This week’s TAMIM Reading List explores power, progress and perception across markets, cities and culture. We begin with the newly released Forbes 400, highlighting shifts among America’s wealthiest, while Philadelphia marks a milestone by no longer ranking as the nation’s poorest big city. Jaguar Land Rover’s cybersecurity breach exposes the fragility of digital supply chains, and the story of Thomas Peterffy traces the origins of modern market making. We examine changes to Australia’s Home Guarantee Scheme, test-drive the fastest car ever on Australian roads, and close with a sharp reflection on the fading art of deep thinking in today’s distracted world.

As investors, we are often told to focus on the long term. But what happens when the long term collides with the present? That is exactly what we are seeing in the world of digital infrastructure, specifically data centres, the modern-day engine rooms of the internet. Their insatiable appetite for power, cooling, and connectivity is quietly reshaping the global investment landscape.

Behind every click, stream, chatbot, AI model, or Zoom call, there is a server somewhere, whirring away in a climate-controlled warehouse. And that server wants power, a lot of it. It also wants reliable fibre connections, physical security, backup systems, and increasingly, proximity to renewable energy. This convergence of demand and complexity is turning data centres into one of the most compelling, misunderstood, and urgent investment stories of the next decade.

Let us unpack what is happening and what it means for your portfolio.

The Rise and Rise of AI Infrastructure

For all the hype about AI, and much of it is warranted, one unsexy truth continues to underpin its trajectory. Infrastructure eats ambition for breakfast.

Generative AI tools like ChatGPT or image-generation models might seem magical, but their magic depends on compute power, storage capacity, and high-speed data flow. And the demands are growing at a geometric pace. Microsoft, Amazon, Google, Meta, and others are collectively pouring hundreds of billions of dollars into building, renting, or upgrading the data centre capacity needed to support AI workloads.

Why is this so intense?

AI workloads consume far more energy and bandwidth than traditional computing.

Training a large language model can take weeks on thousands of GPUs, demanding huge electricity loads and cooling.

Inference, or using a model, requires lower but still consistent power, creating sustained demand at scale.

The shift toward AI as a service is embedding these workloads into nearly every vertical, from banking to retail to healthcare.

This dynamic has caught policymakers, regulators, and energy providers off guard. Many believed digital demand would level out. They were wrong.

Electricity, the New Bottleneck

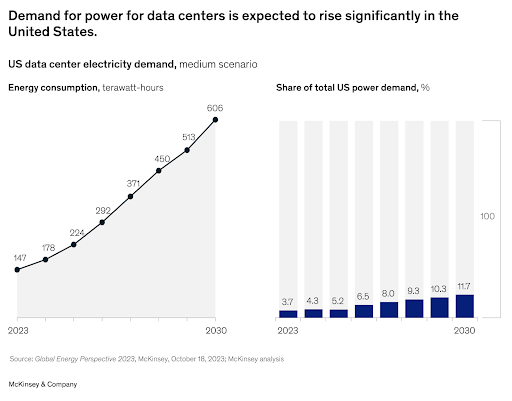

According to industry estimates, data centres already consume around 2 to 3 percent of global electricity. In some jurisdictions, it is far higher. Dublin and Northern Virginia have become cautionary tales of what happens when power demand outstrips grid capacity.

In Japan, new data centre builds around Tokyo are being paused due to grid constraints. In Singapore, moratoriums on new data centres have been imposed due to land and energy shortages. In Australia, power availability is already determining which locations can support new development.

If you think this is a niche problem, think again. The U.S. Energy Information Administration now predicts that electricity demand from data centres could double by 2030. And that may still be conservative if AI adoption continues to accelerate.

What does that mean?

New data centres will increasingly be co-located with energy infrastructure, hydro, solar, nuclear, or even geothermal.

Energy-intensive workloads may migrate toward regions with abundant and cheap power, such as Norway, Canada, and parts of the U.S. Midwest.

Legacy grids, such as Australia’s, will come under pressure to modernise rapidly, or risk missing the AI and cloud transformation entirely.

