If you strip investing down to its bare, unfriendly bones, you end up with a simple reality: over long periods, your returns converge toward the quality of the people running your money and the businesses you own.

Balance sheets matter, valuations matter, industry structure matters, but if the person with their hands on the steering wheel is mediocre, misaligned, or playing a three year game in a thirty year world, nothing else will save you.

At TAMIM, we have always leaned into founder led and owner minded businesses, especially in the small and mid cap space where information is messy and narrative is cheap. The Intelligent Fanatics framework helps formalise something good investors often do intuitively, back the rare leaders who combine obsession, integrity, culture building, and rational long term decision making in a way that compounds far beyond what spreadsheets alone can see.

Today we want to unpack what that looks like in practice, how to spot it early, and why it is particularly powerful in the part of the market we fish in.

What is an Intelligent Fanatic, really?

The phrase “Intelligent Fanatic” captures a certain type of builder. Not just a gifted operator, not just a hustling founder, but an individual or team that consistently transforms average businesses, or unglamorous niches, into compounding machines over decades.

Common threads show up across industries and eras:

They are learning machines, constantly improving the playbook.

They think in ten year blocks, not ten week news cycles.

They build cultures where staff think and act like owners.

They weaponise incentives, transparency, and trust instead of slogans.

They are frugal with themselves, generous with aligned people, and ruthless with waste.

They stay paranoid enough to adapt, but focused enough not to chase every shiny distraction.

Most crucially, their moat is not a single product feature or a regulation, it is the system of people, culture, incentives, and standards that competitors cannot easily copy. You can copy an app or a pricing model, you cannot copy twenty years of built trust, habits, discipline, and shared mission.

For investors, especially in micro, small and mid caps, recognising this pattern early can be the difference between buying “a cheap stock” and partnering with a wealth compounding institution in its awkward teenage years.

Culture as the real moat

The Intelligent Fanatic lens starts with one uncomfortable truth: almost everything tangible can be replicated over time.

What endures is how a firm:

Hires

Promotes

Shares information

Treats its people when things get hard

Allocates capital when no one is watching

The standout leaders build cultures with three reinforcing pillars.

Employee first, shareholder smarter Not in the soft, corporate brochure sense. In the hard, economic sense.

They pay well enough to attract talent, share the upside through equity or profit share, give autonomy with accountability, and create a direct, visible link between performance and reward. When done properly:

Staff fight to stay, not to escape.

Customers feel the difference in service and care.

Shareholders benefit from lower turnover, higher productivity, and stronger brands.

The Intelligent Fanatic trick is understanding that “employee first” is not anti shareholder, it is how you maximise shareholder value over 10, 20, 30 years.

Radical clarity of incentives Vague profit share schemes and “you are all part of the family” speeches are useless. Intelligent Fanatics:

Publish clear rules, targets, and formulas.

Align both upside and downside.

Avoid designs that reward revenue at any cost, or short term sugar highs.

This attracts a certain personality, ambitious, competitive, long term. The culture then selects, filters and compounds that DNA.

Frugality with teeth These leaders are acutely careful with costs. Offices are functional, not ostentatious, leadership behaviour signals that every dollar is a tool, not a trophy.

That frugality is not about being cheap, it is about:

Leaving more capital to invest in product, people, systems.

Showing staff and investors that management is aligned.

Protecting the business in downturns so culture survives shocks intact.

For us as investors, cheap signalling, scattered strategy, and vanity spending are all useful red flags.

Obsession, focus, and the long game

The Intelligent Fanatic is not “balanced” in the way HR brochures like to pretend. Their business is their life’s work. They are relentless. Still, the key is not raw intensity, it is focused intensity.

Patterns we look for:

Strategic simplicity: One or two core advantages deepened over time, not six new “growth pillars” every result.

Capital discipline: Earnings recycled into the highest return internal opportunities first, not reflexive acquisitions to “buy growth.”

Patient buildout: Infrastructure, people and systems often built “ahead of earnings,” showing confidence in a much larger future footprint.

In small and mid cap land, this often looks boring in real time:

Re investing in product rather than maximising this year’s dividend

Over communicating with staff and customers rather than talking at conferences

Quietly entering adjacent markets where their existing edge transfers

Price, on the other hand, is rarely boring. That disconnect is where we like to work.

Productive paranoia and experimentation

One of the most attractive traits in Intelligent Fanatics is what Jim Collins called “productive paranoia.” They are never comfortable.

They assume:

Customers are less loyal than the P&L suggests.

Competitors are hungrier than they appear.

Technology, regulation, or tastes can flip the script.

But, crucially, they act on this mindset constructively:

Encouraging small, reversible experiments.

Protecting downside with modest bet sizes.

Killing failed projects quickly without destroying the internal culture of initiative.

Markets often misread this. Ramped investment, experimentation, or temporary margin compression gets punished by investors trained to think quarter by quarter. Our job, and your edge as a thoughtful investor, is to distinguish:

Wasteful empire building, from

Intelligent Fanatic style reinvestment that extends the moat.

