In February 2025, global technology markets were rocked by one of the sharpest momentum-driven selloffs in recent memory. A convergence of tariff shocks, geopolitical tensions, and algorithmic unwinds led to indiscriminate liquidations, particularly in the technology sector. On the surface, it looked like chaos. But underneath, something else is happening.

This is not the end of the technology boom. In fact, it may be the beginning of a new chapter. The selloff coincides with foundational shifts in global innovation, particularly in artificial intelligence, robotics, and decentralised energy. These transformations are accelerating. The current correction represents a rare entry point for long-term investors positioned for what’s next.

The Innovation Supercycle: A Technological Cambrian Explosion

The world is in the early innings of a multi-decade innovation supercycle. From neural networks to humanoid robots, programmable biology to autonomous logistics, the building blocks of tomorrow’s economy are rapidly taking shape. These aren’t siloed trends, they’re converging.

AI is now the central nervous system of innovation. It enhances everything it touches: medicine, mobility, finance, and manufacturing. And unlike prior booms, this wave is rooted in deflationary cost curves and exponential adoption. Innovation is no longer aspirational, it is the most practical path forward.

The Three Pillars of Strategic Investment

To navigate this new era, we propose a framework built on three interlinked domains of global power:

Technology – Advanced computing, AI applications, automation, and scalable software.

Energy – Decentralised, resilient systems: nuclear, battery storage, and microgrids powering the AI age.

Money – Digital finance, programmable assets, and sovereign investment strategies.

These three pillars don’t just drive growth they define control. A nation or company’s power will increasingly be determined by its positioning across these domains. Investment should follow the same logic.

AI’s Evolution: From Infrastructure to Intelligence

We are moving from Phase 1 of the AI cycle, characterised by the infrastructure buildout (GPUs, data centres, and model training), into Phase 2: application.

The new leaders are those deploying AI at scale across real-world domains. Companies like Confluent (data streaming), Kinaxis (real-time supply chains), and Tesla (robotics and autonomy) are emerging as critical layers in the productivity stack.

The value is shifting away from the plumbing and toward the user experience. As AI becomes cheaper and more accessible, it will drive a Cambrian explosion of intelligent applications.

February’s Selloff: Forced Unwind or Foundational Opportunity?

The recent correction, triggered by tariff escalations and a momentum unwind, caught even seasoned investors by surprise. High-beta sectors like semiconductors, cloud platforms, and digital infrastructure faced sharp drawdowns.

But beneath the surface, nothing fundamental has changed. AI adoption is rising. Cloud budgets are expanding. Robotics is scaling. The selloff was mechanical, not existential.

Sentiment indicators have hit extreme lows. Systematic exposure has been flushed out. These are historically bullish signals, especially when underlying demand remains strong.

The Policy Tailwind: Industrial Strategy Meets Innovation

Tariffs are not just a punitive tool, they’re an industrial policy. The current U.S. administration’s reshoring agenda is a direct attempt to force capital onshore and revive domestic productivity.

This policy shift aligns perfectly with technological trends. AI, automation, and supply chain intelligence are the key enablers of competitive onshoring. Platforms like Kinaxis and Tesla stand to benefit as both enablers and beneficiaries of this shift.

The New Arms Race: Intelligence, Not Iron

Just as the Cold War spurred the space race, today’s geopolitical competition is fuelling a digital arms race. China’s release of DeepSeek is a clear signal: supremacy in AI and robotics is the new high ground.

This race is generative. It forces breakthroughs. And it creates enormous opportunities for companies and investors who understand the stakes. Whether in synthetic biology, AI agents, or advanced manufacturing, innovation is now a geopolitical necessity.

Strategic Positioning: Buying the Future on Sale

For those with a long-term lens, the recent selloff is not a warning, it’s an invitation. Many next-decade compounders are trading 35–55% below their recent highs. These are not speculative flyers but businesses building the infrastructure of the next economy.

Rather than chasing yesterday’s winners, the opportunity lies in identifying Phase 2 leaders, those converting AI and energy into tangible productivity.

The TAMIM Takeaway

Panic is not a strategy. Innovation is.

The market is experiencing a short-term volatility event driven by geopolitics and quant flows. But the long-term trend is unchanged: the world is rewiring itself around intelligence, autonomy, and decentralised energy.

Periods like February 2025 are potentially how new wealth is created. When noise drives price but fundamentals remain intact, the result is a window of opportunity.

We believe that the companies shaping tomorrow’s systems of intelligence, energy, and capital are trading at attractive valuations. The rotation underway is painful in the moment, but it is shifting capital to where it is most needed: application-layer technology, resilient infrastructure, and geopolitical independence.

