The market continues to present opportunities for the strategic investor ahead of the upcoming earnings season.

Amidst recent volatility, the small-cap space remains a fertile ground for potential, as demonstrated by the latest developments in the TAMIM Australian Equity portfolios. Below are three companies held with an update on recent developments.

Viva Leisure Expands with Key Acquisitions and Membership Growth

Viva Leisure Limited (ASX: VVA), a leading provider of health and fitness clubs across Australia, has announced the early completion of three Western Australian acquisitions, marking a significant milestone in the company’s expansion strategy. Originally scheduled to finalise by the end of August 2024, these early completions will provide an additional month of contribution to the FY2025 results.

With these acquisitions, Viva Leisure introduces its Club Lime brand to its sixth State/Territory, further solidifying its position as Australia’s largest non-franchised health club brand. The acquisitions, totaling $15.7 million, include eight locations with approximately 20,000 members. These additions are expected to contribute over $3.9 million in EBITDA annually, with forecasted synergies of $1.0 million from FY2026.

CEO and Managing Director, Harry Konstantinou highlighted the company’s success, stating, “Our recent achievements mark a significant milestone for Viva Leisure. Surpassing the upper end of our revenue guidance for FY2024 underscores our relentless pursuit of excellence and growth.”

In addition to acquisitions, Viva Leisure has seen robust membership growth. Corporate memberships have exceeded 210,000, marking a 15% increase since June 2023. Network memberships have also grown to over 385,000, reflecting a 12% increase. The company now operates 180 corporate locations and 356 network locations, further establishing its market presence.

The company’s strategic refurbishment program, announced in August 2023, has also been completed successfully, with 27 locations undergoing enhancements. Plus Fitness, one of Viva’s brands, continues to break records, securing 21 new locations in FY2024 and surpassing 200 operating locations globally.

Looking ahead, Viva Leisure is poised for continued success with a strong pipeline of greenfield locations and ongoing acquisition strategies. More importantly management noted they are on track for the upper end of guidance achieved for Q4 and FY2024 revenue. The company’s full-year results for FY2024 will be released on 14 August 2024, promising a comprehensive update on these significant achievements.

Bravura Solutions: Proposed Return of Capital and Updated Guidance

Bravura Solutions (ASX: BVS) has announced a proposed return of capital to shareholders.

Contingent on receiving the necessary approvals from shareholders at the upcoming Annual General Meeting (AGM) and securing a favourable Class Ruling from the Australian Taxation Office (ATO) the company intends to distribute up to $75.3 million or 16.7 cents per share. This decision follows a thorough review of Bravura’s capital management strategy, following on from the previous management’s decision to raise capital in March 2023 and the significant transformation executed during FY24. The board has determined that the business is overcapitalised and aims to return excess capital to its shareholders within three months of the AGM, pending the requisite approvals.

This follows on from the July market update where Bravura announced an upgrade to its FY24 financial guidance.

The unaudited operating earnings guidance has been increased to approximately $25 million, up from the previously forecasted range of $18 million to $22 million. Additionally, Cash operating earnings guidance stands at around $10 million. CEO Andrew Russell attributed this upgrade to the successful execution of Bravura’s transformation strategy, which has stabilised the business and surpassed budget expectations.

We have previously discussed how we believe Bravura is a turnaround story and with the company’s proactive capital management and upgraded financial guidance position the business continues to show signs of this being the case.

Dropsuite’s Strong Q2 FY24 Results

Dropsuite Limited (ASX: DSE) reported its Q2 FY24 update displaying an encouraging set of results.

The company showcased significant growth across several key performance indicators. We’ve previously written about how Dropsuite is approaching an inflection point and the company continues to focus on expanding its market presence and enhancing its product offerings. As a result, the Q2 numbers have yielded impressive outcomes, particularly in Annual Recurring Revenue (ARR), the number of paid users and churn rate.

One of the standout metrics from Dropsuite’s Q2 FY24 report is the remarkable growth in ARR.

