Few investors have shaped modern markets quite like Ken Griffin. From installing a satellite dish on the roof of his Harvard dorm to building Citadel into the most profitable hedge fund in history, Griffin’s journey is a masterclass in conviction, strategy, and relentless learning.

In a wide-ranging conversation at Stanford’s “View from the Top” series, Griffin shared insights from over three decades of investing. This wasn’t just about P&L; it was about resilience, adaptability, the importance of culture, and why selling is the most underrated skill in business. For investors, especially those navigating today’s volatile and AI-disrupted markets, there’s a lot to unpack.

Here are the key lessons that resonate with our own philosophy at Tamim Asset Management.

1. Start with a Competitive Advantage

Griffin’s first principle, whether launching Citadel in 1990 or evaluating a new idea today, is deceptively simple: know your edge.

“If I can’t establish what our competitive advantage is going to be, there’s no point starting the journey.”

This is timeless. For professional and private investors alike, every position should begin with the same question: what do I know or understand better than the market? At Tamim, our edge lies in deep company-level research, identifying underappreciated opportunities, and maintaining patience when the market overreacts.

Whether you’re stock-picking, backing a fund, or running a business, know your moat, strengthen it, and revisit it often.

2. Hire for Talent, Train for Culture

In the early days, Griffin couldn’t compete for veteran Wall Street talent, so he focused on something even more powerful: bright young minds, well-paid, with responsibility and a mission.

“We hired really bright, ambitious people. We gave them a tremendous amount of responsibility.”

The result? Citadel alumni now run desks at JPMorgan, Credit Suisse, and beyond. For investors, this is a reminder to back teams who can attract and retain top talent. The quality of people, be it in a listed company or a fund manager, is often the greatest predictor of long-term success.

Look past the headlines and focus on leadership, alignment, and culture.

Griffin described Citadel as a place defined by its rate of learning, a culture of rapid iteration, debate, and relentless improvement.

“An incredibly high rate of learning is the essence of what makes our culture so successful.”

Investors must operate the same way. Market dynamics change. What worked five years ago may be obsolete today. Whether it’s understanding new sectors, decoding earnings calls, or evaluating macro risk, curiosity and adaptability are essential.

At TAMIM, we call this the feedback loop: hypothesis, test, review, refine. This is how investment processes evolve, and how alpha is sustained.

4. Selling Is the Most Underrated Skill

Perhaps the most surprising takeaway from Griffin’s interview was his passionate argument for learning to sell.

“If we’re all going to eat, someone has to sell.”

He shared how a $10 plaque in his mentor’s office changed his perspective: selling isn’t sleazy, it’s survival. Whether it’s pitching to investors, onboarding clients, or communicating a stock thesis, selling matters.

For investors, this applies to how you communicate conviction, how you network, and how you build relationships in the investing ecosystem.

Great ideas die in silence. Learn to articulate your edge.

5. Take Risk When You Have Little to Lose

Griffin started Citadel at 22 with $1 million in backing. His mindset?

“When you’re in your 20s, what’s your worst-case scenario? It’s not that bad.”

While the specifics won’t apply to everyone, the principle holds: understand your risk asymmetry. Early in your career, or at times of personal or portfolio strength, you can afford to swing harder.

At TAMIM, we assess risk not just by volatility, but by context. When balance sheets are strong and optionality is high, risk-taking can be rational, even essential.

6. Press Your Advantage. Let Go When You’re Wrong.

The best investors know when they’re right, and they act decisively. Just as importantly, they know when they’re wrong and move on without emotion.

“My best stock pickers are right 54% of the time. The key is: they press when they’re right, and they let go when they’re wrong.”

This is one of the hardest lessons in investing. We fall in love with our ideas. We ignore new evidence. We rationalise underperformance. But to succeed, you must be clinical.

At TAMIM, our internal discipline forces regular position reviews, catalysts reassessments, and a framework to reduce or exit when the facts change.

7. Know Where AI Fits and Where It Doesn’t

Griffin offered a sobering take on generative AI:

“It’s a productivity enhancement tool. It saves time. But I don’t think it will revolutionise most of what we do in finance.”

He argues that AI excels at static problems (e.g. radiology, translation) but struggles with forward-looking domains like investing. However, he also believes AI will change the world around us, automating call centres, transforming marketing, and displacing white-collar work.

The investor takeaway? Don’t dismiss AI, but don’t blindly assume it will solve everything. Focus on companies deploying AI to real-world problems and improving margins, not just those with buzzwords in their investor decks.

