ClearView (ASX: CVW) 1H FY25 Update: A Turning Point in Valuation & Growth

ClearView (ASX: CVW) has long been a business with strong fundamentals, yet its stock has remained undervalued in recent times. Now, with the worst of its claims experience behind it, earnings stabilising, and a bold share buyback program in place, the company is taking active steps to close the gap between its market price and intrinsic value.

At a time when life insurers are becoming more attractive due to potential interest rate cuts, ClearView is positioned to benefit from a rebound in margins, an expansion in embedded value, and potential corporate interest. With a discount to embedded value exceeding 45% and a valuation multiple of just 6.2x forecasted FY26 earnings, the company is trading at levels that sophisticated investors should be watching closely.

![]()

The 1H FY25 results reflect a company in transition. While a temporary spike in claims impacted the first quarter, the sharp recovery in Q2 profitability suggests this was an anomaly rather than a trend. Management has moved quickly to reprice policies, improve claims oversight, and refocus the business, ensuring that growth and earnings trajectory remain intact. Now, with an aggressive share buyback in play, strong premium growth, and a renewed focus on profitability, the stock’s risk-reward profile looks increasingly attractive.

Balance Sheet & Capital Management: Closing the Valuation Gap

ClearView’s net assets stand at $363 million, or 55.1 cents per share, yet the stock continues to trade at around 44 cents, representing a 20% discount to net asset value. The company’s embedded value per share has also increased by 9.5% to 80.7 cents, yet the market still applies an astonishing 45% discount to this figure.

Management is now taking action to close this valuation gap. Instead of paying a dividend, ClearView has announced a share buyback of up to 10% of issued capital, reflecting its confidence in the underlying business and the attractiveness of repurchasing shares at current depressed levels. This move is particularly compelling given that life insurance businesses typically become more valuable in a falling interest rate environment, where their embedded value rises as discount rates decline.

Additionally, the company maintains $7 million in surplus capital, giving it financial flexibility to execute its growth initiatives while rewarding shareholders through capital allocation. The real question now is whether the buyback will be fully executed or deployed opportunistically, either way, it represents a clear signal that management sees significant upside potential in the stock.

1H FY25 Financial Performance: A Recovery in Motion

ClearView continues to strengthen its market position, with its advice in-force premium market share holding at 3.8% ($356 million) and gross premium growth increasing by 8% to $191.4 million. New business market share sits at 10.6%, with new business revenue at $16.3 million, down 8% year-over-year, a decline that appears more cyclical than structural.

The first half of FY25 was defined by a short-term hit to profitability. Life Insurance Underlying NPAT dropped 22% to $15.2 million, largely due to a $6.2 million claims loss in Q1. However, the rebound in Q2 earnings confirms that claims experience has normalised.

NPAT in Q1 stood at $4.2 million, but by Q2, it had recovered to $11.0 million, restoring profitability to historical trends. While group Underlying NPAT fell 28% to $12.5 million, this was expected given the Q1 impact. Importantly, management has already taken steps to prevent a repeat of these claims losses, implementing repricing, improved claims management, and retention measures. These proactive adjustments should ensure stabilised margins going forward.

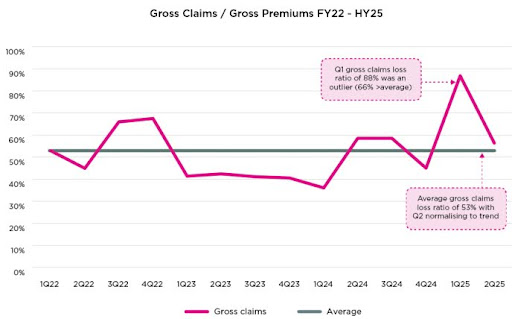

Claims Losses: A Temporary Setback, Not a Structural Weakness

The Q1 claims spike, while impactful, does not appear to be a long-term issue. The Q2 claims ratio normalised, indicating that the worst of the volatility has passed. ClearView has the ability to reprice policies when needed, giving it the flexibility to restore profit margins if claims experience deviates from expectations.

(Source: ClearView FY25 Half Year Results Presentation)

The company has already repriced products, strengthened claims oversight, and reinforced customer retention strategies to ensure margin protection. These measures provide a much-needed safety net, allowing the business to remain resilient against unexpected fluctuations in claims experience.

Outlook: The Stage Is Set for Higher Margins & Growth

Looking ahead, ClearView is on track for a much stronger second half, with multiple tailwinds in place to support earnings recovery and stock re-rating.

Premium rate increases are set to take effect from February 2025, aligning with higher reinsurance costs and adjusted risk assumptions. This ensures long-term sustainability in underwriting profitability, protecting margins as the business scales.

For FY25, gross premium revenue is forecast to reach $395 – $400 million, supported by stable policyholder retention and premium growth. Management expects Life Insurance NPAT margins to improve to 9-10% for the full year, with a further expansion to 10-12% in the second half.

ClearView’s technology transformation project remains on schedule for completion in 1H FY26, unlocking operational efficiencies and cost savings. Additionally, the planned exit from wealth management by June 2025 will allow the company to fully focus on its core life insurance business, eliminating a loss-making segment and streamlining operations.

(Source: ClearView FY25 Half Year Results Presentation)

With FY25 Group Underlying NPAT expected to come in at $32.5 million, ClearView remains undervalued at a PE ratio of 8.9x, a discount that does not accurately reflect its improving earnings trajectory.

FY26 Targets: A Major Growth Inflection Point

Looking further ahead, ClearView has upgraded its FY26 gross premium target to $440 million, up from the previous $400 million forecast. The company’s new business market share target remains 12-14%, while Life Insurance NPAT margins are expected to expand to 11-13%.

At the midpoint, this translates to FY26 Life Insurance NPAT of $52.8 million and Group NPAT of $46.8 million, putting ClearView on an exceptionally attractive PE ratio of just 6.2x.

With the business tracking ahead of expectations, management is growing increasingly confident in its ability to deliver stronger margins, higher earnings, and long-term value creation.

The TAMIM Takeaway

ClearView is at a critical inflection point. The temporary earnings weakness in Q1 has been addressed, claims experience has returned to trend, and earnings power is rebounding. The company is making the right moves to unlock shareholder value, and if FY26 targets are met, the stock could easily re-rate toward a fair value of 70-80 cents per share within the next 6-12 months.

Life insurers also tend to perform well in a declining interest rate environment, as lower rates boost embedded value. This macro tailwind, combined with ClearView’s aggressive share buyback, improved margins, and operational focus, makes the risk-reward profile highly compelling at current levels.

Furthermore, with ongoing consolidation in the industry, ClearView remains a prime takeover candidate, offering strong market positioning, scalable earnings, and significant upside for a strategic buyer.

The key factors to watch will be buyback execution, margin expansion, and continued earnings momentum, all of which could act as catalysts for a substantial re-rating in ClearView’s valuation.

For investors looking for a turnaround story with a clear upside path, ClearView is one to watch.

_____________________________________________________________________________________

Disclaimer: ClearView (ASX: CVW) is held in TAMIM Portfolios as at date of article publication. Holdings can change substantially at any given time.