The company reported an ARR of AUD 39.92 million, representing a 31% year-over-year increase. This substantial growth confirms Dropsuite’s ability to attract and retain customers through its comprehensive suite of cloud-based backup and archiving solutions. The ARR growth is a testament to the company’s successful execution of its strategic initiatives and further solidifies our thesis that the company can scale its business and expand its customer base via its partner ecosystem.

During Q2 FY24 the company brought its churn rate back down to below 3%, consistent with its historical performance.

This follows on from an increase in the March quarter to just under 5%. Dropsuite previously reported that the increase was primarily due to increased competition on pricing especially in the Europe, Middle East, and Africa (EMEA) region. It was noted last quarter that the company had been introducing the necessary measures to address and mitigate churn going forward which appear at this stage to be working.

Dropsuite has seen a significant increase in its paid user base.

The number of paid users grew by a record 112k during the quarter to reach a total count of 1.35 million. This growth is indicative of the strong demand for Dropsuite’s solutions and the company’s ability to penetrate new markets. The expanding user base is a critical driver of Dropsuite’s recurring revenue model, providing a stable and predictable income stream.

Dropsuite CEO Charif Elansari commented:

“Continued growth in the global data protection market, combined with our leading position and customer-centric approach, drove record seat additions in Q2 2024. This momentum, along with continued expansion of our MSP partnerships, fuels our optimism for future growth. Furthermore, churn returned to its historical level of <3% after a slight uptick in the March quarter. This reflects our strong commitment to client service and support across the organisation. With a robust balance sheet, favourable market tailwinds including data security and regulation, and a highly scalable distribution channel, we are well positioned to deliver growing and sustainable returns to our shareholders.”

Dropsuite’s Q2 FY24 results reflect the company’s impressive business model and its ability to execute its growth strategies effectively. The significant increases in ARR and paid users demonstrate Dropsuite’s strong market position and its potential for continued success.

The TAMIM Takeaway

The market continues to present opportunities for the strategic investor ahead of a flurry of earnings reports expected over the next month.

Despite recent volatility, we believe there are still a number of opportunities in the small-cap space that remain ripe with potential, as evidenced by the three companies highlighted above. Strong results, capital returns, upgraded guidance, and ongoing merger and acquisition activity underscore the abundant opportunities available.

The proactive management and growth potential within the current market reinforced our confidence in the long-term value that can be delivered to ASX investors.

Disclaimer:Dropsuite Limited (ASX: DSE), Bravura Solutions (ASX: BVS) and Viva Leisure Limited (ASX: VVA) are held in TAMIM Portfolios as at date of article publication. Holdings can change substantially at any given time.

Would you bet your retirement on predicting the daily weather forecast over the next five years? Just as that gamble would be absurd, so too would be the attempt to perfectly time the stock market.

Negative stories and the allure of market timing can be persuasive, often suggesting that a bubble is forming and a crash is imminent. Gloom seems to be what sells these days. After all, “If it bleeds, it leads” has been said in newsrooms across the world for a hundred years. When it comes to the world of economics and investing, negative opinions also get more attention. Focusing on the potential risks and things that could go wrong seems to add to one’s credibility.

In contrast, those with a glass half-full view can be mistaken for being overly relaxed. After all, could they really have done enough research if they hadn’t unearthed a looming crisis?

However, when it comes to investing, being an optimist pays off. Indeed, over the past 20 years, there have been sharp pullbacks, but the S&P 500 is up over 500% and the NASDAQ 1000% in that period.

It’s easy to see how investors could have been convinced to sell everything in 2019 or during the turmoil of early 2020. However, those who did missed the fastest market rebound of all time and a subsequent remarkable bull run, leaving them with cash on the sidelines. Sitting in cash waiting for another crash hasn’t been fruitful either – inflation has eaten away at your purchasing power while you tried to time the market.

To achieve long-term success, investors need to recognise the illusion of pessimism and avoid poor market timing behaviours.

