Scott Maddock, portfolio manager for the TAMIM Australian Equity Income IMA, takes a look at the trade-off one must account for when aiming to generate income from an equity portfolio. He takes a look at two stocks held to deal with exactly that.

Income vs. Capital return – managing the trade-off in an income portfolio Scott Maddock CBG Asset Management

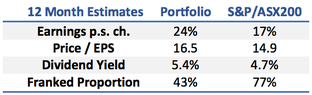

Source: CBG Asset Management

We can deliver income in a portfolio both by crystallising capital gains (selling securities at a profit) and by investing in high yielding securities. When building an income portfolio, we aim to balance investing in higher yielding securities against those with the possibility of growth in value. Few strongly growing companies pay a high dividend – preferring to reinvest capital back in to the business. This grows value but doesn’t pay cash to shareholders. The obvious step for an income portfolio is to focus on high yielding but lower growth companies. However, this ultimately results in low total returns to investors as;

Those companies often underperform the overall (growing) market.

Risk is higher due to excessive concentration in similar sectors / businesses.

Interest rate sensitivity is higher – demonstrated last year when the market withdrew the favoured status of property, utilities and infrastructure.

Our approach therefore has been to build a portfolio which has a yield higher than that of the broad market but also holds shares in companies capable of growing returns or asset values.

This provides the potential for a higher total return while ensuring the income stream generally exceeds that available from cash and interest rate securities. The trade-off means we hold some stocks with high yields, some with low yields but good earnings growth and some which fit in the middle of both ranges.

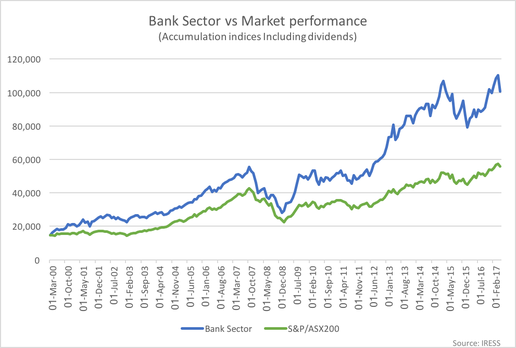

A fine example of this trade-off is the Bank sector. Banks have long been a no-brainer for investors looking for tax effective income (fully-franked) and capital growth Historically, high returns on capital, strong credit growth in the economy and the ability to restrict cost growth to a lower rate than revenue growth supported the sectors total return. Even with a step down in credit growth post the GFC, the banks have outperformed. Credit growth remained solid, reduced competition supported net interest margins and lower credit growth allowed the banks to increase dividend payout ratios. However, capital requirements have now risen, reducing the sustainable payout ratio for a given level of growth. Dividend payout ratios look stretched for NAB and Westpac suggesting little dividend increase is likely. We expect further slowing in housing credit growth and, combined with factors such as the bank levy, the result will be slower earnings and dividend growth. The sector has therefore become less attractive.

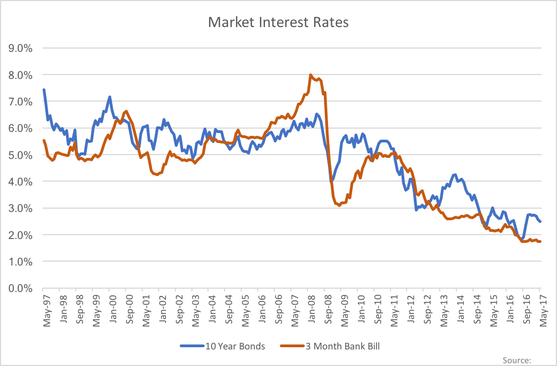

This is the end (?) of a trend which has been dominant in the Australian investment market since the early 1990’s. The implications are that we need to look further afield, to build a portfolio of investments intended to deliver a solid total return while also paying a level of income. Clearly current interest rate levels are not sufficient to deliver a meaningful income from cash, term deposits or longer term bonds. Bond rates are below 3% while shorter term rates are below 2%.