The foundation is in place. The time to build is now.

This week’s reading list explores a market in transition balancing between caution and resilience. We begin with a pulse check on current sentiment before unpacking the data behind recovery timelines and recession signals. The behavioural quirks of investors in volatile times serve as a timely reminder that psychology often drives performance as much as fundamentals. Meanwhile, broader geopolitical and social dynamics from the recalibration of American influence to the search for stability in digital spaces highlight just how interconnected our economic outlook has become. Whether it’s chaos theory or migration policy, each piece underscores the same theme: navigating complexity requires perspective.

There are decades when nothing happens, and then there are weeks when decades happen. For many readers, this rather neatly encapsulates recent market antics. With tariff policies still stuck in a revolving door and markets convulsing like a toddler denied ice cream, it may be wise to take a step back, breathe deeply, and remember that panic rarely built fortunes.

And no – this isn’t another speculative piece about what on earth former President Trump might tweet next. Frankly, we suspect even his advisors are playing catch-up. Attempting to predict the next pivot in policy is akin to trying to do quantum physics in a bouncy castle. Hope springs eternal for “The Art of the Deal,” but investors would do well to steer clear of trying to game political whims.

So what’s a prudent investor to do?

Let’s begin by sketching out a pragmatic framework, underpinned by three high-probability assumptions (note: probabilities, not certainties):

Volatility is likely to remain elevated.

Interest rates and yields will trend lower.

Inflation will stick around (whether transitory or persistent remains to be seen).

A side note on the third point: if prices keep rising and people simply stop buying, we could very well lurch into deflation territory. Yes, it’s possible to have too much of a bad thing.

But rather than clutch pearls, let’s channel our inner Benjamin Graham and revisit the playbook for the “defensive investor” – that ever-patient, quietly compounding character who tends to win in the long run.

Five Timeless Rules for the Defensive Investor

1. Stay Defensive: Focus on Value and Capital Preservation

In uncertain economic times – when inflation runs hot and bond yields sulk – the number one job of a defensive investor is to not lose money. Yes, this sounds simple. No, it is not.

2. Equities Still Hedge Against Inflation

In the long run, equities tend to outpace inflation – unlike most fixed-income instruments, which can be the financial equivalent of watching paint dry while it erodes your purchasing power. Caveat: in a deflationary environment, fixed income may momentarily become your new best friend.

Warning label: Not all equities are created equal. Buying overpriced tech stocks on the dip because yields dropped (again) is not a strategy – it’s a hopeful shrug dressed up as one.

Defensive sectors – think necessities, not novelties

4. Insist on a Margin of Safety

Graham’s crowning jewel: only buy when there’s a meaningful gap between a company’s intrinsic value and its share price. In periods of inflation, pinning down intrinsic value becomes murkier – so build in a healthy buffer.

5. Avoid Speculation

In environments where economic signals are distorted (low rates, contradictory policies, algorithmic overreach), resist the urge to chase “the next big thing.” Stick to fundamentals. Repeat after me: you are not George Soros.

Two Sectors to Watch: Infrastructure & Consumer Staples

Two sectors currently stand out as quintessential havens for the defensive investor.

1. Infrastructure

Infrastructure assets – particularly public utilities – offer reliable cash flow and benefit from falling yields (i.e., lower cost of capital). They may also enjoy a tailwind from fiscal expansion. Bonus: people tend to still need electricity during recessions.

Fancy a closer look? We suggest exploring the sorry state of global infrastructure (read: opportunity knocks) atinfrastructurereportcard.org.

2. Consumer Staples

These are your household essentials – soap, toothpaste, pasta sauce – the things you’ll buy even if Armageddon is trending on Twitter. Crucially, many of these businesses can pass on rising costs to consumers (wants vs. needs, remember?).

Healthcare would normally slot nicely into this mix, though recent years have seen an uptick in regulatory interference – particularly around the Australian PBS scheme.

Two Ideas from the Land of the Rising Sun

Tokyo Gas (TSE: 9531)

Japan’s largest natural gas provider, Tokyo Gas services key population centres including Tokyo and Kanagawa. Despite the backdrop of global energy volatility, management has remained measured – pursuing well-structured acquisitions and clear growth pathways.

Recent moves include:

70% stake in Chevron’s East Texas assets for $575m

$2.3bn acquisition of Rockcliff Energy

Expansion into Vietnam, targeting production by 2029

The company is also investing heavily in E-Methane and hydrogen supply chains, cleverly using existing infrastructure to service Japan. A quadrupling of renewables capacity (from 1.4 GW to 6 GW) is on the agenda.