From Warehouses to Mission-Critical Assets

It is tempting to think of data centres as just real estate, a bunch of warehouses filled with blinking lights. But this view is outdated.

Modern data centres are complex and high-specification infrastructure assets with characteristics more akin to airports or toll roads than commercial offices. They require:

Redundant power and cooling systems

Connectivity to multiple fibre routes

High physical and cyber security

Uptime guarantees of 99.999 percent or higher

Ongoing hardware replacement and upgrades

Tenants, typically cloud providers, government departments, banks, and increasingly AI labs, sign long-term leases with significant upfront commitments. This makes revenue streams predictable, sticky, and well suited to long-duration capital.

Here is where it gets interesting. The capital intensity of building Tier 3 or Tier 4 data centres is rising, while the pool of capable developers is shrinking. That creates a supply and demand mismatch, and an opportunity for investors who know where to look.

The Investment Angle, Infrastructure, Energy, and Edge

We believe that data centre-related infrastructure now deserves a permanent place in the modern investor’s playbook. But it is not just about REITs or hyperscalers. There are several angles to consider.

The Energy Infrastructure Play

As data centre growth collides with grid limitations, companies building the underlying energy infrastructure, from transmission lines to battery storage to small modular nuclear, stand to benefit.

In the U.S., listed infrastructure names like Quanta Services and NextEra Energy have been standout performers. In Japan, we have identified nuclear utility plays with latent capacity that may see data centre co-location demand over the coming decade.

In Australia, we are watching the battle between rising power bills and net-zero targets. Data centre demand could become the tipping point that drives overdue grid investment and possibly unlocks stalled nuclear discussions.

The Edge Computing and Interconnect Opportunity

Not all data has to be processed in giant hyperscale centres. Increasingly, low-latency applications, such as autonomous vehicles, gaming, and AR or VR, require edge data centres, smaller facilities located closer to end-users.

This creates a new layer of infrastructure need, including micro data centres, 5G towers, and fibre routes. Companies operating in this space, or supplying the networking equipment, stand to ride a second wave of digitisation.

The Australian Angle

While much of the action is global, Australia is far from immune.

NextDC and Macquarie Technology are two ASX-listed data centre operators with exposure to this theme. Both are investing heavily in new capacity, including facilities in Sydney, Melbourne, and even regional hubs like Darwin.

Rising power prices, local planning restrictions, and energy availability are shaping expansion plans.

As global AI firms look for sovereign hosting options outside the U.S. and China, Australia could become a key secondary node, if the energy challenge can be solved.

We are also seeing more capital interest from superannuation funds, infrastructure investors, and global private equity targeting Australian digital infrastructure.

Risks and Headwinds

No thematic is without its risks. For data centres, the key ones include:

Energy cost volatility, which can crush margins for operators with exposure to utility prices.

Overbuild risk, where speculative building may outpace demand, especially if AI enthusiasm cools or model training becomes more efficient.

Regulatory backlash, with community opposition, water use concerns, and environmental scrutiny possibly delaying or derailing new builds.

Technological disruption, as advances in chip design or model compression could reduce compute needs per task.

That said, we believe these are risks to manage, not reasons to avoid the space entirely.

The Big Picture, Infrastructure 2.0

We have written extensively at Tamim about the evolving definition of infrastructure. It is no longer just roads, bridges, and rail. In today’s world, infrastructure includes:

Cloud infrastructure

Energy grids

Semiconductor supply chains

Secure data and compute capacity

Data centres sit at the heart of this transformation. They are simultaneously physical assets, enablers of innovation, and geopolitical chess pieces.

In a world where AI, remote work, cloud services, and digital sovereignty are colliding, data centres are quietly becoming the most important buildings on earth.

The TAMIM Takeaway

As investors, we do not chase hype, but we do follow the infrastructure. The digital world needs a physical backbone, and data centres are its vertebrae. While the headlines may focus on Nvidia chips and LLM benchmarks, the real leverage may lie in the quiet and concrete boxes that power them.

