This week’s TAMIM Reading List takes you on a journey through finance, culture, and innovation. Delve into the ongoing reckoning with inflation and explore the rise and fall of Google’s prediction markets. Celebrate the simple joys of the world’s greatest pen and uncover the surprising tricks of Big Toilet Paper. Learn how the CIA recruits Russian spies and follow Paul Mescal’s path to Gladiator II. Be inspired by the cyclists who revolutionised Afghanistan and question if U.S. stocks are overvalued. Finally, explore the rapid adoption of generative AI and what makes a “once-in-a-generation” investment opportunity. Each article brings fresh insights into the challenges and opportunities shaping our world.

In the final instalment of our series, we highlight Racing and Sports [(RAS Technology Holdings Ltd (ASX: RTH)], an ASX-listed company that is carving out a formidable presence in the racing and sports wagering sector. This article follows Parts 1 and 2, where we discussed the broader industry trends and featured two other standout ASX small-cap stocks. Racing and Sports is demonstrating impressive growth through strategic initiatives, financial stability, and a diversified approach to the industry.

Racing and Sports Delivers Impressive FY24 Results, Sets Sights on Continued Growth

In a year marked by substantial strategic advancements and financial accomplishments, Racing and Sports has distinguished itself as a rising force in the global racing and sports wagering industry. The company’s FY24 results reflect its capability to adapt to changing market conditions and lay the groundwork for sustainable growth.

At the core of Racing and Sports’ success is a diversified business model, structured around three key units: Enhanced Information Services, Wagering Technology, and Digital Media. This broad portfolio allows the company to meet the growing market demand for data-driven insights, advanced technology solutions, and engaging digital content across the racing and sports ecosystem. Each unit contributes to a holistic approach that has positioned Racing and Sports to benefit from industry trends while supporting a wide-ranging client base.

Financial Highlights and Milestones

The financial outcomes from FY24 underscore Racing and Sports’ growth momentum. A standout achievement for the year was the company’s first positive before-tax profit of $187,000, a significant leap forward from the previous year’s figures. This profitability milestone highlights Racing and Sports’ successful conversion of its strategic investments into measurable financial gains.

Additionally, the company ended FY24 with a healthy cash balance of $8.3 million, having seen only a modest reduction of $300,000 over the year. This financial stability enables Racing and Sports to fuel its growth objectives, paving the way for strategic reinvestment and operational expansion.

The company’s revenue growth has been impressive, nearly doubling since its ASX listing and reaching $16.2 million in FY24. Furthermore, Racing and Sports achieved over $19 million in annualised recurring revenue, more than doubling in the last two years. This increase reflects the company’s success in developing a loyal, high-margin customer base that is likely to continue contributing to future growth.

Strong Performance Across Business Units

Each of Racing and Sports’ core business units contributed to its positive performance. The Enhanced Information Services division, the foundation of Racing and Sports’ offering, saw a 30% year-on-year increase in annualised recurring revenue, which now stands at $11.7 million. This growth underscores the high demand for data-rich, analytically driven insights, a service that has become essential for operators and stakeholders across the industry.

The Wagering Technology division, a newer and rapidly expanding unit, reached nearly $6 million in annualised revenue, marking an impressive 65% increase from the previous year. This growth reflects Racing and Sports’ ability to capitalise on the ongoing digital transformation of the wagering industry, where technology solutions are critical for operators striving to optimise performance and enhance user experience.

Geographic Expansion and Market Penetration

Racing and Sports has not only strengthened its presence in Australia but also expanded its reach in international markets. In its home market of Australia, the company achieved a 33% year-on-year increase in recurring revenue, demonstrating its resilience and ability to capture further market share even in a mature landscape.

In the UK, a strategic focus for Racing and Sports recurring revenue surged by 43% year-on-year, bolstered by a significant deal with Playbook Engineering. The UK represents a key growth market for the company, and its success there reflects strong demand for Racing and Sports’ offerings and its ability to cater to the sophisticated needs of international clients. Additionally, the company’s “other international markets” segment saw an impressive 167% growth in recurring revenue, highlighting the global appeal and applicability of Racing and Sports’ products and services.

Strategic Partnerships and Growth Initiatives

Looking forward, Racing and Sports is well-positioned for further expansion, with strategic partnerships set to play a key role in its growth journey. The company’s alliance with Waterhouse VC is particularly noteworthy, as it provides access to an extensive network and enhances Racing and Sports’ reach on a global scale. This partnership strengthens Racing and Sports’ competitive position, particularly in the UK and European markets, where it aims to meet rising demand for comprehensive racing solutions.