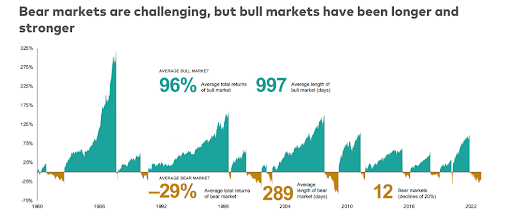

Bear Markets are Shorter, Bull Markets are Longer

Historically, bear markets tend to be shorter and less frequent than bull markets. The S&P 500 index has delivered an annual return of greater than 10% over the past 30 years, including reinvested dividends. If you ha’d invested $100,000 in 1994 and left it alone, it would have grown more than 20-fold, surpassing $2,000,000. Australian shares have delivered close to the same, just over 9% annually, and even the smaller New Zealand market has returned 8.5% annually over that period.

Source: Vanguard

Consider the myriad challenges the world has faced during that time: the September 11 terrorist attacks, numerous wars, a US housing crash, a global pandemic, and multiple recessions in the US and parts of Europe. There have been at least 14 occasions where the S&P 500 fell by more than 10%, including four instances where it dropped over 20%. Twice, the market was cut nearly in half. Despite these significant setbacks, those who stayed invested reaped substantial long-term rewards.

According to Invesco, using data from 1968 to 2020, the average length of a bear market was 349 days, while the average bull market lasted 1,764 days. Research indicates that over the last 92 years, markets have been rising 78% of the time, with only about 20 years spent in bear markets. This historical perspective underscores the importance of staying invested and maintaining a long-term optimistic outlook.

The belief that things will get better, mixed with the reality that the journey will include setbacks, disappointments, surprises, and shocks, is a fundamental principle of investing. Embracing this mindset helps investors avoid the pitfalls of market timing and focus on the sustained growth that historically always follows bear markets.

The Pessimism Bias in News and Investing

Negative news tends to dominate headlines, significantly impacting investor sentiment. Studies have shown that bad news is more likely to be reported and shared, a phenomenon known as the “negativity bias.” This bias can lead investors to make poor decisions based on fear rather than facts.

Famous bearish predictions, such as those forecasting extensive market crashes in the wake of events like the Ukraine war or a follow-on from the COVID-19 pandemic, often do not materialise. Even more pertinent is the fact that, beyond the relatively short and painful period of corrections and bear markets, bulls take over and drive markets to new all-time highs.

Investors who reacted to these dire predictions frequently miss out on subsequent market rallies. In late 2022, headlines were that rising interest rates would be the death of technology and growth. The technology-focused mega-cap leaders dubbed the “Magnificent Seven” (Alphabet, Amazon, Apple, Meta Platforms, Microsoft, NVIDIA and Tesla), climbed 75.71% as a collective during 2023.

“Pessimists sound smart, optimists make money.”

– Nat Friedman

By focusing on the long-term potential rather than short-term volatility, optimists are better positioned to benefit from the market’s inherent upward trajectory.

There is a lot of hype around AI, and it is understandable why some investors might think it’s best to “wait for a crash” before diving in. The market concentration in the top five stocks of the S&P 500—Apple, Microsoft, Amazon, Nvidia, and Alphabet—could easily fool anyone into believing the entire market is overvalued. However, this perspective overlooks the broader opportunities available within the AI sector.

The AI market is projected to grow at a compound annual growth rate (CAGR) of 37% through 2030, according to data from Grand View Research. Last year, the industry reached nearly US$200 billion, and this trajectory suggests it could achieve close to US$2 trillion by the end of the decade.

“Over time, AI will be the biggest technological shift we see in our lifetimes. It’s bigger than the shift from desktop computing to mobile, and it may be bigger than the internet itself. It’s a fundamental rewiring of technology and an incredible accelerant of human ingenuity.”