Investing in the data centre thematic is about more than server racks. It is about:

Power grids

Cooling systems

Network fibre

Land use

Cloud migration

Sovereign infrastructure

And it is a long game. As with ports, airports, or toll roads, the value accrues over years, not quarters. The current moment, where AI demand is exploding, energy grids are stressed, and capital is still relatively accessible, may represent a unique window to position for the decade ahead.

In our view, the digital industrial age has arrived. And just like the railroads of old, those who own the tracks may reap the greatest rewards.

In a market dominated by headlines around megacaps, rate speculation, and geopolitical volatility, it’s easy for investors to miss the quiet achievers, the companies that execute relentlessly, build shareholder value, and fly under the radar. These are the kinds of businesses that reward patient, valuation-driven investors over time, often with the added kicker of a takeover premium when the broader market finally catches on.

Today, we revisit three such ASX-listed names that have been on our 2025 takeover watchlist. Each of these companies, Pioneer Credit (PNC), Edu Holdings (EDU), and ReadyTech (RDY), is quietly executing on its business model, delivering improving fundamentals, and in our view, marching steadily toward a higher valuation. The market may be just waking up, but for long-term investors, the opportunity is already at the table.

1. Pioneer Credit (ASX: PNC) From Periphery to Preferred, The Big Four’s Debt Partner of Choice

Pioneer Credit, once considered a peripheral player in Australia’s receivables management space, is rapidly emerging as a core partner for Australia’s major banks. The company specialises in acquiring and servicing portfolios of written-off consumer debt, with a particular emphasis on personal and unsecured loans. This is a sector often misunderstood by investors due to legacy reputational concerns, but behind the curtain, PNC operates with discipline, transparency, and strong counterparty relationships.

The company’s FY25 results were impressive across all metrics:

Net Profit After Tax: $10.5 million, exceeding guidance by 17%

Cash collections: $142.2 million, up from $140.5 million in FY24

EBITDA: $94 million, versus $88.7 million the year prior

PDP (Purchased Debt Portfolio) assets increased by $20 million

Net assets grew 37% to $60.6 million

Undrawn facilities of $34.3 million provide further balance sheet flexibility

What excites us most is Pioneer’s strategic positioning with the big four banks. The company is now seen as a “preferred partner” in purchasing and servicing debt portfolios, with Westpac already initiating new sales of PDPs to PNC. These relationships are notoriously difficult to secure and, once cemented, tend to be long-lasting. That creates a high degree of visibility in revenue and collections going forward.

Looking ahead, PNC is guiding for more than $18 million NPAT in FY26, which implies 40% earnings growth. With the stock trading on a forward PE of just 7x, we believe there is material room for re-rating, particularly if a dividend is reinstated, as management has hinted. The business is scalable, asset-light, and already profitable. The market has yet to price this in.

We believe PNC represents a textbook example of a misunderstood business that has restructured, refocused, and now stands ready to deliver value, either via continued market performance or as a logical M&A target for larger financial services players or private equity suitors.

2. Edu Holdings (ASX: EDU) Demographic Tailwinds and the Education-as-a-Service Model

Edu Holdings operates in a sector that is fast becoming a structural growth theme in Australia, vocational and higher education for international students. Through its two core subsidiaries, Australian Learning Group (ALG) and the Ikon Institute, EDU provides accredited courses in healthcare, community services, and mental health. These are not “soft” degrees. They are highly employable qualifications in sectors facing chronic labour shortages.

First-half FY25 results made the market sit up and take notice:

Revenue up 114% to $36 million

NPAT of $6.3 million (versus breakeven the prior period)

Total student enrolments hit 5,300, with 4,800 being international

While recent government rhetoric around international student caps has created some headline risk for the education sector, the reality is more nuanced. EDU’s student base is high-quality, often progressing into employment and permanent residency. These are the students Australia wants to retain. Healthcare and aged care, in particular, are in urgent need of skilled labour, and EDU’s qualifications directly align with these needs.

The company continues to invest in expanding course offerings, including new programs in tech and digital skills, while also considering strategic acquisitions in the higher ed space. Importantly, EDU has just paid its first dividend, a clear sign that profitability and capital discipline are now front of mind.