In addition to partnerships, Racing and Sports is pursuing an active approach to growth through strategic acquisitions. By targeting acquisitions that could enhance its capabilities, broaden its footprint, or open up high-revenue opportunities, the company demonstrates a proactive approach to growth that aligns with its commitment to delivering value to shareholders.

The TAMIM Takeaway

Racing and Sports’ impressive FY24 results and strategic initiatives have solidified its position as a prominent player in the racing and sports wagering industry. With a diversified business model, robust financial foundation, and a clear vision for growth, the company is well-prepared to navigate the opportunities and challenges in the dynamic wagering landscape. With an Enterprise value of circa $50 million and ARR of $19 million and growing, we believe the company is undervalued with industry transactions at multiples of the current market cap of RTH.ASX.

For investors, Racing and Sports represents a compelling opportunity in a rapidly evolving industry. The company’s focus on delivering data-driven insights, advanced technology solutions, and engaging digital content sets it apart, making it a valuable player in both the Australian and global markets. Racing and Sports’ ability to capture high-growth segments within its core business units, combined with its disciplined approach to expansion, reinforces its potential for sustained profitability.

As the final feature in our three-part series, Racing and Sports rounds out our selection of ASX small-cap stocks with significant upside potential in the gambling sector. Each company we’ve highlighted BlueBet, PointsBet, and now Racing and Sports exemplifies unique strengths that align with industry trends and position them for continued growth. For investors looking to gain exposure to the ASX-listed gambling sector, these companies represent a balanced portfolio of high-growth opportunities driven by technology, innovation, and strategic expansion.

Stay tuned for more insights from TAMIM as we continue to monitor the Australian and global gambling industry for emerging trends, key players, and high-potential investments.

Disclaimer: RAS Technology Holdings Ltd (ASX: RTH), BlueBet Holdings Limited (ASX: BBT) and PointsBet (ASX: PBH) are held in TAMIM Portfolios as at date of article publication. Holdings can change substantially at any given time.

Investing in Australia’s Big Four banks Commonwealth Bank of Australia (ASX: CBA), National Australia Bank (ASX: NAB), Westpac Banking Corporation (ASX: WBC), and Australia and New Zealand Banking Group (ASX: ANZ) has historically been a cornerstone of Australian portfolios. Renowned for their stability, profitability, and high dividend yields, these banks dominate the ASX and remain pivotal to Australia’s financial system. But as the economic landscape evolves, with rising interest rates, cost pressures, and digital transformation, are they still the safe bet they’ve always been? Let’s dive in.

Commonwealth Bank of Australia (CBA): The Profitability Leader

CBA continues to outperform its peers, reporting a stellar quarterly profit of $2.5 billion (September 2024), up 5% from earlier this year. Its net interest margin (NIM) of 2.07% remains the highest among the Big Four, driven by effective interest rate management and higher treasury earnings. The bank’s robust CET1 ratio of 11.8% and 77% deposit funding ratio highlight its solid financial position.

However, CBA’s substantial exposure to the residential housing market poses a notable risk. With $144.8 billion in risk-weighted assets tied to this sector, a downturn in housing could create challenges. Operating costs, too, rose due to wage inflation, reflecting broader sector trends.

Strength: High profitability and NIM leadership. Weakness: Significant reliance on the housing market.

National Australia Bank (NAB): The Turnaround Story

NAB has undergone a quiet transformation in recent years, delivering $7.1 billion in cash earnings for FY24, supported by a strong CET1 ratio of 12.21%. Its focus on corporate and SME lending differentiates it from the more retail-heavy CBA. NAB’s recent innovations, including advanced fraud prevention tools and a loyalty program, aim to enhance customer engagement.

Despite these positives, NAB’s profitability remains under pressure, with NIMs at 1.71% substantially lower than CBA. Rising impairments in business lending and cost pressures from wage inflation add to the challenges. Furthermore, NAB faces regulatory scrutiny over hardship notices, a potential reputational and financial risk.

Strength: Strong capital base and corporate focus. Weakness: Lower profitability and ongoing regulatory issues.

Westpac Banking Corporation: The Mixed Performer

Westpac reported a $6.99 billion net profit for FY24, down 3% from the prior year. Despite narrowing NIMs (1.95%), Westpac is aggressively pursuing growth in private banking and business lending. Its CET1 ratio of 12.5% and disciplined credit management offer a degree of safety.