How TAMIM applies the Intelligent Fanatics lens

Within TAMIM’s process, especially in the Australian All Cap and Small Cap Income strategies, we already screen hard on balance sheets, cash generation, industry structure, and valuation. The Intelligent Fanatics lens deepens our “people and culture” work and is particularly powerful for founder led, under researched companies.

Here is how we integrate it:

Ownership and alignment

Meaningful skin in the game from key executives and directors.

Sensible remuneration structures that reward multi year outcomes, not one year optics.

Culture signals

Staff turnover data where available.

Glassdoor and industry chatter taken seriously, but filtered.

Language in reports, presentations and calls: humble and specific, or promotional and vague.

Capital allocation record

Track history of raises, acquisitions, buybacks, dividends.

Look for evidence of discipline through cycles, not just in good years.

Operating behaviour in stress

How did management behave in downturns, disruptions, regulatory shocks, or COVID like events, did they dilute, panic, over promise, or use the moment to strengthen the business.

Experimentation with boundaries

Is the company learning and evolving, or simply defending a legacy profit pool, are they taking calculated swings that logically build on existing strengths.

Succession and depth

A real Intelligent Fanatic builds a system that can outlive them.

We look for bench strength, codified culture, and credible leaders beyond the founder.

This framework helps us separate three species that often look similar at first glance:

The charismatic promoter, great story, weak alignment.

The competent caretaker, acceptable results, limited long term upside.

The Intelligent Fanatic, occasionally eccentric, but relentlessly rational in building enduring value.

We are aiming for the third group, at the right price, with sufficient downside protection from balance sheet strength and cash flows.

What this means for you as an investor

For many investors, especially outside the institutional machine, there is a temptation to over focus on screens and underweight the “soft” stuff. That is understandable. Culture is hard to model. Incentives do not slot neatly into a DCF.

Yet, if you study the true long term winners, listed in any market, you repeatedly find:

Long duration, aligned leadership,

Distinctive, durable cultures,

Intelligent use of incentives, frugality, and experimentation,

Consistent treatment of staff and customers that builds reputational equity.

The Intelligent Fanatic framework is simply a structured way of saying: do not outsource your judgement of people. When you invest with us, part of what you are hiring is that obsessive, repeatable assessment of who is driving the bus. We like businesses where, if you removed the share price feed and left us only the behaviour of management and the organisation, we would still be comfortable partners.

That is how you stack the odds of compounding in your favour, even in volatile markets, even in smaller, less covered names.

The TAMIM Takeaway

The only moat that compounds forever is human. Products can be copied, distribution can be bought, technology can leapfrog, regulation can shift. A deeply embedded culture of aligned, obsessed, ethical, experimentally minded people is almost impossible to replicate on demand.

As investors in small and mid cap companies, we are not just buying numbers, we are choosing who to trust with our capital. The Intelligent Fanatics lens sharpens that choice.

At TAMIM, we look for:

Founders and leaders with meaningful skin in the game and a history of rational decisions.

Organisations where incentives are transparent, staff think like owners, and culture is treated as a strategic asset, not a slide in a deck.

Evidence of disciplined frugality, productive paranoia, thoughtful experimentation, and focus on a few enduring advantages.

Get those ingredients right at a sensible valuation, and time, volatility, and even market pessimism become allies rather than enemies. That is how you quietly, patiently, build wealth.

Every new industrial revolution begins with a dream, but it survives only through its infrastructure. Beneath the glossy surface of AI models, electric vehicles, and connected cities lies a far less visible network of pipes, wires, and purifiers that make the modern world function. As capital floods into software, semiconductors, and data centres, it is easy to forget that none of it works without clean water, stable electricity, and microscopic precision in materials.

Japan, long associated with patience and precision, remains home to a handful of global champions quietly building the backbone of this physical revolution. They do not seek headlines or hype. Instead, they engineer reliability into every product they touch. Three names capture this ethos perfectly: Kurita Water Industries, Ibiden, and Sumitomo Electric Industries. Each operates in different industrial domains, yet all share the same DNA of endurance, discipline, and innovation.

For investors, these companies represent a critical intersection between infrastructure and technology. They are not chasing the next app or digital trend. They are supplying the essential tools that make technological growth possible, from ultra-pure water for chip fabrication to optical fibre for global connectivity.

Kurita Water Industries: Purifying the Digital Economy

If AI is the brain of the modern world, water is its bloodstream. Every semiconductor plant, pharmaceutical facility, and data centre depends on water so clean it could dissolve the metals from a regular pipe. Kurita Water Industries has spent over seven decades perfecting this science. Founded in 1949, the company has become a global leader in water treatment, filtration, and recycling.

