This week, as a follow up to a recent telco article, Guy Carson takes a look at Inabox.

Recently we wrote an article looking at the Telecommunications industry in Australia. Our main premise was the introduction of TPG Telecom into the mobile space would cause problems for the existing players and lead to lower margins across the industry. We received a lot of feedback on that article and the most interesting aspect was the amount of readers who had started to move on from the large Telcos and look elsewhere for cheaper alternatives. As a result of this, our belief that the smaller players will continue to rise has been strengthened. These players are typically large non-Telco companies that wish to cross-sell to existing customers and it creates an interesting dynamic in this market. Access to customers is a crucial element that these new competitors have over the incumbents and could lead to a substantial shift in consumer behaviour.

One company that will potentially benefit from this trend is Inabox (IAB.ASX). Whilst the company only has a market cap of $20m, it has a surprising amount going on under the service. The core competency of the business is its Telco-in-a-box platform. This platform allows anyone to become a Telco reseller and they currently have approximately 450 out of the current 1,200 National Broadband Network providers as customers. This means they are exposed firstly to new entrants wanting to setup a Telco capability, and secondly to the growth in subscribers amongst those non-mainstream brands. They also have exposure to the top end of town, as their platform is used by Belong which is Telstra’s low cost brand.

One of the keys for the company is their ability to white label a Telco offering. This means they can partner with non-Telco retailers to enable them to provide these services. The potential here is large. When we look experience offshore we find that retailers have had significant success. For example in the UK, Tesco is now the 2nd biggest Telco provider. The possibility here is that Woolworths, Coles, Aldi and other major retailers can use a platform such as this to add an additional revenue stream from existing customers and capture more of their wallet. The nature of the Telco market hence has the potential to change dramatically over the coming years. Whilst Inabox has a number of strong and significant clients already, the announcement of a blue chip retail client could be a real turning point for the company and its profile.

Source: Company filings

Inabox is largely unknown at the moment and their financials appear messy at first glance. They have been consistently profitable since listing but despite that they have struggled to gain any significant momentum. The acquisition of Hostworks this year could potentially change that. Hostworks was acquired for $7m from Broadcast Australia, who paid $69m for the same business back in 2008. The acquisition adds a cloud services capability to the business in addition to its Telco operations; as a result the company is able to service firms across the entire spectrum of communications and technology. When we add in the runrate EBITDA of the acquisition to the Inabox business we can expect a meaningful step-up in FY18.

The acquisition though did bring some one-off costs and as a result EBITDA and NPAT fell this year. Stripping out those costs, underlying EBITDA rose to $6.1m on flat revenues as low margin operations were exited. As mentioned above, the full year contribution from Hostworks is set to boost this number further in FY18. The company has spent a significant amount of capital building out its platform capabilities and potentially has one more year of circa $4m spend ahead of it. Post this spend a majority of the EBITDA will fall to the bottom line, after some tax of course. Recent guidance is for $100m revenue in the next year, up from $90.1m this year. If EBITDA margins are maintained (and in fact we believe there is the potential that they expand), the company will achieve EBITDA in the order of $6.8m. With a current market capitalisation of $20.1m, the shares are currently trading on a very undemanding multiple.

It must be pointed out that this is a very small company with a little bit of debt so an investment is certainly not without risk. However, given the nature of their platform and the fact that 76% of their revenue is recurring we believe the company is significantly less risky than most other microcap companies. In addition, it operates in the area of connectivity which is a growing sector and has structural tailwinds that should support it over the coming years. Whilst it may not be our largest position, we believe it is worthy investment for part of our capital.

This week the Small Cap team provide a profile on one of their portfolio holdings, Elanor Investors Group (ENN.ASX).

Property and hotel/tourism fund manager and investment company, Elanor Investors Group (ASX:ENN), is a core long term holding of the fund that we believe represents compelling value at current prices. We have been adding to our position in ENN recently.

ENN ticks a large number of boxes for a high quality business including:

Strong management with a proven history of operational out-performance;

High levels of recurring income;

A strong track record of buying assets well, adding value and then realising the asset value;

Favourable tailwinds in the form of growing long term investment demand for high quality, high yield, tourism and property assets; and

An exceptionally strong balance sheet.

In terms of value, ENN is currently trading broadly equal to the market value of the various real estate, tourism and investment assets that it owns. In addition to the ‘hard’ assets that it owns, ENN is building a very successful and profitable funds management division that the market is attributing limited value to. In our experience, this is an unusually attractive opportunity for a high quality, well run business.