However, rising costs, largely attributed to technology investments and inflation, have outpaced peers. Mortgage delinquencies ticked up to 1.05%, signaling potential stress in its residential portfolio. While its digital transformation initiatives, like anti-fraud measures, have shown promise, the broader cost structure remains a concern.

Strength: Investments in technology and digital transformation. Weakness: High operating costs and concentration risks.

Australia and New Zealand Banking Group (ANZ): The Diversified Challenger

ANZ has delivered solid results, with a $6.535 billion statutory net profit and NIMs of 1.5%. The recent acquisition of Suncorp Bank has diversified ANZ’s customer base, adding 1.2 million customers and expanding its regional footprint. ANZ’s focus on digital transformation and operational efficiency positions it well for long-term growth.

However, like its peers, ANZ faces rising costs due to inflation and competitive pressures in lending. While its CET1 ratio of 12.2% reflects capital strength, the bank must sustain this momentum to remain competitive.

Strength: Diversified portfolio and customer base. Weakness: Rising costs and modest NIMs.

The Big Picture: Resilience Amid Challenges

The resilience of Australia’s Big Four banks in the face of economic headwinds is impressive. Rising interest rates have bolstered profitability by improving NIMs, yet the rapid pace of rate hikes has not led to significant stress on their balance sheets. Despite modest upticks in mortgage delinquencies, borrowers remain surprisingly resilient, and credit impairments across the sector have been minimal.

However, valuations for the Big Four banks appear stretched, especially for CBA, trading at north of 25x earnings. NAB, Westpac, and ANZ offer more reasonable valuations but come with distinct risks. With future growth likely tied to the residential property market, volume growth in this sector will be critical.

TAMIM Takeaway: Where Do We Stand?

Australia’s Big Four banks remain well-capitalised institutions with impressive operational resilience. For investors, the question isn’t whether these banks are strong, they are, but whether their current valuations offer sufficient upside to justify the risks.

Best Performer: CBA retains its title as the profitability leader, but its hefty valuation and housing exposure make it a cautious buy.

Momentum Play: NAB shows steady operational improvement, though regulatory scrutiny is a wildcard.

Value Pick: ANZ offers the most compelling risk-reward balance, with diversification and a reasonable valuation.

Wildcard: Westpac needs to tame its rising costs to fully capitalise on its digital investments.

At TAMIM, we recommend a selective approach. While the Big Four banks offer reliable income and defensive qualities, their valuations suggest limited room for error. Investors should prioritise banks that manage costs effectively, adapt to digital demands, and maintain strong governance. In the dynamic Australian banking sector, resilience and disciplined growth remain key.

Disclaimer: Commonwealth Bank of Australia (ASX: CBA), National Australia Bank (ASX: NAB) and Australia and New Zealand Banking Group (ASX: ANZ) are held in TAMIM Portfolios as at date of article publication. Holdings can change substantially at any given time.

The Superannuation Industry (Supervision) Act 1993 (SIS Act) is complex, and navigating its intricacies requires a clear understanding of trustee responsibilities, regulatory requirements, and governance standards. When dealing with such complex matters, the courts can provide valuable guidance on issues such as Non-Compliance and Legal Consequences, Judicial Advice to Trustees, Death Benefits and Trustee Discretion, and Remuneration of Directors.This article examines a recent court case, Re: Gainer Associates Pty Limited [2024] NSWSC 1138, which highlights these critical issues and underscores the importance of robust governance and compliance for self-managed superannuation fund (SMSF) trustees.

Case Overview

The court case focused on an SMSF that became non-compliant following the death of a member. Under the SIS Act, when a member passes away, their legal personal representative must be appointed as the trustee or director of the corporate trustee. In this instance, the NSW Trustee and Guardian (NSWTG), acting as the deceased member’s legal personal representative, appointed an external accountant as director of the corporate trustee instead of taking on the role themselves. This decision breached the SIS Act, rendering the SMSF non-compliant.Despite this misstep, the trustee and NSWTG disclosed the breach to the Australian Taxation Office (ATO) and sought indemnity. This proactive approach became a focal point of the court’s deliberations.

Key Issues and Court Findings

1. Non-Compliance and Legal Consequences

The court acknowledged the SMSF’s breach of compliance rules but emphasised the trustee’s efforts to rectify the situation. The trustee disclosed the non-compliance to the Australian Taxation Office (ATO) and sought indemnity, demonstrating a proactive approach to mitigating potential penalties.

