bank continued to prudently decrease exposure to equities while increasing exposure to infrastructure and property assets. It must be noted, however, that on the latter, the investor has to be a little more discerning (i.e. revaluations). Overall a stellar result and one that shows that the strategic allocation of the business is both prudent and well-suited to the current environment.

On the second part of the equation, we would rate exceptional. We now move to the third part, Incurred Loss.

Incurred Loss

Let’s go to the definition first. The definition of incurred loss is the total amount of benefits paid to policyholders during the current year plus changes to loss reserves from the previous year. Here it is perhaps appropriate to break this definition down into two components. The first is the benefits paid, which more often than not, has a lot more to do with external events outside of the firm’s control and the loss of reserves (which indicates the extent or certainty to which the firm is able to forecast future loss).

On the first point, the business continues to battle the weather gods. The La Nina weather cycle has disproportionately impacted the natural hazard costs exceeding the allowance by 99 Million (this being the third consecutive cycle). Furthermore, flooding in NZ in Jan should see this continue to take a heavy toll (we won’t know the full extent as of yet). Going forward, we see this aspect (i.e. increasingly unpredictable weather patterns) play a prominent role in the business. Whether you attribute this to man-made activity or historic climate cycles, weather patterns are changing and will play a more significant factor in the business outlook.

This brings us to the second part, the firm’s ability to adequately forecast and manage its risk profile (hence reserves). The firm’s skew to QLD and areas with greater exposure to the La Nina have a twofold impact. It must pay higher premiums for reinsurance and keep more catastrophe risk on the balance sheets (which history shows Australian insurers aren’t particularly good at). In this instance, we agree with Andrei Stadnik, the Morgan Stanley analyst’s view that the business needs to emphasise this risk more and not just by using its market leadership in hiking premiums.

In our view, this will be the most significant long-term headwind (i.e. geographic diversification) and their ability to manage catastrophe risk.

Suffice it to say, on the third part of the equation, we say – partial pass. For now, the business’s market power (i.e. the ability to pass on premium increases) seems to outweigh its longer-term risks.

Underwriting Expense

This brings us to the final part of the equation, and with an ex-CFO in charge, as expected, this is one area in which we should expect to see some good performance. Indeed, the guidance regarding ITR previously elaborated on was in no small part a result of operational efficiencies and overall expense reduction. The group has, in fact, confirmed the AUD 2.7 billion in cost savings are on track to be achieved and with a group cost-to-income ratio of 49.9%. Pleasingly the firm seems to have handled the inflationary pressures quite well.

On this front, we can give the business an excellent stellar mark.

Overall Outlook & Growth

Overall the business seems to be on track to continue to deliver for shareholders in the medium term. Investment Income should continue to grow, and even if monetary policy stabilises, we expect overall insurance yields to remain elevated with the benefit of recovery in mark-to-market losses. While we expect earned premium growth to stabilise along with inflation and cost-out initiatives, we expect this to be a reasonable long-term income play. Circa. 5% dividend yield with a high single-digit growth rate going forward.

That said, over the longer term, we continue to watch for signs of better risk management, especially regarding geographic diversification and catastrophe risk.

Disclaimer: Suncorp Group Limited is currently held in TAMIM portfolios.

For most investors, 2022 was a tough year. For CY2022, the Australian Small Ords was down -18.40%, the S&P500 was down -19.40%, and the Nasdaq was down -33.10%. Our Australian All Caps fund did not fare better as we, in particular, experienced tough stock-specific declines, particularly due to de-rating multiples in small caps. However, investing is a long game and the law of mean reversion will likely come to the forefront again in 2023.

For over 100 years markets have always risen to new highs after pulling back: the global march of progress means that, over time, investing in businesses is the best way to compound wealth despite short-term volatility and frequent downturns.

It is worth noting that both on a historical and fundamental basis, 2023 is shaping up to be a strong year for equity markets. Historically after such market downturns as last year, it is rare to see another consecutive year of large losses. In addition, if the US enters a recession this year as expected, markets tend to rally when recessions are announced as investors anticipate an earnings recovery. Finally, China reopening post its zero COVID policy, will be a strong tailwind for the Australian and global economy.

We know our investment process works. Our long-term results annualise as double-digit returns and we expect mean reversion to occur here too. We do not extrapolate one year of under or overperformance as to what we can do, but the average of many years. On that basis, we’re excited for the year to come.