Kurita operates across two major divisions: Electronics and General Industry. The electronics segment serves semiconductor and display manufacturers, supplying ultra-pure water systems and process chemical management services. The general industry division supports everything from oil refineries to food processing, providing boiler and cooling water treatments that keep industrial systems efficient and environmentally compliant.

What makes Kurita remarkable is its integrated approach. It is not just selling chemicals or equipment; it offers full life-cycle solutions that combine engineering, analytics, and on-site maintenance. Kurita’s engineers monitor performance data in real time, adjusting chemical balances and flow rates to maximise system longevity and minimise waste.

This matters because water scarcity is not just a developing-world issue. Semiconductor fabrication plants consume tens of millions of litres per day. As chip production expands globally, water efficiency has become an economic and environmental imperative. Kurita’s role, therefore, sits at the convergence of sustainability and technological necessity. Its systems recycle industrial wastewater, turning what was once a cost into a closed-loop asset.

From an investment perspective, Kurita’s business model is compelling. Its long-term service contracts create steady recurring revenue. Its clients, including the largest chip and electronics producers, have high switching costs due to the mission-critical nature of water systems. And as global regulation tightens around environmental discharge, demand for Kurita’s expertise is only set to grow.

Ibiden: The Silicon Spine of Modern Manufacturing

While Kurita ensures that factories run clean, Ibiden ensures they run fast. Founded in 1912, Ibiden began life as an electric power provider before evolving into one of the most advanced electronics and ceramics manufacturers in the world. Today, it sits at the heart of the global semiconductor ecosystem, supplying printed circuit boards and integrated circuit substrates used in CPUs, GPUs, and high-performance computing systems.

Think of Ibiden as the bridge between design and reality. Every semiconductor chip needs a substrate that connects it to the rest of the system. These substrates must manage heat, conductivity, and mechanical stability within nanometres of precision. Ibiden has mastered this craft, making it a critical supplier to companies like Intel, Apple, and Nvidia.

Its materials expertise extends far beyond electronics. Ibiden’s ceramic components are used in diesel particulate filters, high-temperature insulation, and graphite electrodes for advanced manufacturing. This diversification gives it resilience through economic cycles. When consumer electronics slow, automotive or industrial ceramics often pick up the slack.

What differentiates Ibiden is its deep vertical integration. It produces both the substrates and the specialized ceramics required to handle extreme manufacturing conditions. It even uses its own proprietary processes to recycle waste heat and materials from one division into inputs for another.

In essence, Ibiden represents the Japanese model of compounding expertise: mastering one process at a microscopic level, then layering new technologies on top over decades. For investors, this translates to durability. While new entrants come and go, Ibiden’s reputation for precision and reliability keeps it entrenched within the most demanding supply chains.

As AI data centres and EVs drive exponential demand for processing power, the need for high-performance substrates will continue to rise. Ibiden’s expansion into advanced IC packaging positions it at the centre of this structural growth trend. In a world increasingly obsessed with the virtual, Ibiden quietly builds the physical scaffolding that makes it all possible.

Sumitomo Electric: Wiring the Electrified World

If Kurita provides the water and Ibiden supplies the circuitry, Sumitomo Electric Industries ensures the world stays connected and powered. Established in 1897, Sumitomo Electric is one of Japan’s great industrial conglomerates, with operations spanning power transmission, automotive wiring, optical communication, and advanced materials.

Its products touch nearly every part of modern infrastructure. The company’s Environment and Energy segment manufactures power cables and grid equipment used in renewable energy transmission, while its Infocommunications business supplies optical fibre, fusion splicers, and high-speed data links essential for 5G and cloud networks.

The automotive division, one of the largest globally, produces wiring harnesses and electronic systems for electric and hybrid vehicles. As carmakers electrify fleets and integrate advanced driver assistance systems, the complexity and value of wiring systems have soared. Sumitomo’s decades of experience in safety-critical components make it a preferred supplier for automakers in Japan, Europe, and North America.

Sumitomo’s electronics and industrial materials divisions further demonstrate the company’s breadth. It produces ultra-fine wires, laser optics, and high-performance alloys used in manufacturing and energy infrastructure. Its research into superconducting cables and next-generation semiconductors points to a future where energy loss is minimised, and efficiency becomes the new growth lever.

From an investment standpoint, Sumitomo Electric is a model of strategic balance. It sits at the intersection of electrification, communication, and automation, three megatrends that will define global infrastructure for decades. Its diversified segments cushion it against volatility, while its commitment to R&D ensures it remains relevant across successive technology waves.

Common Threads: Precision, Resilience, and Long-Term Vision

Though Kurita, Ibiden, and Sumitomo Electric operate in distinct fields, they share a philosophical foundation that makes them enduring investments. Each is rooted in Japan’s culture of monozukuri, a term that roughly translates to “the art of making things well.” It represents a devotion to craftsmanship, attention to detail, and continuous improvement.