2. Judicial Advice to Trustees

A significant part of the ruling provided judicial advice under Section 63 of the Trustee Act 1925 (NSW). The court underscored that seeking advice is crucial when trustees face ambiguity, even if the fund is in breach of regulations. This guidance helps trustees ensure the proper administration of trust property.

3. Death Benefits and Trustee Discretion

The court also examined the trustee’s discretion in distributing death benefits. Trustees must exercise their discretion within the bounds of the trust deed and regulatory framework, emphasising the importance of transparency and compliance in decision-making.

4. Remuneration of Directors

A contentious issue involved the remuneration of the external accountant appointed as director of the corporate trustee. The SIS Act prohibits payments from the SMSF that could render it non-compliant. The court allowed remuneration from the deceased member’s estate, provided it was disclosed to the ATO and did not violate the SIS Act.

Implications for SMSF Holders

1. Governance Matters

The case highlights the critical importance of governance in SMSFs. Trustees must adhere to strict regulatory standards and act in the best interests of the fund’s beneficiaries. Non-compliance can result in penalties and jeopardise the fund’s concessional tax treatment.

2. Importance of Legal and Financial Advice

This ruling underscores the value of professional advice for SMSF trustees. Engaging legal and financial experts ensures adherence to the SIS Act and other relevant legislation, particularly during complex scenarios like the death of a member.

3. Estate Planning Considerations

For SMSF members, having a robust estate plan is vital. Clear instructions regarding the appointment of trustees and the management of death benefits can prevent disputes and compliance issues.

4. Transparency with Regulatory Authorities

Trustees must prioritise transparency with the ATO and other regulators. Proactively addressing breaches, as demonstrated in this case, can mitigate legal and financial risks.

Lessons for SMSF Members and Trustees

Know the Rules: Trustees must be well-versed in the SIS Act and the trust deed governing their SMSF. Understanding these rules helps avoid unintentional breaches.

Plan for the Future: Estate planning should include specific provisions for SMSF management, such as appointing a legal personal representative who understands their responsibilities.

Seek Expert Advice: Trustees facing complex issues should not hesitate to seek judicial or professional advice. This approach can help resolve disputes and ensure the fund operates within the law.

Document Decisions: Maintaining detailed records of decisions and communications with regulators can protect trustees from allegations of misconduct.

The Tamim Takeaway

This case serves as a wake-up call for SMSF trustees and members about the complexities of fund management and compliance. While SMSFs offer flexibility and control, they require diligence and a proactive approach to governance. Understanding the legal landscape and engaging with experts when needed can help trustees navigate challenges and safeguard their fund’s long-term viability.For SMSF holders, this is a timely reminder of the need for rigorous planning and adherence to regulations. By prioritising compliance and seeking advice when necessary, trustees can uphold their responsibilities and ensure their fund operates effectively for the benefit of all members.

In Part 2 of our series on trends within the Australian and global gambling industry, we explore two standout small-cap ASX stocks – BlueBet Holdings Limited and PointsBet – that have demonstrated significant potential in a consolidating market. Their impressive growth trajectories, strategic moves, and commitment to technology innovation position them well for future gains. In Part 3, we’ll conclude with another ASX small-cap pick that offers unique value.

BlueBet Holdings Limited: A Powerhouse in Australian Wagering

BlueBet Holdings Limited (ASX: BBT) is a leading online wagering operator in the Australian market, known for its innovative technology, data-driven approach, and relentless focus on delivering a superior customer experience. The company’s recent transformative merger with Betr has further solidified its position as a force to be reckoned with in the highly competitive Australian wagering landscape.

In its first quarter since completing the merger, BlueBet has demonstrated its ability to execute at a breakneck pace, seamlessly integrating the Betr business and unlocking significant synergies. The successful migration of the Betr customer base onto BlueBet’s platform in just 59 days is a testament to the company’s operational excellence and the strength of its technology.

The financial results for Q1 FY25 paint a promising picture for the company’s future. The combined business was operating cash flow positive in the quarter, a remarkable achievement that reflects BlueBet’s disciplined approach to reactivating the Betr customers and swiftly unlocking the efficiencies of its leading technology platform.

Source: BlueBet Holdings

The standout performance came in September, the first full month post-migration, where the business saw a step change in scale. All key metrics were up over 100% compared to BlueBet’s performance in the prior corresponding period, with net win surging more than 150%. This momentum has continued into Q2, with October turnover and net win up 120% and 140%, respectively, compared to the prior corresponding period.