The valuation remains extremely modest, with the company still trading at a single-digit multiple of FY26 NPAT based on our internal projections. The kicker, every additional $1 in revenue is estimated to drop at least 30 cents to the bottom line, thanks to operating leverage in the model.

With directors buying on market and a buyback underway, EDU’s capital management signals confidence. We also think it’s only a matter of time before EDU attracts the interest of a larger education conglomerate or private equity firm. Scalable, profitable, and with a moat built on regulatory accreditation and student outcomes, EDU is ticking all the boxes.

3. ReadyTech (ASX: RDY) The “Picks and Shovels” of the Digital Government Transformation

ReadyTech is a SaaS business that doesn’t just talk about digital transformation, it delivers it across mission-critical government and institutional systems. The company provides cloud-native platforms for education providers, local councils, workforce agencies, and justice departments, sectors typically underserved by large global vendors.

FY25 wasn’t perfect, organic growth slowed a little, but the company has reset expectations and FY26 is shaping up as a return to form.

Here is what we like:

Signed its first university client, expanding its presence in higher education

Cloud migration for 200 plus local council ERP clients is underway

Workforce Solutions segment is growing fast, serving retail, hospitality and logistics

Strong AI roadmap with seven feature launches expected in FY26

Sales pipeline of $33 million, with approximately half in education and higher ed

The strategy is clear, deepen penetration in education and local government, upsell cloud upgrades and modules, and maintain a low churn profile. In other words, sticky revenue, long-term contracts, and increasing ARPU. The company’s recurring revenue model provides strong visibility.

Management has flagged FY27 as a key year for converting pipeline into revenue, particularly as public tenders in education accelerate. Their university pipeline is robust and under-penetrated, while local councils remain ripe for modernisation.

Despite the upside, RDY is trading on just 10x FY27 Cash EBITDA. This is too cheap for a business with net revenue retention north of 100 percent, a sticky government customer base, and strong operating leverage.

Add to this the fact that SaaS multiples globally have been recovering and that RDY’s client base is shielded from discretionary consumer cycles, and we believe RDY is not just undervalued, it is vulnerable. The stock sits squarely in the crosshairs of both strategic acquirers and private equity.

Why These Three Now?

When we talk about takeover candidates, it is not just about spotting a low PE or a recovering share price. It is about identifying businesses that possess the DNA of long-term winners, but which are mispriced due to market inefficiency, temporary issues, or simple neglect.

Each of these companies, PNC, EDU, RDY, fits that mold:

Founder-led or aligned management teams

Clear pathways to profitability or margin expansion

Strong balance sheets with cash optionality

Sector tailwinds with structural demand

Capital management underway

Valuations below intrinsic or replacement value

In today’s environment, where private capital is cashed up and listed equity valuations still lag, we expect strategic buyers to become more active. These types of businesses are precisely what acquirers look for, growing, cashflow-generative, and with low capex requirements.

The TAMIM Takeaway

In a market that often pays too much attention to narratives and not enough to numbers, investors would do well to look beyond the usual suspects. Pioneer Credit, Edu Holdings, and ReadyTech are all at inflection points, not just in terms of earnings, but in how the market perceives them.

These are not moonshots. They are disciplined, founder-led, profitable or about to be, businesses that we believe have significant upside, whether through fundamental rerating or strategic interest.

At TAMIM, we spend our time looking for exactly these types of opportunities. Companies that are being overlooked, underappreciated, and mispriced, but that will not stay that way for long.

Disclosure: Pioneer Credit (ASX: PNC), Edu Holdings (ASX: EDU) and ReadyTech (ASX: RDY) are held in TAMIM Portfolios as at date of article publication. Holdings can change substantially at any given time.

The Federal Reserve is preparing to cut interest rates for the first time since December 2024, signaling a major shift in monetary policy. With inflation still above target and labour market indicators flashing recessionary warnings, investors are facing a paradox: monetary easing in the face of economic fragility and market exuberance. In this article we try to distill recent macroeconomic data, market trends, and fiscal developments into a strategic guide for investors navigating the months ahead.