8. Strategy Is Everything

One of Griffin’s final reflections was a strategic challenge to the audience:

“If I were starting again today, the first question I’d ask is: where do we have a competitive advantage?”

It’s a question every investor should ask at both the fund and position level. What is our edge? How durable is it? Where are we vulnerable?

Great businesses, and great portfolios, are built on strategy, not just analysis. It’s not enough to understand a balance sheet. You must understand the battlefield.

Ken Griffin’s journey is not about luck. It’s about strategy, team-building, and relentless adaptation. The markets have changed since 1990, but the principles of great investing endure:

Know your edge

Hire great people

Build learning systems

Sell with conviction

Take risk when you can

Let go when you’re wrong

Use AI wisely

Always lead with strategy

At TAMIM, we align closely with these ideas. We believe in backing founder-led companies, staying nimble in a changing world, and always being students of the market. We’re not here to play it safe, we’re here to play it smart.

In a world that’s becoming more complex, noisy, and fast-moving, clarity matters more than ever. Sometimes, the best lessons don’t come from textbooks, but from those who’ve built empires in the real world.

In the underfollowed world of ASX small caps, it’s rare to find a stock that combines deeply discounted valuation, tangible earnings visibility, and the potential for outsized upside. Pioneer Credit (ASX: PNC) is one such opportunity. Operating in the personal debt recovery space, this niche player is quietly rebuilding momentum, buoyed by strong sector tailwinds and a disciplined operational reset.

At TAMIM, we’ve long emphasised the value of small cap value stocks that combine real cash flow with misunderstood narratives. Pioneer Credit (ASX: PNC) fits squarely into this camp. With its stock trading well below its liquidation value and clear earnings growth on the horizon, it may be one of the more compelling ASX turnaround opportunities in 2025.

The Business Model: Focused and Understood

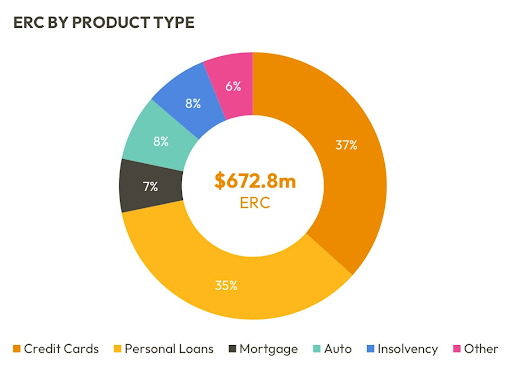

Pioneer Credit is a pure-play retail debt recovery business. Its model is simple: purchase portfolios of delinquent consumer debt (PDPs) at a discount and then collect repayments over time. Unlike some debt recovery stocks on the ASX that dabble in origination or lending, PNC stays firmly within its lane, collection.

It has a customer base of over 750,000 people, with 220,000 active accounts. Approximately half of the debt it manages comes from Australia’s major banks, and the other half from non-bank lenders, providing a diversified stream of accounts.

Since listing in 2014, Pioneer has delivered consistent net IRRs above 15% on its portfolios, suggesting a solid return framework, especially in an asset-light, cash-generating model.

Valuation Gap: A Deep Discount to Fundamentals

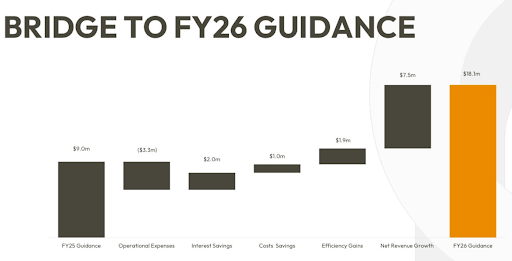

Despite its underlying profitability, Pioneer Credit trades on just 8.5x forecast FY25 earnings and 4x FY26 earnings, assuming the company achieves management guidance of $18 million NPAT by FY26. This implies a sub-$75 million market capitalisation for a business that could feasibly generate more than that in net present value over just a few years.

Perhaps more compelling, management has flagged that the company’s liquidation value sits between $200 million and $330 million. This disconnect, where Pioneer trades closer to its debt recovery value than its going concern value, creates a compelling investment case for patient holders of small cap value stocks in 2025.

The Turnaround Story: From Crisis to Clarity

Pioneer’s journey hasn’t been smooth. In 2019, corporate governance issues and a funding covenant breach led to a trading halt and a dramatic collapse in market value. The stock plummeted, and by April 2020, PNC was trading at just $0.10 per share.