These companies have survived and thrived through oil shocks, currency crises, and technological upheaval because they focus on what they can control: process excellence, product quality, and customer trust. Their innovation is quiet but relentless. Kurita continuously improves its membrane and ion-exchange technologies. Ibiden refines its ceramic composition for higher thermal stability. Sumitomo Electric pushes the frontier of power efficiency and fibre-optic transmission.

The result is a trio of businesses that embody defensive growth. They benefit from secular trends, digitalisation, decarbonisation, and electrification, without depending on short-term cycles. Their balance sheets are conservative, their earnings steady, and their management philosophies aligned with long-term compounding rather than quarterly results.

This patience is often misunderstood by markets that favour speed and narrative. But in infrastructure investing, time is the ultimate competitive advantage. Each incremental improvement compounds over years, building barriers to entry that are nearly impossible to replicate.

The Global Infrastructure Connection

The world is entering a new era of infrastructure investment. Decades of underinvestment are being corrected through government initiatives and private capital flows targeting energy transition, supply chain resilience, and digital connectivity. Yet the definition of “infrastructure” itself is evolving.

It no longer refers solely to bridges and roads. The infrastructure of the 21st century includes data networks, power grids, water systems, and semiconductor fabs. These are the arteries of a connected economy, and they require continuous technological upgrades to stay efficient and secure.

Kurita, Ibiden, and Sumitomo Electric are direct beneficiaries of this shift. Kurita enables sustainable water use in industrial plants. Ibiden provides the high-precision materials that power global chip production. Sumitomo Electric ensures the flow of electrons and information across continents. Together, they form a critical ecosystem that underpins digital infrastructure growth from Tokyo to Texas.

For investors, this presents a powerful diversification opportunity within the infrastructure universe. Traditional infrastructure assets like utilities and toll roads offer stability but limited growth. In contrast, these industrial innovators combine the resilience of infrastructure with the growth of technology, offering exposure to long-term structural trends with less volatility than headline tech names.

Valuation and the TAMIM Perspective

At TAMIM, we often describe our philosophy as second-level thinking, looking past the obvious to find value in the enablers rather than the end products. Kurita, Ibiden, and Sumitomo Electric fit this approach perfectly.

While global attention is fixated on AI developers, chip designers, and EV manufacturers, these Japanese firms quietly supply the inputs that make their success possible. Their valuations, relative to global peers, remain conservative. Many trade at forward earnings multiples well below those of Western industrial or tech companies with similar market positions.

Each company also exhibits balance sheet discipline, maintaining low leverage and consistent free cash flow. This allows them to self-fund research and capital expenditure without diluting shareholders. The result is steady compounding, modest but dependable, supported by real assets, long-term contracts, and deep customer relationships.

In portfolio construction terms, these positions anchor the Global Infrastructure Fund’s exposure to industrial technology. They offer geographic diversification, low correlation with Western peers, and participation in the long-term rebuilding of global supply chains. In an era of rising geopolitical risk and resource nationalism, the stability and neutrality of Japanese industrial champions become increasingly valuable.

TAMIM Takeaway

The next industrial revolution will not be won by those shouting the loudest but by those building the strongest foundations. Kurita, Ibiden, and Sumitomo Electric remind us that progress depends not just on ideas but on infrastructure.

Their work is measured in microns and molecules, yet their impact spans continents. They purify, connect, and power the systems that sustain modern civilisation. For investors, they represent the essence of durable compounding: businesses rooted in necessity, refined through expertise, and propelled by global transformation.

In a world chasing the digital, these are the companies quietly perfecting the physical.

Disclaimer: Kurita Water Industries (6370.T), Ibiden (4062.T) and Sumitomo Electric (5802.T) are held in TAMIM Portfolios as at date of article publication. Holdings can change substantially at any given time.

This week’s TAMIM Reading List explores wealth, wellness, and world events across an eclectic mix of stories. We begin with an inside look at why New York’s richest can’t quite leave, despite higher taxes, and travel to a Honduran island marketing itself as a longevity paradise. We unpack the $9B handshake between UnitedHealth and AARP, and a major drop in gun violence across 150 U.S. cities. Back home, Australians are set to benefit from free solar-powered electricity hours, while in tech, OpenAI inks a massive $38B cloud deal with Amazon. Finally, history literally crumbles as a medieval tower unexpectedly collapses in Rome.

Every first Tuesday in November, Australia stops. Offices pause, phones go silent, and productivity mysteriously dips around 3pm. The Melbourne Cup isn’t just a horse race, it’s a cultural ritual, a national pause button, and occasionally, a mirror reflecting how Australians think about risk, reward, and legacy.

This year’s Cup, won by Half Yours, offered a masterclass in what it takes to build lasting success, in business, in markets, and in life. It was a story of family businesses, preparation, resilience, and yes, a little luck.

In the winners’ circle stood billionaire families, corporate legends, and a jockey who not only made history but beat her own husband in the process. It was “a family affair” — and perhaps the most investable metaphor of the year.

