2024 has been a year of rapid technological advancement and societal change. As we reflect on the year that was, it’s clear that staying informed has been more crucial than ever. Our weekly reading list has been a constant companion, providing insights into the evolving technological landscape, ethical considerations, and societal implications.

From the rise of artificial intelligence and its potential impact on society, as discussed inThe AI We Deserve:: Critiques of artificial intelligence abound, to the enduring relevance of philosophical thought explored inWho can claim Aristotle?, our curated articles have covered a wide range of topics. We’ve delved into the complexities of technological advancements, the ethical considerations surrounding their development, and the potential impact on our future.

As we embark on a new year, we remain committed to providing you with the knowledge and tools you need to navigate the complexities of the technological age. Stay tuned for our 2024 outlook, where we’ll share our insights into the trends and themes that will shape the year ahead.

Ron Shamgar, TAMIM’s Australian Equities Portfolio Manager, continues his 2025 stock picks series with Gentrack (ASX: GTK) a standout performer in mission-critical software solutions for utilities and airports. With a business model built on recurring SaaS revenue and professional services, GTK exemplifies innovation and resilience in an increasingly digitised world.

Transformative Growth Across Key Segments

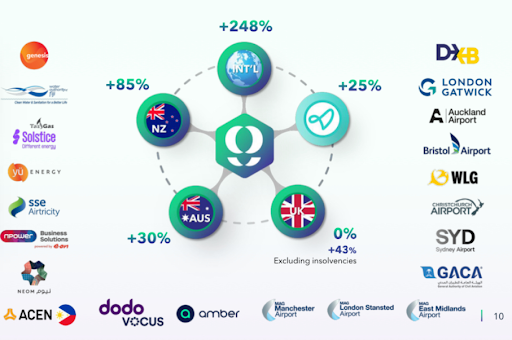

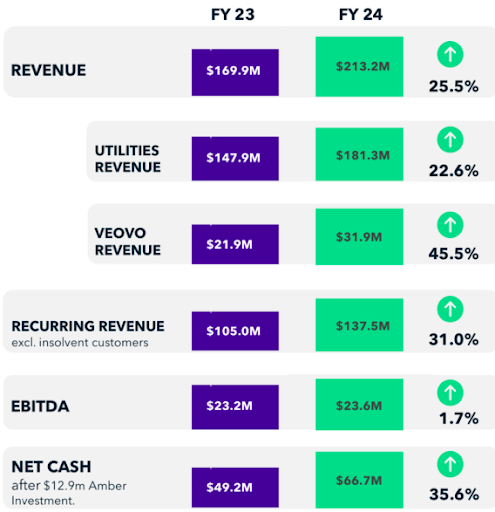

Gentrack’s FY24 results underline its strong growth trajectory, with total revenue reaching $213 million well ahead of its $200 million guidance. The company’s two core business segments have been pivotal to this success:

Utilities (G2): Representing two-thirds of total revenue, the segment grew by 23% to $181 million in FY24. Stripping out one-off insolvency revenues, growth exceeded 50%, driven by a 33% rise in recurring revenue. The segment’s non-recurring revenue also doubled, reflecting heightened demand for upgrades and new implementations among existing and new customers.

Airports (Veovo): Revenue from this segment grew 25% year-over-year (45% including hardware sales), reflecting GTK’s leadership in automating airport operations. The company is actively exploring M&A opportunities to expand Veovo’s offerings and enhance its appeal to global tier-1 and tier-2 airport clients, including Dubai, Sydney, and London airports.

Source: Gentrack Presentation

Operational Efficiency and Margin Expansion

Despite robust revenue growth, GTK has managed to keep headcount increases moderate, driving significant operating leverage. This efficiency, combined with its high-margin recurring revenue streams, allowed the company to expand EBITDA margins.

Source: Gentrack Presentation

GTK’s FY24 EBITDA of $23.6 million was impacted by one-time costs related to its long-term incentive schemes and UK payroll taxes. Adjusting for these, underlying EBITDA grew an impressive 42% to $41 million. The company’s practice of expensing all development costs further highlights the strength of these results compared to peers.

Looking ahead, GTK expects these one-time costs to decline, supporting its medium-term EBITDA margin target of 15-20%.