Since then, the business has stabilised. Debt has been refinanced, most recently in July 2024, reducing interest costs by $8 million annually, and operational discipline has returned. Portfolio acquisitions are now selectively focused, and the business is on a clearer path to profitability.

The result is a company with lower financial risk and stronger operational footing. For investors focused on ASX turnaround opportunities, the transformation at PNC should not be overlooked.

Tailwinds in the Sector: Supply and Rationalisation

Debt recovery stocks on the ASX benefit from cyclical and structural dynamics. The supply of purchased debt portfolios (PDPs) is rising, $325 million in FY24 and expected to grow to $400 million in FY25. Banks and non-bank lenders alike are offloading bad debts at scale, seeking balance sheet relief.

At the same time, the industry is consolidating. With fewer active players and increased focus on return discipline, competition for PDPs is becoming more rational. This trend supports improved IRRs for those with proven collection infrastructure, like Pioneer Credit.

Litigation Optionality: A Material Catalyst

One potential near-term catalyst lies in PNC’s $32 million legal claim against PwC, stemming from legacy audit failures. The claim is set for resolution in Q1 FY26. If successful, it could unlock significant shareholder value, either via special dividends, debt reduction, or accelerated reinvestment in new PDPs.

This litigation represents real optionality, not often found in companies at this valuation level. It adds further upside to an already asymmetric risk-reward profile.

Management’s Long-Term Ambition

The leadership team at Pioneer Credit has outlined a bold target: growing NPAT to $50 million and achieving a $1 billion market cap in the next few years. While ambitious, the framework is grounded in tangible steps:

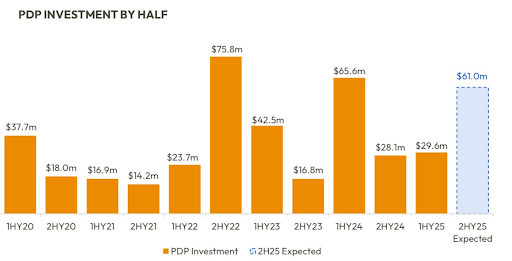

Scaling the PDP book via disciplined acquisitions (guidance: $90m in FY25);

Leveraging existing infrastructure to expand margins;

Monetising the broader customer database beyond collections.

This aspiration aligns with the criteria for small cap value stocks in 2025 that offer a genuine pathway to scale and sustained returns.

Risks: Pricing Reflects Known Challenges

Of course, no investment comes without risk. Pioneer carries debt, $290 million as of the latest update, and requires careful capital management. Regulatory risk is ever-present in the collections space. Execution of the FY25–26 turnaround hinges on sustained PDP purchasing discipline and portfolio performance.

Yet, at a $76 million market cap, these risks appear not only understood but heavily priced in. For investors seeking undervalued opportunities with high upside, Pioneer remains one of the more contrarian ASX turnaround opportunities available.

Tamim Takeaway: Real Cash Flow, Misunderstood Risk, Uncommon Value

Pioneer Credit (ASX: PNC) is the type of stock that rarely makes headlines, but quietly rewards patient investors. It combines a simple business model, a recovering balance sheet, strong insider alignment, and multiple paths to value creation.

Whether you’re seeking exposure to debt recovery stocks on the ASX, looking to add small cap value stocks in 2025, or searching for ASX turnaround opportunities, PNC demands closer inspection.

Actionable Insights for Investors:

Track August 2025 results to confirm earnings momentum.

Watch for developments in litigation that may unlock material capital.

Reassess valuation relative to earnings and liquidation benchmarks.

Position sizing is key, this is a high beta, high reward opportunity.

At Tamim, we continue to find opportunity in unloved, mispriced companies that quietly compound capital. Pioneer Credit (ASX: PNC) fits that thesis, with an added layer of litigation optionality and operating leverage. It may be time for investors to give this hidden gem another look.

Disclaimer:Pioneer Credit (ASX: PNC) is held in TAMIM Portfolios as at date of article publication. Holdings can change substantially at any given time. Source: Company ASX material, discussions with management, Tenva Capital Research

This week’s TAMIM Reading List takes you across the cosmos and back, exploring the evolution of intelligence in animals and the existential mystery of why our universe exists. We delve into Hollywood data to uncover how often lead characters bite the dust, while examining how America’s tipping culture spiralled out of control. On the tech frontier, AI is now printing rocket engines faster, cheaper, and smarter. Meanwhile, we also navigate the sticky political terrain in the U.S. and weigh Billy Slater’s bittersweet coaching dilemma for Origin. From science to sport, politics to pop culture, this list connects the dots across curiosity, progress, and challenge.