– Sundar Pichai (CEO of Google)

The AI value chain is extensive, encompassing everything from semiconductor manufacturing to cloud computing infrastructure. Companies involved in producing the essential components for AI, such as wafers, cables, sensors, and processing power, stand to benefit significantly. Additionally, the demand for AI applications necessitates energy infrastructure, robust data storage and cloud computing solutions, creating opportunities for companies in these sectors.

We never suggest investors blindly throw money into the market, nor do we think index investing is the best method for compounding wealth. However, we do know that the next phase of technological invention and innovation is really in its early days and attempting to perfectly time market entries and exits can lead to missed opportunities.

While large-cap stocks get most of the attention and some valuations may seem extended, there is a vast sea of opportunities in small and mid-cap companies. These smaller firms often fly under the radar but are poised to benefit from decades of growth in AI technology and energy innovation. By focusing on these areas, investors can position themselves to capitalise on the transformative potential of AI while avoiding the pitfalls of market timing.

The Classic Rules of Investing

Long-term investing has consistently proven to be beneficial. Historical performance data shows that despite periodic downturns, markets generally trend upwards over time. Common fears about staying invested during market downturns often lead to poor decision-making. Investors might be tempted to sell their holdings during a dip, but this approach frequently results in missing out on subsequent recoveries.

Two fundamental aspects are crucial for the long-term stock market investor. On the one hand, you have to trust that things will continue to improve in the long run.

The stock market is not the right place for pessimists.

One must have almost unshakeable confidence that the economy and quality of life will continue to improve over time. On the other hand, you have to be realistic. Conditions will not improve every day, every month, or every year. The path will rather be strewn with pitfalls.

Forecasts are often useless because most of the time, they are wrong.

There is no point in trying to predict what is coming; instead, we must prepare for any eventuality that could arise at any time. Saving like a pessimist allows for freedom and security when inevitable drawdowns occur. These are opportune moments to invest rather than run for the hills.

Additionally, with the beginning of a new era of technology and innovation, there is great cause for optimism when you take a long-term view. By maintaining this balanced perspective, investors can navigate market fluctuations and capitalise on the enduring growth opportunities the market offers.

Disclaimer:Alphabet (NASDAQ: GOOG), Amazon (NASDAQ: AMZN), Microsoft (NASDAQ: MSFT) and Tesla (NASDAQ: TSLA) are held in TAMIM Portfolios as at date of article publication. Holdings can change substantially at any given time.

Immerse yourself in this thoughtfully curated reading list and podcast selection, designed to expand your intellect and perspective. From Mark Zuckerberg’s AI ventures to the nuances of market hype, these resources offer a deep dive into contemporary finance and technology. Prepare to engage with expert insights, thought-provoking discussions, and cutting-edge analysis that will enhance your understanding and spark meaningful contemplation.

📺 Inside Mark Zuckerberg’s AI Era (Bloomberg, video (YouTube)

Artificial intelligence (AI) is fundamentally reshaping traditional industries, driving unprecedented change across multiple sectors. From healthcare and finance to manufacturing and media, AI’s transformative impact is both disruptive and empowering. Legacy businesses face significant challenges as AI-driven solutions streamline processes, reduce costs, and enhance accuracy, often rendering traditional methods obsolete. For instance, the healthcare industry sees AI improving diagnostic accuracy and patient care, while in finance, AI algorithms enhance trading strategies and risk management.However, amid this disruption, some forward-thinking companies are seizing the opportunity to reinvent themselves. We believe a prime example of this is AI-Media Technologies (ASX: AIM), a global leader in captioning, transcription, and translation solutions. By embracing change, AI-Media has successfully integrated cutting-edge technologies enabling them to deliver superior accessibility services. This strategic self-disruption not only strengthens AI-Media’s competitive edge but also positions it at the forefront of innovation in the broadcast technology market.