Strong Cash Flow and Strategic Investments

GTK reported free cash flow of $30 million in FY24, closing the year with a 35.6% increase in its cash balance to $66.7 million. This was achieved despite a $12.9 million investment in Amber Electric, reflecting GTK’s ability to execute while maintaining financial strength.

Growth Catalysts for the Future

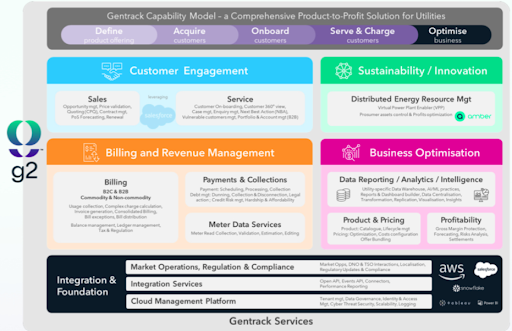

A key driver of GTK’s future growth is its G2 platform, which has been widely adopted by its existing customer base. The platform’s advanced features and capabilities set it apart from competitors, making it the go-to choice for new contracts.

Source: Gentrack Presentation

While GTK remains strong in its core markets of Australia, New Zealand, and the UK, it is also making inroads into Asia and Europe, with new client wins in Saudi Arabia and the Philippines. Though these regions present longer sales cycles, they provide significant long-term growth potential.

TAMIM Takeaway

Since our initial investment in mid-2022 at $1.50, GTK has delivered over 8x returns, now trading at $12.50. Its journey from a niche software provider to a highly profitable tech company underscores its ability to execute and capitalise on long-term tailwinds like the energy transition.

We believe the stock is now being more fully appreciated by investors with substantial growth tailwinds for the next decade. The energy transition is real and every utility company (Energy/Water) will need to upgrade their billing stack in the next few years.

We see significant catalysts in the next 12 months as the pipeline of new business has reached a maturity inflection point and some larger contract wins should be announced in the near term. Hence we believe GTK’s growth story is far from over. Our updated valuation of $25.00 reflects this confidence, with key drivers including:

Continued expansion of the G2 platform in core and emerging markets.

Growing market awareness of GTK’s role in the energy and infrastructure transition.

Larger contract wins that signal a maturing sales pipeline.

For 2025, Gentrack (ASX: GTK) remains our highest-conviction holding in the TAMIM Australian Equities portfolio. It exemplifies the type of transformative companies we seek businesses with strong fundamentals, clear growth drivers, and a commitment to delivering shareholder value.

Atkore Inc. (NYSE: ATKR) is a standout holding within the TAMIM Global Tech and Innovation Fund, managed by Ryan Mahon. As a global leader in electrical and mechanical products, Atkore operates across critical industries such as data centers, telecommunications, and renewable energy. Balancing operational excellence with exposure to long-term growth drivers, the company exemplifies the fund’s focus on transformative themes sitting at the intersection of both the Technology & Energy pillars, and as a prime beneficiary of the upcoming reshoring acceleration.

Diverse Product Portfolio Driving Resilience

Atkore’s comprehensive portfolio includes conduits, cables, metal framing, perimeter security, and cable management solutions. These products are indispensable for industries undergoing infrastructure upgrades and modernisation, particularly in areas like data centres, solar energy, and telecommunications.Atkore’s ability to provide a one-stop solution for its clients positions it as a key player in addressing the evolving needs of these sectors. As a U.S.-based manufacturer with a strong domestic presence, Atkore is well-positioned to benefit from the reshoring and reindustrialisation trends which will likely dramatically accelerate under the Trump administration. In addition, the company’s extensive product portfolio and manufacturing capabilities make it a key supplier for infrastructure development, electr ification projects, and industrial automation initiatives. This diversified approach mitigates risks tied to any one segment, ensuring resilience even in volatile market conditions.

Strategic Measures to Enhance Shareholder Value

Atkore has demonstrated a strong commitment to creating value for its shareholders through a series of proactive initiatives:

Dividend Program: In 2024, Atkore launched a quarterly cash dividend program, signaling confidence in its cash flow generation and commitment to returning capital to shareholders.

Share Buyback Plan: A newly authorised $500 million share repurchase program underscores management’s belief in the company’s long-term growth potential.