Family, Fortune, and Focus

When Darren Thomas, Managing Director of Thomas Foods International, lifted the Cup alongside trainers Tony and Calvin McEvoy, there was something poetic about the moment. Here was a son carrying on his father’s billion-dollar business legacy, celebrating with another father-son team who had just trained Australia’s best stayer.

Thomas summed it up perfectly: “Whether you own a corner deli or a horse training operation, there’s something special about being family.”

The same could be said for investing. The best portfolios, like the best family enterprises, are built on continuity, alignment, and trust. They aren’t built for one race, they’re built for the track ahead.

At TAMIM, we often remind investors that markets reward longevity over brilliance. You don’t have to be the fastest horse out of the gates; you just have to stay on the course when others tire.

Tamim Takeaway: Great portfolios, like great racehorses, are bred over time, not bought on race day.

Preparation Beats Prediction

It’s tempting to think that winners in racing, like in markets, are the result of a lucky pick. But as any trainer will tell you, the Cup isn’t won on the day, it’s won in the months before, on quiet mornings when no one’s watching.

Half Yours had been racing without a break since April, a remarkable feat of endurance. That kind of consistency comes only from meticulous preparation and a team that knows how to manage energy, recovery, and timing.

In investing, we call that research and process. TAMIM’s investment framework, from daily screening to financial modelling to management meetings, is our version of early-morning track work. It’s what allows us to identify high-quality companies long before the market crowds them.

While others chase the next hot tip, we’re watching form, stamina, and temperament, the fundamentals that decide who stays the distance when conditions turn.

Tamim Takeaway: You can’t predict the winner, but you can prepare your stable for any track.

The Jockey’s Mindset

Few moments in sport capture composure like Jamie Melham’s final stretch at Flemington. As the pack surged behind her, Melham’s poise never faltered. When she crossed the line, she became only the second female jockey in history to win the Melbourne Cup, weeks after becoming the first to win the Caulfield Cup.

Her husband, fellow jockey Ben Melham, finished 14th. It’s hard to imagine a more dramatic metaphor for discipline and focus under pressure.

Investing demands the same temperament. Markets reward those who can tune out the crowd and execute their strategy with calm precision. It’s not about emotion; it’s about rhythm, patience, and understanding that some races are marathons disguised as sprints.

When volatility strikes and it always does, the investors who stay composed, who trust their preparation, who don’t oversteer at the first sign of mud, are the ones who finish well.

Tamim Takeaway: You don’t win by reacting to the noise from the grandstand.

The Odds and the Overconfidence Trap

Not every winner is strategic. Sometimes, it’s just a lucky punt. Take businessman and poker player Antanas Guoga, better known as Tony G, who admitted to betting $100,000 on Half Yours at $8.50 odds. He pocketed a cool $1 million.

His take? “It’s much easier just betting on horses and investing in them. That’s much easier than playing poker.”

That’s great for Tony G, but for every big win, there are hundreds of punters who go home lighter. Markets work the same way. There’s no shortage of people who “bet” on hot stocks or swing trades, mistaking speculation for strategy.

The lesson? Confidence is not the same as conviction. Conviction comes from research, evidence, and time-tested process. Confidence often comes from short-term luck and selective memory.

Professional investors build portfolios with the same discipline a trainer brings to a stable, controlling exposure, pacing risk, and ensuring every runner serves a purpose.

Tamim Takeaway: Every market has its punters and its professionals. The difference is process.

Better Than a Takeover

Among Half Yours’ ownership group was Rick Allert, the former chairman of Coles Myer, a man who’s fought some of Australia’s most intense corporate battles. Reflecting on his Cup win, Allert quipped: “This is better than a takeover.”

He might be right. Corporate success and market wins share one critical trait, emotional control. The best leaders, like the best investors, understand timing. They don’t rush into deals or trades for the thrill of it. They wait for alignment, clarity, and the right conditions.

In the Cup, Allert’s patience paid off. Purchased for $350,000, Half Yours has now earned over $8 million in prize money, a 20x return, not unlike what disciplined investors achieve when they stay the course.

Tamim Takeaway: Excitement is not a strategy. The best returns often come quietly, over time.

Timing, Weather, and Track Conditions

Cup Day isn’t always glamorous, but the great ones adapt. They know that track conditions change and the best-laid plans mean nothing if you can’t ride through the mud.

Investors face their own weather. Inflation, interest rates, elections, wars, all part of the unpredictable track. But those who build resilience into their portfolio, through diversification, balance sheet strength, and valuation discipline, don’t panic when the surface turns heavy.

The best investors, like the best jockeys, know what they can control (positioning, pace, preparation) and what they can’t (the weather).

Tamim Takeaway: You can’t change the rain, but you can train for the mud.

From Flemington to the ASX: Spotting the True Thoroughbreds

The Cup field is always full of promising names, pedigrees, and headlines. Yet, every year, only a handful deliver. The same is true for listed equities.