The funds management business

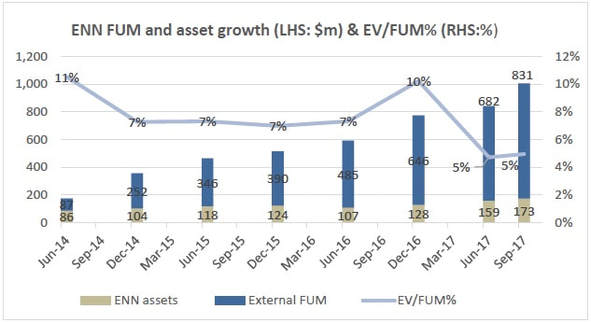

ENN’s funds management business currently has around $800m in external funds under management, and generated segment EBITDA of $8m in FY16 and $11m in FY17.

The business has powerful leverage to ongoing funds under management (FUM) revenue growth and significant potential performance fees. ENN’s management are optimistic about converting their strong pipeline of new fund initiatives which should support good growth into FY18, following a significantly increased origination and capital raising capability.Management’s ability to purchase assets well, and to add value to assets through active and astute management has also resulted in significant embedded performance fees (off balance sheet) that will accrue to ENN as assets are realised over the coming years.The key funds that ENN currently manage include:

Elanor Retail Fund (ASX:ERF) – listed on the ASX in 2016 with gross assets of over $250m

Elanor Hospitality and Accommodation Fund – unlisted fund formed in March 2016 with gross assets of over$100m

Elanor Metro and Prime Regional Hotel Fund – recently announced unlisted fund with gross assets of $73m.

As illustrated below, the growth in FUM over the past several years has been impressive, however the emerging funds management business being developed by ENN has yet to be properly recognised by the market.

Source: Company reports and DMXAM estimates

The chart above sets out the growth in assets both owned by ENN and externally managed by ENN, together with our calculation of the business value (enterprise value) as a proportion of external funds under management – a metric that highlights the relative value the market is applying to ENN’s fund management business.

When ENN listed on the ASX in 2014, its funds management business was valued at 10% of its FUM at the time. This metric has been reducing and sits at c. 5% today, which indicates the business is cheaper now relative to any other time in its trading history. Further, if we were to adopt our estimates of the market values of ENN’s investment assets, rather than the audited book values (with some key assets recorded at cost) used in the analysis above, then the business would appear even cheaper, at less than 2% of its FUM.

The market has been attributing less and less relative value to ENN’s funds management business, over a time when the business has been generating increasing profits and scale and a track record of strong performance outcomes – this represents a compelling opportunity for us. ENN’s underlying funds continue to mature and provide potential for ENN to capture material performance fees.

Valuation

As value investors we are focused upon identifying the most compelling under-valued high quality smaller companies on the ASX. ENN currently stands out as a particularly compelling value opportunity based upon its asset and earnings base.

As a result of recent valuation uplifts to its Hotel and Tourism assets, and forecast mark to market values of its real estate (e.g. ENN’s Merrylands property) and co-investment assets (e.g. ENN’s Belly City fund investment) we estimate ENN’s underlying NAV is now approximately $2.00. With its current share price at around $2.10, this implies very limited value is being applied to ENN’s funds management business. We view the current opportunity to buy a share of a high quality funds management business with a top class management team for next to nothing (and where the share price is supported by the value of its assets) as unusually attractive. Catalysts to potentially unlock this value include the sale of non-core assets, new fund initiatives and asset realisation / generation of performance fees. We remain committed long term investors and look forward to seeing this value being unlocked over time.

Everyone has been obsessed with the FAANGs, FAAMGs or “Sexy Six” for a while now but Robert Swift, manager of the Global High Conviction strategy here at TAMIM, only holds one. Robert takes a look a one of his better performing stocks of late to help explain why this is while examining the fallacy that stocks can be defined by a singular sector.

We often show investors our sector and region weights. These are important aspects of our portfolio construction process because ensuring a wide spread of sector and country exposure is a sensible way to diversify and control exposure to a detrimental event in any one country or sector. The sector definitions make intuitive sense, as do the regions or countries into which the companies are placed, but companies are often classified as one type of company when they are really another. Understanding what drives a company’s profitability, and where the risks lie, is important and to that extent it is important to not just passively accept the classifications given to you by convention.