Two stocks we currently include in the portfolio which offer a bit of both income and capital growth potential are Charter Hall Group (CHC.ASX) and Regis Healthcare Limited (REG.ASX);

Charter Hall is a property funds management business with a successful track record of fund expansion and performance delivery. CHC shares are currently trading on a 12mth dividend yield of 5.2% (unfranked) while delivering strong earnings growth as commercial property values remain strong and demand for professional management of property portfolios drives increased funds under management. CHC also co-invests in the funds and so has a focus on increasing asset values as well as maintaining income levels.

Regis Healthcare is a high-quality operator of Aged Care facilities. Share prices in the sector have been depressed by changes to government funding formulae however REG has been less affected by these changes than the market expected. REG shares are currently trading on a 12mth dividend yield of 4.8% (100% franked) while maintaining a strong outlook for earnings growth in coming years.

This week Guy Carson, manager of the TAMIM Australian Equity All Cap Value IMA, takes a look at the Bank levy announced in Budget 2017. Will the cost be passed on?

Will the bank levy be passed on? Guy Carson

Four weeks ago we wrote an article entitled Australian Banks: The death of a 25 year bull market, in which we looked at recent history and suggested that the tailwinds of lower interest rates and favourable regulation were over for the Big four banks. With regards to regulation, we focused on recent changes from APRA and the indication from that organisation that further measures were to come. What we didn’t expect at the time was action from the Federal government and to that regard we were surprised by the introduction of a bank levy in the 2017 Budget last week.

It is fair to say the banks were caught off guard as well by this move as well. In response the CEO’s of the big four have issued statements suggesting that the cost will be felt by “shareholders or customers” or perhaps a combination of both. The government hopes that the banks will not pass the increase on to customers, with Scott Morrison saying “The banks want to send a message to their customers about how much they value them? Don’t do what they may be contemplating doing [raising rates or reducing returns]. Don’t do it.” Therefore, the suggestion from the government is that shareholders wear the cost.

In order to determine who will feel the bank levy, it’s important to step back and to look at two things:

What is the bank levy? How does it work?

How might the banks react to this new charge?

What is the bank levy?

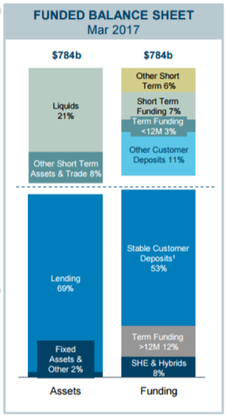

In order to understand how the bank levy works, it’s important to understand how banks are funded. The big four currently have leverage ratios of approximately 5% (ANZ 5.3%, CBA 4.9%, NAB 5.5%, WBC 5.3%), this effectively means they have leveraged their equity 20x and the remaining 95% of the balance sheet is funded by liabilities. It is these liabilities that the bank levy is set to target.

The levy applies to all bank funding outside of shareholders equity (including retained earnings) and deposits less than $250k. The below chart breaks down ANZ’s current balance sheet by both assets and funding source, it is the funding side that we need to focus on.

Source: ANZ company filings

Roughly speaking, the Big 4 have balance sheets that are 10% funded by Shareholders Equity (SHE) and Hybrids, 60% funded by customer deposits and 30% by wholesale funding. The wholesale funding above is split into short term and term funding. These buckets are a product of capital markets and include instruments such as corporate bonds and commercial paper. These bonds are typically held by offshore institutions.

The levy is 6bp and is charged on the liabilities as identified above. To break it down further:

The wholesale funding on the balance sheets of the big four will be subject to the levy, it’s impossible to avoid. So at a minimum 30% of their balance sheet will be subject to it.

The equity component which ranges from 4.9% for CBA to 5.5% for NAB will not be subject to the levy. Note that the 8% number in the diagram from ANZ above includes hybrids which are subject to it. This potentially means less hybrid issuance going forward.

The grey area is where the bulk of the funding comes from and that is deposits. A majority of the current deposit base is over $250k and is subject to the levy. How the banks react to this is potentially the key to who bares the cost of the levy.

How will the banks react?

The banks were caught off guard by the announcement of the levy and as a result we are yet to see any reaction outside of a few statements warning of the consequences. Therefore we’re not yet sure on what will happen but we can look at some hypothetical scenarios. The banks have indicated that the costs of the levy will be felt by “shareholders or customers”, we’d also add in a third category: staff.

Essentially we can see three ways the Australian banks may react:

Take the hit and see Net Interest Margins (NIM) reduce. Meanwhile try to offset the NIM impact by reducing staff numbers, improving productivity and lowering the cost to income ratio.