Financially:

Forward P/E: 16.3x

Trailing P/E: 20x

Forecasted NPAT to double to ¥131bn

Dividend maintained

Oh – and Elliott Management (yes, that Elliott) has taken a 5% stake, urging monetisation of the firm’s $9.7bn real estate holdings. Watch this space.

Kao Corporation (TSE: 4452)

A stalwart of Japanese consumer staples, Kao makes everything from Biore skincare to Jergens moisturiser and industrial cleaning chemicals. Hardly the most glamorous portfolio, but that’s the point – boring is beautiful when the world’s on fire.

Kao is:

Growing earnings through cost control and top-line growth

Riding emerging market middle-class demand, particularly in Southeast Asia and China

Pouring 4% of revenue into R&D

Sitting on a net cash position of ¥108bn (USD $758m)

Valuation:

Forward P/E: 25.1x

Dividend yield: 2.4%

Return on Invested Capital: 10.5%

In short: not cheap, but increasingly compelling.

The Tamim Takeaway: Actions for the Astute Investor

In a world buffeted by volatility and erratic policymaking, the wise investor returns to the bedrock of timeless principles. Here’s what you can do today:

Review your portfolio for resilience. Are your holdings built for all-weather conditions or just the sunny days?

Prioritise capital preservation. Seek dividend-paying businesses with strong balance sheets and pricing power.

Look abroad. Japanese corporates like Tokyo Gas and Kao offer compelling value with global relevance.

Avoid the siren song of speculation. Leave the trend-chasing to TikTok influencers.

Remember: boring is the new brilliant. Infrastructure and consumer staples may not headline the next fintech conference but they might just help you sleep at night.

In investing, as in life, it often pays to be both patient and prepared. Or, as Warren Buffett once said, “Be fearful when others are greedy, and greedy when others are fearful.” Right now, we’d suggest a stiff upper lip and a defensively constructed portfolio.

Disclaimer: Tokyo Gas (TSE: 9531) and Kao Corporation (TSE: 4452) are held in TAMIM Portfolios as at date of article publication. Holdings can change substantially at any given time.

A new and insidious form of recession is brewing, not one born from financial system failure or natural market cycles, but from policy-driven paralysis. At its heart lies an erratic trade strategy, where punitive tariffs are wielded as a bargaining chip in geopolitical gamesmanship. The resulting uncertainty is more than just noise; it’s now a dominant macroeconomic force that threatens to stifle growth, disrupt supply chains, and undermine business confidence globally.

A War with No Winners

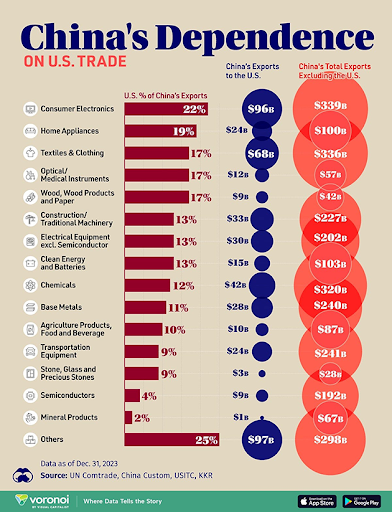

The imposition of blanket 10% tariffs on US trading partners with a jarring 125% rate on China has triggered a tit-for-tat escalation. The idea of “reciprocal trade fairness” may sound appealing in a political soundbite, but in practice it distorts markets, misallocates capital, and invites retaliation.

China’s disproportionate leverage is often misunderstood. While the US runs a large goods trade deficit with China, that doesn’t mean it holds more leverage. China has a higher national savings rate, ample policy tools, and a diversified export base. The US, by contrast, is a consumption-driven economy dependent on low-cost imported goods and global supply chains. Tariffs function as a tax on consumers and businesses alike.

Source: Peter Boockvar

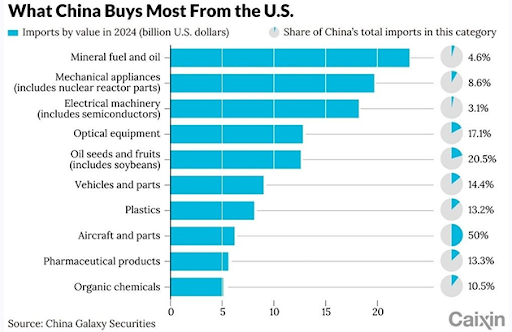

Moreover, there are no quick substitutes. Despite reshoring narratives, shifting production out of China is neither rapid nor frictionless. Meanwhile, American companies that rely on Chinese demand particularly in aerospace, agriculture, and semiconductors are already feeling the pain, with export volumes likely to collapse under the weight of punitive Chinese tariffs.