This is why a sophisticated risk model is critical since many companies classified as one type of business actually contain elements of others. Put together in a portfolio these elements can combine to produce large unintended and undesirable characteristics. Portfolio management is more than picking stocks one by one – you have to know where the aggregated risks are and how big and how to measure them.

A current example of a technology stock which perhaps isn’t, would perhaps be Apple, which is increasingly a consumer goods company? Most of its manufacturing is outsourced although it designs the items and operating system; it relies heavily on constant fashion cycles to drive revenues; and it sells directly to the consumer from its own branded stores. If it were a French luxury goods company such as LVMH or Hermes, would it be treated and rated differently by the stock market? Quite probably. Similarly, Google, while definitely still a tech stock, could also be considered one of the world’s premier advertising companies.

A technological advantage is worthwhile because it protects margins and the business franchise. One of our investment themes is that technology is increasingly to be found everywhere and as a key source of competitive advantage, is not just in semiconductors or circuits, but also in supply chain logistics, or heavy equipment manufacturing, and resource exploration and extraction. As technology enters more industries we ask why do tech stocks (hardware and software), command a premium P/E multiple?

Technology can fail and be subject to intense competition and regulation. Furthermore the capital investment required by technology companies to stay ahead, can be enormous and single failed product cycles disastrous. Nokia used to be THE dominant mobile handset company but missed a couple of product cycles and is now an ‘also ran’. Before then came Sony which really should have invented the iPod or generic digital portable player, since it had been first with The Walkman. For whatever reason it became side tracked and missed the shift to digital. The list goes on. Companies with such requirements to keep spending exposure should arguably trade at a P/E discount to reflect this risk?

Consequently if you can invest in technology without the high P/E then why wouldn’t you? Such opportunities exist and they exist outside the sector classified as “technology”. Our favourite example would perhaps be Gilead, the bio technology company. This is now our largest holding after a decent rally in the last few months.

Following the Kite acquisition we have looked at what the acquired cancer technology does and it is pretty astounding. Just as clever as placing binary code on a graphics chip and sound card to make a mobile phone – or at least we think so.

Kite, now owned by Gilead, specialises in oncology or cancer treatments. They have produced a new way to fight certain types of aggressive cancers by reprogramming the body’s own auto immune system. CAR-T or Chimeric Antigen Receptors are programmed onto T cells which are taken from the blood of the patient. T cells do the fighting against foreign cells for the body. These receptors are programmed to fight the specific cancer and are consequently a much less traumatic process then radiation, surgery, or chemotherapy which are the other options.

The best analogy we can think of is the training of special police forces to drop into a crowd riot and identify and take away the key agitators. Up until now, the only option has been to isolate and contain the whole crowd and be prepared to arrest everybody and anybody.

Adding to the complexity is the fact that the blood has to be reprogrammed in a laboratory and then taken back to the patient. This has to be done quickly since these cancers are often aggressive. Think of this as supermarkets running logistics to get fresh food from the farm to your table in a few hours or days. And yet supermarket multiples are higher than GILD which trades on a P/E of less than 12x.

CAR-T is applicable in other areas than oncology so Gilead have potentially bought a complete drug delivery system. Currently it is dealing with blood and potentially lymphoma cancers, but tumours in pancreas or liver or auto immune diseases like type 1 diabetes or lupus are potentially treatable and curable with this CAR-T approach.

For all those ESG investors out there it also does some real good since it actually cures people, it isn’t just a treatment. Hence the shrinking market for some of Gilead’s original drugs which cured Hepatitis C.

For certain there are risks, as with any investment. Gilead needs to grow its other drug treatments offshore and incidentally has just won approval in China for its Hepatitis C drug. Additionally, Gilead and Kite won’t be the only pharmaceutical company developing this treatment, and Novartis, a Swiss based company, is already out there with an approved product, but it trades on a multiple of 30x. There will also be an issue with the cost of CAR-T, since treatment is expected to be c.$500k for a one time attempt.

However, we think that buying cutting edge technology on a P/E of 11x is a pretty good price and notwithstanding the challenges with its existing drug pipeline, as well as obtaining US government approval for this therapy, GILD looks to be up with Novartis and ahead of the crowd, and as worthy as Facebook, Apple, and Amazon as being considered a technology leader: at a fraction of the valuation.

Adrian Lemme, analyst with the TAMIM Australian Equity Income portfolio, takes a look at the impending arrival of Amazon and the impact it should have on the Aussie landscape.