Since deposits under $250k are now more attractive on a relative basis, the big four could increase Term Deposit rates for lower amounts and try to lock in funding that way.

Increase interest rates for borrowers, most likely mortgage holders as that the bulk of their asset book.

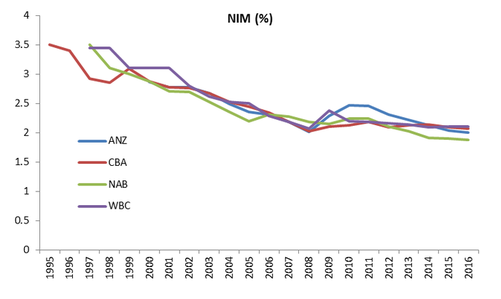

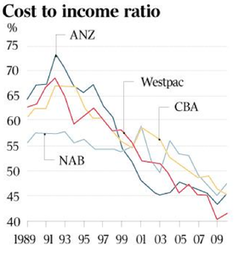

We’ll start by looking at scenario one. The banks NIMs have been declining for over 20 years from levels of around 3.5% to 2.0% today.

Source: Thomson Reuters & company filings

The offsetting factor though has been their productivity. Technology and scale has brought down the cost to income ratio for banks by allowing them to work more efficiently with less staff concentration. The below chart shows this with cost to income ratios dropping from above 60% in the early 1990s to around 40% today.

Source: The Australian, CSLA

So if the banks were to except the 6bp charge on their NIM, they may look to reduce staff numbers and costs further. This is a path the banks are currently undertaking and ANZ CEO Shayne Elliot was very open at the recent result that in a low credit growth environment, the only way to grow profit is to shrink your expense base. ANZ has stripped out $150m of staff costs over the last 12 months and plans to cut it further over the next two years.Ultimately, the banks won’t be able to fully offset the NIM impact through cost control but it will help.

Moving onto scenario two. In August last year, after the RBA cut interest rates we saw something unusual. The big banks all moved to increase term deposit rates. This lasted for about a month and was essentially a market share grab from the big four against the smaller players. Given the now relative attractiveness of smaller deposits, we may see something similar in the coming weeks. The flow on effect will be that players such as Bendigo Bank and Bank of Queensland will be forced to increase their rates to compete. Therefore funding costs across the industry will rise. Although it must be noted that the regionals will still have an advantage over the big four, as it is impossible for the big four banks to reprice their entire funding book. It is only the marginal flow that will be repriced which is a small aspect.

Rising funding costs brings us to scenario three and the pass through. If the big banks do successfully push marginal funding costs up across the industry, then mortgage rates will rise. This follows a recent trend of “out of cycle” rate rises. The interesting thing is that it is questionable, given high household debt, whether the economy can withstand increasing interest rates. As a consequence if rates do continue to rise, it raises the probability of further RBA cuts later this year.

Now these three scenarios are not mutually exclusive. Ultimately we’d expect all three to happen to some degree. Banks have been cutting costs for some time in the face of slower revenue growth, it can be expected this will continue. We expect there will some sort of market share grab with respect to Term Deposits in the not too distant future and in conjunction with that we might see a rise in interest rates for mortgage holders right across the industry. The combination of all three may still not be enough to absorb the levy and hence the prices of the Australian banks have fallen since its announcement.

So where does this leave us with respect to our view on the banks? In our recent piece, we noted that banks faced a risk of greater regulation and whilst we did not expect this levy, it is part of a greater trend. This levy therefore further reinforces our view that the best days in terms of share price performance are behind them.

Finally, we do note that the recent history of the Australian government is not great with regards to market timing. In 2012, the then Labour government signalled the end of the mining boom when they introduced the mining tax. Has this Liberal government’s 2017 Budget managed to do the same with the banking boom?

Robert Swift, of the TAMIM Global Equity High Conviction IMA, was recently invited to attend the ever-popular Berkshire Hathaway AGM. He has taken the time to write some notes on what he found interesting and what he observed.