About the Company

AI-Media offers a comprehensive suite of products, including LEXI, an AI-powered automatic captioning tool, various encoding tools for seamless caption delivery and the iCap network allowing integration of the process. AI-Media’s acquisition of EEG Enterprises in May 2021 was a transformative move that significantly enhanced the company’s position in the captioning and video technology market. This strategic acquisition not only expanded AI-Media’s presence in North America but also added crucial technologies to its product suite, making it a fully vertically integrated player in the industry. The integration of EEG’s technologies, including the LEXI automatic captioning solution and the iCap Cloud Network, allowed AI-Media to offer end-to-end solutions for captioning, transcription, and translation. The iCap network, being the world’s largest and most secure captioning delivery network, processes over 9 million minutes of content monthly, giving AI-Media a significant competitive advantage. This vertical integration means AI-Media can now provide solutions at every stage of the captioning process, from encrypting source data to encoding, captioning, transcription, and translation. The company’s solutions are trusted by world-leading broadcasters and organisations, including major sporting events and global media companies.

Ai-Media’s Competitive Advantage

Historically, human captioners were essential, serving as intermediaries who repeated spoken content and trained the model to recognise specific voice prints. However, outside of complex scenarios, advancements in AI technology have diminished the necessity for these intermediaries. Despite slow group revenue growth in recent years, Ai-Media’s technology sector has experienced rapid expansion. Not only is the tech side of the business growing, it is doing so at a significantly higher gross margin than that of the legacy services business. A crucial piece of Ai-Media’s strategy is the iCap network, which transitioned from a free model to a fee-based one, thereby increasing reinvestment and reinforcing its competitive edge. This move underscored the businesses competitive advantage as rivals continued using iCap, unable to develop similar infrastructure independently. Ai-Media’s iCap network not only sustains its dominance but also facilitates the upselling of its advanced ASR technology, including Lexi. US broadcasters with existing encoding hardware/software are easily transitioning to Lexi, demonstrating the seamless integration and appeal of Ai-Media’s offerings. While the shift in technology is internally disrupting Ai-Media’s service revenue, it is having the same impact on competitors. The issue for Ai-Media’s competitors is that it doesn’t have the iCap advantage. With ambitions to expand iCap’s dominance globally and upsell Lexi services, Ai-Media’s strategy presents a promising area for investors to watch. The potential for global network expansion coupled with impressive automatic speech recognition (ASR) capabilities positions Ai-Media as a noteworthy player in the broadcast technology market.

Recent Results

Ai-Media is due to report the full year 2024 results in August. In its most recent update for the first half in February, AI-Media reported strong financial results. The company’s revenue increased by 10% to $37.2 million compared to the prior corresponding period. While not a huge jump overall, the technology side of the business grew revenue by 38%, driven by the growth in Lexi. The higher margin growth in technology revenue led to a 16% increase in gross profit to $20.5 million, with group gross margin increasing to 63%. This flowed through to improved operating earnings. The companies saw a 39% increase in operating earnings compared to the prior period to $1.9 million. AI-Media’s cash position remained strong, with $11.7 million in cash and no debt as of December 31, 2023. The company also reported positive operating cash flow of $3.6 million for the period. The company’s strategic focus on expanding its technology offerings and improving operational efficiency positions it well for its continued transition towards profitability.

The TAMIM Takeaway

As AI continues to revolutionise industries, AI-Media exemplifies how embracing technological disruption can lead to significant competitive advantages. The strategic integration of AI-powered tools like LEXI and the iCap Cloud Network has not only elevated their service offerings but also fortified their market position. By focusing on technological advancements and operational efficiency, AI-Media has successfully transitioned from a reliance on legacy services to becoming a leading innovator in the broadcast technology market. With an ever growing technology segment and improving operating earnings, the company is well positioned to move toward break-even profitability in the future. With its strong cash position, Ai-Media is well-equipped to continue expanding its global network and enhancing its ASR capabilities. _____________________________________________________________________________________________ Disclaimer: AI-Media Technologies (ASX: AIM) is held in TAMIM Portfolios as at date of article publication. Holdings can change substantially at any given time.