Amazon Not Introducing Internet to Australia TAMIM Australian Equity Income – Merlon Capital Partners

Every day it seems the media is reporting how Amazon will destroy Australian retailers. We are under no illusion that Amazon will take market share and reduce the profitability of Australian retailers. It would be foolish to think otherwise given that Amazon grew its North American sales by 25% to US$80b during 2016 and this remarkable growth shows no signs of abating. However, after reviewing key differences between Australia and other markets, we believe the impact of Amazon is being overplayed and continue to see excellent value in the retail sector.

Online retail is maturing

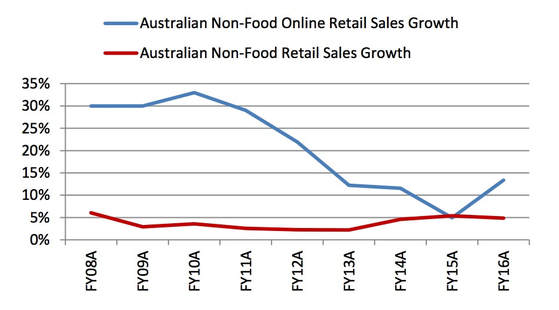

The growth of online retailing in Australia has slowed from around 30% pa up until FY11 to an estimated 13% in FY16 (chart below). In recent months this growth has fallen further to 7-8%. We believe the lower growth in recent years has partly been a function of the lower Australian dollar which has reduced the price incentive to purchase from international online retailers. Nevertheless, we expect Amazon’s expansion and the associated media coverage will see online sales growth accelerate.

Growth in Online Retail Sales (Non-Food) vs Retail Sales (Non-Food)

Source: ABS, NAB, Merlon

Amazon’s Australian entry

It must be recognised that Amazon already has a market presence in Australia through the amazon.com.au site (Kindle) as well as export sales. While not disclosed, market estimates put Amazon’s sales in Australia at between $500 and $700 million. This obviously provides a good launching pad but also means at least initially that sales in Australia will somewhat cannibalise their current sales.

Amazon’s decision to expand in Australia at this time is closely linked to the upcoming introduction of GST for low value imports. Former Amazon executives have told us that until now Australia was considered to have been well serviced by Amazon’s other sites. With the change to the GST threshold, Amazon has lost an important competitive advantage and has therefore taken the view that it needs to establish a local presence to defend and grow its sales here.

Amazon is likely to start with Fulfilment Centres in Brisbane, Sydney and Melbourne. Amazon Prime (as discussed later) will likely commence within two years of entry as per the Mexico experience. Amazon ‘Prime’ memberships will be aggressively marketed following launch by heavily discounting the first year’s annual fee as was done in Italy.

Amazon’s competitive advantage and impact on industry structure

In assessing the impact of Amazon on the Australian retail sector, we draw on our investment process which places significant emphasis on industry structure and competitive advantage. We believe that high returns on capital and hence free cash generation can only be sustained through a combination of favourable industry structure and strong competitive positioning. Through our qualitative scorecard, we explicitly consider Amazon’s impact on industry structure and the competitive advantages enjoyed by the listed retailers.

Amazon will impact the industry structure of Australian retailing by reducing barriers to entry for niche retailers through its third party marketplace. The bargaining power of customers will also increase with increasing price transparency and product choice. On the other hand, it is reasonable to expect further industry consolidation as existing online operators become marginalised and weaker physical retailers exit.

Amazon also clearly possesses competitive advantage across cost, product differentiation and service.

Amazon has a cost advantage by avoiding retail rents and store labour, both of which are high in Australia by global standards. Through its wide range and Amazon Prime, Amazon can fractionalise delivery costs relative to mono-line retailers.

Importantly, we do not believe Amazon will have a sustainable advantage sourcing branded products cheaper than large domestic retailers. Global suppliers will have no choice but to offer equivalent prices to local retailers and domestic warranties will remain important.

With regards to product differentiation, no retailer in the world can match Amazon’s range. Amazon operates in virtually all retail categories including fresh food and its US site is estimated to have approximately 500 million products for sale. It is able to achieve this principally through the use of its third party Marketplace that greatly enhances the range beyond what Amazon could stock alone.

Amazon’s ability to develop intimate relationships with its customers through bundling its offers and convenient fulfilment is perhaps its greatest source of competitive advantage. Through Amazon Prime, US customers qualify for free two day shipping on orders of at least $25 for an annual fee of $99. Amazon is estimated to have 60 million US households signed up to Amazon Prime and is rolling out similar services in other markets. This service is made even more attractive by the bundling of the Prime Video streaming service. Additionally, the Amazon Prime Now service enables free two hour delivery on a range of over 25,000 items. Same day delivery will threaten traditional retail profit pools generated from categories such as high margin accessories.