At TAMIM, our job is to spot the winners, the companies with stamina, leadership, and resilience to handle any track.

A company with a strong balance sheet is like a horse with a powerful stride, it keeps pace even when the field slows. A management team with integrity is like a good jockey, it knows when to push and when to hold.

And a business model with recurring revenue is like a horse bred for distance, it can go further than the rest.

This is why we look beyond short-term results to understand the breeding ground: how a company earns, reinvests, and grows.

Tamim Takeaway: Pedigree matters, in horses, in management teams, and in portfolios.

Legacy and the Long Game

Half Yours’ victory wasn’t just about prize money; it was about legacy. For the McEvoys, it was a family triumph decades in the making. For Darren Thomas, it was another chapter in a generational business story.

Investing, too, is about legacy. The compounding of capital over decades builds intergenerational wealth, but only when guided by patience and principle.

The families behind Australia’s great private companies, the Thomases, the Georges, the Allerts, share a common trait: they think in decades, not quarters. They reinvest profits, stay disciplined in adversity, and refuse to let short-term market sentiment dictate long-term direction.

That’s why the Melbourne Cup matters. It reminds us that endurance, preparation, and teamwork win the big races, not the loudest tip or the flashiest form guide.

Tamim Takeaway: Real wealth isn’t won on Cup Day, it’s trained over years of consistent effort.

The Emotional Dividend

When Jamie Melham crossed the finish line, she said, “Nothing ever, ever compares to this feeling right now.” You could feel the emotion, not just pride, but the release of years of hard work.

Every investor knows a version of that feeling, the moment a long-held conviction finally pays off. It might be a turnaround stock that doubles, a small cap that finally re-rates, or a portfolio that compounds quietly for a decade.

But that joy doesn’t come from chasing luck. It comes from doing the hard work early, staying disciplined when it’s dull, and trusting your process.

That’s the essence of long-term investing. It’s not glamorous, and it rarely trends on Cup Day. But it’s deeply satisfying, because it’s earned.

Racing and Investing: The Shared Playbook

Racing Lesson

Investment Parallel

Train for the track

Build for the market cycle

Trust your jockey

Trust your process

Breed for stamina

Invest in durable earnings

Ignore the punters

Tune out short-term noise

Respect the weather

Manage macro risk

Celebrate your team

Stay aligned with partners

Just as Half Yours was a collective effort, from breeders to trainers to owners, successful investing is a team sport. It takes analysts, managers, and investors all aligned toward a single goal: compounding capital over time.

Final Stretch: From the Winners’ Circle to the Portfolio

Standing in the rain at Flemington, Rick Allert declared, “Your heart doesn’t pump like it does here.” He was right. Markets rarely provide the thrill of a Cup win. But they do provide something better: freedom, stability, and legacy.

The Melbourne Cup may stop the nation, but for investors, it should start a reflection on patience, preparation, and the quiet power of long-term thinking.

Because in both racing and investing, the great ones aren’t chasing a single moment. They’re building something that endures beyond the finish line.

TAMIM Takeaway: In racing, the photo finish defines the moment. In investing, it’s the years between the races that define the legacy.

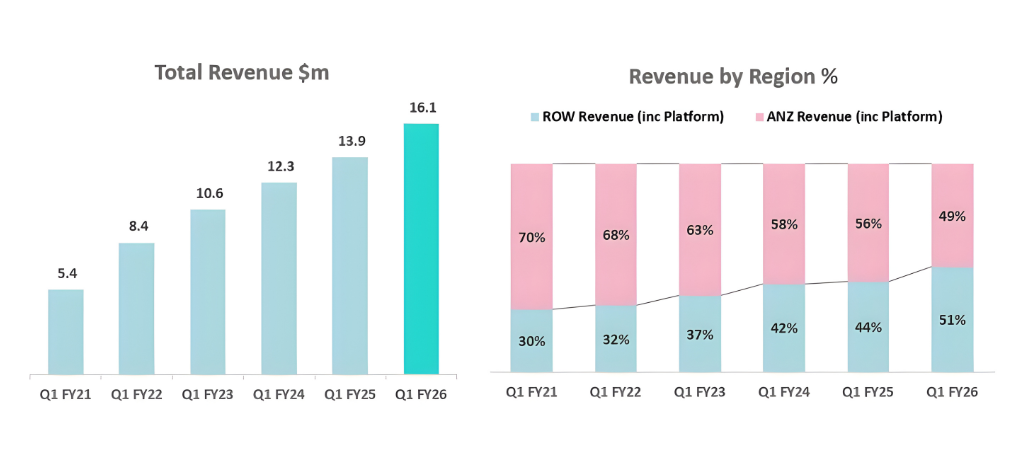

In the small-cap universe, few transformations are as profound as when a domestic success story becomes a true global operator. For Pureprofile (ASX: PPL), that turning point has arrived. In the September quarter, the company achieved a milestone years in the making: international revenue surpassed domestic sales for the first time in its history. It may sound like a statistic, but it represents something far more important, a validation of strategy, patience, and disciplined execution in a notoriously volatile industry.