Berkshire Hathaway AGM – notes from the ground

Robert Swift

It’s one of the most sought after AGMs to attend globally and it typically happens in May in Omaha, Nebraska. It is, of course, the Berkshire Hathaway AGM hosted by Warren Buffet and Charlie Munger. It is an investment and media frenzy with unbridled adulation for the duo even from wealthy investment industry veterans. To give you some idea of the frenzy, the presentation kicks off at 9am; the doors to the auditorium open at 7am, and the queue for good seats started up at 5am outside! I went with a friend who is a (happy) shareholder and he was kind enough to drop me off at 5.45am to save his place in the line. In years gone by he had his place saved by younger analysts who would sleep out overnight to ensure he got in right at the front. I was a severe disappointment to him with my lack of commitment!

I attended this year for the first time. I am glad I went and I found the whole exercise fascinating from an investment and sociological perspective.

It was actually great fun, and informative, to chat to folks queuing patiently early in the morning. There were people from all over the world, and people with plenty to say about the state of capital markets, and provide their opinions on politicians and central banks.

I also spent the previous afternoon strolling around the exhibition hall in which Berkshire showcase, and sell, as many of their products as they can. They have turned the company AGM into another profit centre. Smart to get investors to pay for your own AGM!

Rather than analyse Berkshire Hathaway which plenty of folks do, (it is one of the largest USA companies by market capitalisation) I thought it might be more interesting to make observations from the Friday and Saturday: the shopping in the exhibition hall, and the queuing, and then the Q&A at the AGM with Warren Buffet and Charlie Munger answering a very wide range of questions and dealing with some protests too.

Americans really don’t mind wealth creation. It’s clearly felt that Warren and Charlie are worth every cent they have made. There is no begrudging their fabulous wealth (Warren Buffet’s 17% stake is worth about USD$70bn) and there is no jealousy or outrage about this net worth. The only outrage came from a German activist investor in the Q&A. At least from what I saw. This attitude to successful wealth creation and the ‘equal opportunity’ is perhaps uniquely American. The obverse attitude to wealth is creeping in in some countries and that is felt to be a bad thing – at least by those queuing and they weren’t all Americans.

The consumer likes theatre and company and will spend money. Plenty of people were spending plenty of money on Friday and were seemingly buying stuff which was readily available on line or in department stores. It is no secret that the retail scene in the USA is depressed but it may be that the retailers are just doing it wrong? The trick appears to be to get crowds in and to have entertainment. It is all about getting footfall traffic because the impulse to buy, once inside, is enormous. USA retailers have waited for shoppers who then receive unsmiling service. The products haven’t been pitched and it isn’t a theatrical or memorable event but merely a transaction. Cheap ice creams and a chance to sit in a NetJets cabin; helpful and plentiful service, and some unique items for sale at this event only, all made for plenty of spending and happy people. Retailers everywhere take note. Make your spaces fun places.

There is a serious issue with the perceived ethics and integrity within the USA political and business system. By comparison, Warren Buffet, who has pledged to give away his fortune on his death, is a shining light. His statements on executive pay (too high) and incentives (too easy) went down well. He nicely illustrated the bias in current share option schemes where the strike price remains static such that the executives with such a scheme in place, can take more of the business from its owners (the shareholders) merely by doing their jobs.

Invest for the long term and let the power of compounding do its magic. Berkshire was a leading New England-based textile company. Buffett took control of Berkshire on May 10, 1965. At that time, the company had a market value of about $18 million and shareholder’s equity of about $22 million. It was a steal relative to net worth at the time but its market capitalisation is now over USD$400bn. We all try to ignore the short term but it’s hard because what we buy is typically marked to market on a daily basis. Berkshire owns outright much of what it buys and its valuation schedules allow it to look through any short term volatility.

Clearly you can’t double every year but even 8% pa with minimal volatility makes for a large number over a lifetime of investing. Be long term greedy.

Berkshire Hathaway is actually a hybrid Private Equity listed USA equity value biased business. To compare its NAV progression against the S&P 500 is incorrect and to challenge Berkshire to a performance contest with an equity fund is a mismatch. It would be better to compare its NAV progression against a pool of private equity fund returns and the S&P500. Given that Berkshire has no need to exit its investments, nor to deploy its capital raised quickly into deals it has a competitive advantage against PE funds too. While it is unique it is surprising that a hybrid like this isn’t in evidence elsewhere? Maybe Softbank in Japan is the nearest thing?