Retailers with large store footprints will need to compete on in-store experience and service, while utilising store networks for instore ordering and shipping to store for ‘click and collect’.

There is no doubt that the entry of Amazon will diminish the attractiveness of the retail industry structure in Australia and place pressure on incumbent retailers to cut costs, improve their propositions and strengthen their relationships with customers.

Contrasting the overseas experience with Australia

Amazon has been in the US, UK and Canadian markets for well over a decade. We have therefore studied these markets to gain a better understanding of Amazon’s likely impact in Australia.

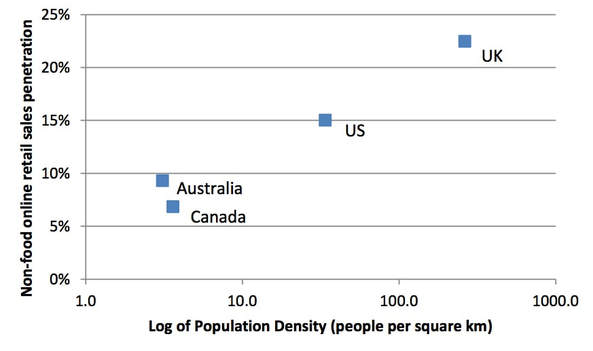

A key observation when comparing these four countries is that the success of not only Amazon, but online retailing in general, is significantly linked to population density:

Non-food online retailer sales penetration vs population density

Source: ABS, NAB, US Census Bureau, UK Office for National Statistics, Statistics Canada, Merlon

As shown by the chart, non-food online retail sales penetration is highest in the UK, which also has the greatest population density. Correspondingly, penetration is lowest in Canada and Australia where density is lowest. Importantly, Canada’s official data excludes international online sales. Given Canada’s close proximity to the US, it is reasonable to assume that Canada’s penetration including international online purchases is in line or slightly above Australia.

This relationship is perfectly logical given that the more dense an area is, the faster and more cost effective it is to fulfil an online order (since there will be many other orders in the same area).

Sceptics will say that Australia is actually very dense on the east coast. But this is no different to Canada which has similar levels of density in its main cities along the southern border to the US.

Linking this back to Amazon, it has clearly struggled in Canada. Amazon entered Canada in 2002, later launching Consumer Electronics in 2008 and remaining categories in 2010. While Amazon does not disclose its Canadian retail sales, we can infer from its segment accounts that it is doing at most US$2b of sales (excluding third parties) out of a total Canadian retail market of US$320b. This pales in comparison to Amazon’s US retail sales of approximately US$78b. Even adjusting for lower population, Amazon has not been nearly as successful in Canada as it has been in the US and has admitted as such.

US sales tax arbitrage helped in the early years

Sales tax is an important feature of Amazon’s US experience that will not be replicated in Australia. For many years, Amazon enjoyed an enormous free kick because it was not required to collect state and local sales taxes in states where it did not have a physical presence (for example, a fulfilment centre). For example, in 2011 it only levied these taxes on sales from five states. This gave it a distinct price advantage over its store based competitors where state and local government taxes can quickly add 7-10%. Today, Amazon collects sales tax in all 45 states with a sales tax regime but this was mostly addressed only this year. At this point it’s a non-issue in the US given the scale and customer acceptance that Amazon has already achieved. Clearly though, Amazon’s growth in Australia will not benefit from the same circumstances since it will be required to collect the 10% GST from day one.

Convenience of delivery will be another challenge for Amazon. Missed deliveries will either incur a costly redelivery or force the customer to collect from the Post Office, Courier Depot or other pick-up point. This is a much poorer customer experience than very dense US cities like New York, where some customers can simply collect their delivery from their doorman as they return home.

Impact on retail sector stocks

Given Australia’s similarities to Canada and differences to the US, we expect it will take longer than many expect for Amazon to have a meaningful impact on the Australian market. Nevertheless, Australian retailers will lose share and endure margin pressure as Amazon expands, but the extent will vary by category and competitive position of individual retailers.

Established pure play online retailers will be among those first impacted. Clearly, eBay will be challenged since it is most comparable to Amazon domestically (particularly with respect to Amazon’s Marketplace). In the US, Amazon dwarfs eBay and we therefore expect Amazon will eventually overtake eBay here.