Looking at our portfolio allocations, it’s important to stick to our principles and continue to invest in growing companies that have strong balance sheets to withstand a downturn and any cyclical businesses that may recover quickly in time.

We must remember that the strongest gains in markets tend to happen right after markets bottom, and since there’s no one there to ring the bell, timing the markets is impossible. This is why we remain invested and will outperform when markets recover.

We are now firmly of the view that the worst of this cycle is behind us and although markets may continue to be volatile in early 2023, we expect an overall strong performance during the year. As of writing, some of this optimism is already showing in the portfolio’s performance.

Here are three holdings we believe are set to rise in the coming twelve months.

Retail Food Group (ASX: RFG)

Retail Food Group is a food services and brand franchisor. This investment is a special situation where a new management team are in turnaround mode. Since 2017, Retail Food Group has been shrouded in controversy and out of favour. Explosive allegations were made regarding the company’s dealings with franchisees following an investigation conducted by The Sydney Morning Herald. At the time, it was alleged that Retail Food Group failed to provide adequate financial information for the stores being sold to franchisees for those that operated stores such as Michel’s Patisserie, Donut King, and Brumby’s.

Understandably, the market reacted very negatively to the situation and floored the Retail Food Group share price down a crippling 98% within two years. Skip to now and the Australian Competition and Consumer Commission (ACCC) has completed its investigation and the company is moving ahead with a new management team.

Retail Food Group is well-positioned to grow earnings from multiple internal growth initiatives, as well as being better placed to attract new franchisees and commercial partners, which was previously impacted by the shadow of the ACCC investigation.

The results are beginning to show with profits this year expected to grow up to 35% to $29 million in operating earnings (EBITDA). During the past month, the company delivered good news with an agreed settlement with ASIC for previous misconduct. The outcome of circa $10 million was favourably below market expectations. Going forward we see Retail Food Group beginning dividend payments and resuming its store network growth. Additionally, Retail Food Group currently trades at a multiple half that of its peers, positioning the stock to re-rate if management continues to restore growth and goodwill.

Mayfield Education (ASX: MFD)

After slower merger and acquisition (M&A) activity in 2022, stabilising market conditions this year will provide the right environment for these kinds of situations to kick off again. Additionally, with small cap valuations getting hammered in the past twelve months, some lucrative opportunities have risen for the right suitors.

Mayfield Education is a Victorian-based childcare provider with 28 centres. In 2021 the company acquired its competitor Genius Education for cash and script, making Genius its largest holder (35%). Then, during 2022 these acquired 14 Genius centres underperformed relative to the original Mayfield centres, the central reason for earnings to miss expectations and for any earnout payment to be cancelled.

Recently, Genius surprisingly made a takeover offer of Mayfield for $1.28 per share of the stock it doesn’t already own. The offer was quickly superseded by Busy Bees Early Learning bidding $1.35 per share. Busy Bees previously acquired Think Education (ASX: TNK) in 2021 in what ended up being a contested takeover battle.

The highest bid from Busy Bees only values Mayfield stock at approximately 11 x price-to-earnings (PE). The offer precedes what we expect to be an earnings recovery and doesn’t reflect the positive outlook for the company. We are sitting tight and waiting for the corporate activity to play out.

G8 Education (ASX: GEM)

Another holding within the sector is G8 Education, one of the largest childcare companies in Australia. The company released a positive trading update in December, with operating earnings (EBIT) of $71 million and net-profit-after-tax (NPAT) of $41 million. Year-on-year core occupancy improved to 77.3%. Management has also shown discipline with better cost control and managing labour shortages to achieve cost savings which mitigate inflationary pressures.

The balance sheet is also in a solid position with net debt at 1.2x operating earnings and, so far, $32 million has been spent on a share buyback initiative.

We see 2023 as a positive year for the childcare sector with both favourable government policies and improvement in occupancy levels as the COVID impact completely wears off. We also expect staff shortages to ease as the international visa backlog unwinds. Overall we see the sector re-rating on the back of improved earnings and dividends. With Mayfield on the verge of being acquired, we see G8 Education as an attractive alternative exposure to the sector.

Disclaimer: Retail Food Group (ASX: RFG), Mayfield Education (ASX: MFD), and G8 Education (ASX: GEM) are currently held in the TAMIM Fund: Australia All Cap portfolio.