The benefits of flexibility offered by free cash flow are enormous. Too much debt is a serious problem. Markets panic routinely and the ability to deploy capital from free cash flow or having liquid assets gives you the chance to strike. Fortunes are made at the bottom not at the top. Berkshire invested about $50bn in 2008. The value of the insurance companies, owned by Berkshire, in providing this cash flow are increasingly apparent. Maybe Softbank isn’t quite there yet in not having this free cash flow?

PE funds are currently bidding up the value of private businesses making it hard to deploy capital in this area. Valuations are rich and sacrificing liquidity in the pursuit of an extra 2-3% return or for tax minimisation is currently dangerous. Valuations are also rich in government bonds and you shouldn’t be lending the government money at these interest rates either!

We hope this article is different and interesting. We are not going to try and copy Berkshire’s investing structure but interestingly have some listed companies in common.

This week the Small Cap team take a look at why investors frequently undervalue a simple but proven business and instead hit for the fences with supposed disruptors.

Why investors often undervalue simple businesses

Summary:

We have noticed that investors often gravitate towards exciting but unproven business models which promise disruption. In contrast, investors often tend to overlook more simple business models which are generating good cash flows here and now. We view this behavioural bias as a key driver behind the opportunity set we are focused upon capturing, the under-valued high quality smaller companies which consistently generate cash flows and tend to out-perform long term.

Investors love excitement!

In our experience there is a clear behavioural bias in the smaller companies’ market towards the more exciting stories. Investors often tend to gravitate towards businesses which promise to revolutionise a market in reaction to a major challenge which people can identify with. When these businesses are presenting to investors they tend to highlight the challenge they are aiming to address and then show numerous charts showing what it would mean for their business if their new approach could gain only a small portion of the entire existing market. Such presentations can dazzle investors with compelling big picture charts and very large numbers. This is how hype is created in the investment world.

Big win mentality: the driving force

So why are investors so attracted to the hype? Why does it attract highly intelligent people despite the seemingly obvious risks?

The fact of the matter is a very small portion of revolutionary business models will succeed over the long term, and thus create enormous wealth for their early shareholders along the way. As can be seen here, for example, if you had invested in Amazon at its IPO you would currently be sitting on a c.49,000% increase in value since 1997.

There are other similar examples of life changing gains in revolutionary new business models, and each story will have been told thousands of times over until it has reached near mythical status. And this is what is driving investor interest in “blue sky” business models; a belief that “this could be the one which creates life changing wealth for me”; often referred to as a big win mentality.

Putting a value on “blue sky” business models often irrelevant

At this point it is worth asking: how does one value a “blue sky” business model which is aiming to capture an emerging opportunity?

As a starting point, investors don’t have many financial metrics to focus upon since most of these companies don’t generate earnings or even revenues. As a result, investors will often look at the overall market size and work back to a fair stock value based upon successful market share capture by the business looking forward.

This backwards methodology of valuing a business pre-supposes that the business model is going to be successful over the long term, despite a complete lack of evidence.

Why “blue sky” investing doesn’t generally work…

It is obvious where we are going with this.

While a small portion of investors will benefit from Amazon like returns by investing in a revolutionary start-up, we believe there are a number of reasons which explain why investing in “blue sky” business models is generally a poor long term investment strategy:

High risk of disappointment – By investing with a strong-held assumption that an unproven business model will succeed, and valuing the business on this basis, investors are very exposed to disappointment risk.

When the disappointments come they are usually of significant size – When a new business model fails to gain traction as hoped, the difference between the expected financial performance and the actual financial performance is usually large. With large disappointments, come large share price falls.

The hit rate of highly successful “blue sky” business models is remarkably low – Most investors’ chances of being exposed to the right business model is very low as a result.

It is hard to invest with conviction in “blue sky” companies which means it is highly unlikely most investors would invest enough capital (if there is one successful “blue sky” company in their portfolio) to make the life changing gains they are aiming for. As a result, if a portfolio is exposed to one of the few successful “blue sky” business models, its positive returns will be from a low weighting, and are likely to be heavily diluted by the decreasing valuations across the less successful emerging companies in the portfolio.

Want to change lanes? Simple business models: a few simple ingredients

So what are the key aspects of a simple business model? Here is our list:

Long term trading history, preferably as a listed entity – A company which has been listed for many years is far easier to understand than a newly listed entity as a long term listed history will reveal the business’s key growth drivers and risks.