In terms of individual retail categories, Amazon’s success will be linked to the extent of service and importance, or lack thereof, of in-store experience. Amazon does best in categories that have products with low service requirements and that are easy to ship in a box. While there is very little sales mix data available for Amazon, it is true to say that its market shares are highest in Media, Electrical, Sports and general merchandise. On the flip side, it has very low share in large whitegoods (approximately 1% in the US), furniture, Auto and grocery.

From this perspective, we also see Department stores as being significantly impacted by Amazon’s entry. In the US, this category has been contracting for the last 10 years with store closures now accelerating. Of particular note is Kmart, which has very high margins and very low prices. Ironically, these low prices make the shipping cost far more significant and will be at high risk once Amazon Prime launches with free one or two day delivery.

In-store experience needs to improve and costs need to come down

One of Amazon CEO Jeff Bezos’s famous quotes is “Your margin is my opportunity”.

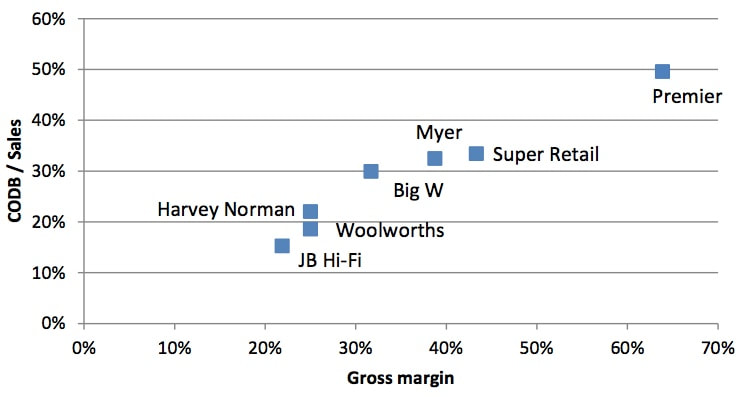

On a stock level, we consider the retailers at most risk from Amazon are those that exhibit both high levels of gross margin selling commodity products and high costs of doing business (CODB). Retailers with these characteristics may very well find their lunch cut by Amazon through its low price strategy and low operating costs. Given this, we have plotted a subset of Australian retail stocks using these two metrics:

Australian retailer gross margins and CODB / Sales

Source: Company Reports, Merlon

JB H-Fi is well positioned to compete with Amazon given it has both a very low gross margin and low operating costs (which is partly a function of its very high sales per square metre). On the other hand, retailers such as Super Retail, Myer and Big W face more challenges because both their gross margins and cost bases are substantially higher than Amazon’s (which we estimate has a retail gross margin of 22-25% and a retail CODB / sales of approximately 15-20% of sales). While Premier stands out as most exposed on these metrics, it sells its own products not available elsewhere. Furthermore, its Smiggle and Peter Alexander brands are particularly differentiated in the marketplace.

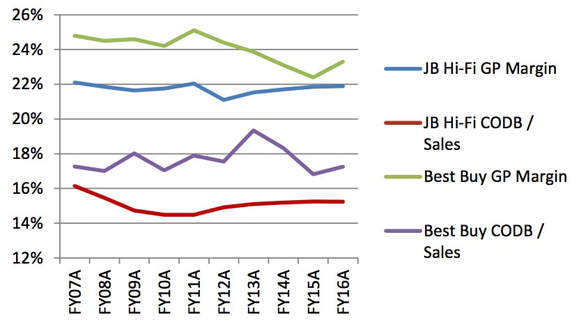

We have also compared JB Hi-Fi and Harvey Norman to offshore electrical market retailers Best Buy (US) and Dixons Carphone (UK). From this, we expect that JB Hi-Fi and Harvey Norman can each hold sales and earn reasonable margins after a period of adjustment given the experience of both Best Buy and Dixons Carphone. For example, Best Buy took a hit to profitability in 2013 but started with a higher gross margin and CODB / Sales than JB Hi-Fi has currently, meaning that JB Hi-Fi is comparatively better positioned (below). In any case, Best Buy’s margin has since largely recovered.

JB Hi-Fi EBITDA Margin Composition vs Best Buy

Source: Company Reports, Merlon

Underscoring JB Hi-Fi’s low gross margin, our sampling of prices by electrical category suggests that the differential in pricing on Amazon’s US website to JB Hi-Fi (when adjusting for GST and currency) is minimal aside from a few categories such as Accessories, Headphones and AV receivers. In the case of the latter two categories, we believe this is mostly a function of suppliers charging more here because they can but we expect these suppliers will be forced to adjust their pricing to better reflect US prices.