From Research Boutique to Data-Driven Platform

Five years ago, Pureprofile was an Australian market-research firm struggling for relevance in a crowded local market. Fast-forward to FY26, and it has evolved into a global insights and data platform spanning 13 markets, with more than half its revenue generated offshore. The shift was neither sudden nor accidental. It was the product of a methodical internationalisation strategy, one that favoured building durable capabilities over chasing short-term growth headlines.

Pureprofile’s core proposition has expanded well beyond surveys and panels. It now delivers technology-enabled insight generation, allowing brands, agencies, and researchers to access high-quality, first-party data through a combination of human panels and automated platforms. In an era where data privacy and authenticity are paramount, that positioning has become immensely valuable.

The Mathematics of Global Scale

Numbers tell the story best. In FY21, offshore operations represented roughly 30 per cent of total revenue. Today that figure exceeds 50 per cent. This doubling of international exposure has fundamentally altered the company’s risk and opportunity profile. The UK and US markets, where Pureprofile has been deliberately investing, now contribute the lion’s share of global insights spending, together representing nearly 78 per cent of the total addressable market.

From an investor’s perspective, this diversification has three key implications:

Reduced geographic cyclicality; Australian advertising and research budgets are seasonal. Global diversification smooths those peaks and troughs.

Improved pricing power; International clients operate in more complex, higher-value research environments. That complexity commands premium pricing.

Higher margin potential; Platform-based revenue carries structurally higher EBITDA margins, and Pureprofile’s mix is tilting decisively in that direction.

Margins Built on Technology

Pureprofile’s management has long understood that profitability in this industry doesn’t come from human headcount, it comes from platforms. Roughly 20 per cent of group revenue now flows through technology-enabled channels, such as Data Rubico, the company’s self-serve insights platform. These products automate data collection, survey design, and analysis, cutting service delivery costs while simultaneously increasing client stickiness.

This evolution mirrors the shift seen in other SaaS-like models across the insights industry. Companies that successfully transition from project-based consulting to recurring platform usage often see EBITDA margins expand by several hundred basis points. For Pureprofile, the groundwork has been laid: scalable infrastructure, a growing base of recurring clients, and the operational leverage to monetise it.

Innovation as a Culture, Not a Slogan

Where many small-caps falter is execution fatigue, innovation gives way to maintenance. Pureprofile’s differentiator has been a relentless pursuit of product innovation. The company’s AI-driven research tools represent a structural leap forward. These tools use machine learning to segment audiences, predict survey outcomes, and reduce sampling bias, enhancements that elevate both data quality and speed to insight.

The result: higher customer satisfaction, lower churn, and stronger pricing power. It’s the difference between selling a service and selling a solution.

The US Opportunity: Playing on the Biggest Stage

If the UK was Pureprofile’s training ground, the United States will be its proving ground. The US accounts for over half of global market-research spending. Yet, despite the dominance of large incumbents such as NielsenIQ, Ipsos, and Dynata, there remains a substantial mid-market opportunity. Clients increasingly demand agile, transparent, and tech-forward partners, a gap tailor-made for Pureprofile’s model.

The company’s acquisition of iLink in Australia provided a template for how it might approach US expansion: disciplined valuation, cultural alignment, and integration that adds real capability rather than just scale. Management has hinted that strategic acquisitions could be on the horizon to deepen its American presence.

With a net-cash balance sheet and growing EBITDA, the company is well-placed to act when the right opportunity arises.

Financial Outlook: Growth With Discipline

Guidance for FY26, $63–64 million in revenue and 10–11 per cent EBITDA margins, signals a management team confident in both its trajectory and cost discipline. For context, this implies a near-doubling of EBITDA in just three years, alongside consistent top-line growth. Importantly, that expansion is self-funded. Pureprofile’s balance sheet remains unlevered, giving it optionality in capital allocation, whether toward acquisitions, technology investment, or potential capital returns in future years.

Valuation remains undemanding: 7-8× FY26 EBITDA for a business now structurally global, technology-enabled, and operating in one of the fastest-growing adjacencies to AI.

The Strategic Context – Data as the Fuel of AI

To fully appreciate Pureprofile’s long-term optionality, investors must step back and view it through the lens of the broader data economy. Every AI model, whether developed by OpenAI, Anthropic, or Google, depends on high-quality, permissioned data. The battle for differentiated datasets is intensifying, and companies that already possess longitudinal, verified consumer insights are becoming strategic assets.

It’s not inconceivable that in the coming years, AI developers or marketing-tech giants could look to acquire insights platforms like Pureprofile to enhance training data quality and consumer understanding. In this sense, Pureprofile’s growing global dataset, covering diverse geographies, demographics, and behavioural segments, may represent its most valuable hidden asset.