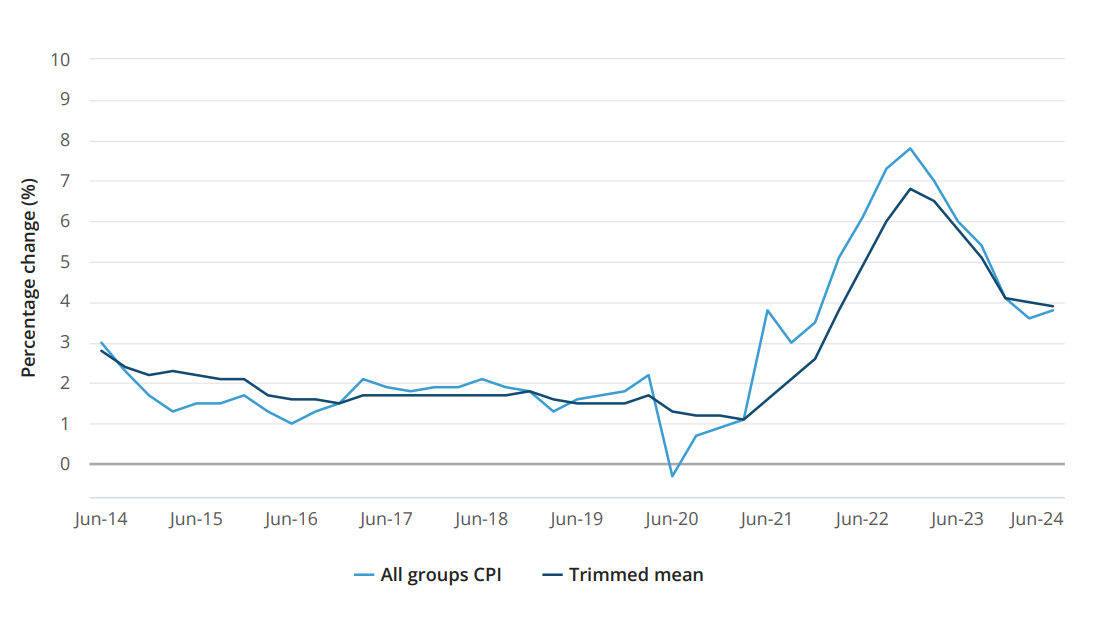

As investors, staying informed about economic indicators is crucial to making sound investment decisions. The Consumer Price Index (CPI) is one such indicator, providing insights into the inflationary trends within the economy. Today, the Australian Bureau of Statistics (ABS) released the CPI data for the June Quarter 2024.

Overview of the June Quarter 2024 CPI Data

The CPI data for the June Quarter 2024 reveals a 1.0% increase in prices over the quarter and a 3.8% increase over the past twelve months. While this marks a continuation of the inflationary trend, the underlying details provide a nuanced view of the economic landscape.

Source: Australian Bureau of Statistics

Key Statistics and Detailed Analysis

The housing sector remains a significant driver of inflation. Prices in this category increased by 1.1% for the quarter and 5.2% over the year. The rise in housing costs was primarily driven by higher rents, which increased by 2.0% this quarter, reflecting strong demand and low vacancy rates. Additionally, new dwelling purchases by owner-occupiers rose by 1.1% due to higher labour and material costs. Electricity prices also saw a notable increase of 2.1%, influenced by the exhaustion of Energy Bill Relief Fund rebates.

In the category of food and non-alcoholic beverages, there was a 1.2% increase this quarter and a 3.3% rise over the year. Notable price movements included a significant rise in fruit and vegetable prices, up by 10.6% this quarter due to unfavourable growing conditions. Meals out and take away foods also increased by 0.6% quarterly and 4.2% annually, while non-alcoholic beverages rose by 1.1% this quarter.

The clothing and footwear sector experienced a 3.1% surge in prices this quarter and a 2.9% rise over the year. This increase was driven by new season stock and the end of promotional activities. Similarly, the alcohol and tobacco category saw a 1.5% quarterly rise and a 6.8% annual increase, primarily due to the biannual AWOTE indexation and residual impacts from the February excise increase.