From a category perspective, while Amazon is the number two player in US electronics, JB Hi-Fi’s recent acquisition of The Good Guys and Harvey Norman’s exposure to whitegoods and furniture (approximately 40% of sales) should offer some insulation given Amazon’s miniscule (1%) US Appliances (Kitchen/Laundry) share. We also expect both JB Hi-Fi and Harvey Norman to benefit from further consolidation, with Department stores most likely to exit this category as well as smaller, sub scale electrical players. In any case, Harvey Norman’s international businesses and conservatively valued commercial property portfolio will also act to buffer any impact from Amazon on its Australian franchise operations.

With regard to Supermarkets, Amazon’s recent acquisition of Whole Foods in the US is evidence that Amazon Fresh will be a premium rather than price-led proposition. This supports our view that bricks and mortar is critical to any omni-channel strategy and plays into the strengths of Woolworths and Coles. Amazon has been dabbling in physical retailing since 2015 although to date focused on bookstores and showcasing its own gadgets.

Finally, we believe that retail Real Estate Investment Trusts (REITs) will need to reduce rents over time to enable retailers to better compete with Amazon. Clearly, a specialty retailer with rental expense representing 25% or more of sales will struggle to be able to match the pricing of Amazon whose total costs to sales is below that. While the market has started to price this into retail REITs such as Scentre Group, we believe it is still not fully priced in.

A lot is already factored in

Our investment philosophy is built around the notion that companies undervalued on the basis of sustainable free cash flow and franking will outperform over time. That said we also believe that markets are mostly efficient and that cheap stocks are always cheap for a reason. It follows that we are focused on understanding why cheap stocks are cheap. To be a good investment, market concerns need to be already priced into the current share price or deemed invalid. We incorporate these aspects with a “conviction score” that feeds into our portfolio construction framework.

As discussed above, our qualitative scorecard provides a vantage point from which to consider Amazon’s impact on the retail industry structure and the competitive advantages enjoyed by incumbent players. This qualitative assessment weighs into our projected growth rates and sustainable cash flow estimates for the retail stocks that we cover. For JB Hi-Fi and Harvey Norman we have modestly trimmed our estimates of sustainable free cash flow in recent months on the basis that their growth and margins will be impacted by Amazon but on balance think that they will still remain strong, viable businesses.

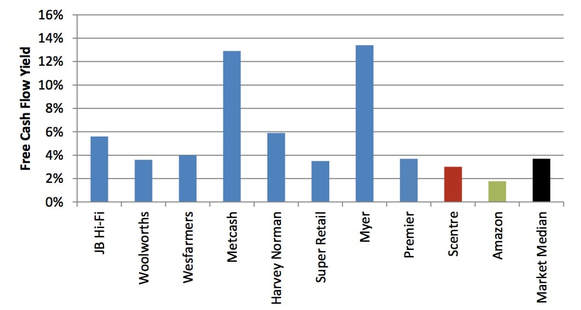

It follows that we believe the market has become overly pessimistic. Since 4 November 2016 when Amazon’s expansion was first speculated in the press to 30 June 2017, discretionary retailers such as JB Hi-Fi, Harvey Norman, Super Retail and Myer have underperformed the ASX200 by between 23% and 36% resulting in relatively high free cash flow yields (Figure 9). The supermarket stocks have understandably held up better given their strong grocery businesses and Wesfarmers’ diversification in Hardware and Coal etc.

Last reported free cash flow yields

Source: Company reports, Merlon

Rather than the entry of Amazon, we view elevated housing prices and highly indebted consumers as the most significant issues facing the listed retailers. As we have discussed previously, we think house prices are modestly overvalued but not to the extent many commentators suggest. Further, household savings rates are historically high and balance sheets historically strong which somewhat tempers our concerns.

Note: The portfolio underlying the TAMIM Australian Equity Income IMA retains positions in Harvey Norman, JB Hi-Fi, Wesfarmers, Woolworths and Metcash but has no exposure to retail REITs, Super Retail or Myer at the time of publication.

Guy Carson takes a look at the series of booms that have been propping up the Australian economy over the last decade and where we might be headed from here.

Australia has just celebrated 26 years without a recession and the Government as well as the Reserve Bank of Australia (RBA) are cheering the ongoing growth. In fact, the common consensus amongst these authorities is that growth is set to rebound from its current 1.9% year on year rate and wages are set to rise as well. There were some encouraging signs in the latest GDP release, most notably the increase in public fixed asset spending (infrastructure), however when we step and take a longer term view things aren’t so rosy.