Operational Efficiency: The company continues to streamline operations, driving productivity and reducing costs without compromising innovation or customer service.

These measures highlight Atkore’s disciplined approach to capital allocation, which has been instrumental in maintaining investor confidence and positioning the company for sustained growth across cycles.

Financial Performance and Growth Potential

Although Atkore reported a slight decline in revenue and net income for fiscal 2024 primarily due to pricing pressures and industrial challenges, the company remains highly profitable, with $472.9 million in net income. This decline is largely cyclical, does not detract from the company’s long-term growth trajectory, and is one of the reasons why we view now as a unique opportunity to evaluate a position.Atkore has maintained robust free cash flow, enabling reinvestment in high-growth areas while rewarding shareholders. Its financial strength positions it to capitalise on future opportunities, particularly in data centre infrastructure and renewable energy.

Why Atkore could be a Top Pick for 2025

Atkore stands out as a top pick for 2025 due to its strong market position, exposure to high-growth industries, and commitment to innovation. Key reasons include:

Riding Market Tailwinds: The rapid expansion of data centres (driven by both reshoring and AI-driven rearchitecting), renewable energy projects, and telecommunications infrastructure provides a strong growth runway for Atkore’s products and solutions.

Reshoring and Reindustrialisation: As the U.S. focuses on reshoring and domestic infrastructure investment, Atkore is a direct beneficiary of these macroeconomic trends.

Multiple Pillars: Atkore hits multiple pillars central to TAMIM’s investment philosophy Technology and Energy aligning it with the fund’s transformative focus.

Attractive Valuation: With a favourable 12-month analyst price target above current levels, Atkore presents a compelling investment opportunity.

Strategic Positioning: Likely to find a bottom in early 2025, Atkore is well-positioned for a multi-year push as a core beneficiary of policy tailwinds, including the Trump administration’s agenda to drive industrial growth.

A Strategic Holding in the TAMIM Global Tech and Innovation Fund

As part of the TAMIM Global Tech and Innovation Fund, Atkore aligns perfectly with our investment philosophy of identifying businesses at the forefront of technological transformation. Its role within the fund reflects its potential to benefit from transformative trends in Technology and Energy.Under the guidance of Ryan Mahon, the fund seeks companies with strong fundamentals and exposure to long-term growth opportunities. Atkore’s innovative solutions, market leadership, and ability to adapt to evolving trends underscore why it is an important holding in the portfolio.

The TAMIM Takeaway

Atkore Inc. is a story of resilience, innovation, and growth. Its diversified portfolio ensures relevance across multiple high-growth industries, while its proactive initiatives demonstrate a clear commitment to enhancing shareholder value.Looking ahead, Atkore’s strong fundamentals, market tailwinds, and alignment with major policy initiatives position it as one of the most compelling opportunities in the TAMIM Global Tech and Innovation Fund. For investors seeking exposure to transformative sectors with the potential for sustained growth, Atkore has the potential to be a top stock to watch for 2025 and beyond. ___________________________________________________________________________________________________ Disclaimer: Atkore (NYSE: ATKR) is held in TAMIM Portfolios as at date of article publication. Holdings can change substantially at any given time.

The contentious proposal to tax unrealised capital gains on superannuation balances exceeding $3 million has been officially abandoned for this year, marking a significant development for SMSF trustees and the broader superannuation sector. The government’s Treasury Laws Amendment (Better Targeted Superannuation Concessions and Other Measures) Bill 2023 faced hurdles in the Senate, ultimately stalling its progress and removing it from the legislative agenda for now.

This update offers a reprieve to SMSF trustees and administrators who were bracing for the potential financial and administrative impact of the proposed tax changes. Below, we break down the latest developments and their implications for SMSF trustees.

Key Update: Division 296 Tax Shelved

The proposed tax, aimed at superannuation balances exceeding $3 million, would have introduced a significant departure from existing taxation norms by taxing unrealised capital gains. Critics argued that the measure imposed disproportionate burdens on SMSFs and their members, particularly those holding illiquid assets such as property, which could have forced premature asset sales to cover tax liabilities.