BlueBet’s strategic and disciplined approach to reactivating the Betr customer base has been a key driver of this impressive performance. By aligning the reactivation efforts with key sporting and racing events, the company has been able to engage customers in an efficient and profitable manner, protecting the combined business’ strong net win margin.

The company has also made significant progress on the cost synergy front, upgrading its annualised synergy target by 20% to $16.9 million. This, combined with the favourable terms secured for the exit of the US market, has bolstered BlueBet’s cash position and put it on a clear path to profitability.

Looking ahead, the company remains confident in its ability to deliver positive monthly EBITDA by the end of the calendar year and full-year EBITDA positivity in FY25. This optimism is underpinned by the company’s focus on strategically reactivating the dormant Betr customer base, leveraging key sporting and racing events as catalysts.

Moreover, the company’s scalable platform, repeatable integration model, and experienced team position it well to execute on its organic growth plans and aggressively pursue further inorganic opportunities to grow its share of the Australian wagering market. CEO Andrew Mance has made no secret of the company’s ambition to achieve a 10% plus market share, and the successful integration of Betr has brought it one step closer to realising this goal.

Overall, BlueBet’s strong Q1 performance and promising outlook suggest the company has navigated the integration process seamlessly, setting the stage for continued profitable growth in the quarters and years ahead. As the company continues to innovate, drive operational efficiencies, and capitalise on the significant reactivation opportunity presented by the Betr customer base, it is poised to cement its position as a true powerhouse in the Australian wagering industry. We estimate BBT will generate $15-20 million of Ebitda in FY26.

PointsBet Delivers Impressive FY24 Results, Sees Path to Sustained Profitability

Online sports betting and iGaming operator PointsBet (ASX: PBH) has reported strong financial results for the 2024 fiscal year, highlighting its growing presence in key regulated markets and a clear trajectory towards sustained profitability.

The company’s Australian business was a standout performer, with statutory segment EBITDA surging to $26.8 million, up from just $0.1 million in the prior year. This marked the fifth consecutive year of positive full-year EBITDA for PointsBet’s Australian operations, underscoring the strength and resilience of the business.

Revenue in Australia grew by 10% during the year, outpacing the broader market, driven by solid performances in both racing and sports betting. PointsBet also made significant investments in consumer protection measures, integrating a national self-exclusion register and banning credit card deposits, demonstrating its commitment to responsible gambling.

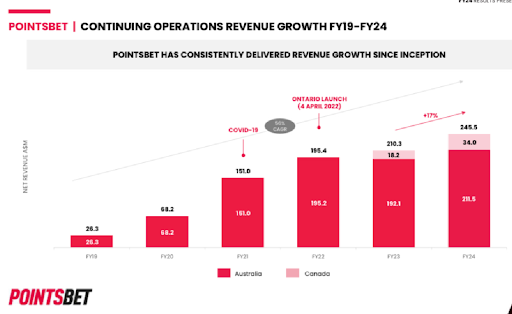

Across the group, PointsBet reported a 17% increase in revenue to $245.5 million, while reducing its EBITDA loss to $1.8 million – a $47.2 million improvement from the prior year. The company ended the fiscal year with a strong financial position, holding $28.1 million in corporate cash and $19.3 million in net assets.

While the Australian business continues to be a reliable performer, PointsBet is particularly excited about the growth prospects in Canada, where the company has been steadily building its presence. In the 2024 fiscal year, the Canadian business saw revenue increase by 87%, with the EBITDA loss narrowing to $19.7 million from $35.8 million in the prior period.

The Ontario market has been a key driver of PointsBet’s Canadian success, with the company successfully increasing its market share in the fast-growing province. Looking ahead, the company sees significant further potential, with the addressable market expected to expand as Alberta and British Columbia regulate their online sports betting and iGaming sectors in the coming years.

PointsBet’s proprietary “Odds Factory” technology has been a key competitive advantage, powering its sports betting offerings in both Australia and Canada. The company’s investments in data science, product development, and customer relationship management have also paid dividends, driving improved revenue retention and customer acquisition.

For the 2025 fiscal year, PointsBet has provided guidance of revenue between $280-$290 million, representing growth of 14-18%, and normalised positive EBITDA of $11-$16 million. Importantly, the company expects to reach cash flow breakeven in FY25 as it continues to scale its business and benefit from operating leverage.

Looking further ahead, PointsBet has outlined an illustrative path to EBITDA margins of around 20% and EBIT margins of 15% in the future, underpinned by its stable cost base and the significant operating leverage it expects to achieve. This equates to a potential $60 million of Ebitda next few years.