AI Tokens, Data Demand, and the Small Cap Opportunity

Artificial intelligence is no longer confined to research labs or theoretical discussions, it’s already reshaping global industries. At the core of this revolution are AI tokens, units of data that fuel the training and operation of AI models. In a recent report from Microsoft, it was revealed that over 100 trillion tokens were processed last quarter, with a record 50 trillion in April alone, a fivefold increase year-on-year.

This surge isn’t just about bytes and bandwidth. It’s about real commercial opportunity. As AI adoption explodes, companies that produce, process, and monetise data at scale are in high demand. While tech giants like Microsoft and Google dominate headlines, there is a growing cohort of AI-driven small-cap stocks on the ASX that are quietly positioning themselves to benefit from this tectonic shift.

In this piece, we spotlight three ASX-listed businesses, AI Media, Straker Translations, and Pure Profile, which we believe are well placed to ride the AI token boom. These are real, profitable companies with strong management, clear strategies, and untapped upside.

AI Media: Reinventing Captioning with a SaaS DNA

AI Media, once a traditional live captioning business, is undergoing a remarkable reinvention. Its mission: to transform into a scalable, SaaS-first AI media solutions provider. That pivot is already underway, with half of its current revenue now coming from technology-based products.

The company’s new AI-driven product suite, Lexi Captions, Lexi Voice, and Lexi Brew, is the engine of that transformation. Launched in April, Lexi Voice helps move the company away from hardware-based revenue toward recurring high-margin SaaS income.

AI Media commands an 80% market share in U.S. live broadcasting and is actively expanding into new verticals, courtrooms, classrooms, and lecture theatres, as well as geographies, particularly Europe and APAC. Management is aiming for $150 million in revenue by FY29, with Lexi products expected to drive 80% of that.

Strategic joint ventures, encoder acquisitions, and partnerships with global distribution networks could further accelerate growth. With a strong balance sheet and founder-led leadership, AI Media is one of the few AI-driven small-cap stocks in Australia with proven product-market fit and visible long-term growth levers.

Straker Translations: AI-Powered Language at Scale

Straker Translations, a New Zealand-based company with a 25-year legacy, is also undergoing its own evolution. Once a traditional services business, Straker is now focused on selling AI translation tools powered by its proprietary datasets. In the AI world, data is the currency, and Straker has plenty of it.

The company’s competitive edge lies in its ability to create and validate customer-specific AI language models. This is made possible through its crowd-sourced network of 100,000 freelancers and a highly valuable historical dataset built over decades. Straker’s Verify AI product adds an extra layer of transparency, offering both automated and human-validated outputs.

One of the most exciting near-term catalysts is its Swift Bridge AI initiative in Japan. With new government mandates requiring English-Japanese financial translations for 2,000 listed companies, this program alone could unlock a significant revenue channel.

Trading at just 0.5x revenue, and with strong balance sheet backing, Straker looks undervalued. The company is also pushing hard on ecosystem development, aiming to lock in 100 partnerships within six months. In a market that’s expected to consolidate rapidly, Straker stands out as a future-ready player with real operating leverage.

Pure Profile: Fuelling AI with First-Party Data

Pure Profile is a lesser-known ASX-listed company that specialises in AI-powered insights and data solutions. The company collects first-party data via proprietary platforms and sells this to governments, brands, and other organisations for decision-making.

In the first half of FY25, Pure Profile generated $29.2 million in revenue (22% growth YoY) and $1.6 million in net profit. More importantly, it’s now targeting the UK and U.S. markets, 5x and 30x the size of Australia, respectively, where the appetite for data is surging.

One of the most innovative parts of its business is avatar-based video surveys, allowing companies to interact with synthetic respondents and dramatically reduce cost and turnaround time. Beyond that, Pure Profile is exploring synthetic data products, a space likely to become a foundational input in the training of large AI models.

With EBITDA forecast at $7 million next year and a market cap of only $50 million, Pure Profile looks like a high-growth AI token enabler trading at a discount. M&A opportunities, particularly in the UK and Southeast Asia, could help accelerate its expansion.