Factors Contributing to Moderating Inflation

Despite these increases, some categories saw price decreases, helping to moderate overall inflation. Communication costs, for instance, decreased by 0.8% this quarter, although they remain 1.4% higher annually. This decline was primarily due to reduced costs in telecommunication equipment and services.

The furnishings, household equipment, and services category saw only a 0.8% increase this quarter and a -1.1% annual change, indicating some deflationary pressures. Additionally, domestic holiday travel and accommodation prices fell by 4.8% this quarter, contributing to lower overall inflation in the recreation and culture category.

Trends and Predictions

While the overall CPI indicates a continued rise in prices, underlying trends suggest a potential moderation in inflation. The trimmed mean, which reduces the effect of irregular or temporary price changes, rose by 0.8% this quarter, down from 1.0% in the previous quarter. Similarly, the weighted median increased by 0.8%, indicating a steadying of inflationary pressures.

Analysis of Non-Tradables vs. Tradables

Non-tradables, which are influenced primarily by domestic factors, remained high at 5.0% annual inflation. Key contributors included rents, which increased by 2.0% this quarter, medical and hospital services, which rose by 2.1%, and new dwelling purchases by owner-occupiers, which increased by 1.1%. On the other hand, tradables, affected by international trade, saw an annual inflation increase for the first time since September 2022. This rise was driven by high prices in automotive fuel, significant price increases in fruit and vegetables, and higher costs in clothing and footwear due to global supply chain issues.

Tamim’s Takeaways

Despite the overall rise in CPI, several indicators suggest that inflationary pressures might be moderating. The trimmed mean and weighted median show a reduction in the rate of inflation, indicating that the most volatile price changes are beginning to stabilise. Additionally, deflationary trends in categories such as communication and furnishings could offset rising costs in other areas. The significant drop in domestic holiday travel and accommodation prices might also reflect broader trends in discretionary spending, which could help moderate overall inflation.

Looking ahead, while housing and food prices remain high, the stabilisation in other categories suggests that the overall inflation rate may begin to decline in the coming quarters. Factors such as continued policy interventions, potential improvements in supply chains, and changes in consumer behaviour could all contribute to this moderation.

Viva Leisure Limited (ASX: VVA), a leading provider of health and fitness clubs across Australia, has announced the early completion of three Western Australian acquisitions, marking a significant milestone in the company’s expansion strategy. Originally scheduled to finalise by the end of August 2024, these early completions will provide an additional month of contribution to the FY2025 results.

Viva Leisure Limited (ASX: VVA), a leading provider of health and fitness clubs across Australia, has announced the early completion of three Western Australian acquisitions, marking a significant milestone in the company’s expansion strategy. Originally scheduled to finalise by the end of August 2024, these early completions will provide an additional month of contribution to the FY2025 results. Bravura Solutions (ASX: BVS) has announced a proposed return of capital to shareholders.

Bravura Solutions (ASX: BVS) has announced a proposed return of capital to shareholders.

However, amid this disruption, some forward-thinking companies are seizing the opportunity to reinvent themselves. We believe a prime example of this is AI-Media Technologies (ASX: AIM), a global leader in captioning, transcription, and translation solutions. By embracing change, AI-Media has successfully integrated cutting-edge technologies enabling them to deliver superior accessibility services. This strategic self-disruption not only strengthens AI-Media’s competitive edge but also positions it at the forefront of innovation in the broadcast technology market.

However, amid this disruption, some forward-thinking companies are seizing the opportunity to reinvent themselves. We believe a prime example of this is AI-Media Technologies (ASX: AIM), a global leader in captioning, transcription, and translation solutions. By embracing change, AI-Media has successfully integrated cutting-edge technologies enabling them to deliver superior accessibility services. This strategic self-disruption not only strengthens AI-Media’s competitive edge but also positions it at the forefront of innovation in the broadcast technology market.