GDP growth over the last decade has averaged 2.5% per annum; this is the weakest ten year average since the 1990 recession. On a per capita basis the story gets worse, Real GDP per capita has averaged just 0.9% over the last 10 years, the weakest since Malcolm Fraser was Prime Minister. In other words, outside of an increased population through record immigration, the Australian economy is barely growing. As a result of this weak growth, wages have stalled and households are becoming vulnerable. It becomes increasingly clear to us that Australia has joined the rest of the developed world in “Secular Stagnation”.

“Secular Stagnation” is a term originally used by Alvin Hansen back in 1938 and more recently popularised by noted economist Larry Summers. The theory is that four major factors are weighing on growth, inflation and hence interest rates. These factors are deleveraging, demographics, wealth transfer and technological advance. Whilst Australia is currently fighting the demographic trend through record immigration, it is the prospect of deleveraging that has most observers worried.

Deleveraging is the consequence of high debt levels globally at the household, corporate and government level. Debt has risen steadily since the 1980s as interest rates have fallen. If we look back to the start of that period, it marked an important transition. The manufacturing base of the world started to shift from West to East and the rise of the Chinese economy started. As a response to slowing economic growth Central Banks in the developed world began to cut interest rates. Over the period since, every time the global economy appeared to stall, interest rates were cut by 4-5% in order to stimulate growth and never fully recovered to their previous peak. The developed world shifted to a consumer driven services economy.

Source: Thomson Reuters

By definition, the ability of consumers to purchase goods and services is equal to their income plus the net amount of debt they take on (or pay off). As interest rates decreased, households took on more debt and boosted the economy. The problem with this model is twofold, for increasing economic growth rates the amount of debt taken on in the next period has to be more than the previous period and secondly households (unlike governments) have a limit to how much they can borrow. Most of the developed world discovered that limit in 2008 whilst Australian households have continued to lever up, albeit it at a slower rate recently. The problem the RBA has now is the closer you get to zero, the less impact interest rate cuts are likely to have. In addition they have been quite vocal around the record levels of household debt, indicating they are unlikely to cut interest rates further.

It is quite extraordinary that the Australian economy has managed to avoid a recession in the wake of the mining boom. One of the key drivers has been the residential property market and in particular the construction boom. This boom started was spurred on by the RBA cutting interest rates from 4.75% to 1.5%. By cutting interest rates, they boosted property prices and that flowed through to construction. Whilst people tend to focus on those property prices in Melbourne and Sydney, for GDP and Employment it’s the volume of construction that matters. Leading indicators of residential construction started to point down late last year (particularly in Brisbane) and this driver of growth is likely to subside. Currently it appears the slowdown will be gradual but it is important to keep an eye on the key indicators to see if the decline does accelerate. Additionally whilst the national slowdown may be gradual, there will be pockets that experience a hard landing.

This period for Australia is very similar to early 2000s in the US where the Federal Reserve cut interest rates from 6.5% to 1% in response to the mild recession caused by the Tech Wreck. This kick-started property prices and led to a residential construction boom which of course didn’t end so well. During that time, Australia had a significant advantage over the rest of the world with the dawn of the mining boom. This meant that when a shock came along the RBA and the Government had significantly more firepower than the rest of the world. Fast forward to today and the RBA has used up most of its bullets. On the other side, one of the benefits of the property boom has been a vast improvement in the fiscal condition of both the New South Wales and Victorian governments due to record Stamp Duty payments. The chart below which looks at the debt balance of the NSW government and the rate which they plan to spend it over the coming years.

Source: NSW Government 2017/18 Budget

With this improvement, these governments have started on an infrastructure spending spree.

One side effect of low interest rates is that cheap money tends to lead to speculative investment and this in turn leads to booms and busts. As a result bubbles have become increasingly common around the world, whether it was the tech bubble in the late 1990s or the multiple property bubbles in 2007. Australia appears to be following that route with a series of rolling booms from resources to property to infrastructure, all without being able to find stable “trend” growth. So what this means for your Australian equity portfolio? Stocks exposed to the booms will see peaks and troughs; mining and mining stocks have seen it and are now through the worst. Residential property, consumer and finance stocks now look vulnerable despite recent record profits. On the other hand companies exposed to infrastructure construction are starting to see work in hand increase. Cimic’s share price has hit its highest level since 2010 and at the smaller end of town, a number of contractors are reporting record order books.