Earnings and cash flow positive – We view this as a key requisite of a simple business model. All businesses should ultimately be about generating a profit and positive operating cash flow. Rather than speculating if a business will achieve profitability in the future, we believe the true simple test is here and now.

Understand-able business model and activities – This one is key. We always ask ourselves if we genuinely understand how a company is making money. And to be honest, the answer is often no with “blue sky” business models.

Honest and competent management – When we meet a management team we want to walk away with a feeling of trust that they are running the business competently and are honest with their shareholders.

Stock example – an under-valued simple business model: PNC

Pioneer Credit Limited (ASX:PNC) is a great example from our portfolio of a simple, profitable business which is growing its earnings through sensible strategies from an excellent management team.

What does the company do?

PNC is a financial service business specialising in the purchase of debt ledgers.

Do we understand the business?

Yes, we do– the company aims to generate the highest possible pay back from each debt portfolio it purchases: i.e. the company may purchase a portfolio for only 20c in the dollar with the intention of generating as high as possible a payback in the coming years.

Does the company generate earnings and a positive cash flow?

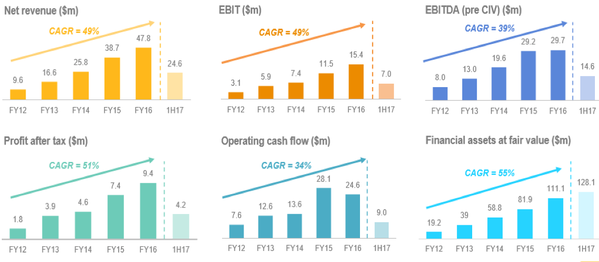

Yes, the company recently reaffirmed its FY17 guidance of at least $10.5m statutory NPAT, while it also guided to an additional 12% increase in earnings for FY18 based on pre-announced FY18 EPS consensus of 24 cents (approx. 27 cents or $16m NPAT).

KEY PNC FINANCIAL METRICS: FY12 to FY17

Source: PNC company presentation

Does the company have a long term trading history, preferably as a listed entity?

Yes, the company has been listed for 3 years and had been highly successful for a decade prior to listing.We first invested in PNC in mid-2015, and have increased our investment in the company over time as we have become more comfortable with management, the business model and the company’s long term potential. Over that time PNC has also grown from being the minnow of the ASX listed debt collectors (after Credit Corp and Collection House) to being the second largest acquirers of ledgers in FY17.

Market awareness has increased over this time, as has broker coverage. Four brokers now cover PNC with price targets of between $2.00 and $3.05. FY18 earnings estimates are generally in line with PNC’s guidance (ranging from 27 cents to 28 cents) which puts PNC on a PE multiple of approximately 7x to 8x earnings at current prices.

Are management honest and competent?

In our experience, yes. We have met them a number of times and have always been very impressed.

Conclusion:

Call us simple but we will stick with investing in simple, profitable businesses which are growing their earnings by virtue of sound management strategies. We believe this strategy will continue to deliver superior long term returns.

This week the Small Cap team review their investment in Zenitas Healthcare Limited (ZNT.ASX).

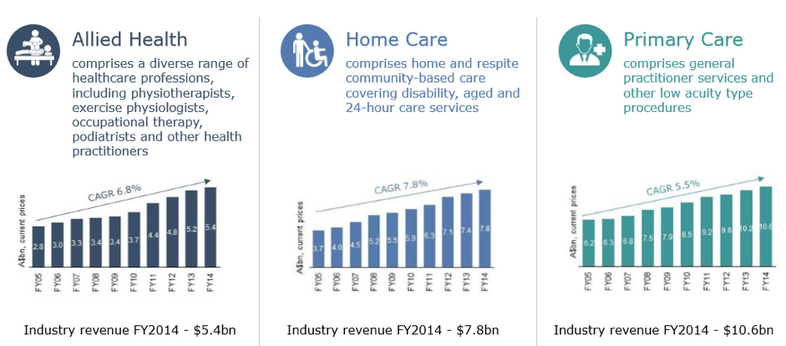

Zenitas Healthcare Limited (ZNT.ASX – formerly BGD.ASX) is a community healthcare company providing a range of community-based health services – allied care, home care & GP services. Combined, these services enable an integrated healthcare offering, primarily aimed at reducing the high cost of acute hospital care. Community healthcare is expected to benefit from supportive government policy, as community-based health services represent a cost effective solution compared to high cost hospital care. The three areas in which ZNT operates have demonstrated solid long term growth as shown below:

Source: ZNT company filings

We first invested in ZNT when it was known as BGD Corporation in December 2015, when it was undertaking a small raising to fund the acquisition of a group of profitable GP clinics (Modern Medical) and had a market capitalisation of under $5m.