The Fed’s Pivot, Rate Cuts Amid Inflation

The Fed is expected to lower the federal funds rate by 25 basis points to 4.00–4.25%, with markets pricing in three cuts by year-end and three more in 2026, potentially bringing rates down to 2.88%, slightly below the Fed’s long-run target of 3%.

This pivot is driven by:

Dovish signals from recent policy meetings,

Bond market expectations showing a 96% probability of a cut,

Historical consistency in Fed actions aligning with market pricing.

Investor insight: Rate cuts typically boost risk assets, but cutting into rising inflation (CPI at 2.9%) is historically rare. The last time this occurred was in October 2008, during a deep recession. Today’s environment is different, with unemployment at 4.3% and the S&P 500 at all-time highs.

The current CPI trend is 11.6% above the 2% inflation path,

The Fed’s decision to cut rates suggests a prioritisation of employment over price stability.

Investor insight: Inflation erodes purchasing power and compresses real returns. While rate cuts may stimulate growth, they risk reigniting inflationary pressures, especially if fiscal and corporate spending remain elevated.

Labour Market, Cracks Beneath the Surface

US Labour market data reveals:

Unemployed persons now exceed job openings for the first time in four years,

Payroll growth has slowed to less than 1% year-over-year, the weakest since March 2021,

June saw a net job loss of 13,000, ending a 53-month streak of positive payrolls,

The BLS revised job creation down by 911,000, the largest downward revision on record,

Youth unemployment (ages 20 to 24) hit 9.4%, over 5% above the national average.

Historically, a 0.9% rise in unemployment from cycle lows has preceded recessions by an average of three months. That threshold was reached in August 2025.

Investor insight: Labour market weakness is a leading indicator of economic downturns. Defensive positioning and quality stock selection become critical in late-cycle environments.

Fiscal Stimulus, Borrowing Without Brakes

Despite labour market fragility, the U.S. government continues aggressive fiscal spending:

$1.9 trillion deficit over the past year,

National debt surged by $1.3 trillion in just three months post-debt ceiling raise,

Interest expense on debt hit $1.21 trillion, now exceeding defense spending.

This fiscal expansion is short-term stimulative but long-term unsustainable. It props up asset prices and consumer demand, but risks crowding out private investment and fueling inflation.

Investor insight: Fiscal tailwinds may support markets in the near term, but rising debt and interest costs could lead to volatility and policy constraints down the road.

AI Boom, Corporate CapEx Explosion

Tech giants are investing heavily in AI infrastructure:

Meta: +408% CapEx growth over five years,

Amazon: +331%,

Alphabet: +316%,

Microsoft: +260%.

Combined, these firms are projected to spend $369 billion on CapEx in the next 12 months, four times more than five years ago.

Investor insight: AI is not just hype, it’s driving real capital allocation. Investors should consider exposure to companies leading in AI infrastructure, cloud computing, and data analytics.

Market Euphoria, All-Time Highs Across the Board

Despite macro concerns, markets are euphoric:

S&P 500 crossed 6,600, with 25 all-time highs in 2025,

Nasdaq hit 22,000, doubling in five years,

Dow reached 46,000, marking 13 consecutive years of record highs,

Every major asset class is positive year-to-date, a rare occurrence last seen in 2019.

Gold is up 40% year-to-date, on pace for its best year since 1979. Over the last 20 years, gold and U.S. stocks have returned the same: +658%, though with vastly different volatility profiles.

Investor insight: Easy money fuels asset bubbles. While momentum is strong, investors should remain vigilant about valuation risks and potential corrections.

Structural Challenges, Education and Trade Deficits

Beyond markets, structural issues loom:

Reading and math scores for U.S. seniors are at record lows, with only 35% proficient in reading and 22% in math,

Trade deficit up 31% year-over-year, reflecting persistent imbalances.

These trends suggest long-term headwinds to productivity and competitiveness.

Investor insight: Structural weaknesses may not impact short-term returns but could shape long-term growth trajectories. Diversification into global markets and innovation-driven sectors is prudent.