However, the bill’s inability to secure sufficient support in the Senate has deferred these changes for now, providing SMSF trustees with more time to plan and adjust strategies without the immediate pressure of new tax obligations.

Why the Deferral Matters for SMSFs

Breathing Space for Trustees SMSF trustees now have additional time to assess their portfolios and adapt their strategies without worrying about potential tax liabilities on unrealised gains. This delay offers an opportunity to prepare for any future legislative proposals that might revisit this issue.

Preservation of Flexibility The shelving of the Division 296 tax allows SMSFs to maintain their flexibility in asset allocation. Trustees can continue investing in property, equities, and other illiquid assets without the immediate concern of tax liabilities on unrealised gains.

Continued Advocacy The deferral highlights the impact of stakeholder advocacy, including the efforts of the SMSF Association and independent policymakers. Ongoing dialogue with policymakers will be essential to ensure that any future proposals balance the government’s goals with the needs of SMSFs.

What Led to the Delay?

The legislation faced significant opposition in the Senate, particularly from crossbenchers and advocacy groups. The government’s attempt to fast-track the passage of multiple bills through a guillotine motion was unsuccessful, underscoring the contentious nature of the proposed superannuation changes.

The SMSF Association welcomed the deferral as a victory for the sector, with CEO Peter Burgess describing it as a chance to revisit and refine the proposal to better address its unintended consequences.

What’s Next for SMSFs?

While the immediate threat of taxing unrealised gains has been removed, SMSF trustees should remain vigilant as the government may revisit the proposal in future legislative sessions. In the meantime, here’s what SMSF trustees should consider:

Review Asset Allocations Use this time to assess your portfolio and identify opportunities to optimise your SMSF structure. Ensure your investments align with long-term retirement goals and provide flexibility for potential legislative changes.

Consult Professionals Work with your accountant or financial advisor to evaluate current asset valuations and explore options for managing potential tax implications. Proactive planning will ensure your fund remains resilient to future changes.

Stay Informed Keep abreast of updates regarding superannuation legislation. The deferral offers a temporary reprieve, but staying informed will help you adapt to any future reforms.

The TAMIM Takeaway

The deferral of the $3 million super tax is a significant development for SMSFs, providing much-needed relief to trustees concerned about the impact of taxing unrealised gains. While this year’s legislative agenda no longer includes the proposed changes, SMSF trustees should use this time to strengthen their investment strategies and ensure they are prepared for any potential future proposals.

The postponement reflects the importance of stakeholder engagement in shaping fair and effective superannuation policies. At TAMIM Asset Management, we encourage SMSF trustees to remain proactive, consult with experts, and focus on maintaining compliance and performance in an ever-evolving legislative environment.

Stay tuned for further updates as we continue to monitor developments in superannuation legislation. For more insights and resources, visit our website.

As the year winds down, this week’s TAMIM Reading List reflects on progress, challenges, and mysteries that defined 2024. Explore the rise of driverless cars with Waymo and Reddit’s remarkable journey through the social media landscape. Dive into the utopian dreams of a “mad egghead” and the cutting-edge reality of AI-powered weapons. Revisit COVID-19’s impact through 17 pivotal charts, and unravel the financial puzzles surrounding MicroStrategy. Discover alarming data privacy concerns, tips on giving the perfect speech, and groundbreaking theories linking dark matter and dark energy. From teenage mathematicians exploring fractals to the evolving nature of our world, this list captures the spirit of curiosity and innovation.

Gentrack’s FY24 results underline its strong growth trajectory, with total revenue reaching $213 million well ahead of its $200 million guidance. The company’s two core business segments have been pivotal to this success:

Gentrack’s FY24 results underline its strong growth trajectory, with total revenue reaching $213 million well ahead of its $200 million guidance. The company’s two core business segments have been pivotal to this success:

Atkore’s comprehensive portfolio includes conduits, cables, metal framing, perimeter security, and cable management solutions. These products are indispensable for industries undergoing infrastructure upgrades and modernisation, particularly in areas like data centres, solar energy, and telecommunications.

Atkore’s comprehensive portfolio includes conduits, cables, metal framing, perimeter security, and cable management solutions. These products are indispensable for industries undergoing infrastructure upgrades and modernisation, particularly in areas like data centres, solar energy, and telecommunications.