The TAMIM Lens – Quality Growth With a Margin of Safety

At TAMIM, we tend to look for businesses that combine three ingredients:

Earnings visibility: recurring or repeatable revenue models.

Operational leverage: where incremental sales translate into disproportionate profit growth.

Management alignment: leadership that thinks in years, not quarters.

Pureprofile now ticks each of those boxes. Its internationalisation strategy has created a natural hedge against domestic cyclicality. Its technology stack provides embedded leverage. And its management team has shown an ability to deliver on guidance consistently, an underrated signal of competence in the small-cap space.

The Competitive Moat – Not Just Panels, but Relationships

The market-research and insights industry is highly fragmented. The barriers to entry are low, but the barriers to trust are high. Pureprofile’s moat lies not just in its technology, but in its relationships with clients and panel members, built over years of transparent data practices and reliable delivery.

Moreover, its platform model means that every new client increases network value: more respondents, richer datasets, smarter algorithms. This flywheel effect strengthens over time and makes replication increasingly difficult for new entrants.

Challenges on the Road Ahead

No investment story is without risk. For Pureprofile, the key challenges are:

Execution risk in the US, competing with larger, better-resourced incumbents will require precise strategy and disciplined capital use.

Technology pace, keeping up with AI-enabled analytics and automation requires sustained R&D investment.

Currency exposure, as international revenue rises, foreign-exchange volatility becomes a more material factor.

Yet, these risks are the natural companions of opportunity. The fact that Pureprofile is now exposed to such dynamics is itself evidence of how far the company has come.

The Broader Investment Thesis

The global insights market is forecast to grow 6–8 per cent annually through 2030, driven by digitisation, privacy regulation, and the rise of predictive analytics. Within that context, Pureprofile occupies a sweet spot: small enough to be agile, established enough to be credible, and positioned at the intersection of data, technology, and marketing intelligence.

If management continues to execute, there’s a realistic pathway to doubling revenue again within five years, with EBITDA margins converging toward 15 per cent. At current multiples, that could imply significant re-rating potential as the market recognises its transformation from service provider to platform business.

Case Study: A Measured Globalisation Playbook

Pureprofile’s journey offers a blueprint for how smaller Australian tech firms can succeed globally:

Start with core capability, own a defensible niche domestically.

Export expertise, not ego, build relationships in select offshore markets before scaling.

Invest in process automation, technology is the bridge between small-cap resources and global reach.

Maintain financial discipline, fund growth through operations, not dilution.

In short, it’s about winning slowly but surely.

Valuation and Peer Context

When compared with peers in the global insights ecosystem, Pureprofile screens as deeply undervalued:

Company

FY26 EV/EBITDA

Revenue Mix

EBITDA Margin

Pureprofile

8×

51% International

10 – 11%

YouGov (UK)

14×

90% International

20%

Dynata (US, private)

~12×

80% International

18%

Even allowing for scale differences, the gap suggests room for multiple expansion as Pureprofile’s international revenues and platform margins grow.

Why Now Matters

Crossing the 50 per cent international threshold isn’t just a headline, it marks a structural re-rating opportunity. The market tends to treat companies as “local” until a clear majority of their revenue is global. Once that shift occurs, comparables change, investor coverage widens, and valuation frameworks evolve.

Pureprofile is at precisely that juncture. For long-term investors, such inflection points often represent the most asymmetric entry opportunities.

Looking Forward – The Next Chapter

Management’s focus now is twofold:

Deepening penetration in core international markets (UK, US, Europe).

Scaling platform revenue through Data Rubico and AI-enabled solutions.

These initiatives are mutually reinforcing, the larger the client base, the richer the data; the richer the data, the more valuable the platform. That flywheel, once fully spinning, could turn Pureprofile into one of the most attractive acquisition candidates in the Asia-Pacific insights sector.

TAMIM Takeaway

Pureprofile’s evolution from an Australian market-research boutique into a global data and insights platform is a story of quiet persistence and strategic patience. While the market has yet to fully recognise the scale of the transformation, the ingredients are now in place: a diversified revenue base, margin expansion potential, proprietary technology, and exposure to a structural growth industry.

At around 7× FY26 EBITDA and with a net-cash balance sheet, Pureprofile offers both value and optionality, a rare combination in the current market. For investors seeking exposure to the data economy without paying Silicon-Valley multiples, Pureprofile represents an inflection point in both growth and profitability. Its steady execution, expanding international footprint, and strategic alignment with the AI revolution make it an overlooked gem in the ASX small-cap landscape.

In a world where information is currency, Pureprofile isn’t just selling data, it’s building the infrastructure of insight.

Source: Pureprofile Limited (ASX: PPL) – Q1 FY26 Quarterly Report Investor Presentation

Source: Pureprofile Limited (ASX: PPL) – Q1 FY26 Quarterly Report Investor Presentation