The TAMIM Takeaway

As the Fed prepares to cut rates into a backdrop of elevated inflation, slowing job growth, and euphoric markets, investors must balance optimism with caution. The data paints a picture of short-term stimulus and long-term uncertainty.

Here’s what smart investors should consider:

Diversify across asset classes. With every major asset class in the green, now is the time to rebalance, not chase.

Focus on quality and resilience. Companies with strong balance sheets, pricing power, and consistent cash flow will outperform in volatile conditions.

Watch inflation and labour trends. These are the Fed’s compass. If inflation reaccelerates or unemployment spikes, policy could shift again.

Lean into innovation. AI-driven CapEx is reshaping the economy. Exposure to infrastructure and enablers of this transformation is key.

Prepare for volatility. The S&P 500’s average intra-year drawdown is -14%. Risk is the price of return.

The TAMIM Takeaway is clear: stay agile, stay informed, and invest with discipline.

In markets, the spotlight often shines brightest on the dazzling names, the tech giants, the disruptive start-ups, the firms that seem to exist in permanent hyper-growth. Yet investors who spend all their time chasing glamour risk overlooking the real enablers of global transformation. These are the companies that may look “boring” on the surface, classified as industrials, or peripherals, or auto parts suppliers, but in reality they sit at the centre of structural shifts reshaping economies.

At Tamim, we often refer to this as the “In Rust We Trust” mindset, a belief that industrial and enabling businesses, though less glamorous, can generate exceptional returns when positioned correctly. This week we highlight three such companies from our Global High Conviction portfolio: Evonik Industries, Logitech International, and Magna International. Each is exposed to powerful global themes, urbanisation and energy renewal, digital adoption and gaming, and the evolution of mobility. Together, they show how conviction in overlooked sectors can generate both resilience and upside.

Evonik: Chemicals, Nutrition, and the European Dilemma

Evonik Industries, listed in Frankfurt, is one of the world’s leading specialty chemical companies. With operations spanning specialty additives, nutrition and care, smart materials, and infrastructure services, it might be pigeonholed as another cyclical European chemical stock. But Evonik is far more than that.

At the heart of its business lies animal nutrition, particularly methionine, a key amino acid supplement used in poultry and livestock farming. This is a structurally growing market, protein consumption continues to rise across Asia, and farmers worldwide are increasingly reliant on high-quality supplements to improve efficiency and sustainability. Evonik is one of the dominant suppliers in this niche, with a product range that includes MetAMINO, the benchmark methionine brand for global animal farming. This business is not cyclical fashion, it is critical infrastructure for the global food chain.

Still, near-term challenges remain. The European economy has slowed, weighing on Evonik’s revenue base. In FY25, total revenue slipped from €16.3 billion to €16.0 billion, with EBITDA down from €2.1 billion to €1.8 billion. Yet net income turned sharply positive at €461 million, thanks to efficiency gains and cost control. Here lies the first key point for investors: Evonik is structurally efficient. Cost-cutting and what one might call “Teutonic discipline” mean that when revenue growth returns, incremental gains will drop through to the bottom line at higher margins than before.

The second point is income resilience. Evonik currently offers a dividend yield above 7%, backed by a stable balance sheet and conservative capital management. In a world where bond yields fluctuate and equity markets remain volatile, that yield provides both downside protection and investor patience.

The third point is strategic optionality. Europe’s energy policy, particularly Germany’s, remains conflicted. The heavy tilt towards renewables without sufficient baseload capacity has exposed industries like chemicals to high and volatile energy costs. But any adjustment, a recognition that nuclear or alternative energy sources must form part of the mix, would disproportionately benefit companies like Evonik. In other words, Evonik provides investors with a kind of “backside coverage” on a European policy U-turn. If policy improves, the company wins. If it does not, larger peers with greater energy exposure will suffer even more, leaving Evonik relatively advantaged.

Finally, Evonik’s local-for-local production strategy is a hidden strength. By producing close to end markets, it minimises exposure to global trade frictions, tariffs, or supply chain disruptions. In an era of fragmentation and reshoring, this model becomes more valuable. Expansion into Asia-Pacific remains on the agenda, promising further diversification away from Europe.