Why AI Tokens Matter for Small Caps

The rise of AI tokens isn’t a niche story, it’s a structural shift in how digital value is created and consumed. AI models live on data, and the companies producing or organising that data, whether via transcription, translation, or insight generation, sit on a new kind of digital infrastructure.

Microsoft’s 100 trillion-token milestone is a preview of what’s coming. While the mega caps will always have their place, small agile players with domain expertise and a clear use case can deliver outsized returns.

From SaaS-led captioning to high-value translation models and data monetisation platforms, the three companies we’ve covered, AI Media, Straker, and Pure Profile, aren’t just tagging along for the AI ride. They’re building the tracks.

TAMIM Takeaway: Betting on the Infrastructure Behind AI

At TAMIM, we are drawn to the enablers, the picks and shovels that support the next wave of growth. The rise of AI tokens and the companies operationalising them offer precisely that opportunity.

AI Media is building a SaaS flywheel in content accessibility. Straker Translations is turning its legacy data into an AI translation advantage. Pure Profile is feeding AI’s insatiable demand for structured data.

Each of these businesses shares the following common traits:

Founder-led

Profitable or near break-even

Operating with strong balance sheets

Trading at a meaningful discount to intrinsic value

For investors looking to play the AI trend beyond the crowded mega cap space, these AI-driven small-cap stocks represent a compelling thematic. As always, do your homework, monitor upcoming catalysts (including earnings updates), and size your positions accordingly.

The AI arms race isn’t slowing down. These are the companies helping to fuel it.

Disclaimer: AI-Media Technologies (ASX: AIM), Straker Limited (ASX: STG) and Pure Profile Limited (ASX: PPL) are held in TAMIM Portfolios as at date of article publication. Holdings can change substantially at any given time.

Introduction: The Case for Real Assets in a Repricing World

In the current investment environment, where rates remain elevated, growth forecasts are patchy, and risk sentiment oscillates week-to-week, there’s a growing argument for looking past the noise. At Tamim, we’ve long been proponents of thematics grounded in long-duration cash flows and macro resilience. Infrastructure, particularly listed infrastructure, continues to earn its place as a vital, underappreciated pillar in that framework.

Why infrastructure, and why now? Because amid global uncertainty, few asset classes offer the same blend of defensiveness, inflation linkage, and long-term structural growth. As allocations to risk assets get reassessed in real time, infrastructure stands out not just as a ballast, but as a ballast with a growth driver.

This note, the first of a two-part series, outlines why listed infrastructure should command more attention in investor portfolios, especially in Australia where it’s structurally under-allocated. Our focus is not just on the appeal of stable cash flows, but on how these assets align with key megatrends shaping the global economy in the years ahead.

A Real Asset in an Unreal Environment

Infrastructure sits at the intersection of economics and physicality. Unlike digital-first business models or intangible-heavy growth stories, these are physical assets providing essential services: power, water, transport, communications. They are not easily disrupted. They are not easily replaced. In many cases, they are irreplaceable.

This tangibility matters in a world where asset prices are often untethered from fundamentals. While equity markets recalibrate to higher rates and political shifts, infrastructure offers something deeply reassuring: cash flows backed by regulation, concession agreements, or long-term contracts.

More than anything, listed infrastructure offers a rare combination in public markets, specifically predictable revenue with structural tailwinds.

Inflation-Linked Resilience

In theory, many equities are supposed to offer a hedge against inflation. In practice, few do particularly over shorter cycles. Infrastructure, however, often embeds inflation directly into its revenue models.

Whether through regulated utility returns, contracted CPI-linked escalators, or usage-based fees that track nominal GDP, infrastructure earnings tend to rise with inflation, not after the fact, but concurrently. This provides a real hedge, not just a theoretical one.

The relevance of this feature has only increased in recent years. As monetary authorities globally battle stickier inflation across labour and services, real assets with embedded inflation linkage are increasingly valuable, not just for capital preservation, but for income growth.

A Strategic Role in Portfolio Construction

We often speak of infrastructure as offering a “third way”, somewhere between bonds and equities. It carries equity-like growth with bond-like cash flow characteristics. This makes it particularly attractive during periods of uncertainty.

For long-term investors, infrastructure performs several roles:

Diversification: Infrastructure’s correlation to broader equities is relatively low, particularly during drawdowns.

Income stability: Cash yields from mature infrastructure assets can be consistent and above-market, with lower payout volatility.

Defensive growth: The asset class participates in upside when growth surprises to the upside (e.g., increased utilisation) while protecting the downside via essential service provision.