Source: Scott Lincicome

Uncertainty as a Policy Tool

The volatility isn’t just about tariffs it’s about the unpredictability of implementation. Tariffs are announced, suspended, reintroduced. Businesses can’t plan. Investors can’t price risk. Consumers pull back. The mere anticipation of trade disruptions has prompted importers to accelerate purchases (especially of commodities like gold), distorting GDP data and giving the illusion of volatility where none might otherwise exist.

Recent estimates from the Atlanta Fed suggest first-quarter GDP growth could be artificially depressed due to front-loaded gold imports. Strip that out and we’re flat at best. Add declining business investment, shrinking tourism, and delayed capital projects, and we have the ingredients for a technical recession, even without a financial crisis.

Supply Chains Don’t Turn on a Dime

Contrary to optimistic policy rhetoric, domestic production can’t instantly fill the gap left by disrupted imports. 30% of Home Depot’s stock and more than 70% of Walmart’s product base still trace back to China. A significant share of industrial components, construction materials, and consumer goods will see price spikes or disappear altogether. Domestic manufacturers, already coping with inflationary pressures and wage increases, cannot easily absorb these shocks or compete on price internationally.

Even attempts at substitution such as switching from aluminium windows (sourced from China) to wood highlight the disruption. These aren’t seamless transitions. They carry cost implications, operational risks, and often lower customer satisfaction.

Strategic Paralysis Is the Real Risk

Business leaders don’t need perfection, but they do need predictability. Investment decisions from building a new plant to hiring staff depend on some level of stability. Right now, that anchor is missing.

And it shows. US companies are delaying growth plans. Exporters are scrambling. Multinational firms are rerouting supply chains at enormous cost. Even sectors tangentially affected like tourism are seeing demand erode. Canadian tourism to the US is down 10%, a reminder that tariffs ripple beyond trade figures and into the broader services economy.

The longer this ambiguity persists, the greater the risk that we tip into a self-inflicted slowdown. Not because fundamentals have deteriorated, but because decision-makers at every level consumer, business, and investor are frozen in place.

TAMIM Takeaway: Actionable Insights for Investors

In a world increasingly shaped by political noise and policy whiplash, long-term investors must remain disciplined, opportunistic, and anchored in fundamentals. Here’s how we’re thinking about it:

1. Position for Resilience, Not Headlines

Focus on businesses with pricing power, strong balance sheets, and low dependence on discretionary capex cycles. These are the companies that survive not just recessions, but policy-driven storms.

2. Supply Chain Matters More Than Ever

Assess your portfolio exposure to companies reliant on fragile or concentrated supply chains. Look for businesses that can pivot suppliers, manage inventory dynamically, or benefit from reshoring tailwinds.

3. Watch for Inefficient Dislocations

Policy uncertainty creates pockets of irrationality. Quality businesses may become mispriced due to sentiment overshoots. Be ready to buy when others freeze, volatility is a friend to the prepared.

4. Cash Is Strategic, Not Idle

Maintaining liquidity allows us to capitalise when the fog clears. We’re content to wait and strike with conviction, rather than chase momentum in uncertain markets.

5. Follow the Real Data, Not the Noise

Short-term GDP figures may be skewed by statistical quirks. Stay focused on core leading indicators: employment trends, credit growth, business investment intentions, and margin stability.

At Tamim, we aim to invest through the cycle, not just for the next quarter. While the global environment is clouded by uncertainty, it is precisely this kind of climate where long-term value investors can generate outsized returns by ignoring the noise, sticking to process, and backing quality with patience.

This week’s TAMIM Reading List is wrapped in the language of tariffs—those deceptively simple levers that can jolt markets, bend geopolitics, and shape entire economies. With Trump’s aggressive trade agenda back in focus, we explore the political, economic, and global reactions to the wave of U.S. tariffs. Beyond the headlines, we dive into the rise of private credit, the surprising staying power of COBOL in finance, and the shifting culture of rejection goals. Discover how Brazil built a world-class aircraft manufacturer, meet the platform reshaping science (arXiv), and unravel the mutiny inside Musk’s AI empire. Trade policy or not, the forces of transformation are everywhere.

Source: Scott Lincicome

Source: Scott Lincicome