Evonik may never capture headlines in the same way as a software darling, but it remains a case study in why “boring” can be brilliant, a resilient dividend payer, a market leader in animal nutrition, and a call option on Europe’s energy sanity.

Logitech: Picks and Shovels for the Digital Age

If Evonik epitomises industrial resilience, Logitech represents the quiet power of “picks and shovels” in the digital age. Headquartered in Switzerland, Logitech designs and sells peripherals: keyboards, mice, headsets, webcams, speakers, and gaming gear. Hardly the stuff of investor dreams, some might think. After all, how exciting can keyboards really be?

Quite exciting, as it turns out. Logitech sits at the intersection of several powerful trends: the gaming boom, the rise of streaming and digital content, and the hybrid work revolution. When Nvidia sells a graphics card, the gamer who buys it almost always purchases complementary hardware, a high-quality headset, a responsive mouse, a mechanical keyboard. In many ways, Logitech’s business is the necessary add-on to the GPU cycle. You can think of it as a leveraged play on the gaming and AI ecosystem without paying Nvidia multiples.

Financially, the company remains robust. FY25 revenues rose to $4.6 billion, with EBITDA holding at $759 million. Net cash sits at $1.4 billion, providing a fortress balance sheet. Margins have compressed somewhat as competition in peripherals remains intense, but free cash flow remains strong, enabling dividends and share buybacks. Indeed, Logitech has a track record of returning capital to shareholders while maintaining investment in innovation.

Importantly, the company is not just selling “dumb” hardware. Increasingly, Logitech integrates software-enabled features, AI-powered optimisation, and cloud-linked services into its products. For enterprise clients, Logitech’s video conferencing equipment, ConferenceCams, controllers, webcams, has become a key enabler of hybrid work. In the gaming space, its Logitech G line continues to dominate esports and streaming, while acquisitions like Loupedeck add to its ecosystem for creators.

Valuation is not cheap, forward P/E sits around 25x, but for a company with this balance sheet strength, market positioning, and exposure to structural growth, we see it as justified. More importantly, Logitech represents an investment where the product cycle is not a question of “if” but “when.” Hybrid work, digital content creation, and gaming are not fads, they are embedded in the modern economy.

In short, Logitech embodies the Tamim principle of looking past the obvious. Investors who chase Nvidia may win or lose depending on GPU cycles, but those who hold Logitech capture the durable, everyday monetisation of that cycle, the keyboards, cameras, and headsets that make the ecosystem work.

Magna International: The Tech in Car Parts

If Logitech is about digital picks and shovels, Magna International is about rethinking what a “car parts” supplier really is. Based in Canada, Magna is the largest auto supplier in North America and the third largest globally. With over 280,000 employees worldwide and operations spanning body structures, seating, vision systems, and powertrains, it is a behemoth of the automotive industry. Yet calling Magna a simple “parts supplier” misses the point.

The auto industry is in flux. Electric vehicles grab headlines, but adoption is uneven, infrastructure lags, and consumers remain cautious. Internal combustion engines remain dominant in many markets, particularly in developing economies. Hybrids, offering lower emissions and fuel savings without range anxiety, are increasingly emerging as the pragmatic middle ground. This is where Magna shines.

The company’s hybrid drivetrain technology, particularly its six-gear systems and clutch modules, offers automakers a best-in-class solution for hybrid vehicles. Unlike some suppliers betting entirely on EVs, Magna has positioned itself as the bridge technology provider, supporting ICE, hybrid, and EV platforms. This diversified exposure reduces risk while giving it leverage to whichever powertrain dominates the next decade.

Financially, Magna remains solid. FY25 net income rose to $1.2 billion despite a slight dip in revenue to $41.6 billion. EBITDA increased to $3.9 billion, reflecting cost control and operational efficiency. The company pays a dividend yield above 4% and trades on less than 9x forward earnings, compelling for a business with global scale and exposure to growth segments. Recent contract wins, including vehicle assembly partnerships with XPENG, reinforce its relevance in next-generation mobility.