It is this duality, resilience and relevance, that makes infrastructure such a core holding for institutions globally, and increasingly, for retail portfolios seeking to hedge volatility with something productive.

Thematic Alignment: From Transition to Digitisation

Perhaps the most compelling reason to revisit infrastructure in 2025 is how well it maps to the defining macro themes of the coming decade.

Energy Transition

From grid modernisation to renewables, infrastructure is the literal and figurative backbone of the decarbonisation effort. Massive capital deployment is required, not in apps or marketplaces, but in transformers, substations, interconnectors, and storage.

Governments globally are leaning into this transition with policy and capital support. Infrastructure sits at the nexus of these policy-driven buildouts.

Demographic and Urban Growth

Ageing populations and urbanisation are not new trends, but their implications are compounding. The demand for transport networks, aged care facilities, and water security infrastructure continues to grow, not just in the developed world, but in high-growth markets across Asia and Latin America.

Digital Infrastructure

The digital economy still relies on physical infrastructure. Fibre, mobile towers, edge computing, and hyperscale data centres are the new pipes and roads. This “soft” infrastructure shares many of the cash flow characteristics of its hard infrastructure peers, and its capital intensity and longevity make it functionally identical from an investment standpoint.

In each of these areas, listed markets offer partial but meaningful exposure to the transition underway.

Repricing and the Opportunity in Listed Markets

Despite the strength of the underlying cash flows, listed infrastructure names have not been immune to market-wide volatility. As rates rose, discount rates increased. Valuations compressed. Sentiment swung.

But beneath the surface, the fundamentals remain largely intact. In fact, many listed infrastructure businesses have continued to grow earnings per share, pay dividends, and reinvest in their asset bases. What we’re seeing is a disconnect between price and value, a situation that doesn’t last forever.

This divergence creates opportunity.

Listed infrastructure is now trading at attractive multiples relative to history and private market equivalents. Investors with a long horizon and a focus on fundamentals have an entry point that may not last as macro clarity returns.

Liquidity vs Illiquidity: Don’t Confuse Smoothness with Safety

One critique often made of listed infrastructure is its exposure to market sentiment. Prices can move independently of fundamentals. This is true.

It’s also true of all listed assets, and often, the “smooth” returns of private infrastructure funds mask significant embedded risk. Illiquidity doesn’t eliminate volatility. It just hides it.

In contrast, listed infrastructure provides:

Real-time pricing

Transparent governance

Flexibility to rebalance or exit

For investors seeking both liquidity and infrastructure-like outcomes, it remains a highly viable path.

The Australian Dilemma: Scarcity of Local Names

The domestic listed infrastructure pool in Australia is increasingly narrow. Takeovers and privatisations have removed key names from the ASX. This scarcity only reinforces the need to look globally or to seek infrastructure traits in adjacent sectors.

That doesn’t mean there’s no opportunity here. It does mean however, that investors need to be creative, thematic, and willing to build a mosaic exposure rather than rely on a single name or ETF.

The second part of this series will examine how to do this effectively, combining local names, global strategies, and thematic adjacencies to create a robust infrastructure allocation.

TAMIM Takeaway: Quiet Strength, Real Utility

Infrastructure doesn’t promise exponential upside. It doesn’t pivot or disrupt or dazzle. But that’s precisely its appeal.

In 2025, with capital markets recalibrating and many investors re-evaluating their portfolios, real assets with real cash flows and real economic relevance are having a moment.

Infrastructure offers:

Stability in earnings and dividends

Hedge against inflation and policy volatility

Alignment with long-term macro trends

Actionable insights for investors:

Reassess your portfolio’s exposure to long-duration, real assets.

Consider global listed infrastructure as a way to enhance income and reduce beta.

Use market volatility to build positions in attractively priced infrastructure-linked strategies.

Focus on thematics, energy transition and digital transformation, where infrastructure is essential.

As we often say at Tamim, investing isn’t just about chasing growth, it’s about ensuring the foundations are sound. Infrastructure, now more than ever, deserves to be one of those foundations.

AI Media, once a traditional live captioning business, is undergoing a remarkable reinvention. Its mission: to transform into a scalable, SaaS-first AI media solutions provider. That pivot is already underway, with half of its current revenue now coming from technology-based products.

AI Media, once a traditional live captioning business, is undergoing a remarkable reinvention. Its mission: to transform into a scalable, SaaS-first AI media solutions provider. That pivot is already underway, with half of its current revenue now coming from technology-based products.