Pointsbet reported a strong start to the 2025 fiscal year, with impressive growth across its key markets.

In the September quarter, the company delivered a net win of $65.3 million, up 12% from the prior corresponding period. This was driven by improved sports betting net win margins of 9.7% and a 50% increase in iGaming net win.

The Australian trading business continued its growth trajectory, with a 7% increase in net win compared to the prior year. Active client numbers grew 5% to 238,238, as the company saw double-digit growth in the mass market segment and marginal growth from VIPs.

In Canada, the company delivered stellar results, with net win growing 62% to $8.7 million. This outpaced the overall Ontario market, which grew by around 37%. The strong performance was driven by growth in both the sportsbook and iGaming verticals.

Overall, PointsBet’s impressive FY24 results and clear roadmap to sustained profitability demonstrate the company’s strong positioning in the rapidly evolving online sports betting and iGaming landscape. With a focus on regulated markets, proprietary technology, and a commitment to responsible gambling, PointsBet appears well-equipped to deliver long-term value for its shareholders.

This week media reports indicated PBH to be in the crosshairs of overseas parties looking to acquire the company at a valuation north of $300 million. With the stock doubling to $1.00 since we first bought in, we still see upside if a bid does emerge in the near term. We also view a potential merger between PBH and BBT as highly accretive with estimates of $25-$30 million of synergies alone. A merged group could deliver in excess of $80 million of Ebitda pro forma.

The TAMIM Takeaway

Both BlueBet Holdings and PointsBet have delivered impressive performances in FY24, demonstrating the strength of their respective strategies and positioning them as key players in the Australian wagering and iGaming industry. BlueBet’s successful integration of Betr and PointsBet’s growing presence in Canada reflect the opportunities for growth and consolidation within the industry.

For investors, these companies represent compelling opportunities to gain exposure to a highly competitive, rapidly evolving market. BlueBet’s focus on operational efficiencies, cost synergies, and strategic customer reactivation through high-profile events positions it for sustainable growth in Australia. PointsBet’s expansion in Canada and the strength of its Australian operations showcase its capability to scale effectively, with a clear roadmap to profitability and market expansion.

The Australian and global gambling landscape is increasingly competitive, with regulatory challenges and evolving consumer preferences shaping the industry. However, the growth strategies of companies like BlueBet and PointsBet demonstrate the potential to navigate these challenges and capitalise on emerging opportunities.I

n Part 3, we will conclude our series by introducing a final small-cap ASX stock that stands out in this dynamic market. This pick offers unique value with a specialised focus that complements the growth trajectories of BlueBet and PointsBet. Stay tuned as we unveil our final insight for investors looking to capture upside in the Australian gambling sector.

Disclaimer: BlueBet Holdings Limited (ASX: BBT) and PointsBet (ASX: PBH) are held in TAMIM Portfolios as at date of article publication. Holdings can change substantially at any given time.

CBA continues to outperform its peers, reporting a stellar quarterly profit of $2.5 billion (September 2024), up 5% from earlier this year. Its net interest margin (NIM) of 2.07% remains the highest among the Big Four, driven by effective interest rate management and higher treasury earnings. The bank’s robust CET1 ratio of 11.8% and 77% deposit funding ratio highlight its solid financial position.

CBA continues to outperform its peers, reporting a stellar quarterly profit of $2.5 billion (September 2024), up 5% from earlier this year. Its net interest margin (NIM) of 2.07% remains the highest among the Big Four, driven by effective interest rate management and higher treasury earnings. The bank’s robust CET1 ratio of 11.8% and 77% deposit funding ratio highlight its solid financial position. NAB has undergone a quiet transformation in recent years, delivering $7.1 billion in cash earnings for FY24, supported by a strong CET1 ratio of 12.21%. Its focus on corporate and SME lending differentiates it from the more retail-heavy CBA. NAB’s recent innovations, including advanced fraud prevention tools and a loyalty program, aim to enhance customer engagement.

NAB has undergone a quiet transformation in recent years, delivering $7.1 billion in cash earnings for FY24, supported by a strong CET1 ratio of 12.21%. Its focus on corporate and SME lending differentiates it from the more retail-heavy CBA. NAB’s recent innovations, including advanced fraud prevention tools and a loyalty program, aim to enhance customer engagement.

BlueBet Holdings Limited (

BlueBet Holdings Limited (

Online sports betting and iGaming operator PointsBet (

Online sports betting and iGaming operator PointsBet (