Beyond hybrids, Magna is also active in eDrive systems, battery enclosures, and autonomous vehicle components such as cameras, radar, and interior sensing. In effect, it is a stealth technology company embedded within the auto supply chain. Investors may see “car parts,” but the reality is sensors, drive systems, and assembly expertise at the cutting edge of mobility.

Magna demonstrates why we look for misunderstood exposures. The narrative may focus on Tesla and BYD, but the enablers, the companies that provide the drivetrain, the seats, the chassis, are often better value, more diversified, and just as exposed to mobility’s future.

Conclusion: Conviction in the Overlooked

Taken together, Evonik, Logitech, and Magna reflect a consistent Tamim philosophy: finding value and resilience in companies that are not always obvious market darlings but sit at the heart of structural change. Evonik shows how chemicals and animal nutrition can deliver both yield and upside in an evolving Europe. Logitech highlights how peripherals can be the indispensable tools of gaming, streaming, and hybrid work. Magna illustrates how the largest auto parts supplier can in fact be a stealth technology play on hybrids and mobility transformation.

Each faces headwinds. Evonik grapples with Europe’s energy malaise. Logitech competes in a commoditised peripherals market. Magna contends with auto industry cyclicality and trade tensions. But each also carries strong balance sheets, shareholder returns, and exposure to secular trends.

For investors, the lesson is clear: not all opportunity is found where the headlines shine. Sometimes, conviction means looking at the so-called boring names and realising they are the backbone of transformation.

Tamim Takeaway

The world is changing, and so are the enablers. Whether in the amino acids that feed the food chain, the peripherals that connect us to digital worlds, or the hybrid drivetrains that bridge mobility’s future, opportunity lies in companies that quietly make the system work. At Tamim, we invest with conviction in these overlooked but essential businesses, confident that in time, the market will catch up to the value they deliver.

Disclaimer:Evonik Industries AG (XTRA: EVK), Logitech International S.A. (SWX: LOGN) and Magna International Inc. (TSX: MG) are held in TAMIM Portfolios as at date of article publication. Holdings can change substantially at any given time.

Pioneer Credit, once considered a peripheral player in Australia’s receivables management space, is rapidly emerging as a core partner for Australia’s major banks. The company specialises in acquiring and servicing portfolios of written-off consumer debt, with a particular emphasis on personal and unsecured loans. This is a sector often misunderstood by investors due to legacy reputational concerns, but behind the curtain, PNC operates with discipline, transparency, and strong counterparty relationships.

Pioneer Credit, once considered a peripheral player in Australia’s receivables management space, is rapidly emerging as a core partner for Australia’s major banks. The company specialises in acquiring and servicing portfolios of written-off consumer debt, with a particular emphasis on personal and unsecured loans. This is a sector often misunderstood by investors due to legacy reputational concerns, but behind the curtain, PNC operates with discipline, transparency, and strong counterparty relationships. Edu Holdings operates in a sector that is fast becoming a structural growth theme in Australia, vocational and higher education for international students. Through its two core subsidiaries, Australian Learning Group (ALG) and the Ikon Institute, EDU provides accredited courses in healthcare, community services, and mental health. These are not “soft” degrees. They are highly employable qualifications in sectors facing chronic labour shortages.

Edu Holdings operates in a sector that is fast becoming a structural growth theme in Australia, vocational and higher education for international students. Through its two core subsidiaries, Australian Learning Group (ALG) and the Ikon Institute, EDU provides accredited courses in healthcare, community services, and mental health. These are not “soft” degrees. They are highly employable qualifications in sectors facing chronic labour shortages.

Evonik Industries, listed in Frankfurt, is one of the world’s leading specialty chemical companies. With operations spanning specialty additives, nutrition and care, smart materials, and infrastructure services, it might be pigeonholed as another cyclical European chemical stock. But Evonik is far more than that.

Evonik Industries, listed in Frankfurt, is one of the world’s leading specialty chemical companies. With operations spanning specialty additives, nutrition and care, smart materials, and infrastructure services, it might be pigeonholed as another cyclical European chemical stock. But Evonik is far more than that.