MP Materials (MP.NYSE)

![]()

The Rare Earth Elements:

Scandium, Yttrium, Lanthanum, Cerium, Praseodymium, Neodymium, Promethium, Samarium, Europium, Gadolinium, Terbium, Dysprosium, Holmium, Erbium, Thulium, Ytterbium, Lutetium

MP currently produces ~15% of the global supply of rare earths, currently in the form of an intermediate product — rare earth concentrate — that requires further processing in Asia. It currently sells its output to China-based, and 8% shareholder, Shenghe Resources for further processing but this is subject to change once MP implements their upcoming expansion strategies at the Mountain Pass mine. The company plans to reinvest the free cash flow generated from operations into expanding MP’s US capabilities, including restoration of domestic refining capability at Mountain Pass by next year. MP Materials will relaunch its onsite processing facilities, setting the foundation for a renewed, self-sufficient US rare earth industry. MP Materials shares have more than trebled since listing on the New York Stock Exchange in November 2020.

Rare Earth Elements

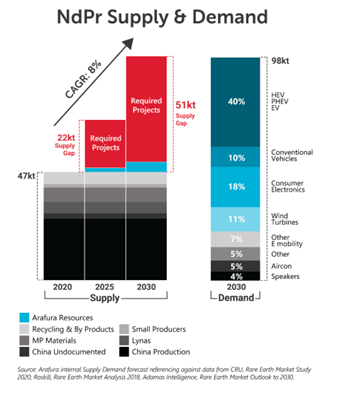

Rare earth elements are far more abundant than their name suggests but extracting, processing and refining the metals poses a range of technical, political and environmental issues. Most of the rare earth deposits are found along with radioactive materials that contribute to ecosystem disruption and release hazardous byproducts into the atmosphere. As a result, it is often difficult to receive the necessary environmental approvals to develop a rare earths mine. Environmental regulations are often more stringent than inside China which is why the country dominates the rare earth industry, producing over 80% of global supply as mentioned.

Electric Vehicles

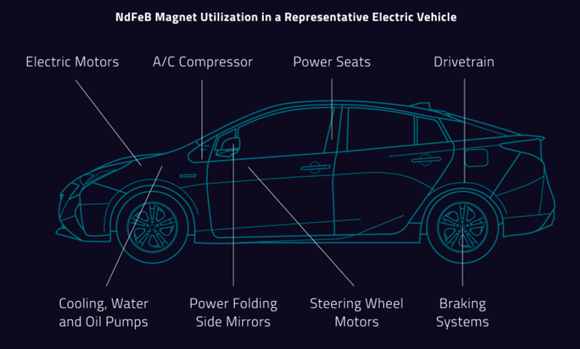

With electric vehicles being one of the three pillars of our Global Mobility fund (along with autonomy and sharing/connectivity), we look for companies that will benefit from the imminent growth in electric vehicle production by participating in the ecosystem that is being built around the industry. While the US intends to shift away from China to source their rare earth supply, without domestic production this would have a significant effect on American consumers as domestic demand for batteries and electric vehicles ramps up. The pace of demand growth is expected to rise rapidly over the next few years as sales of electric vehicles are slated to reach 12.2m in 2025, according to data from IHS Markit.

” The wind turbine market is anticipated to account for ~30% of the global growth in the use of rare earth magnets from 2015-2025. Using rare earth metals prevents the use of gearbox. Rare earth magnets make the turbines lighter, cheaper, more reliable, easier to maintain and capable of generating electricity at lower wind speeds.”

Stage II + III Strategy

As it currently stands, all of MP’s rare earth production requires further processing in Asia, something that the US is clearly anxious about. Following the acquisition of the Mountain Pass mine in 2017, the mine’s production is approximately 3.2x greater than the highest ever production in a twelve-month period by the former operator using the same capital equipment. That was the first stage of MP’s strategy. The second stage of MP’s Mountain Pass strategy will see MP Materials relaunch its onsite processing facilities, setting the foundation for a renewed and self-sufficient US rare earth industry. This would mean that MP Materials no longer has to send their product for further processing in Asia, they will now be able to sell their concentrate to end users which will have a huge cost-benefit. MP is aiming to finish their second stage in 2022. Stage III would be downstream integration, to be completed via either building a captive integrated magnet supply chain or investing in this capability via an acquisition, partnership or joint venture. The integration of magnet production would establish MP as the first and only fully-integrated source of supply for rare earth magnets in the Western Hemisphere. In addition to offering end-market magnet customers a complete Western supply chain solution, MP believe downstream integration would also create a material incremental value creation opportunity.

Outlook & Thesis

We see MP Materials as a company with multiple tailwinds moving forward. The shift toward a self-sustained supply chain in the US will obviously have a favourable outcome for US rare earths miners and provide further support for future projects. The demand side for rare earths is looking strong with electric vehicle production ramping up as well as other applications in things like electronics and wind turbines. Looking over at the supply side, due to the radioactive material that is usually found with rare earths, these mines are hard to bring into production so our outlook for the price of these elements is very strong. The completion of MP’s Stage II plans will be a major catalyst for the company, it will make them the only US company that can provide a rare earth end product to consumers. This will not only be cost-effective but will give them sizable leverage when negotiating off take agreements with US consumers.

MP are currently sitting on over US$1.1bn in cash, enabling them to execute their strategy at the Mountain Pass mine while also allowing them the opportunity to make further acquisitions or JV agreements, further increasing their production and presence in the future. In their last quarterly announcement, MP had an underlying EBITDA of 64%. Considering the cost benefits of their Stage II implementation and their increased bargaining power in terms of off take agreements, MP is sitting on a highly profitable mine. MP Materials is another company in TAMIM’s Global Mobility portfolio that will benefit from the shift towards decarbonisation through electric vehicles and clean energy applications. We see MP Materials dominating the rare earths industry in America and they will be the only US based company that has the ability to provide an end product to consumers without relying on Asia.