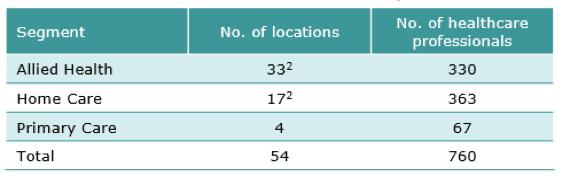

In December 2016, we increased our investment in ZNT by participating in a larger capital raising ($30m) to fund various acquisitions, which was well supported by Australian institutional investors and an Asian healthcare investor. ZNT now operates from 54 locations throughout Australia, employing 700+ health professionals, providing services across allied health, home care and primary care (GPs). ZNT now owns Australia’s largest allied health/physiotherapy business, and the first ASX listed home-care business.

Source: ZNT Prospectus (October 2016)

Note: ZNT’s Allied Health division provides home care services in WA

ZNT’s offering is unique, in that it is focused on having its three divisions (allied, home care and primary care) complement each other, through:

Offering an integrated patient care approach utilizing services from across its divisions;

Cross referrals (particularly from GP to allied health, i.e. chronic disease management);

Co-locating facilities; and

Centralised management and administration.

Since relisting in January, two brokers have commenced research coverage on ZNT:

Wilsons (current price target $1.25) noted “Zenitas Healthcare offers an exposure to the emerging Australian community-based healthcare market. We expect Zenitas will deliver solid network growth as it expands and integrates three service verticals in allied health, general practice medicine and homecare.”

Bell Potter (current price target $1.27) noted “Zenitas Healthcare is a fresh take on corporate healthcare in Australia. The business incorporates General Healthcare, Allied Healthcare and Home Care Services in an integrated model that aims to service high needs patients and the growing home care industry”.

In recent months ZNT’s Management has been focused on developing the cross referral network of the current businesses and building out practitioner numbers/utilization rates in those facilities that have excess capacity. Given the relatively fixed cost base, these initiatives offer meaningful earnings upside.

ZNT also has an extensive pipeline of acquisition opportunities currently under review that have the potential to add significant scale to each of the three ZNT verticals. ZNT currently has debt and equity funding available of up to $20m to pursue these acquisitions (equating to a possible contribution of ~$4m to $5m in EBITDA earnings).

Bell Potter have assumed FY18 earnings incorporates an additional $3m of acquired EBITDA (resulting in total EBITDA of $9.7m forecast for FY18), which flows through to their forecast EPS for FY18 of 10.5cents. On current prices, this places ZNT on an FY18 PE of under 10x and a 5% dividend yield. Wilsons are forecasting more modest acquired EBITDA ($1.4m) in FY18 in their assumptions (forecast FY18 EBITDA of $8.0m), therefore ZNT has the balance sheet capacity to comfortably exceed broker forecasts (i.e. the potential to acquire up to $5m EBITDA to add to their FY17 forecast EBITDA of $6.6m – reaffirmed by ZNT on 28 April 2017) without incurring dilution.

We like ZNT as it is in a sector supported by strong tailwinds and encouraging thematics, it is priced on an undemanding multiple, has multiple and credible pathways to grow, and is run by an experienced management team. While it is early days, (ZNT currently has a market cap of $45m), ZNT has the platform in place to become a leading national community healthcare player and respected brand, with the potential to have multiple clinics providing integrated services offerings in major cities throughout Australia.

Recent ASX announcements indicate that larger institutional investors that supported the December 2016 capital raise have been buying more stock on market. We have also been adding to our position into recent weakness, and ZNT now represents one of our larger holdings.

Source: CBG Asset Management

Source: CBG Asset Management